Connecticut Health Insurance 2026: Access Health CT, Covered CT & Costs

Connecticut health insurance for 2026 centers on Access Health CT, the state’s own exchange that operates independently of HealthCare.gov. Only two carriers participate in 2026 — Anthem Blue Cross Blue Shield and ConnectiCare — offering 22 plans across Bronze, Silver, Gold, and Catastrophic tiers. The Connecticut Insurance Department cut carrier rate requests from an average 23.3 percent to 16.8 percent, and the state added $70 million in subsidies to offset the expiration of enhanced federal credits. Connecticut’s Covered CT program continues to provide $0-premium, $0-cost-sharing Silver coverage for residents up to 175 percent of the federal poverty level, and a new Temporary Premium Assistance program extends partial state subsidies through 2026 for households up to 500 percent FPL. This guide covers the full Connecticut health insurance landscape — Access Health CT enrollment, both carriers, Covered CT, HUSKY Health, costs by income, and when off-marketplace PPO coverage makes more sense for Connecticut health insurance buyers above the subsidy cliff.

Where do you want to start?

How Access Health CT Works in 2026

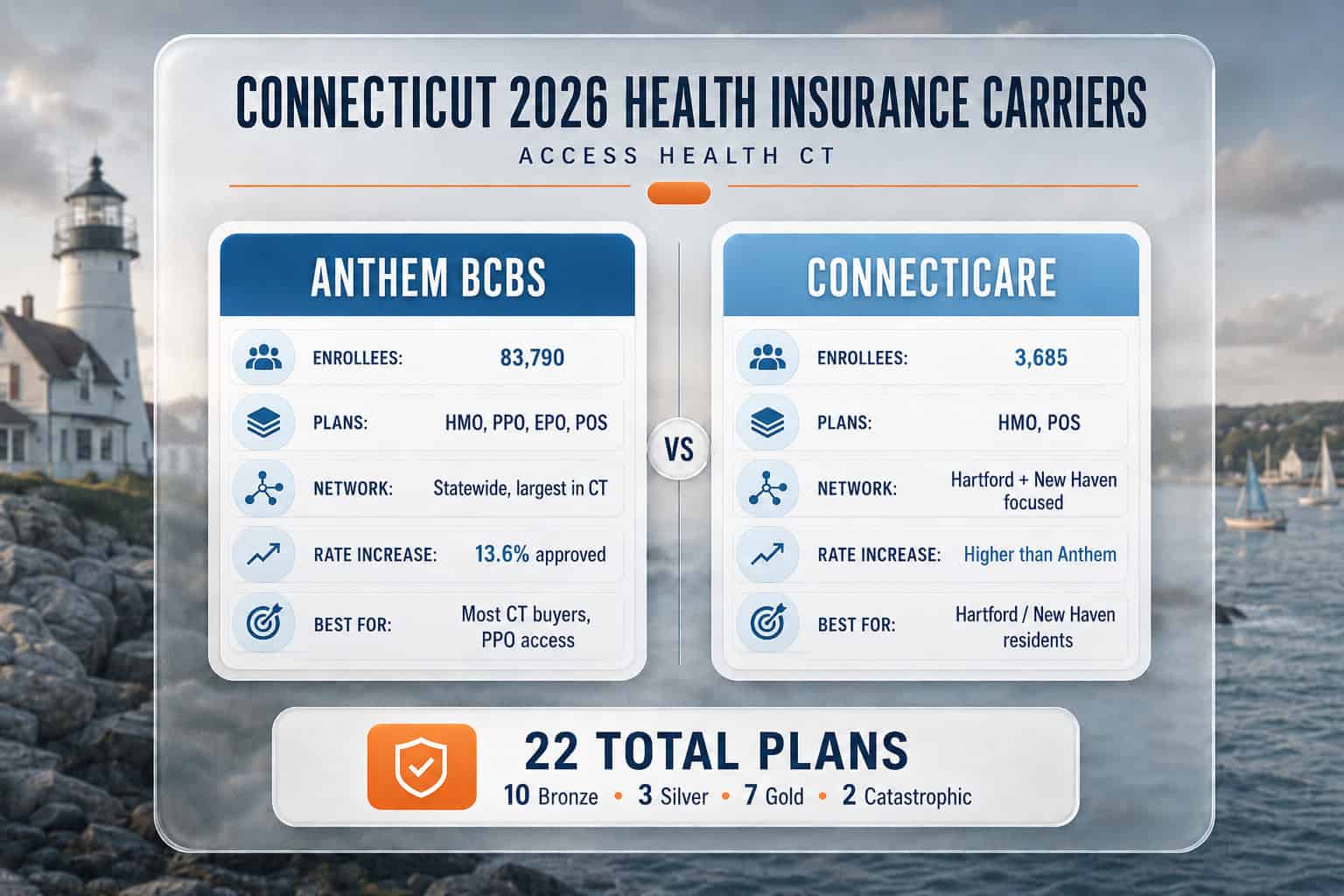

Connecticut operates Access Health CT, its own state-based marketplace, rather than using HealthCare.gov. Connecticut residents enroll at AccessHealthCT.com, the only place where federal premium tax credits, cost-sharing reductions, the Covered Connecticut program, and the new state-funded Temporary Premium Assistance are available. Two carriers offer the full 22-plan lineup for 2026: Anthem Blue Cross Blue Shield with 83,790 enrollees across its broader statewide network, and ConnectiCare with 3,685 enrollees focused on in-state provider networks.

| Feature | Access Health CT (CT State-Based) | HealthCare.gov (Federal) |

|---|---|---|

| Operator | Connecticut state exchange authority | Federal CMS |

| Enrollment site | AccessHealthCT.com | HealthCare.gov |

| 2026 OEP window | Nov 1, 2025 – Jan 31, 2026 (extended) | Nov 1, 2025 – Jan 15, 2026 |

| State subsidy programs | Covered CT + Temporary Premium Assistance | None |

| Carriers for 2026 | Anthem BCBS + ConnectiCare (2 carriers) | Varies by state |

| Plan count for 2026 | 22 plans (10 Bronze, 3 Silver, 7 Gold, 2 Catastrophic) | Varies by state |

Connecticut extended the 2026 open enrollment period to January 31, 2026 — two weeks longer than the standard federal deadline — in response to the enhanced subsidy expiration and new state assistance programs. A Special Enrollment Period for Temporary Premium Assistance ran from February 1, 2026 through June 30, 2026 for residents not already enrolled.

Why Connecticut Premiums Rose 16.8 Percent for 2026

The Connecticut Insurance Department approved an average 16.8 percent rate increase for 2026, cutting carrier requests averaging 23.3 percent. Anthem was approved at 13.6 percent average on 83,790 enrollees, with individual plan ranges from 6.1 percent to 22.5 percent. ConnectiCare sought 26.1 percent (later 34.5 percent) on 3,685 enrollees. Primary drivers were higher emergency department utilization, behavioral health costs, and specialty pharmacy spending — plus the December 31, 2025 expiration of enhanced federal premium tax credits.

| Carrier | Enrollees | Requested Increase | Approved Increase |

|---|---|---|---|

| Anthem BCBS | 83,790 | 14.2% (adj. 18.6%) | 13.6% avg (6.1%–22.5% by plan) |

| ConnectiCare | 3,685 | 26.1% (adj. 34.5%) | Reduced by CID review |

| Statewide average | ~87,000+ | 23.3% | 16.8% |

State offset: Connecticut committed $70 million in 2026 to partially replace the $295 million in federal enhanced subsidies that expired December 31, 2025. The state subsidy fully covers the gap for households earning 100–200 percent FPL and provides 50 percent coverage for households earning 400–500 percent FPL. This is a 2026-only commitment — not guaranteed for 2027.

Covered Connecticut and the 2026 Subsidy Programs

Connecticut offers layered financial assistance programs that make coverage significantly cheaper than sticker prices suggest for most enrollees. About 80 percent of Access Health CT enrollees received premium tax credits in 2026, with average credits of $952 per month and an average net premium of $100 per month. The table below maps income to the applicable assistance program.

| Income (Single Adult, 2026) | % FPL | Program | Effective Cost |

|---|---|---|---|

| Under $22,025 | <138% | HUSKY D (Medicaid expansion) | $0 premium |

| $22,025 – $26,575 | 138%–175% | Covered Connecticut | $0 premium + $0 cost-sharing on Silver |

| $26,575 – $31,920 | 175%–200% | APTC + State Temporary Assistance (100%) | Near $0 after full gap coverage |

| $31,920 – $62,600 | 200%–400% | APTC only (standard federal) | Varies; avg ~$100/mo net |

| $62,600 – $78,250 | 400%–500% | APTC + State Temporary Assistance (50%) | Partially offset; call Access Health CT |

| Above $78,250 | >500% | No subsidy | Full sticker price — off-exchange often better |

Covered Connecticut — the $0 plan: Residents earning up to 175 percent FPL who are not Medicaid-eligible can enroll in a Silver plan through Access Health CT, accept all available federal tax credits, and have the state pay the remaining premium and all cost-sharing. The result is a plan with $0 monthly premium, $0 deductible, $0 copays, and $0 out-of-pocket — effectively the most comprehensive coverage available in Connecticut at no cost. Over 51,629 residents enrolled for 2026, up more than 10,000 from the prior year.

2026 Temporary Premium Assistance — call required: The state subsidy for 100–200 percent FPL and 400–500 percent FPL households was not reflected in Access Health CT’s online enrollment system as of early 2026. To receive the Temporary Premium Assistance, residents must call Access Health CT at 1-855-805-4325. The Special Enrollment Period for this assistance runs through June 30, 2026.

Connecticut’s Two Health Insurance Carriers for 2026

Connecticut has the fewest on-exchange carriers of any state with a functioning marketplace — just two for 2026. Anthem Blue Cross Blue Shield dominates with 83,790 enrollees and the broadest provider network in the state. ConnectiCare, a Connecticut-based carrier, serves 3,685 enrollees with a more concentrated in-state network. Both carriers offer plans across Bronze, Silver, and Gold tiers; Anthem also offers the two Catastrophic plans available on the exchange.

Anthem Blue Cross Blue Shield

95%+ of CT marketEnrollees: 83,790 | Plans: HMO, PPO, EPO, POS

Anthem is the dominant Connecticut carrier by enrollment and network size, operating the largest provider directory in the state including access to Yale New Haven Health, Hartford HealthCare, and Nuvance Health systems. Anthem offers both HMO and PPO products on and off the exchange, making it the primary PPO option for Connecticut buyers who need out-of-network access or specialist care without referrals. The 2026 approved rate increase of 13.6 percent on average was the lowest carrier increase requested in the state.

Best for: Most Connecticut buyers; PPO access; statewide network; Fairfield County to Windham County coverage.

ConnectiCare

In-state focusedEnrollees: 3,685 | Plans: HMO, POS

ConnectiCare is a Connecticut-based carrier focused on in-state provider networks, particularly strong in the Hartford and New Haven metropolitan areas. ConnectiCare Benefits, Inc. administers coverage for Covered Connecticut program enrollees alongside Anthem. POS plans offer limited out-of-network access with referrals. ConnectiCare sought a substantially higher rate increase than Anthem for 2026, reflecting smaller risk pool exposure to the high-cost utilization trends that drove 2026 filings industry-wide in Connecticut.

Best for: Hartford and New Haven metro residents; buyers whose primary care and specialist providers are within the ConnectiCare network.

Compare Anthem and ConnectiCare Plans for 2026

ForHealthInsurance.com shows after-subsidy pricing across both Access Health CT carriers, checks Covered CT and Temporary Assistance eligibility, and compares off-marketplace PPO options — free, licensed, no extra cost.

Get a Quote Call 888-215-4045HUSKY Health — Connecticut Medicaid and CHIP

Connecticut health insurance enrollment and eligibility go through Access Connecticut at access.ct.gov or by calling 1-855-805-4325. Rate filings and consumer complaints route through the Connecticut Insurance Department, which cut the 2026 carrier requests from an average 23.3 percent down to the approved 16.8 percent.

| Program | Covers | Income Limit (2026) | Cost |

|---|---|---|---|

| HUSKY A | Children, parents, caregivers, pregnant women | Varies by category; up to 201% FPL for children | $0 premium for most |

| HUSKY B (CHIP) | Children above HUSKY A income limits | Up to 323% FPL for children | Small premiums possible |

| HUSKY C | Aged, blind, and disabled individuals | Income + asset test applies | $0 premium; spend-down possible |

| HUSKY D | Low-income adults 19–64, no children (ACA expansion) | Up to 138% FPL (~$22,025 single) | $0 premium |

Connecticut Does Not Have a State Health Insurance Mandate

Connecticut does not impose a state individual health insurance mandate. The federal mandate penalty was reduced to $0 effective 2019, and Connecticut — unlike Massachusetts, New Jersey, California, Rhode Island, and Washington DC — has not enacted a replacement. Residents who go without coverage owe no state tax penalty. Connecticut has considered but not passed a mandate over several legislative sessions.

Going uninsured in Connecticut forfeits federal premium tax credits, Covered CT benefits worth thousands of dollars annually for low-income residents, and HUSKY Health eligibility for qualifying adults. It also exposes households to the full cost of any medical care needed during a coverage gap — Connecticut has some of the highest hospital rates in the country, with average emergency department visits running $2,000–$4,000 before insurance adjustments at Yale New Haven Health and Hartford HealthCare systems.

How to Choose Connecticut Coverage for Your Situation

With only two carriers on exchange and layered state subsidy programs that don’t appear in Access Health CT’s online system for 2026, choosing the right Connecticut health insurance requires checking actual eligibility by phone as well as comparing online plan prices. The income-based guide below covers the most common buyer situations.

| If you are… | Best path |

|---|---|

| Single, earning under $22,025 | HUSKY D Medicaid — free, enroll at access.ct.gov |

| Earning $22,025–$26,575 (138–175% FPL) | Covered CT — $0 premium + $0 cost-sharing Silver plan |

| Earning $26,575–$31,920 (175–200% FPL) | APTC + Temporary Assistance — call 1-855-805-4325 |

| Earning $31,920–$62,600 (200–400% FPL) | Access Health CT Gold or Bronze after standard APTC |

| Earning $62,600–$78,250 (400–500% FPL) | APTC + partial state assistance — call to confirm |

| Above $78,250 (500%+ FPL, Stamford/Greenwich corridor) | Off-marketplace PPO — no subsidy, broader network |

| Self-employed in CT | Off-marketplace PPO + HSA if above subsidy cliff |

| Child under 19, family income up to 323% FPL | HUSKY B (CHIP) — low or no cost |

For Connecticut residents above 500 percent FPL — concentrated in Fairfield County, Greenwich, Westport, and the Stamford-New Haven corridor — off-marketplace PPO plans typically offer better value than sticker-priced on-exchange HMOs. See private Connecticut health insurance for off-exchange options, or review the carrier comparison guide for a head-to-head of Anthem and ConnectiCare plans.

Frequently Asked Questions About Connecticut Coverage

What is Access Health CT?

Access Health CT is Connecticut’s official state-based health insurance marketplace, operating independently of HealthCare.gov. Connecticut residents enroll through AccessHealthCT.com — the only place where federal premium tax credits, cost-sharing reductions, the Covered Connecticut program, and state Temporary Premium Assistance are available. Only two carriers participate for 2026: Anthem Blue Cross Blue Shield and ConnectiCare.

What is the Covered Connecticut program?

Covered Connecticut is a state-funded program providing $0 premium and $0 cost-sharing Silver coverage to residents earning up to 175 percent of the federal poverty level — about $26,575 for a single adult in 2026 — who are not eligible for HUSKY Health Medicaid. Enrollees must select a Silver plan through Access Health CT and accept all available federal tax credits. The state pays remaining premiums and all cost-sharing. Over 51,629 residents enrolled for 2026.

Does Connecticut have a state individual mandate?

No. Connecticut does not have a state individual health insurance mandate. The federal penalty was reduced to $0 effective 2019, and Connecticut has not enacted a replacement — unlike Massachusetts, New Jersey, California, Rhode Island, and Washington DC, which impose state penalties. Going without coverage in Connecticut carries no tax penalty but forfeits federal tax credits, Covered CT benefits, and HUSKY Health eligibility.

How much did Connecticut health insurance go up for 2026?

The Connecticut Insurance Department approved an average 16.8 percent rate increase for 2026 — down from the 23.3 percent carriers requested. Anthem was approved at 13.6 percent average on 83,790 enrollees; ConnectiCare received a smaller approval on its 3,685 enrollees. Connecticut offset increases with $70 million in state subsidies, and the average net premium for subsidy-eligible enrollees is approximately $100 per month for 2026.

What is HUSKY Health in Connecticut?

HUSKY Health is Connecticut’s Medicaid and CHIP program in four tiers: HUSKY A covers children, parents, and pregnant women; HUSKY B is CHIP for children above HUSKY A limits (up to 323% FPL); HUSKY C covers aged, blind, and disabled individuals; and HUSKY D covers low-income adults without children (ACA Medicaid expansion, up to 138% FPL). Connecticut is one of only four states nationally running Medicaid on fee-for-service rather than managed care, with administrative costs of about 4.5 percent.

Can I buy Connecticut health insurance outside Access Health CT?

Yes. Connecticut residents can buy ACA-compliant individual plans directly from Anthem or ConnectiCare off the exchange, or from other carriers offering off-marketplace products. Off-marketplace plans carry full ACA protections but do not access federal tax credits, Covered CT, or state Temporary Premium Assistance. They enroll year-round and typically offer broader PPO networks. Off-marketplace coverage makes most sense for buyers above 500 percent FPL with no subsidy eligibility.

Related Connecticut Health Insurance Resources

Explore the cluster guides — small business coverage, affordability, carrier comparisons, the Access Health CT marketplace, and private off-exchange options for Connecticut.

Group plans, the SHOP tax credit, and ICHRA for Connecticut employers.

Affordable Connecticut CoverageHow subsidies and Covered Connecticut lower premiums for those who qualify.

Best Health Insurance in ConnecticutAnthem, ConnectiCare, and Cigna compared on price and provider network.

Connecticut MarketplaceEnrollment windows, deadlines, and subsidies on the Access Health CT marketplace.

CT Private & Off-ExchangeOff-exchange and private plan options for Connecticut residents wanting flexibility.

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required.

Enroll in Connecticut Health Insurance for 2026

Access Health CT, Covered CT, and HUSKY Health combine to give most Connecticut households a coverage path. ForHealthInsurance.com checks eligibility across every program, compares both carriers, and completes enrollment at no extra cost.

Get a Quote Call 888-215-4045Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Connecticut residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.