DC Health Insurance: A Complete 2026 Guide to DC Health Link, Carriers, and Costs

Health insurance in the District of Columbia works differently than in any state. DC operates an all-marketplace individual market through DC Health Link, with only two carriers selling individual plans for 2026 and a longer enrollment window than most of the country. This guide explains how the DC market is structured, what coverage costs in 2026, which carriers are available, how PPO networks reach across DC, Maryland, and Virginia, and when DC residents can enroll.

What brings you to DC health insurance today?

How DC’s Health Insurance Market Works

DC is the only jurisdiction in the country where every individual and small-business health plan is sold through a single exchange. DC Health Link is the District’s exclusive marketplace, operated by the DC Health Benefit Exchange Authority. For 2026, two carriers offer individual coverage on DC Health Link — CareFirst BlueCross BlueShield and Kaiser Permanente — across a total of 27 individual plans.

This all-marketplace structure is unique to DC. In most states, residents can buy ACA-compliant individual coverage either through HealthCare.gov (or a state exchange) or directly from a carrier off-exchange. In DC, off-exchange individual coverage is not available. Every CareFirst and Kaiser individual plan a DC resident can purchase runs through DC Health Link, whether the resident qualifies for subsidies or not. The DC Health Benefit Exchange Authority (HBX) was created by the Health Benefit Exchange Authority Establishment Act of 2011 and consolidated under DC Code §31-3171.04 — the statute that made the District a “no off-exchange” market.

Three carriers participate in the broader DC Health Link system, but only two sell to individuals. UnitedHealthcare offers plans for 2026 exclusively through the DC Health Link Small Business Marketplace, available to employer groups with 1 to 50 employees. Individuals shopping for their own coverage will see CareFirst and Kaiser only. CareFirst contributes both HMO and PPO plans; Kaiser offers HMO coverage. The total individual plan count held steady at 27 for plan year 2026, while small group plans dropped from 171 to 161 across the three SHOP carriers.

Why “DC Health Link” appears everywhere on this page: there is no separate “off-exchange” DC market to talk about. When a DC resident shops for individual health insurance, they shop on DC Health Link. The marketplace name and the District’s individual market are the same thing.

How Much DC Health Insurance Costs in 2026

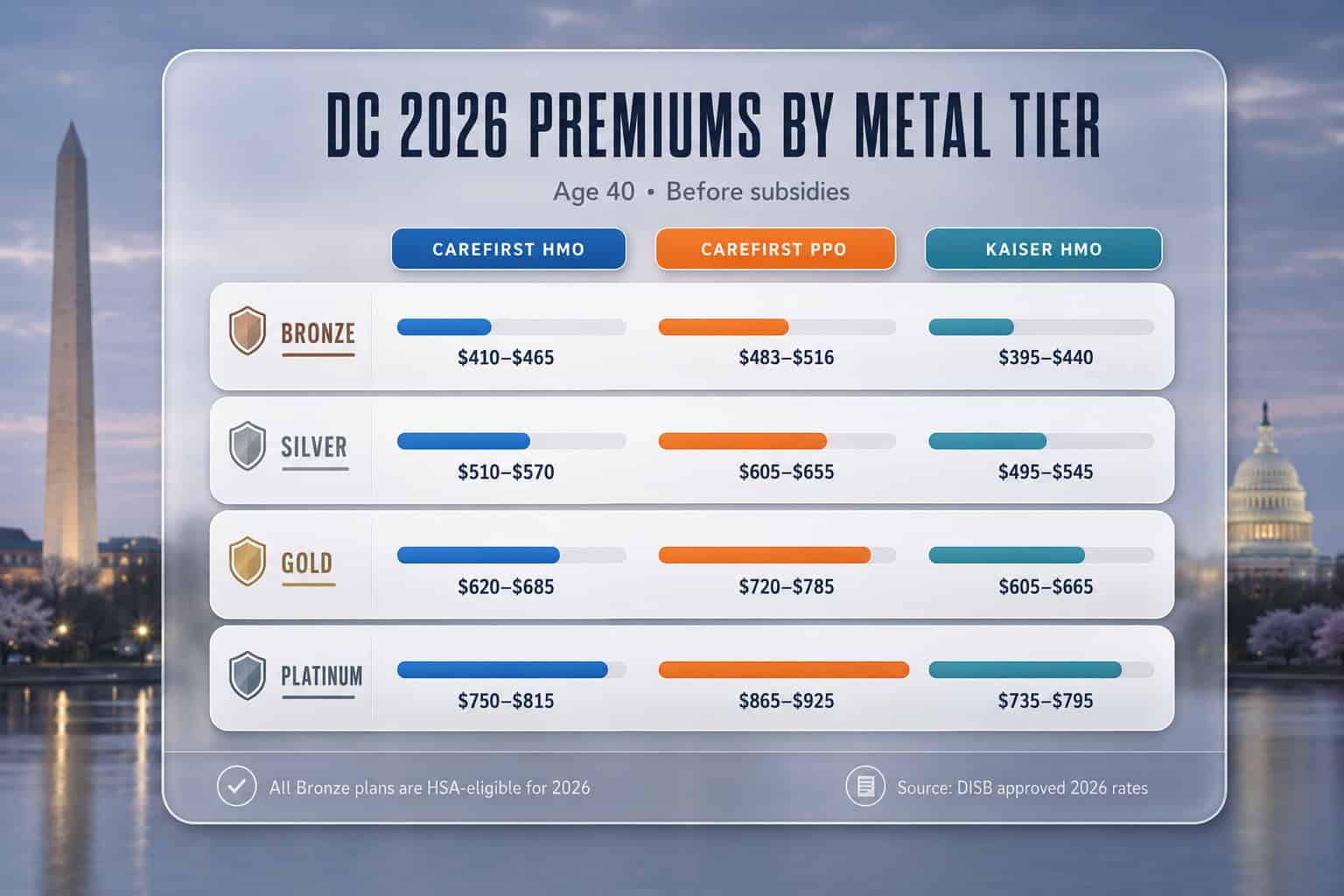

The average individual DC Health Link premium for a 40-year-old is approximately $582 per month in 2026, after the DC Department of Insurance, Securities and Banking (DISB) approved an average increase of 8.7% for individual plans. Premiums vary by age, metal tier, and whether you choose CareFirst HMO, CareFirst PPO, or Kaiser HMO. About 28% of DC Health Link enrollees receive federal premium subsidies, well below the 93% national marketplace average.

The 2026 rates were finalized by DISB on September 29, 2025, after a public hearing where actuaries presented their cases and DC residents shared concerns. The regulator scaled back what the carriers originally requested. CareFirst had proposed 4.1% on HMO plans and 12.6% on PPO plans for individuals; Kaiser had proposed 12.9% across the board. After review, DISB approved a lower weighted average that the agency estimated would save District residents more than $1.2 million in 2026. Small group rates landed at an average 9.5% increase. The drivers, according to DISB rate filings, were higher base-period claims experience, medical inflation, and a lower projected risk adjustment receivable for the combined pool.

Subsidy uptake in DC differs sharply from the national pattern, and it shapes how affordable coverage feels for District residents. According to DC Health Benefit Exchange Authority data, only about 28% of DC Health Link individual enrollees receive federal premium tax credits, compared to roughly 93% of marketplace enrollees nationwide. The gap reflects DC’s higher median household income — federal subsidies phase out faster for higher-income households — and the District’s larger share of enrollees who earn above 400% of the Federal Poverty Level. For DC residents who do qualify, subsidies follow the same federal premium tax credit formula used everywhere else, calculated against the second-lowest-cost Silver plan available on DC Health Link.

Scenario — 35-year-old Capitol Hill resident, $68,000 income:

At $68,000 a year (about 470% of FPL for a single adult in 2026), this resident is above the standard federal subsidy cliff but qualifies under the temporary American Rescue Plan extension structure if Congress renews enhanced subsidies. Without subsidies, a CareFirst Silver HMO at approximately $550/month costs $6,600 per year. With a Kaiser Bronze HMO at $425/month, annual premiums drop to about $5,100 — a $1,500 saving — but with a higher deductible.

PPO vs HMO in DC — Why Network Choice Matters Across State Lines

DC is one of the strongest markets in the country for choosing a PPO over an HMO, because most DC residents routinely see doctors in Maryland and Virginia. CareFirst’s PPO plans use the national Blue Cross Blue Shield network and cover roughly 95% of doctors and 96% of hospitals nationwide — including the major hospital systems in Bethesda, Arlington, and Alexandria. Kaiser HMO members are restricted to Kaiser facilities and the Mid-Atlantic Kaiser network.

The DC metro area’s medical infrastructure is genuinely interstate. A federal worker living in Petworth might see a primary care doctor on H Street, deliver a baby at Sibley Memorial in Northwest DC, and see a specialist at Johns Hopkins Sibley — straightforward in-network with a PPO. The same worker on an HMO plan might find their orthopedist in Bethesda, their cardiologist in Arlington, or their child’s pediatric specialist at Children’s National’s Northern Virginia campus is out of network. For DC residents who already cross the Potomac or the Maryland line for care, the PPO premium difference often pays for itself the first time a specialist visit gets billed in-network instead of out-of-network.

CareFirst BlueChoice PPO

BCBS nationalUses the BCBS national network. No referrals required for specialists. In-network coverage at MedStar Washington Hospital Center, GW Hospital, Howard University Hospital, Sibley Memorial, Johns Hopkins Sibley, and major Bethesda/Arlington systems. Premium runs roughly 15–20% higher than comparable HMO plans.

CareFirst BlueChoice HMO

Mid-tierLower premiums than the PPO. Requires choosing a primary care physician and getting referrals for specialists. Network is concentrated in the DC, MD, and Northern VA region but smaller than the PPO. Best for residents who get all their care locally in DC and don’t expect frequent specialist visits.

Kaiser Permanente HMO

IntegratedCare delivered through Kaiser-owned medical centers and physicians in the Mid-Atlantic region. No referrals between Kaiser specialists. Strong integrated care model with electronic health records across all providers. Limited to Kaiser facilities — care outside Kaiser is only covered for emergencies.

Which fits DC residents best?

If you see doctors in Maryland or Virginia, or want freedom to choose specialists without referrals, a CareFirst PPO is usually the strongest fit. If you prefer one integrated medical home and lower premiums, Kaiser is the lowest-cost path. CareFirst HMO sits between them on both cost and flexibility.

Nationally, the PPO product is ForHealthInsurance.com’s strongest match for residents who value provider flexibility. For a full head-to-head of the two DC carriers — CareFirst versus Kaiser on price, network, and quality — see our guide to the best health insurance in DC. The full national PPO comparison — including how DC’s BCBS PPO compares to PPO options in other markets — is covered on the PPO health insurance plans hub.

Compare DC Health Link Plans for 2026

Free help from licensed agents — no obligation, no extra cost to you.

The DC Health Insurance Carriers for 2026

Two carriers sell individual coverage on DC Health Link for 2026: CareFirst BlueCross BlueShield (HMO and PPO) and Kaiser Permanente (HMO only). A third carrier, UnitedHealthcare, participates in DC Health Link’s Small Business Marketplace (SHOP) for employer groups but does not sell individual coverage. CareFirst dominates the individual market with roughly two-thirds of enrollment; Kaiser holds the remainder.

CareFirst BlueCross BlueShield is the largest health insurer in the DC region by enrollment and is the only individual-market carrier in DC offering a true PPO product. CareFirst markets its individual plans on DC Health Link under the BlueChoice brand, with both HMO and PPO networks. The BCBS national network gives CareFirst PPO members in-network access nearly anywhere in the country — a meaningful advantage for DC’s substantial population of federal workers, lobbyists, and consultants who travel frequently. According to the CMS Marketplace Open Enrollment data, DC’s marketplace enrollment has held steady for plan years 2024 and 2025 with CareFirst capturing the majority of individual enrollment.

Kaiser Permanente operates a closed-network integrated care model in DC, Maryland, and Northern Virginia. Kaiser members receive care at Kaiser-owned medical centers from Kaiser-employed physicians, with electronic medical records shared across all providers. Kaiser’s monthly premiums in DC are typically the lowest available at the Bronze and Silver tiers, and its quality ratings on DC Health Link are consistently among the highest in the market for 2026 plan year coverage.

CareFirst BlueCross BlueShield

HMO + PPOPlans on DC Health Link: CareFirst BlueChoice HMO, CareFirst BlueChoice PPO, CareFirst BlueChoice HSA Bronze, CareFirst BlueChoice Plus

Network type: HMO + PPO (only individual PPO in DC)

Service area: All of DC plus the Maryland and Virginia BlueChoice region

Best for: Residents who see providers in Maryland or Virginia, want PPO flexibility, or need access to the BCBS national network for travel

Kaiser Permanente

HMO onlyPlans on DC Health Link: Kaiser Permanente DC Bronze, Silver, Gold, Platinum HMO; Kaiser DC HSA-Qualified Bronze

Network type: HMO only (closed Kaiser network)

Service area: DC and Kaiser’s Mid-Atlantic region

Best for: Residents who want one integrated medical home, lower premiums, and don’t need providers outside the Kaiser system

UnitedHealthcare

SHOP onlyPlans on DC Health Link: Choice Plus, Core Essential, OCI HMO — SHOP only

Network type: PPO, EPO, HMO (depending on plan)

Service area: DC small business employer groups, 1 to 50 employees

Best for: DC small businesses offering group coverage — not available for individuals shopping their own coverage

How carrier choice plays out

For most DC individuals, the practical decision is CareFirst PPO vs. Kaiser HMO. CareFirst HMO sits as a middle option. A licensed agent can compare specific plans against your providers, prescriptions, and budget — most of the work involves checking whether your existing doctors are in each carrier’s network.

Subsidies, Healthy DC, and Affordable Coverage Paths

DC offers three affordability paths for residents who can’t pay full premium: federal premium tax credits through DC Health Link (used by about 28% of DC enrollees), DC Medicaid for very-low-income residents (administered by the DC Department of Health Care Finance), and the new Healthy DC Plan launching for 2026 — a no-monthly-premium, no-cost-at-care option for qualified DC residents announced on the DC Health Link landing page for the 2026 plan year.

The federal premium tax credit works the same in DC as in every other ACA market. Eligibility is calculated against the second-lowest-cost Silver plan available to you on DC Health Link, with subsidies sized so that benchmark Silver coverage costs a defined percentage of your income. DC’s relatively high median income means more enrollees fall above the standard subsidy ranges than in most states, which is why the 28% subsidy uptake on DC Health Link sits well below the 93% national marketplace average reported in KFF’s State Exchange Profile for DC.

DC Medicaid covers adults up to 215% of the Federal Poverty Level — one of the most generous Medicaid expansion thresholds in the country. The DC Department of Health Care Finance administers Medicaid through District Direct (the consolidated benefits portal at districtdirect.dc.gov), and three managed care organizations deliver care: AmeriHealth Caritas DC, CareFirst Community Health Plan DC, and MedStar Family Choice. Residents who qualify for DC Medicaid will be routed to it during DC Health Link enrollment automatically based on income. For the federal premium tax credit, household income is reported on IRS Form 8962 at tax time to reconcile the advance credit against actual income.

The Healthy DC Plan — new for 2026: DC Health Link introduced the Healthy DC Plan for the 2026 plan year, described on the DC Health Link homepage as quality coverage with no monthly payments and no costs when you get care. Eligibility is income-based and limited to DC residents. The plan is administered through DC Health Link alongside marketplace and Medicaid coverage.

When and How to Enroll in DC Coverage

DC’s annual open enrollment for 2026 plan year coverage on DC Health Link runs November 1, 2025 through January 31, 2026 — a window two weeks longer than the federal HealthCare.gov window, which ends January 15. DC also recognizes pregnancy as a qualifying life event, opening a Special Enrollment Period that most states do not offer. Coverage starts January 1 for plans selected by December 15.

The longer DC enrollment window matters most for residents who miss the December 15 effective-date deadline. A DC resident who enrolls on January 20 still gets coverage starting February 1 — in most states, that same enrollment would be locked out entirely. DC’s longer window reflects the District’s status as a state-based marketplace operating under the Affordable Care Act’s flexibility for SBM jurisdictions to extend enrollment periods beyond federal defaults.

Special Enrollment Periods open DC Health Link outside the annual window for qualifying life events. DC recognizes the standard federal qualifying events — loss of other coverage, marriage, birth or adoption, moving to DC, and income changes affecting subsidy eligibility — plus pregnancy. DC is one of a small group of U.S. jurisdictions (including New York, New Jersey, Maryland under a 2023 expansion, and a handful of others) where becoming pregnant qualifies as its own SEP trigger, distinct from giving birth. Pregnant DC residents can enroll on DC Health Link at any point during pregnancy with coverage starting the first of the following month.

| Enrollment Path | 2026 Window | Coverage Start |

|---|---|---|

| Open Enrollment — Early | November 1 – December 15, 2025 | January 1, 2026 |

| Open Enrollment — Late | December 16, 2025 – January 31, 2026 | February 1, 2026 (or March 1) |

| SEP — Job loss, move, marriage, birth | 60 days from qualifying event | First of following month |

| SEP — Pregnancy (DC-specific) | Anytime during pregnancy | First of following month |

| DC Medicaid enrollment | Year-round | Same month if approved by 15th |

Enrollment happens at DC Health Link directly, by phone at (855) 532-5465, or with help from a licensed agent. Agents do not charge the consumer — broker compensation is built into the carriers’ filed rates and is identical whether you enroll directly or with assistance.

DC Plan Types, Metal Tiers, and What’s New for 2026

DC Health Link offers the four standard ACA metal tiers — Bronze, Silver, Gold, and Platinum — plus a Catastrophic option for under-30 enrollees and people with hardship exemptions. New for 2026: all Bronze plans on DC Health Link are eligible for a Health Savings Account, expanding tax-advantaged coverage at the lowest premium tier. The Essential Plans option also returned for 2026, covering primary care, specialists, urgent care, and generic prescriptions without a deductible.

Metal tier choice trades monthly premium against out-of-pocket cost when care is used. Bronze plans carry the lowest premiums but the highest deductibles and out-of-pocket maximums — they fit people who expect minimal care during the plan year and want catastrophic protection. Silver plans are the standard middle option and are required to be available with cost-sharing reductions for enrollees between 100% and 250% of the Federal Poverty Level who qualify. Gold and Platinum plans charge higher monthly premiums but pay a higher share of medical bills when care happens — they fit people with chronic conditions, expected procedures, or families with young children.

Bronze

All HSA-eligible 2026Lowest monthly premium. Highest deductible — typically $7,000–$8,500 in DC for 2026. Pairs with a Health Savings Account for tax-advantaged savings on medical expenses. Best for healthy individuals expecting minimal care.

Silver

Subsidy benchmarkStandard middle tier. Deductibles in DC run $4,500–$6,500 for 2026. Cost-sharing reductions cut Silver out-of-pocket exposure for enrollees under 250% FPL. The benchmark for federal subsidy calculations.

Gold and Platinum

Lowest deductibleHighest premiums, lowest deductibles ($1,500–$3,500 for Gold; under $1,000 for Platinum). Best for chronic condition management, planned procedures, or families with frequent care needs.

Essential Plans

Returned 2026A streamlined option covering primary care, specialist visits, urgent care, and generic prescription drugs without requiring you to meet the deductible first. Available across all four metal tiers on DC Health Link.

Frequently Asked Questions About DC Coverage

DC health insurance shoppers ask the same questions repeatedly: who sells plans in DC, can I buy outside DC Health Link, when is open enrollment, what does pregnancy mean for my coverage, why are 2026 rates higher than 2025, and how does the new Healthy DC Plan work. The answers below cover what every DC resident should know before shopping for 2026 coverage on DC Health Link.

How many health insurance carriers sell individual plans in DC?

Two carriers sell individual plans through DC Health Link for 2026: CareFirst BlueCross BlueShield and Kaiser Permanente. UnitedHealthcare participates only in the DC Health Link Small Business Marketplace (SHOP) for employers with 1 to 50 employees, not the individual market.

Can DC residents buy health insurance outside DC Health Link?

No. DC is structured as an all-marketplace individual market. All ACA-compliant individual and family plans are sold exclusively through DC Health Link. Off-exchange individual plans are not available the way they are in most states.

When is open enrollment for DC health insurance in 2026?

Open enrollment for 2026 DC Health Link coverage runs November 1, 2025 through January 31, 2026. DC’s enrollment window is longer than the federal HealthCare.gov window, which ends January 15. Coverage starts January 1 for plans selected by December 15.

Does pregnancy trigger a Special Enrollment Period in DC?

Yes. DC is one of a small group of jurisdictions where becoming pregnant qualifies as a life event that opens a Special Enrollment Period on DC Health Link. In most states, only birth, adoption, or foster placement qualifies. Pregnant DC residents can enroll outside open enrollment.

Why are DC’s 2026 health insurance rates higher than 2025?

DISB approved an average 8.7% increase for individual plans and 9.5% for small group plans for 2026. The regulator reduced what carriers originally proposed, saving DC residents more than $1.2 million. Drivers include higher base-period claims, medical inflation, and lower risk adjustment receivables.

What is the Healthy DC Plan?

Healthy DC is a no-cost health coverage program launching for the 2026 plan year through DC Health Link. Qualified DC residents pay no monthly premium and no cost-sharing when they receive care. Eligibility is income-based and limited to specific DC residency criteria.

DC Health Insurance Resources

Go deeper on the DC market — the DC Health Link marketplace, affordable coverage paths, individual plans for the self-employed, and nationwide PPO coverage.

How DC Health Link works, enrollment windows, deadlines, and subsidies.

Affordable Health Insurance in DCMedicaid, the Healthy DC Plan, and the cheapest CareFirst and Kaiser plans.

Individual Health Insurance in DCDC Health Link coverage for the self-employed, freelancers, and contractors.

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required.

Get DC Health Insurance Help for 2026

Compare CareFirst and Kaiser DC Health Link plans with a licensed agent. No cost to you.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving District of Columbia residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.