Short-Term Health Insurance New Jersey 2026: Mandate Rules, 4-Month Cap & Alternatives

Short-term health insurance in New Jersey carries a risk no other state’s short-term buyers face quite as directly: the NJ individual mandate. Unlike most states where going without ACA coverage means a coverage gap, New Jersey residents who carry only short-term health insurance for any month still owe the Shared Responsibility Payment on their state tax return for those months — because short-term plans do not satisfy the NJ mandate’s minimum essential coverage requirement. This guide covers that critical distinction, the 4-month federal cap that took effect September 2024, and the NJ-specific alternatives that usually serve residents better.

What are you looking for?

The NJ Mandate Problem: Short-Term Doesn’t Count

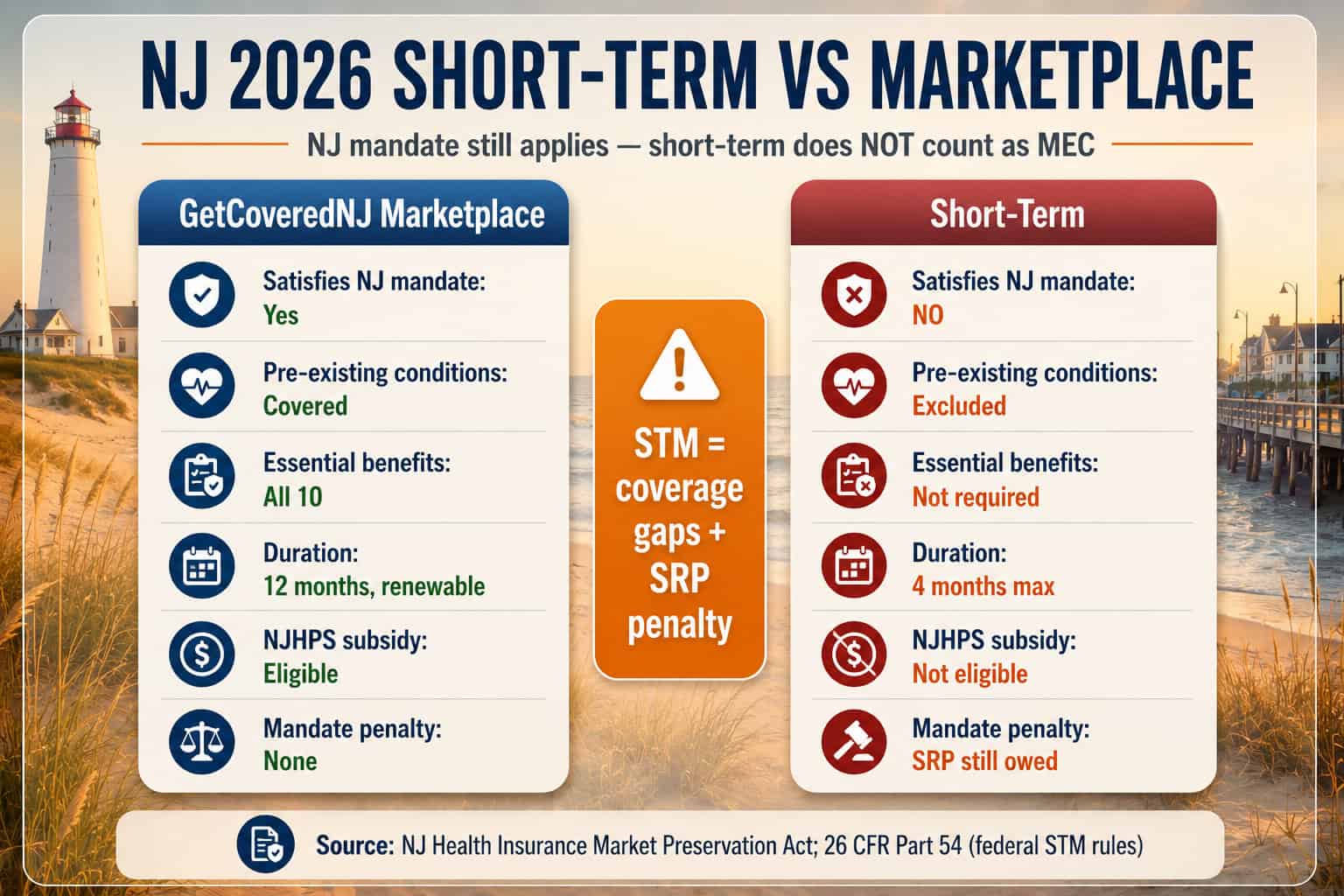

Short-term health insurance in New Jersey creates a financial trap unique to mandate states. NJ’s individual mandate requires minimum essential coverage — and short-term plans are explicitly excluded from MEC. A resident carrying only short-term coverage for January through April owes the Shared Responsibility Payment for each of those months on the NJ-1040, in addition to any costs the short-term plan does not cover due to pre-existing exclusions or benefit caps.

| Coverage Type | Satisfies NJ Mandate | SRP Owed |

|---|---|---|

| GetCoveredNJ marketplace plan | Yes | No |

| Off-exchange ACA-compliant plan | Yes | No |

| Employer-sponsored plan (MEC) | Yes | No |

| NJ FamilyCare / Medicaid | Yes | No |

| Short-term health insurance | No | Yes — SRP still owed |

| No coverage at all | No | Yes — SRP owed |

⚠️ The double-cost trap

A New Jersey resident who purchases short-term health insurance instead of a marketplace plan faces two financial risks simultaneously — the coverage gaps inherent in short-term plans (pre-existing condition exclusions, no essential health benefits, dollar caps) AND the NJ Shared Responsibility Payment for each uninsured month under the mandate. The SRP for a single adult earning $50,000 runs approximately $575 annually under the income-based calculation. Short-term coverage does not reduce this obligation by a single dollar.

Federal Short-Term Rules: The 4-Month Cap

Federal regulations effective September 1, 2024 substantially shortened the maximum duration of short-term health insurance plans. The prior rules allowed initial contracts of up to 364 days with renewals extending to 36 months. The current rules limit initial contracts to 3 months with a maximum 1-month renewal — capping total coverage at 4 months. New Jersey follows the federal cap without additional state restrictions.

| Rule Component | Pre-September 2024 | Current Rules |

|---|---|---|

| Initial contract maximum | 364 days | 3 months |

| Total with renewal | Up to 36 months | 4 months maximum |

| Same-carrier re-issue | Common workaround | Not permitted for same period |

| NJ mandate impact | SRP owed for all months | SRP owed for all months |

The 4-month cap fundamentally changes what short-term coverage is. Under prior rules, a NJ resident could maintain short-term coverage for years — accepting the mandate penalty and pre-existing condition exclusions in exchange for lower premiums. Under current rules, the maximum exposure is 4 months, which aligns short-term coverage to actual gap-bridging use cases: a 6-week job transition, a month before new employer benefits begin, or a brief period before a GetCoveredNJ special enrollment period takes effect.

What Short-Term Plans Cover and Exclude in NJ

Short-term health insurance plans in New Jersey are not required to cover the ACA’s ten essential health benefits. Coverage varies by carrier and plan, but most NJ short-term products share a common exclusion pattern that makes them unsuitable for anyone with ongoing medical needs, prescriptions, or any prior health condition.

| Benefit | ACA Marketplace (GetCoveredNJ) | Typical NJ Short-Term Plan |

|---|---|---|

| Pre-existing conditions | Covered, no exclusions | Excluded (look-back 12–60 months) |

| Maternity care | Required | Typically excluded |

| Mental health/substance use | Required with parity | Limited or excluded |

| Prescription drugs | Required (formulary) | Often excluded or capped |

| Preventive care | No cost-sharing required | Subject to deductible |

| Annual benefit maximum | Prohibited | Common ($250K–$2M) |

| Emergency care | Covered at in-network rates | Covered (usually with high deductible) |

The pre-existing condition look-back period is the largest single risk. Most NJ short-term carriers use a look-back window of 12 to 60 months — any condition diagnosed, treated, or with symptoms during that period may be excluded from coverage. Someone who saw a doctor for back pain, depression, or elevated blood pressure in the prior year may find that all related care is denied as a pre-existing condition, regardless of how minor the prior incident was. The NJ Department of Banking and Insurance regulates short-term carriers under federal short-term limited-duration insurance rules.

Check Your NJ Marketplace SEP Before Buying Short-Term

Most NJ residents considering short-term coverage qualify for a GetCoveredNJ special enrollment period that produces ACA-compliant coverage — satisfying the mandate and potentially qualifying for NJHPS. A licensed NJ agent confirms SEP eligibility and compares marketplace options at no cost.

NJ Alternatives to Short-Term Coverage — Check These First

Most situations that lead New Jersey residents toward short-term health insurance actually qualify for a better alternative. GetCoveredNJ‘s special enrollment period triggers, the NJ Easy Enrollment Program via state tax filing, and NJ FamilyCare eligibility for lower-income residents each produce ACA-compliant coverage that satisfies the mandate — at costs that often undercut short-term premiums after NJHPS applies. The New Jersey individual health insurance guide covers those ACA-compliant paths in full, and the self-employed coverage guide covers the same ground for 1099 workers between contracts.

| Situation | Better Alternative | SEP Available? |

|---|---|---|

| Lost job or employer coverage | GetCoveredNJ SEP (60 days) | Yes — immediate |

| Moved to New Jersey | GetCoveredNJ SEP (60 days) | Yes — immediate |

| Turned 26, off parent’s plan | GetCoveredNJ SEP (60 days) | Yes — immediate |

| Pregnancy | GetCoveredNJ SEP (NJ-only trigger) | Yes — 60 days from conception |

| Missed open enrollment | NJ Easy Enrollment Program | Year-round via state tax return |

| Income under 138% FPL | NJ FamilyCare — applies anytime | Year-round enrollment |

💡 The NJ Easy Enrollment Program is the most overlooked alternative

New Jersey residents who missed the January 31 open enrollment deadline and have no qualifying life event can still trigger a GetCoveredNJ special enrollment period by completing the NJ-EZ Enroll Form when filing their state income tax return. The resulting marketplace coverage satisfies the mandate, may qualify for NJHPS subsidies, and eliminates both the SRP penalty and the short-term pre-existing condition exclusion risk. This pathway is unique to NJ and connects tens of thousands of uninsured residents to coverage annually.

When Short-Term Coverage Legitimately Fits in NJ

Short-term health insurance in New Jersey has legitimate use cases — narrow situations where the 4-month coverage window fits a genuine gap, the buyer has no pre-existing conditions that would be excluded, and no GetCoveredNJ SEP is immediately available. The financial reality is that buyers still owe the NJ SRP for those months, so the decision should account for both the short-term premium and the mandate penalty as combined costs. Buyers whose real need is broad provider access rather than a short gap should compare the New Jersey PPO health insurance options instead.

⚠️ Situations where short-term is the wrong choice in NJ

Any household with pre-existing conditions; anyone eligible for an immediate GetCoveredNJ SEP; anyone below 600 percent FPL who would qualify for NJHPS on the marketplace; anyone whose gap exceeds 4 months; and anyone who believes short-term coverage will protect them from the SRP penalty — it will not.

Short-Term Carriers Available in New Jersey

Short-term health insurance carriers in New Jersey are a separate market from the five GetCoveredNJ carriers. National short-term specialists operate in NJ under federal short-term limited-duration insurance rules, with carriers varying by county and plan design. None of the five GetCoveredNJ marketplace carriers — Horizon, AmeriHealth, Oscar, UnitedHealthcare, or Ambetter — sell short-term individual products as their primary individual offering.

| Carrier | NJ STM Available | Typical Coverage | Monthly Premium Range (40-yr-old) |

|---|---|---|---|

| UHC / Golden Rule | Yes | Emergency + limited outpatient | $130–$260 |

| Pivot Health | Yes | Multi-tier plans | $110–$240 |

| National General / Allstate | Yes | STM with optional riders | $100–$220 |

| Marketplace Silver (unsubsidized) | N/A | Full ACA-compliant coverage | $485–$680 |

| Marketplace Silver after NJHPS | N/A | Full ACA-compliant coverage | $60–$380 (income-dependent) |

The premium comparison matters in the right direction. Short-term premiums of $110–260 per month look cheaper than unsubsidized marketplace Silver at $485–680. But for most NJ residents below 400 percent FPL, the subsidized marketplace comparison is $60–380 per month — making the margin much narrower or even reversing the advantage. The NJ SRP obligation on top of short-term premiums further erodes the cost advantage for most income levels.

Common Short-Term Coverage Mistakes in New Jersey

Four mistakes consistently hurt NJ residents who consider or purchase short-term health insurance — each reflecting a misunderstanding specific to how NJ’s mandate, the NJHPS subsidy stack, or the federal 4-month cap interact with short-term coverage decisions.

Frequently Asked Questions About NJ Short-Term Health Insurance

Common questions about short-term health insurance in New Jersey — covering whether STM satisfies the mandate, the 4-month cap, what alternatives exist, whether STM avoids the SRP penalty, pre-existing condition exclusions, and what short-term plans actually cover.

Does short-term health insurance satisfy the NJ individual mandate?

No. Short-term health insurance does not constitute minimum essential coverage under New Jersey law and does not satisfy the NJ individual health insurance mandate. Residents who carry only short-term coverage for any month of the year still owe the Shared Responsibility Payment on their NJ state income tax return for those months — the greater of $695 per adult or 2.5 percent of household income, capped at the statewide average Bronze plan premium.

How long can short-term health insurance last in New Jersey?

Federal rules effective September 2024 cap short-term health insurance plans at a 3-month initial contract with a maximum 1-month renewal, totaling 4 months of coverage. New Jersey follows the federal cap without adding additional state restrictions. After the 4-month cap is reached, a new short-term plan from the same carrier cannot be issued for the same coverage period.

What are the alternatives to short-term health insurance in New Jersey?

Most New Jersey residents considering short-term coverage qualify for a better alternative. Qualifying life events including job loss, marriage, birth, pregnancy, moving to NJ, and aging off a parent’s plan open 60-day GetCoveredNJ special enrollment periods. The NJ Easy Enrollment Health Insurance Program lets uninsured residents trigger enrollment through the state tax return without a qualifying event. Both alternatives produce ACA-compliant coverage that satisfies the NJ mandate and may qualify for NJHPS subsidies.

Can I use short-term insurance to avoid the NJ penalty?

No. Short-term health insurance explicitly does not satisfy the New Jersey individual mandate’s minimum essential coverage requirement. Residents who purchase short-term plans thinking they fulfill the mandate requirement will still owe the Shared Responsibility Payment for those months when filing NJ Form NJ-1040. The only ways to avoid the SRP are to have qualifying ACA-compliant coverage, NJ FamilyCare, Medicare, employer-sponsored plans meeting MEC standards, or a valid mandate exemption.

Are pre-existing conditions covered by NJ short-term health insurance?

No. Short-term health insurance carriers in New Jersey can deny coverage for pre-existing conditions, exclude treatment related to those conditions, or refuse to issue a policy entirely based on health history. This is a fundamental difference from GetCoveredNJ marketplace plans, which must accept all applicants regardless of health status and cannot impose any pre-existing condition exclusions under ACA rules.

What does short-term health insurance cover in New Jersey?

Most New Jersey short-term plans cover emergency care, hospitalization, and limited outpatient services subject to plan-specific dollar caps. Short-term plans are not required to cover the ACA’s ten essential health benefits — meaning maternity care, mental health services, preventive care without cost-sharing, and prescription drug coverage are typically excluded or limited. Coverage varies significantly by carrier and plan; read the specific exclusions carefully before purchasing.

Related New Jersey Health Insurance Resources

Explore the rest of the New Jersey coverage library — the statewide overview, the GetCoveredNJ marketplace, carrier comparisons, and cost and subsidy guidance.

Complete 2026 overview — carriers, FamilyCare, mandate, and subsidy paths.

GetCoveredNJ MarketplaceEnrollment steps, NJ Health Plan Savings, and the Easy Enrollment Program.

Best NJ Health PlansFive-carrier comparison with 2026 rate changes and OMNIA network guide.

Costs & Savings GuidePremium ranges by age and county with the full NJHPS subsidy guide.

Find a Better NJ Coverage Option Than Short-Term

Most NJ residents shopping short-term coverage qualify for GetCoveredNJ special enrollment — with ACA-compliant coverage that satisfies the mandate and may qualify for NJHPS subsidies. ForHealthInsurance.com confirms SEP eligibility and completes enrollment at no extra cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving New Jersey residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.