Small Business Health Insurance in Hawaii 2026: PHCA, HMSA, and Group Plans

Hawaii is the only state in the United States with a pre-ACA employer health insurance mandate. The Hawaii Prepaid Health Care Act of 1974 requires employers to provide health coverage to employees working 20 or more hours per week, well below the ACA’s 30-hour federal standard. For small business health insurance Hawaii employers, PHCA compliance is not optional and applies to businesses of any size. This guide explains the law, which carriers offer small business health insurance in Hawaii, and how ACA tools like SHOP and ICHRA interact with PHCA obligations. For a full overview of the Hawaii market, see the Hawaii health insurance guide.

What do you need help with?

Understand my PHCA obligations

What the law requires and which employees must be covered

See requirements ↓Check SHOP tax credit eligibility

Up to 50% credit for businesses with fewer than 25 FTE

Check eligibility ↓The Hawaii Prepaid Health Care Act: What Every Employer Must Know

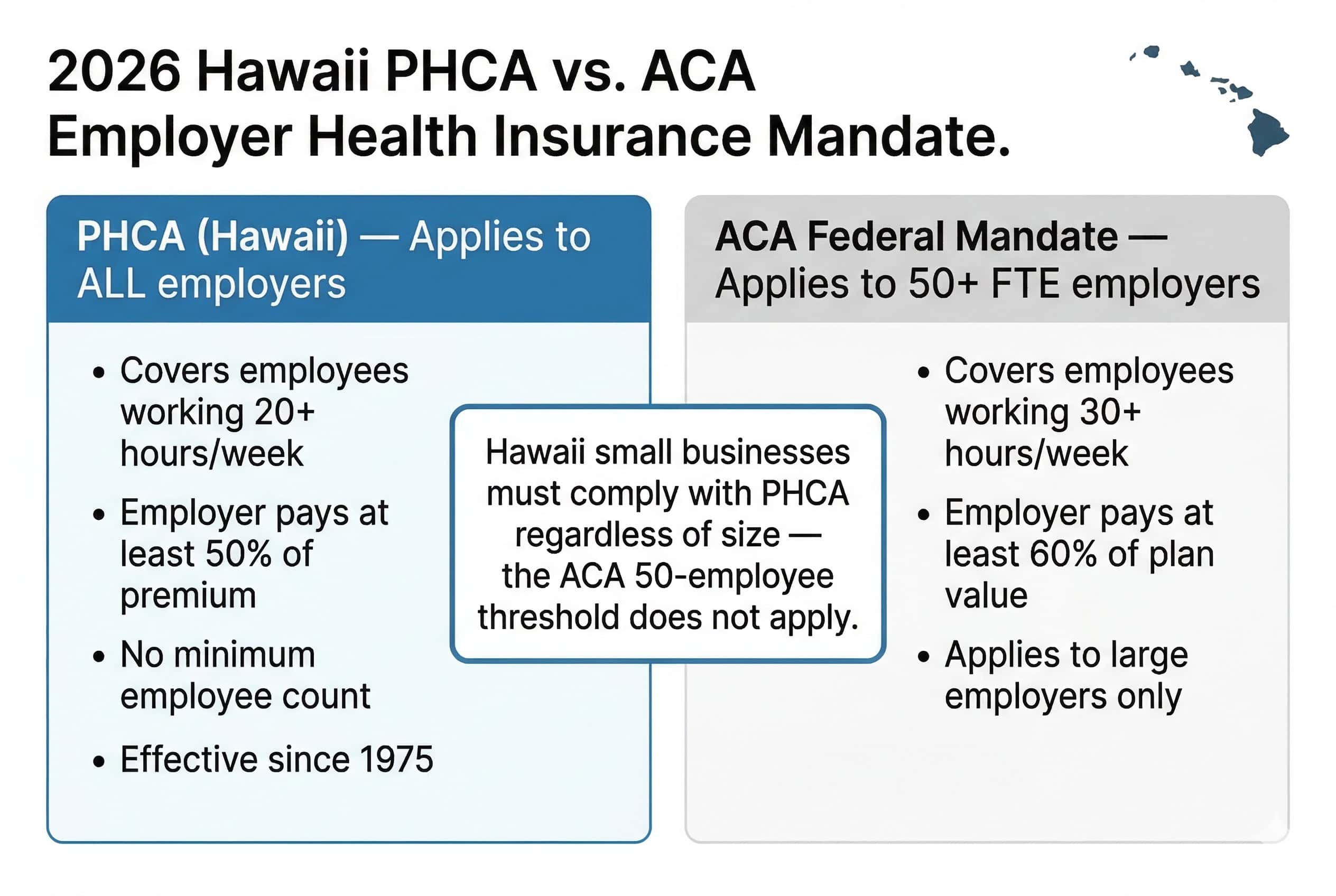

The Hawaii Prepaid Health Care Act (PHCA) of 1974 requires all Hawaii employers to provide health insurance to employees who work 20 or more hours per week for four consecutive weeks. Employers must pay at least 50% of the monthly premium. The law applies to businesses of any size and is enforced by the Hawaii Department of Labor and Industrial Relations.

The PHCA’s 20-hour threshold is the most important distinction from federal law. Under the ACA, employers with 50 or more full-time equivalent employees must offer coverage to employees working 30 or more hours per week. The PHCA applies to all Hawaii employers regardless of size — a restaurant with two employees each working 22 hours per week must provide PHCA-compliant coverage. This makes small business health insurance in Hawaii obligations broader and more immediate than the ACA alone would require.

According to the Hawaii Department of Labor and Industrial Relations, the PHCA has been in effect since July 1, 1975, making Hawaii the only state with a pre-ACA employer mandate. The law is grandfathered from the ACA’s employer shared responsibility provisions, meaning Hawaii employers operate under PHCA rules rather than the ACA’s employer mandate for employees working 20–29 hours per week.

PHCA Key Requirements for 2026

Cover employees working 20+ hours/week for 4+ consecutive weeks. Pay at least 50% of the monthly premium. Coverage must meet minimum benefit standards set by the Hawaii Department of Labor. Employees working fewer than 20 hours/week or in their first 4 weeks of employment are not covered by PHCA, but may be offered coverage voluntarily.

Group Health Insurance Carriers for Hawaii Small Businesses

Small business health insurance Hawaii employers have four primary group carriers for 2026: HMSA (statewide, PPO and HMO), Kaiser Permanente Hawaii (Oahu only, HMO), UHA (University Health Alliance, group plans statewide), and HMAA (Hawaii Management Alliance Association, association-based). HMSA is the dominant carrier across all islands; Kaiser is competitive for Oahu businesses; UHA and HMAA serve specific employer markets.

HMSA Group Plans

- Dominant carrier; available on all six major islands

- Group PPO and HMO options for employers

- BlueCard national network for employees who travel

- HMSA Preferred Provider Plan (PPO) most common group product

- Nonprofit BCBS affiliate since 1938

- Works with employers of any size

Kaiser Permanente Hawaii

- Oahu-based businesses only; not available on neighbor islands

- Integrated HMO model; Kaiser facilities and insurance combined

- Competitive group premiums for Oahu employers

- Moanalua Medical Center as primary care hub

- High employee satisfaction scores in Hawaii

- No PPO option; employees must use Kaiser network

UHA: University Health Alliance

- Hawaii-based carrier with employer market focus

- Strong presence among professional and university-affiliated employers

- Statewide network through HMSA provider agreements

- PPO and HMO group plan options

- Individual market access limited; primarily group plans

HMAA: Hawaii Management Alliance Association

- Association-based group health carrier

- Available to member businesses through HMAA membership

- Competitive rates for smaller employer groups

- Strong presence in Oahu’s business community

- PPO options for member employers

- Not available to general public; employer group enrollment only

For a detailed comparison of HMSA and Kaiser quality ratings, complaint data, and network strength, see the best health insurance in Hawaii guide. Neighbor island employers are limited to HMSA, UHA, and HMAA; Kaiser is only available for Oahu-based group plans.

SHOP Marketplace and Tax Credits for Hawaii Small Businesses

Hawaii small business health insurance employers with fewer than 25 full-time equivalent employees may qualify for the Small Business Health Care Tax Credit through the ACA’s SHOP marketplace. The credit covers up to 50% of premiums paid for qualifying small employers, but only if coverage is purchased through SHOP. Hawaii employers using SHOP can offer HMSA or Kaiser plans through HealthCare.gov’s small business portal.

| Business Size | PHCA Obligation | SHOP Tax Credit Eligible | Recommended Approach |

|---|---|---|---|

| 1–10 employees | Yes, if any work 20+ hrs/wk | Yes; up to 50% credit if avg wages below $56,000 | SHOP for tax credit; HMSA or Kaiser |

| 11–24 employees | Yes | Yes; partial credit (phases out) | Compare SHOP credit vs. direct group plan cost |

| 25–49 employees | Yes | No; above SHOP credit threshold | Direct group plan: HMSA, Kaiser, UHA, or HMAA |

| 50+ employees | Yes; PHCA and ACA mandate both apply | No | Direct group plan; consult agent for ACA compliance |

SHOP Tax Credit Requirement

The Small Business Health Care Tax Credit is only available when coverage is purchased through HealthCare.gov SHOP. Hawaii employers buying group coverage directly from HMSA or Kaiser do not qualify for the federal tax credit, even if they otherwise meet the criteria. Employers within the credit-eligible range should compare SHOP vs. direct carrier costs before enrolling. For a full breakdown of small business health insurance Hawaii tax credit eligibility, see the IRS guide linked above. The IRS SHOP tax credit guide covers eligibility rules and calculation methods in detail.

Get PHCA-Compliant Group Coverage for Your Hawaii Business

Compare HMSA, Kaiser, UHA, and HMAA group plans for your island and employee count. A licensed agent can verify PHCA compliance and identify SHOP tax credit eligibility at no cost.

PHCA Compliance Steps for Hawaii Small Businesses

Hawaii small businesses must select a PHCA-compliant health plan, enroll eligible employees (those working 20+ hours for four consecutive weeks), and pay at least 50% of the monthly premium. New employees become eligible after four consecutive weeks at 20+ hours per week. Employers must notify employees of their rights under the PHCA and maintain records for DLIR audits.

Identify PHCA-eligible employees

Any employee who works 20 or more hours per week for four consecutive weeks becomes PHCA-eligible. Track hours carefully; Hawaii’s 20-hour threshold captures many part-time workers in the state’s large hospitality and tourism industry. Seasonal workers who hit the threshold must also be offered coverage.

Select a PHCA-compliant health plan

Choose a group health plan that meets PHCA minimum benefit requirements from an approved carrier: HMSA, Kaiser (Oahu), UHA, or HMAA. The plan must include basic hospitalization, surgical care, and outpatient services. A licensed agent can verify PHCA compliance for a specific plan before enrollment. This step is essential for any Hawaii small business health insurance arrangement.

Pay at least 50% of the premium

PHCA requires employers to contribute at least 50% of the monthly premium for employee-only coverage. Employer contributions are fully deductible as a business expense under federal tax law. Employee premium contributions are made pre-tax through a Section 125 cafeteria plan, reducing payroll tax liability for both employer and employee.

File PHCA documentation with DLIR

Hawaii employers must maintain records of PHCA-eligible employees and coverage offered. The Hawaii DLIR may audit PHCA compliance, particularly for employers in Hawaii’s hospitality sector where seasonal and variable-hour employment is common. Licensed agents assist with PHCA documentation requirements at no additional cost.

Real Scenario: Kauai Restaurant, 8 Employees, 5 Working 25 Hours Per Week

A Kauai restaurant owner has 8 total employees: 3 full-time (40 hrs/week) and 5 part-time at 25 hours per week. All 8 are PHCA-eligible under the 20-hour threshold. Kaiser Permanente is not available on Kauai, so HMSA is the primary option for small business health insurance in Hawaii on the neighbor islands. With 8 employees, the business is SHOP-eligible for the Small Business Health Care Tax Credit. If average employee wages are below $56,000, the owner could receive a federal tax credit covering up to 50% of premiums paid through SHOP — reducing the annual insurance cost significantly. A licensed agent can calculate the SHOP credit vs. direct HMSA group plan pricing to identify the lower total cost.

ICHRA and QSEHRA: Alternatives to Traditional Group Plans

Small business health insurance Hawaii employers that find traditional group plans cost-prohibitive can use Individual Coverage HRAs (ICHRA) or Qualified Small Employer HRAs (QSEHRA) as PHCA-compliant alternatives. Under these arrangements, the employer reimburses employees for individual market plan premiums; employees choose their own HMSA or Kaiser plan and the employer manages a fixed monthly contribution. ICHRA has no size limit; QSEHRA is for employers with fewer than 50 full-time employees.

ICHRA: Individual Coverage HRA

Employer sets a monthly reimbursement amount (any amount). Employees purchase their own individual HMSA or Kaiser plan on or off exchange and submit for reimbursement. No size limit; works for any Hawaii employer. Employees cannot receive ICHRA reimbursements and marketplace subsidies simultaneously. Best for employers with varied workforce needs across multiple islands.

QSEHRA: Qualified Small Employer HRA

For Hawaii employers with fewer than 50 full-time employees. 2026 contribution limits: up to $6,350/year for employee-only coverage; $12,800/year for family coverage. Employees purchase individual HMSA or Kaiser plans and submit receipts. QSEHRA allowances reduce ACA marketplace subsidy eligibility dollar-for-dollar. Simpler administration than ICHRA for smaller employers. Employees needing individual coverage guidance can see the Hawaii individual health insurance guide.

Both ICHRA and QSEHRA can satisfy the small business health insurance Hawaii employer obligation under PHCA when structured correctly. The Department of Labor EBSA small business resources provide HRA compliance guidance. Hawaii-specific PHCA compliance with HRA arrangements should be verified with a licensed agent familiar with both PHCA and federal HRA regulations. For employees who purchase individual coverage through these arrangements, the Hawaii health insurance marketplace guide covers enrollment and subsidy interaction. Employees with incomes that may qualify for Med-QUEST should also review the affordable health insurance guide for Hawaii.

Frequently Asked Questions — Small Business Health Insurance in Hawaii

The most common questions about small business health insurance in Hawaii involve PHCA coverage thresholds, which carriers are available by island, how the SHOP tax credit works, and whether ICHRA or QSEHRA can satisfy the employer mandate.

Is health insurance required for small businesses in Hawaii?

Yes. The Hawaii Prepaid Health Care Act of 1974 requires all Hawaii employers, regardless of business size, to provide health insurance to employees who work 20 or more hours per week for four consecutive weeks. Employers must pay at least 50% of the monthly premium. The obligation applies to businesses with even one eligible employee, making small business health insurance Hawaii obligations broader than the federal ACA 50-employee threshold.

What carriers offer small business health insurance in Hawaii?

Hawaii small business employers can choose from four primary group carriers for 2026: HMSA (available on all six major islands, PPO and HMO), Kaiser Permanente Hawaii (Oahu only, HMO), UHA (statewide, group plans), and HMAA (association-based group plans, primarily Oahu). HMSA is the most widely used carrier for small business health insurance in Hawaii across all islands. On neighbor islands, employers are limited to HMSA, UHA, and HMAA. For help comparing all small business health insurance Hawaii options by island, a licensed agent can provide a no-cost comparison.

What is the SHOP marketplace and does it apply to Hawaii?

The SHOP (Small Business Health Options Program) marketplace at HealthCare.gov allows Hawaii employers with fewer than 50 full-time equivalent employees to offer HMSA or Kaiser health plans to their employees and potentially qualify for the Small Business Health Care Tax Credit. The credit covers up to 50% of premiums for employers with fewer than 25 FTE employees earning average wages below $56,000. Employers must purchase coverage through SHOP to claim the credit. SHOP enrollment is available year-round for qualifying Hawaii employers.

How does the PHCA interact with the ACA employer mandate?

Hawaii is grandfathered from the ACA’s employer shared responsibility provisions for employees working 20–29 hours per week. This means Hawaii employers operate under PHCA rules for those employees rather than the ACA’s 30-hour threshold. For employees working 30 or more hours per week, both PHCA and ACA requirements apply, though PHCA’s 50% minimum premium contribution is the key standard in practice. Hawaii businesses with 50 or more full-time equivalent employees must also comply with ACA reporting requirements regardless of PHCA coverage.

Can I use an ICHRA or QSEHRA instead of a group plan in Hawaii?

Yes. Hawaii employers can use an Individual Coverage HRA (ICHRA) or Qualified Small Employer HRA (QSEHRA) as an alternative to a traditional group plan, provided the arrangement satisfies the PHCA’s 50% minimum contribution requirement. Under ICHRA, the employer reimburses employees for individual HMSA or Kaiser plan premiums with no contribution limit. Under QSEHRA, employers with fewer than 50 full-time employees can contribute up to $6,350/year (employee-only) or $12,800/year (family) in 2026. PHCA compliance with HRA arrangements should be reviewed with a licensed agent familiar with Hawaii law.

Hawaii Health Insurance Guides

Complete 2026 guide: PHCA, Med-QUEST, HMSA, Kaiser, and all coverage pathways

Hawaii Health Insurance MarketplaceHealthCare.gov SHOP enrollment, subsidy eligibility, and open enrollment dates

Best Health Insurance in HawaiiCompare HMSA PPO, Kaiser HMO, UHA, and HMAA: carrier profiles for 2026

Affordable Health Insurance in HawaiiMed-QUEST, subsidies, and lowest-cost individual plan options by island

Individual Health Insurance in HawaiiFor self-employed owners and employees needing individual coverage

PPO Health Insurance PlansCompare PPO plans nationwide: BlueCard network, provider flexibility, no referrals

Compare Hawaii Small Business Health Insurance for 2026

HMSA group PPO from ~$500/employee/month, Kaiser HMO on Oahu, SHOP tax credits up to 50% for qualifying employers. Get a PHCA-compliant small business health insurance Hawaii quote for your business and island.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Hawaii residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.