Hawaii Health Insurance Marketplace 2026: HealthCare.gov Guide

Hawaii uses the federal marketplace at HealthCare.gov for individual and family health insurance enrollment — not a state-run exchange. The Hawaii Health Connector, the state’s own exchange, launched in 2013 and closed in 2015 after spending approximately $204 million in federal grants without reaching financial sustainability. Today, the health insurance marketplace Hawaii residents use runs through HealthCare.gov, where HMSA and Kaiser Permanente offer Bronze through Platinum plans. This guide covers how the health insurance marketplace in Hawaii operates, subsidy eligibility, what changed in 2026, and how to enroll. For a full overview of the Hawaii coverage landscape, see the Hawaii health insurance guide.

What do you need to know?

Why Hawaii uses HealthCare.gov

The state exchange closed in 2015; here’s how the health insurance marketplace in Hawaii works now

Learn more ↓Get a free marketplace quote

Compare HMSA and Kaiser plans with subsidies applied by island

Get a quote →Why Hawaii Uses HealthCare.gov Instead of a State Exchange

Hawaii is one of only two states whose state-based exchange shut down after launch. The Hawaii Health Connector closed in 2015 after spending approximately $204 million in federal grants without achieving enrollment sustainability. Hawaii residents now use HealthCare.gov for ACA plan enrollment. HMSA and Kaiser Permanente are the two carriers available on the health insurance marketplace in Hawaii for 2026.

The Hawaii Health Connector opened in October 2013 and struggled from the start. Hawaii’s PHCA employer mandate already covered most employed residents, leaving a smaller potential individual market than projected. After exhausting federal establishment grants, the Connector officially closed in 2015, transferring its enrollees to HealthCare.gov. Hawaii is one of only two states whose exchange shut down entirely; the other is Oregon, which transitioned in 2014.

The closure explains why Hawaii’s health insurance marketplace enrollment remains small: approximately 25,000–30,000 residents out of 1.4 million, compared to states like Florida where over 4 million enrolled. The PHCA and Med-QUEST cover the majority of Hawaii residents before they reach the marketplace. Carrier licensing and consumer complaint information for HMSA and Kaiser is maintained by the Hawaii Insurance Division.

2026 Open Enrollment Dates

Start: November 1, 2025 | Deadline for January 1 coverage: December 15, 2025 | Final deadline: January 15, 2026. Special Enrollment Periods remain open year-round for qualifying life events.

How to Enroll in a Hawaii Marketplace Plan

Hawaii residents enroll through HealthCare.gov during Open Enrollment (November 1 through January 15) or during a Special Enrollment Period triggered by a qualifying life event. Neighbor island ZIP codes show only HMSA plans; Oahu ZIP codes show both HMSA and Kaiser options. Off-exchange HMSA plans can be purchased directly at any time without a tax credit.

Check Med-QUEST eligibility first

Hawaii residents earning up to $20,800 (single) or $43,100 (family of four) in 2026 may qualify for Med-QUEST at $0 premium. Apply through the Hawaii Med-QUEST Division or via HealthCare.gov — both routes work. If Med-QUEST eligible, marketplace plan enrollment is not needed.

Create or log into HealthCare.gov

Visit HealthCare.gov and create an account or log in. Enter your Hawaii ZIP code, which determines island location and carrier availability. Oahu ZIP codes show both HMSA and Kaiser for the health insurance marketplace Hawaii enrollees; Maui, Hawaii Island, Kauai, Molokai, and Lanai ZIP codes show HMSA plans only.

Review plans with subsidies applied

HealthCare.gov displays HMSA and Kaiser plans with premium tax credits pre-applied based on household income. Silver plans for incomes between 138% and 250% FPL carry cost-sharing reductions that lower deductibles below the standard Silver tier. Compare Bronze, Silver, and Gold tiers by monthly premium, deductible, and out-of-pocket maximum.

Enroll and pay the first premium

Complete enrollment on HealthCare.gov and pay the first month’s premium directly to HMSA or Kaiser. Coverage begins January 1 for enrollments completed by December 15, or February 1 for enrollments by January 15. Coverage does not activate without the first premium payment.

Outside of open enrollment, a special enrollment period opens a 60-day window after qualifying life events including job loss, marriage, birth of a child, and relocation between islands. Hawaii’s large hospitality and tourism sector makes job-loss SEP particularly common, especially after seasonal layoffs on Maui and Hawaii Island. Residents between jobs should compare COBRA costs against subsidized marketplace plans before enrolling — details are in the individual health insurance guide for Hawaii.

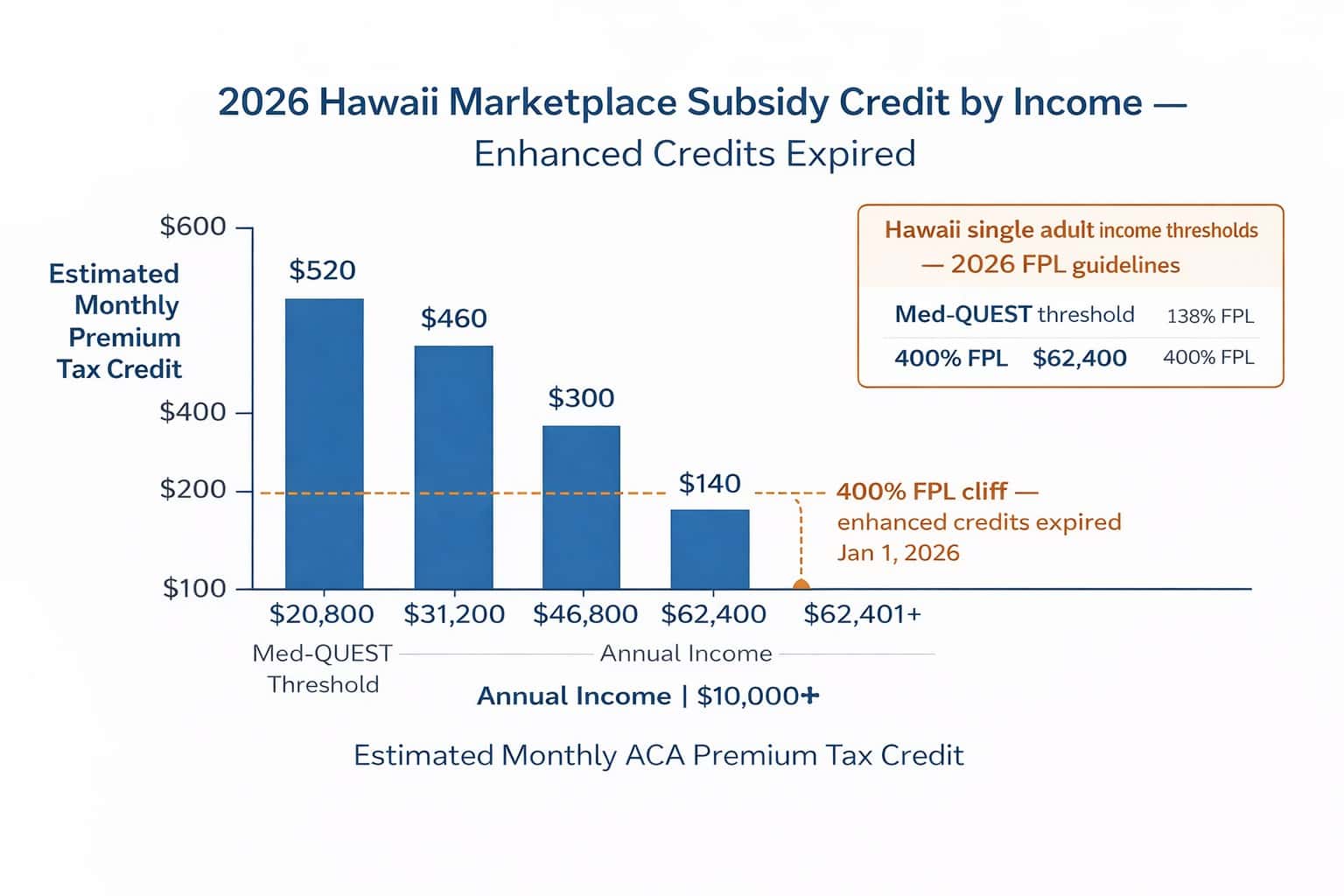

2026 Subsidy Changes: What Hawaii Enrollees Need to Know

Enhanced premium tax credits expired December 31, 2025. Hawaii residents who relied on boosted credits from 2021 through 2025 face significantly higher 2026 net premiums. Standard ACA subsidy rules now apply: premium tax credits are available for incomes between 100% and 400% FPL (approximately $15,060 to $62,400 for a single adult). Residents above $62,400 receive no credits in 2026.

The 400% FPL Subsidy Cliff Is Back for 2026

From 2021 through 2025, enhanced credits eliminated the cliff; residents at any income received some subsidy. Starting January 1, 2026, residents earning above 400% FPL (~$62,400 single) receive $0 in premium tax credits. Those just above the threshold may find off-exchange HMSA PPO plans more cost-effective than unsubsidized marketplace plans.

| Income Level (Single Adult, 2026) | % of FPL | 2026 Subsidy Status | Best Option |

|---|---|---|---|

| Up to $20,800 | Up to 138% | Med-QUEST eligible; $0 premium | Apply via Med-QUEST Division |

| $20,800 – $31,200 | 138% – 200% | Large tax credits + CSR available | Silver plan on HealthCare.gov |

| $31,200 – $46,800 | 200% – 300% | Moderate tax credits | Silver or Bronze on HealthCare.gov |

| $46,800 – $62,400 | 300% – 400% | Smaller tax credits | Compare on-exchange vs. off-exchange HMSA |

| Above $62,400 | Above 400% | No tax credits in 2026 | Off-exchange HMSA PPO recommended |

Hawaii Marketplace Carriers: HMSA and Kaiser for 2026

Two carriers offer plans on the health insurance marketplace Hawaii uses for 2026: HMSA and Kaiser Permanente Hawaii. HMSA offers HMO and PPO plans on all six major islands. Kaiser offers HMO plans on Oahu only — neighbor island residents have access only to HMSA on the exchange. Both carriers offer Bronze, Silver, Gold, and Platinum tiers.

HMSA: All Islands

- HMO and PPO options on HealthCare.gov

- Available on all six major islands

- Only carrier for neighbor island residents on the exchange

- BlueCard PPO: national network for inter-island and mainland travel

- Silver + CSR plans available for 138%–250% FPL

- Off-exchange PPO plans available year-round, no enrollment window

Kaiser Permanente: Oahu Only

- HMO plans only; integrated care model

- Available to Oahu residents only

- Not available on any neighbor island

- Generally lower premiums than HMSA PPO plans

- Requires using Kaiser network providers and facilities

- No out-of-network coverage (emergencies excepted)

For a full comparison of HMSA and Kaiser quality ratings, network strength, and 2026 premium data — including off-exchange options not shown on the health insurance marketplace Hawaii uses — see the best health insurance in Hawaii guide. For residents above the 400% FPL threshold, off-exchange HMSA PPO plans purchased directly from HMSA offer comparable coverage without marketplace restrictions. A licensed agent can compare on-exchange and off-exchange HMSA options at no cost. For HMSA and Kaiser group plan options for employers, see the Hawaii small business health insurance guide.

On-Exchange vs. Off-Exchange: Which Is Right for You?

Hawaii residents who qualify for premium tax credits must enroll through HealthCare.gov; subsidies are only available on-exchange. Residents above the 400% FPL threshold ($62,400 single in 2026) receive no credits on-exchange and should compare off-exchange HMSA PPO plans, particularly for BlueCard national network access for inter-island and mainland travel.

Enroll On-Exchange (HealthCare.gov)

Income is between 100% and 400% FPL ($15,060–$62,400 single). Any subsidy eligibility means HealthCare.gov is the only path to financial assistance. Med-QUEST applicants also use HealthCare.gov to apply for Hawaii Medicaid.

Consider Off-Exchange HMSA

Income is above $62,400 single; no credits available on-exchange in 2026. Or if PPO flexibility and HMSA BlueCard national network coverage are priorities for frequent inter-island or mainland travel. Available year-round with no enrollment window.

Apply for Med-QUEST

Income is below 138% FPL (approximately $20,800 single or $43,100 for a family of four in 2026). Hawaii is a Medicaid expansion state. Med-QUEST covers eligible residents at $0 premium through AlohaCare, Ohana Health Plan, and other managed care organizations. Enrollment is open year-round. See the affordable health insurance guide for details.

Use Special Enrollment Period

A qualifying life event occurred outside open enrollment: job loss, marriage, birth of a child, relocation to a new island, or aging off a parent’s plan at 26. Most events open a 60-day window on HealthCare.gov. Hawaii’s tourism and hospitality workforce frequently uses job-loss SEP given seasonal employment patterns.

Real Scenario: Maui Resident, Age 44, $38,000 Annual Income

A 44-year-old Maui hospitality worker on Maui earns $38,000 annually (approximately 243% FPL) and loses employer coverage after a seasonal layoff. The job loss triggers a 60-day special enrollment period on HealthCare.gov. On the health insurance marketplace Hawaii uses, Maui ZIP codes show only HMSA plans. At 243% FPL, a Silver HMSA plan qualifies for both premium tax credits and cost-sharing reductions — a plan with a standard Silver premium of approximately $520/month drops to around $190–$220/month after credits, with the CSR benefit reducing the Silver deductible well below the standard tier.

Compare Hawaii Marketplace Plans for 2026

HMSA Silver plans on Oahu start around $490/month for a 40-year-old before subsidies. Kaiser Silver runs approximately $460/month on Oahu. Neighbor island residents see only HMSA. Verify Med-QUEST eligibility at $20,800 and compare all options for your island.

Frequently Asked Questions About the Hawaii Health Insurance Marketplace

The most common questions about the health insurance marketplace in Hawaii involve why Hawaii uses HealthCare.gov, open enrollment dates, which carriers are available by island, and how the 2026 subsidy changes affect net premiums.

Does Hawaii have its own state health insurance marketplace?

No. Hawaii’s state exchange (the Hawaii Health Connector) shut down in 2015 after spending approximately $204 million in federal grants without reaching financial sustainability. The health insurance marketplace Hawaii residents now use is HealthCare.gov. The closure was largely driven by Hawaii’s PHCA employer mandate, which already covered most employed residents and left too small an individual market to sustain an independent exchange. Hawaii is one of only two states whose state-based exchange shut down entirely.

When is Open Enrollment for Hawaii marketplace plans?

The 2026 health insurance marketplace Hawaii Open Enrollment Period ran from November 1, 2025 through January 15, 2026 on HealthCare.gov. Coverage began January 1, 2026 for enrollments completed by December 15, 2025, or February 1, 2026 for enrollments completed by January 15. Outside open enrollment, Hawaii residents can enroll through a Special Enrollment Period if they experience a qualifying life event such as job loss, marriage, birth of a child, or relocation to a new island.

Which carriers are on the Hawaii health insurance marketplace?

Two carriers offer plans on Hawaii’s HealthCare.gov marketplace for 2026: HMSA (Hawaii Medical Service Association) and Kaiser Permanente Hawaii. HMSA offers HMO and PPO plans and is the only marketplace option for neighbor island residents on Maui, Hawaii Island, Kauai, Molokai, and Lanai. Kaiser offers HMO plans only and is available primarily to Oahu residents. Both carriers offer Bronze, Silver, Gold, and Platinum tiers.

Do Hawaii residents qualify for premium tax credits in 2026?

Hawaii residents using the health insurance marketplace Hawaii on HealthCare.gov and earning between 100% and 400% FPL — approximately $15,060 to $62,400 for a single adult in 2026 — qualify for premium tax credits. Those earning below 138% FPL ($20,800) may qualify for Med-QUEST at $0 premium. The enhanced premium tax credits available from 2021 through 2025 expired December 31, 2025. The subsidy cliff at 400% FPL has returned — residents earning above $62,400 receive no credits in 2026.

What qualifies as a Special Enrollment Period in Hawaii?

Qualifying life events for Special Enrollment in Hawaii include: losing employer or other health coverage, getting married or divorced, having or adopting a child, permanently relocating to a new island or state, aging off a parent’s plan at 26, and gaining citizenship. Most qualifying events open a 60-day enrollment window. Hawaii’s large hospitality and tourism sector means job-loss SEP is particularly common, especially following seasonal layoffs on Maui and Hawaii Island.

Can I get an off-exchange HMSA plan instead of enrolling on HealthCare.gov?

Yes. HMSA offers health plans directly (outside of HealthCare.gov), including PPO plans that may not be available on the exchange. Off-exchange plans are not eligible for premium tax credits, so they are most appropriate for residents earning above 400% FPL who receive no subsidies in 2026. Off-exchange HMSA PPO plans provide access to HMSA’s statewide network across all six major islands and the BlueCard national network for mainland coverage. A licensed agent can compare on-exchange and off-exchange HMSA options at no cost.

Hawaii Health Insurance Guides

Complete 2026 guide: PHCA, Med-QUEST, HMSA, Kaiser, and all coverage pathways

Best Health Insurance in HawaiiHMSA PPO vs. Kaiser HMO: island-by-island carrier comparison for 2026

Affordable Health Insurance in HawaiiMed-QUEST eligibility, subsidies, and lowest-cost plan options by island

Individual Health Insurance in HawaiiCoverage for self-employed, part-time workers, and those between jobs

Small Business Health Insurance in HawaiiPHCA employer obligations, group plans, UHA, HMAA, and SHOP options

PPO Health Insurance PlansCompare PPO plans nationwide: BlueCard network, provider flexibility, no referrals

Get Help with Hawaii Marketplace Enrollment

From Med-QUEST at $0 for incomes up to $20,800, to subsidized HMSA Silver on HealthCare.gov for incomes up to $62,400, to off-exchange HMSA PPO above the subsidy cliff, — a licensed agent can find the right health insurance marketplace Hawaii option for 2026 for your island and income.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Hawaii residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.