Idaho Health Insurance Marketplace: Your Health Idaho 2026 Guide

If you’re looking for health insurance in Idaho, the state marketplace is where most residents start. Idaho runs its own enrollment system — separate from the federal website — where you can compare plans, check whether you qualify for lower costs, and sign up for coverage. This guide explains how the Idaho health insurance marketplace works, what’s changed for 2026, when you can enroll, and what to do if you missed the enrollment window.

What brings you here today?

Why Idaho Runs Its Own Health Insurance Marketplace

Idaho is one of 21 states (plus DC) that operate their own health insurance marketplace instead of using HealthCare.gov. The state exchange, called Your Health Idaho, is the only place Idaho residents can apply for premium tax credits — credits that 87% of the roughly 117,000 Idahoans who enrolled for 2026 received in 2025. For 2026, Your Health Idaho offers 154 medical and 21 dental plans from eight private insurance carriers.

Running its own Idaho health insurance marketplace gives the state control over enrollment schedules, carrier negotiations, and consumer assistance programs. The Idaho Legislature voted to create Your Health Idaho in March 2013 under Idaho Code Title 41, Chapter 61, and Idaho later became the first state-based marketplace in the country to migrate from HealthCare.gov to its own technology platform — completing the transition for 2015 coverage. All enrollment, plan comparison, and subsidy applications now happen at yourhealthidaho.org — not HealthCare.gov. Approximately 117,000 Idahoans enrolled through this system for 2026 coverage. Idaho residents who try to enroll through the federal site are redirected to Your Health Idaho.

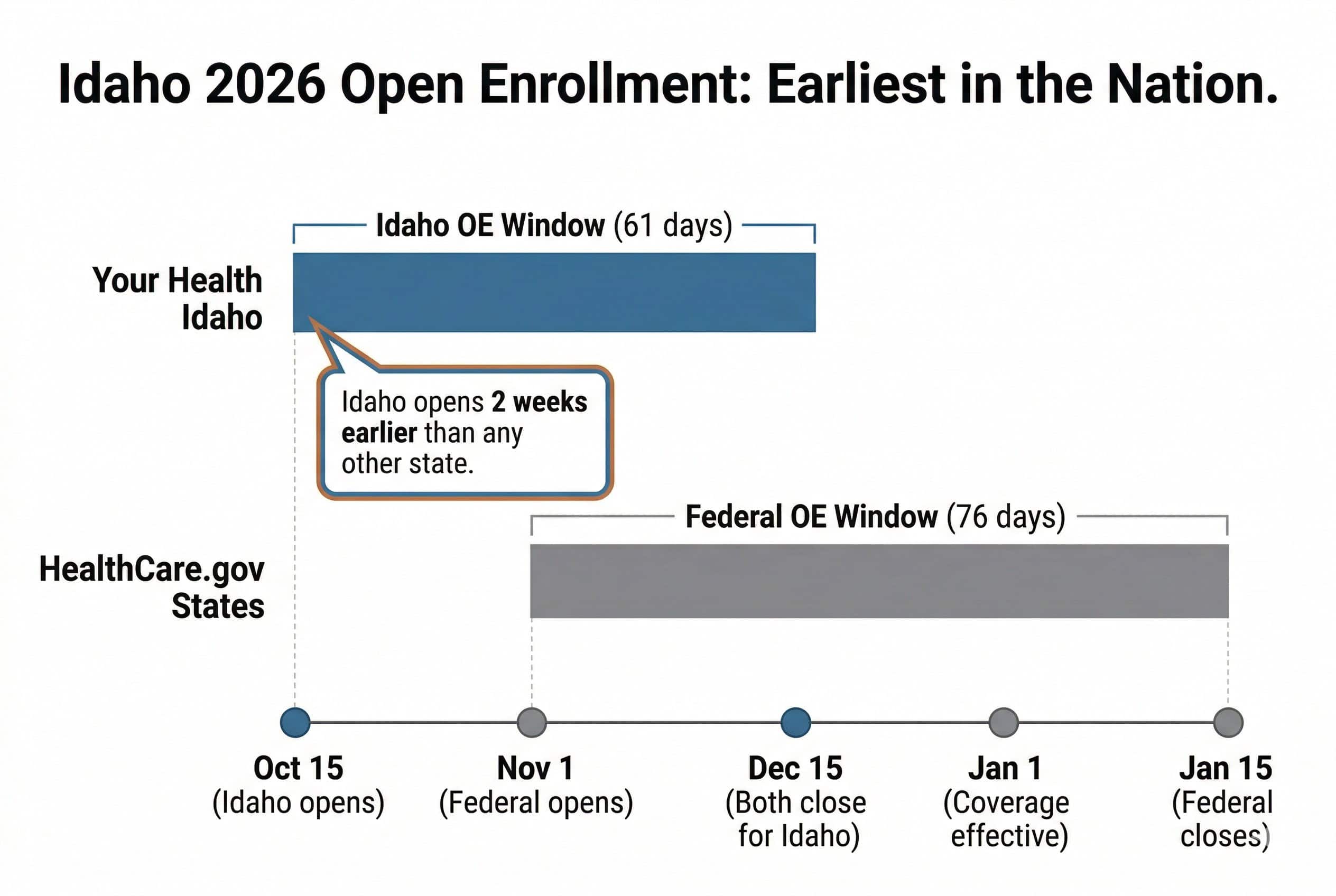

The Idaho health insurance marketplace also sets its own open enrollment window. While most states using HealthCare.gov open enrollment on November 1, Idaho starts two weeks earlier on October 15 — the earliest start date of any state in the country. Your Health Idaho Executive Director Pat Kelly oversees the platform, which launched October 1, 2014, when nearly 76,000 Idahoans enrolled in the first open enrollment period despite federal HealthCare.gov system challenges. This 16-day head start gives Idaho residents more time to compare 154 medical and 21 dental plans before coverage begins on January 1.

Key difference from HealthCare.gov states: Starting in fall 2026 for 2027 coverage, HealthCare.gov is shifting to a November 1 through December 15 open enrollment window — but Idaho’s October 15 start date still complies with the new federal rules, which require enrollment to start no later than November 1 and end no later than December 31. Idaho will continue using its earlier schedule.

How to Enroll Through Your Health Idaho

Enrollment through Your Health Idaho takes four steps: create an account at yourhealthidaho.org, complete the application, compare plans using the side-by-side tool, and select coverage. About 117,000 Idahoans enrolled this way for 2026, and 87% qualified for premium tax credits. The entire process can be completed online, by phone at 855-944-3246, or with free help from a Your Health Idaho-certified agent or Consumer Connector — all at no cost.

Create an Account

Visit yourhealthidaho.org and create a free account. You’ll need your name, email address, and a password. This account stores your application, plan selections, and tax credit eligibility for future years.

Complete the Application

Enter household information including income, family size, and current coverage status. Have proof of income (pay stubs, tax returns, or W-2s) and identification ready. Your subsidy eligibility is calculated immediately after submission.

Compare Plans

Use the side-by-side comparison tool to filter and compare medical and dental plans by premium, deductible, provider network, and metal tier. All 154 medical plans for 2026 are displayed with your subsidy applied so you see the actual monthly cost.

Select and Enroll

Choose a plan, review the details, e-sign the enrollment form, and submit. Coverage for plans selected during open enrollment begins January 1. You can also schedule a free appointment with a Your Health Idaho-certified agent who can walk through the entire process at no cost.

Idaho 2026 Open Enrollment: October 15 Through December 15

Open enrollment for 2026 Idaho health insurance ran from October 15 through December 15, 2025 — the earliest start date of any state exchange in the country. Approximately 117,000 Idahoans enrolled during this window, up from roughly 76,000 in Your Health Idaho’s first open enrollment a decade earlier. Coverage selected during open enrollment took effect January 1, 2026. The next open enrollment period for 2027 coverage will follow the same October 15 through December 15 schedule.

Idaho’s early start matters because more than half of all enrollments historically happen in the final week of open enrollment — and a substantial share on the final day. Starting earlier gives Idaho health insurance marketplace shoppers more time to compare plans, especially important in 2026 given the subsidy changes affecting 87% of Your Health Idaho enrollees.

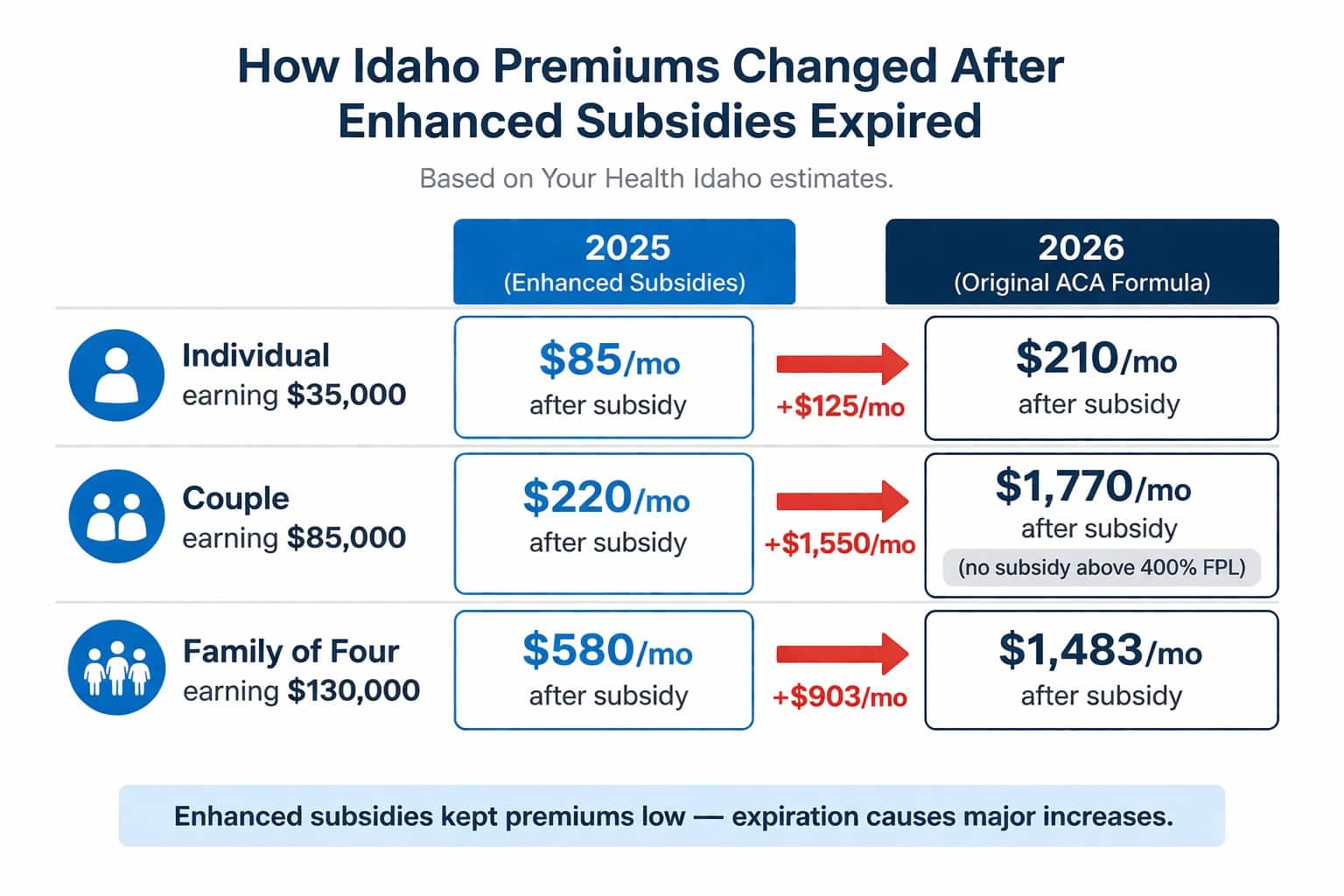

For 2026, approximately 117,000 Idahoans enrolled through Your Health Idaho during the open enrollment window. The Idaho Department of Insurance’s October 2025 rate release approved an average 10% rate increase across all eight 2026 marketplace carriers — less than half the national average — thanks to the state’s reinsurance program, which the Idaho DOI estimates reduces 2026 individual market premiums by 18%. After-subsidy premium increases were significantly larger for many enrollees because the enhanced subsidy formula expired December 31, 2025.

Idahoans already enrolled through Your Health Idaho are automatically renewed each year. However, auto-renewal does not guarantee the same subsidy amount — plans and pricing change annually, so reviewing options between August 1 and December 15 is important even for current Idaho health insurance marketplace enrollees. For 2026, approximately 59% of Idaho enrollees selected Bronze-tier plans (up from 49% in 2025) — a shift driven by the enhanced subsidy expiration that Your Health Idaho Executive Director Pat Kelly described to CNN as “a pretty good indicator of affordability concerns.”

What Changed for Idaho Marketplace Plans in 2026

The most significant change for 2026 is the expiration of enhanced premium tax credits on December 31, 2025. These enhanced subsidies had kept costs lower for the 87% of Your Health Idaho enrollees who qualify for tax credits since 2021. Without them, Idaho marketplace enrollees face significantly higher net premiums, with KIFI Local News 8 reporting an estimated 117,000 Idahoans could see premiums more than double.

2026 Subsidy Impact: The enhanced premium tax credits created by the American Rescue Plan (2021) and extended through the Inflation Reduction Act expired on December 31, 2025. Under the original ACA formula now in effect, subsidies are limited to households earning between 100% and 400% of the Federal Poverty Level ($15,650–$62,600 for an individual using 2025 FPL, which determines 2026 marketplace eligibility). Households above 400% FPL lost subsidy eligibility entirely. Check Idaho cost-saving strategies and current subsidy eligibility →

Beyond the subsidy expiration, several federal policy changes took effect for the 2026 plan year that directly impact the approximately 117,000 Idaho health insurance marketplace enrollees — changes that contributed to roughly 24,400 Idahoans disenrolling in the months following December 15, 2025, per a Your Health Idaho post-enrollment report:

- Income below 150% FPL no longer qualifies as a special enrollment trigger. Previously, dropping below this income threshold let residents enroll outside of open enrollment. This path is now closed — Idahoans in this situation must wait for the next open enrollment or experience a different qualifying life event.

- Bronze and Catastrophic plans now qualify as high-deductible health plans (HDHPs). This means they can be paired with a Health Savings Account (HSA), allowing enrollees to save pre-tax dollars for medical expenses.

- Verification requirements tightened. Income documentation must be submitted within 90 days when there’s a data mismatch — the previous automatic 60-day extension has been removed.

- Auto-renewal no longer guarantees a tax credit. Starting with the 2026 plan year, Your Health Idaho enrollees must actively verify their eligibility information between August 1 and December 31 to remain eligible for premium tax credits and cost-sharing reductions.

The pre-subsidy rate increase for 2026 across Idaho’s eight marketplace carriers averaged 10% — less than half the national average. This relatively modest increase reflects Idaho’s state reinsurance program (1332 waiver approved by HHS on August 16, 2022), which continues to hold premiums lower than they would be without it. According to CMS’s 2026 Open Enrollment Period National Snapshot, 87% of Your Health Idaho enrollees received advance premium tax credits in 2025. The after-subsidy cost increase for 2026 is far larger for most enrollees because the subsidy formula itself changed. Learn more about Idaho’s reinsurance program and how it affects premiums →

Compare Idaho Marketplace Plans

See 2026 plans from all 8 carriers on Your Health Idaho. Bronze plans start at $349/month (St. Luke’s Health Plan), Silver averages $481/month, and 87% of Idaho enrollees received tax credits — averaging roughly $407/month in 2025 (KFF).

Choosing a Metal Tier on Your Health Idaho

Your Health Idaho organizes all 154 medical plans into four metal tiers — Bronze, Silver, Gold, and Platinum — based on how costs are shared between the insurer and the enrollee. Bronze plans have the lowest monthly premiums but highest out-of-pocket costs, while Platinum plans have the highest premiums but cover the largest share of medical expenses. For 2026, approximately 59% of Idaho enrollees selected Bronze (up from 49% in 2025), and 47% of Silver enrollees qualified for cost-sharing reductions.

| Metal Tier | Insurer Pays | You Pay (Out-of-Pocket) | Best For |

|---|---|---|---|

| Bronze | ~60% of costs | ~40% of costs | Healthy individuals who want low premiums and rarely use care |

| Silver | ~70% of costs | ~30% of costs | Moderate users; qualifies for cost-sharing reductions below 250% FPL |

| Gold | ~80% of costs | ~20% of costs | Frequent care users who want predictable costs |

| Platinum | ~90% of costs | ~10% of costs | High utilization; only POS plans available in Idaho at this tier |

Silver-tier plans hold a unique advantage on Your Health Idaho: enrollees with household income below 250% of the Federal Poverty Level ($39,125 for an individual using 2025 FPL for 2026 marketplace) qualify for cost-sharing reductions (CSRs) that lower deductibles, copays, and out-of-pocket maximums beyond what the premium subsidy provides. In 2025, 47% of Idaho marketplace enrollees had CSR-eligible Silver plans. CSRs are only available through the exchange — not from off-exchange plans.

The shift toward Bronze plans in 2026 reflects the enhanced subsidy expiration. With smaller tax credits, many Idaho health insurance marketplace enrollees who previously chose Silver or Gold plans downgraded to Bronze to keep monthly premiums manageable — accepting higher deductibles and out-of-pocket costs in exchange. For 2026, Bronze plans in Idaho also now qualify as high-deductible health plans (HDHPs) that can be paired with Health Savings Accounts (HSAs), adding a tax-advantaged savings option. The 2026 individual out-of-pocket maximum is $10,600, with $21,200 for family plans.

On-Exchange vs. Off-Exchange: When Going Direct Makes Sense

Idaho residents can purchase health insurance either through Your Health Idaho (on-exchange) or directly from a carrier (off-exchange). The key difference: premium tax credits and cost-sharing reductions are only available through the exchange. Off-exchange plans from Blue Cross of Idaho, Regence Blue Shield, and SelectHealth offer PPO options with broader networks that may be valuable for Idaho residents who don’t qualify for subsidies.

For anyone who qualifies for a premium tax credit — which includes Idaho households earning between 100% and 400% FPL ($15,650–$62,600 for an individual using 2025 FPL) under the 2026 formula — enrolling through the Idaho health insurance marketplace is almost always the better financial choice. The subsidy can only be applied to exchange plans, and it often reduces the monthly premium by hundreds of dollars. Per KFF, Idaho’s enhanced premium tax credits averaged approximately $407/month in 2025 — a level that will decline for many enrollees in 2026 as the enhanced credits expire.

The off-exchange option becomes relevant when an Idaho household earns above the subsidy threshold (above $62,600 for an individual or $128,600 for a family of four in 2026). Without a tax credit, on-exchange and off-exchange plans from the same carrier cost the same amount. At that point, off-exchange PPO plans may offer practical advantages: broader provider networks, no referral requirements, and out-of-network coverage. For rural Idaho residents — where the nearest specialist can be 100+ miles from home — PPO flexibility is particularly important. Compare PPO health insurance plans nationwide →

PPO carriers in Idaho: Blue Cross of Idaho, Regence Blue Shield, and SelectHealth offer PPO plans through both Your Health Idaho and direct enrollment. Mountain Health CO-OP and Moda Health Plan are primarily HMO carriers. Not all eight 2026 marketplace carriers serve every Idaho county — Boise metro typically has the most options, while rural counties may have fewer carriers available.

Special Enrollment: How to Get Idaho Coverage After Open Enrollment

If you missed open enrollment, you can still enroll in Idaho health insurance through a Special Enrollment Period (SEP) triggered by a qualifying life event such as losing coverage, getting married, having a baby, or moving Idaho zip codes. You generally have 60 days from the event to enroll through Your Health Idaho — or 90 days for loss of Idaho Medicaid (138% FPL, about $22,025 for a single adult), CHIP, or other government coverage.

Of the roughly 24,400 Idahoans who disenrolled from Your Health Idaho in early 2026, many became eligible to re-enroll under one of these qualifying life events. Qualifying life events that open a Special Enrollment Period on the Idaho health insurance marketplace include (with a 60-day window unless otherwise noted):

- Loss of coverage — losing employer insurance, aging off a parent’s plan at 26, exhausting COBRA, or losing Idaho Medicaid/CHIP eligibility

- Marriage or divorce — 60 days from the date of the event

- Birth or adoption — 60 days to add the child and adjust coverage

- Permanent move — moving to a new Idaho zip code or county where different plans are available (moving within the same zip code does not qualify)

- Income change affecting Idaho Medicaid eligibility — losing Idaho Medicaid opens a 90-day window to transition to marketplace coverage through Your Health Idaho

- Native American/Alaska Native enrollment — members of federally recognized tribes can enroll year-round without a qualifying life event

To enroll through a Special Enrollment Period, log into your Your Health Idaho account (or create one), report the qualifying life event, and upload supporting documentation such as a termination letter, marriage certificate, birth certificate, or proof of new Idaho address. Your Health Idaho verifies the documentation within 7–10 business days before you can select a plan, per Idaho Code Title 41 standards. Unlike HealthCare.gov states, all Idaho health insurance marketplace special enrollment applications are processed through the state system. For free help with the process, certified agents and Consumer Connectors across all 44 Idaho counties provide free assistance — call Your Health Idaho at 855-944-3246 or find a local agent at yourhealthidaho.org.

2026 change: Earning less than 150% of the Federal Poverty Level ($23,475 for an individual using 2025 FPL) is no longer a qualifying life event by itself. Previously, dropping below this threshold triggered a special enrollment period. Idahoans in this situation must now wait for the next open enrollment window or experience a different qualifying event. Idaho residents below 138% FPL ($22,025 for an individual using 2026 FPL) may qualify for Idaho Medicaid instead, which has year-round enrollment.

Example: Sarah in Twin Falls

Sarah, 32, works for a small employer in Twin Falls that doesn’t offer health insurance. She missed the December 15 open enrollment deadline. In February, she gets married. Her marriage is a qualifying life event — she has 60 days to create an account on Your Health Idaho, submit her marriage certificate, and select a plan. With a combined household income of $52,000, she qualifies for a premium tax credit that brings her Silver-plan premium from $512/month down to approximately $280/month.

Idaho Marketplace: Common Questions Answered

The most common Idaho health insurance marketplace questions cover the difference between Your Health Idaho and HealthCare.gov, open enrollment dates (October 15 through December 15), 2026 plan costs and subsidies for the roughly 117,000 enrollees, the 8 available carriers, and when residents can enroll through a Special Enrollment Period. Below are direct answers to the questions Idahoans ask most often before enrolling.

Is Your Health Idaho the same as HealthCare.gov?

No. Idaho operates its own state-based exchange at yourhealthidaho.org, separate from the federal HealthCare.gov marketplace. Idaho residents must enroll through Your Health Idaho to access marketplace plans and premium tax credits. If you visit HealthCare.gov as an Idaho resident, you’ll be redirected to the state site. Idaho is one of 21 states (plus DC) that operates its own exchange platform.

When is open enrollment for 2027 Idaho health insurance?

Open enrollment for 2027 coverage through the Idaho health insurance marketplace is expected to run from October 15 through December 15, 2026 — the same schedule Idaho has used since Your Health Idaho launched in 2014. Idaho has the earliest open enrollment start date of any state in the country.

Can I enroll in Idaho health insurance right now?

Outside of open enrollment (October 15 – December 15), you can only enroll if you experience a qualifying life event such as losing coverage, getting married, having a baby, or moving to a new Idaho zip code. Native Americans can enroll year-round. If you need coverage and don’t have a qualifying event, check whether you’re eligible for Idaho Medicaid, which has year-round enrollment for residents with income below 138% of the Federal Poverty Level ($22,025 for an individual using 2026 FPL).

How much does marketplace health insurance cost in Idaho?

Costs depend on the plan tier, your age, and whether you qualify for a premium tax credit. For a 40-year-old in 2026, Bronze plans start at approximately $349/month (St. Luke’s Health Plan) and Silver plans average around $481/month before subsidies. About 87% of Your Health Idaho enrollees received a tax credit averaging roughly $407/month in 2025 (per KFF). See the Idaho affordable health insurance page for detailed cost breakdowns by tier and age.

Do I have to use the marketplace, or can I buy insurance directly?

You can buy an identical ACA-compliant plan directly from carriers like Blue Cross of Idaho, Regence Blue Shield, or SelectHealth without going through Your Health Idaho. However, premium tax credits and cost-sharing reductions are only available through the exchange. If you earn between 100% and 400% of the Federal Poverty Level ($15,650–$62,600 for an individual using 2025 FPL for 2026 marketplace), the exchange is almost always the better financial choice. Off-exchange enrollment makes sense primarily for households above the subsidy threshold who want broader PPO networks.

What carriers offer plans on Your Health Idaho?

Eight carriers offer individual plans through Your Health Idaho for 2026: Blue Cross of Idaho, Regence Blue Shield of Idaho, SelectHealth, Mountain Health CO-OP, Moda Health Plan, PacificSource Health Plans, St. Luke’s Health Plan, and Molina Healthcare. These are the same eight that offered 2025 coverage. Not all carriers serve every Idaho county — availability depends on your zip code. Boise metro has the most options, while rural counties may have fewer carriers. Compare all 8 Idaho carriers →

Idaho Health Insurance Resources

Start Your 2026 Idaho Marketplace Enrollment

Compare 2026 plans from all 8 Your Health Idaho carriers — Blue Cross of Idaho, Regence Blue Shield, SelectHealth, Mountain Health CO-OP, St. Luke’s Health Plan, Molina, Moda, and PacificSource. Idaho’s reinsurance program reduces premiums by 18%, and 87% of Idahoans qualify for tax credits averaging roughly $407/month in 2025 (KFF). Free help available at 888-215-4045 or through Your Health Idaho’s 855-944-3246 line.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Idaho residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.