Small Business Health Insurance in Idaho: 2026 Group Plans & Employer Guide

Offering health insurance is one of the most effective ways for Idaho small businesses to attract and keep good employees — especially in a state where many rural communities have limited employer options. Small business health insurance Idaho employers can access features eight carriers, competitive rates that increased just 11% for 2026 per Idaho Department of Insurance Director Dean Cameron’s October 3, 2025 release, and multiple ways to structure coverage. This guide walks employers through group plan options, costs, tax credits, and alternatives like ICHRA and QSEHRA for businesses with 1 to 50 employees.

What brings you here today?

Idaho’s Small Group Health Insurance Market in 2026

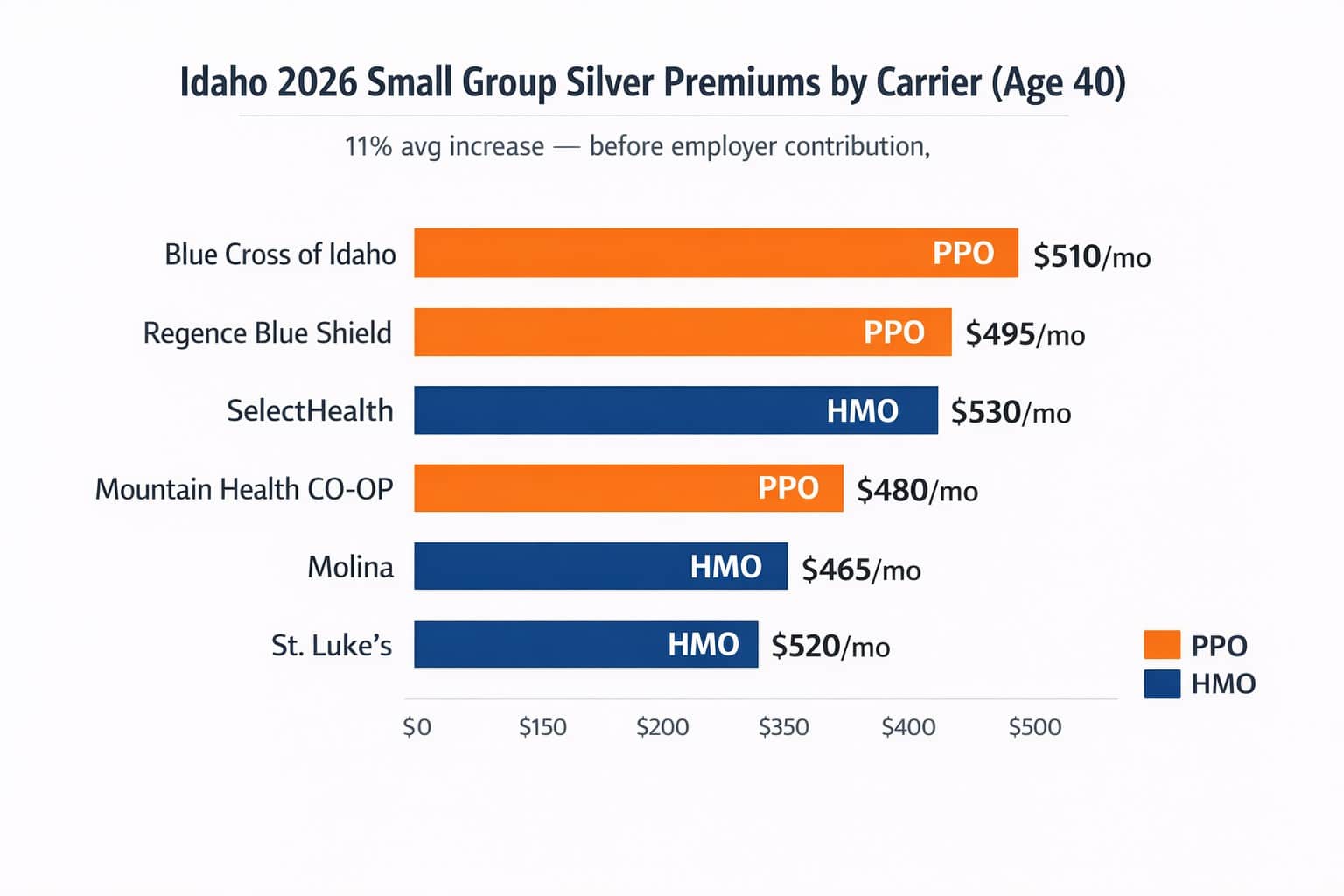

Idaho’s small group market serves businesses with 1 to 50 employees and features 8 carriers offering ACA-compliant group plans — Blue Cross of Idaho, Regence Blue Shield, SelectHealth, Mountain Health CO-OP, Molina, Moda, PacificSource, and St. Luke’s. The average small group rate increase for 2026 is 11%, per the Idaho Department of Insurance October 3, 2025 release. Idaho employers can buy group coverage directly from carriers, through SHOP via Your Health Idaho, or through a licensed broker.

Small business health insurance Idaho employers purchase through the state’s group market is regulated under the same ACA rules that apply nationwide: carriers must cover essential health benefits, cannot deny coverage based on employee health status, and must offer plans at all four metal tiers (Bronze, Silver, Gold, Platinum). However, unlike the individual market, Idaho’s reinsurance waiver does not apply to small group plans — so the 18% premium reduction that benefits individual market enrollees does not carry over to employer-sponsored coverage.

Idaho’s eight individual market carriers also participate in the small group market, though not all serve every county. Blue Cross of Idaho is the dominant small group carrier, serving all 44 counties with the broadest PPO network — covering 96% of Idaho physicians statewide. Regence Blue Shield and SelectHealth are also significant small group carriers in Idaho. For businesses in rural Idaho where carrier choice is limited to two or three options, Blue Cross of Idaho’s statewide coverage is often the default. The Idaho Department of Insurance Rate Review portal publishes carrier filings and rate justifications for the small group market.

Group Plan Types: PPO, HMO, and EPO for Idaho Employers

Idaho small businesses can choose between PPO, HMO, EPO, and POS group plans. PPO plans — offered by Blue Cross of Idaho, Regence Blue Shield, and SelectHealth — give employees the freedom to see any provider without referrals, especially valuable for Idaho businesses with employees spread across the state’s 83,569 square miles and 44 counties. HMO plans from Molina, Mountain Health CO-OP, and St. Luke’s offer lower premiums but restrict care to in-network providers.

The plan type decision carries extra weight for small business health insurance Idaho employers in rural areas. A Boise-based business with all employees in Ada County can comfortably choose an HMO — multiple carriers have strong in-network options within 15 miles. But a business with employees in Salmon, McCall, or the panhandle needs PPO flexibility so those workers can access specialists without driving 100+ miles to find an in-network provider.

Group PPO plans from Blue Cross of Idaho and Regence also provide out-of-state coverage through the national Blue Cross Blue Shield network. Idaho businesses with employees who travel for work or live near the Oregon, Washington, Utah, or Montana border benefit from this cross-state access. The State of Idaho itself chose a Regence PPO in July 2024 — and roughly 22,700 (about 85%) of its state employee plan enrollees use it per Idaho Capital Sun reporting. Compare Idaho PPO and HMO carriers and costs →

Group PPO

Carriers: Blue Cross of Idaho, Regence, SelectHealth

Referrals: Not required

Out-of-network: Covered at higher cost

Best for: Multi-location businesses, rural employers, companies with traveling employees

Group HMO

Carriers: Molina, Mountain Health CO-OP, St. Luke’s, SelectHealth

Referrals: Required for specialists

Out-of-network: Not covered (except emergencies)

Best for: Boise metro businesses, cost-conscious employers with strong local network options

What Small Business Health Insurance Costs in Idaho for 2026

Small group premiums in Idaho vary by carrier, plan type, metal tier, employee age mix, and county. For a 40-year-old employee, group Silver plan premiums typically range from $450 to $650/month before employer contributions. The 11% average rate increase for 2026 was driven by rising healthcare costs, prescription drug expenses (including weight-loss medications like Ozempic and Wegovy), and general medical inflation. Idaho employers typically pay 50%–80% of the employee-only premium across the state’s 44 counties.

| Business Size | Avg Monthly Premium (Employee Only) | Avg Employer Share (70%) | Avg Employee Share (30%) |

|---|---|---|---|

| Sole proprietor + 1 | $510/month (Silver) | $357 | $153 |

| 5 employees | $480–$550/month avg | $336–$385 | $144–$165 |

| 10 employees | $470–$540/month avg | $329–$378 | $141–$162 |

| 25 employees | $460–$530/month avg | $322–$371 | $138–$159 |

| 50 employees | $450–$520/month avg | $315–$364 | $135–$156 |

Larger groups generally get slightly better rates because the risk is spread across more employees. But in Idaho’s small group market, the difference between a 5-person and 50-person group is relatively modest — typically 5%–10% in premium variation. The bigger cost driver is the age mix of employees: a group with mostly younger workers pays significantly less than one with employees in their 50s and 60s. Small business health insurance Idaho employers purchase is community-rated within the small group market, but age bands create meaningful differences.

Compare Idaho Small Group Plans

See 2026 group plan options from Blue Cross of Idaho, Regence, and all available carriers in your county — with employer and employee cost splits calculated.

Small Business Tax Credits and Financial Incentives in Idaho

Idaho small businesses may qualify for the federal Small Business Health Care Tax Credit, which covers up to 50% of the employer’s premium contributions for qualifying businesses. To be eligible, an Idaho business must have fewer than 25 full-time equivalent employees, pay average annual wages of approximately $67,000 or less, and contribute at least 50% of employee-only premium costs. The credit must be claimed through SHOP enrollment via Your Health Idaho.

The Small Business Health Care Tax Credit is available for up to two consecutive years and is claimed by filing IRS Form 8941. The maximum credit is 50% of premium contributions for for-profit businesses and 35% for tax-exempt organizations. In practice, the credit phases out as business size and wages increase, so the smallest businesses with the lowest-paid employees receive the largest benefit.

To access the credit, Idaho businesses must enroll through the SHOP (Small Business Health Options Program) marketplace operated by Your Health Idaho. The Idaho process: email the SHOP application to [email protected] or mail to Your Health Idaho, P.O. Box 50143, Boise ID 83705 — Your Health Idaho then assigns a SHOP ID number, after which employers enroll directly with their chosen carrier. For SHOP help, Your Health Idaho’s customer line is 855-944-3246; certified Consumer Connectors statewide assist at no cost across all 44 Idaho counties.

SHOP eligibility requirements in Idaho

Your business must have 1–50 employees, offer coverage to all full-time employees (those averaging 30+ hours/week), enroll at least 70% of eligible employees, and have your office or employee work site located within Idaho. You can begin offering SHOP plans at any time of year — there’s no open enrollment restriction for employers. The federal SHOP marketplace guide provides additional information on eligibility requirements.

ICHRA and QSEHRA: Alternatives to Traditional Group Plans

Idaho small businesses finding traditional group plans too expensive have two federal alternatives: ICHRA (Individual Coverage HRA) and QSEHRA (Qualified Small Employer HRA). Both let Idaho employers reimburse employees tax-free instead of buying a group plan. These arrangements work especially well in Idaho — where Pat Kelly, Your Health Idaho’s executive director, reports 76% of 2026 enrollees received subsidies averaging $402/month, leaving net premiums near $108/month for many employees buying individually.

ICHRA

Employer size: Any (1–1,000+)

Monthly cap: No federal limit — employer sets the amount

Employee eligibility: Must have individual health insurance

Tax treatment: Tax-free for both employer and employee

Key advantage: Employees choose their own plan from Idaho’s 8 carriers and 158 marketplace plans; employer controls the budget with a fixed monthly reimbursement

QSEHRA

Employer size: Under 50 employees only

2026 monthly cap: $537.50/month individual ($6,450/year), $1,091.66/month family ($13,100/year)

Employee eligibility: Must have minimum essential coverage

Tax treatment: Tax-free for employer; may reduce employee’s premium tax credit

Key advantage: Simpler to administer than ICHRA; works well for very small Idaho businesses (under 10 employees) that can’t negotiate competitive group rates

Both ICHRA and QSEHRA are especially attractive for small business health insurance Idaho employers need when their workforce is spread across the state. Instead of choosing one group plan that may not have in-network providers in every employee’s county, the employer sets a reimbursement amount and each employee picks the individual plan that works best for their location. An employee in Boise might choose a low-cost St. Luke’s HMO, while an employee in Salmon picks a Blue Cross of Idaho PPO with statewide coverage — and the employer’s cost is the same fixed amount for both. See individual plan costs for Idaho employees →

How to Set Up Small Business Health Insurance in Idaho

Setting up group health insurance in Idaho involves four main steps: choosing a coverage structure (group plan, ICHRA, or QSEHRA), comparing carrier options in your county, enrolling through SHOP via Your Health Idaho or directly with a carrier, and onboarding employees. The process can begin at any time of year — unlike individual marketplace enrollment, there’s no open enrollment window for small group plans in Idaho’s 44 counties.

Choose a Coverage Structure

Decide between a traditional group plan (employer selects and partially funds one plan for all employees), an ICHRA (employer reimburses employees for individual plans they choose), or a QSEHRA (employer sets a fixed monthly reimbursement up to $537.50/month individual ($6,450/year) / $1,091.66/month family ($13,100/year) for 2026 per IRS Rev. Proc. 2025-32). A licensed broker can model the cost differences for your specific workforce in Idaho — this consultation is free.

Compare Idaho Carriers in Your County

Check which carriers serve your business location. Boise metro employers typically have 6–8 options; rural Idaho businesses may have 2–3. For multi-location businesses with employees across Idaho, Blue Cross of Idaho’s all-44-county PPO network avoids the problem of employees in different counties having no in-network options. Request quotes from at least three carriers.

Enroll Through SHOP or Directly

If pursuing the Small Business Health Care Tax Credit, you must enroll through Your Health Idaho’s SHOP program — complete the application, receive your SHOP ID, then enroll with your chosen carrier. If you don’t qualify for the tax credit, you can enroll directly with a carrier or through a broker, which is often faster and simpler.

Onboard Employees

Provide employees with plan details, enrollment forms, and contribution information. New employees typically have a 30–60 day waiting period before coverage begins. Idaho law follows the federal ACA standard requiring coverage for employees averaging 30+ hours per week. Businesses with 50+ full-time equivalent employees are subject to the employer mandate and face penalties for not offering affordable coverage.

Rural Idaho Business Challenges: Carrier Availability and Network Access

Idaho’s geography creates unique challenges for small business health insurance Idaho employers in rural areas face daily. With 44 counties spanning 83,569 square miles and a population concentrated in the Boise metro area, businesses outside Ada and Canyon counties often have fewer carrier choices and limited provider networks. KFF data on Idaho’s individual market shows Blue Cross of Idaho is the only carrier available in every county for both individual and small group coverage.

A construction company in Idaho Falls (Bonneville County) that employs workers across eastern Idaho faces a practical problem: SelectHealth exited Bonneville County for 2026, reducing PPO options. An agricultural business in the Magic Valley (Twin Falls, Jerome, Cassia counties) needs coverage that works for employees who may be 50+ miles from the nearest specialist. A logging operation in the panhandle (Boundary, Bonner counties) needs emergency coverage that extends across the Washington and Montana borders.

For these businesses, group PPO plans from Blue Cross of Idaho or Regence solve the geographic problem by letting employees see any provider — including across state lines — without referrals. The premium difference between a group HMO and group PPO in Idaho is typically $30–$60/month per employee at the Silver tier. For rural employers exploring small business health insurance Idaho carriers offer, that premium difference buys meaningful access that an HMO cannot match. Alternatively, ICHRA lets each employee choose the plan that works best for their specific county, shifting the network decision from the employer to the individual worker.

Idaho Small Business Health Insurance: Common Employer Questions Answered

The most common questions Idaho employers ask about small business health insurance Idaho rules cover the federal employer mandate (50+ FTEs only), minimum group size (1 employee), the 8 small group carriers serving Idaho’s 44 counties, plan flexibility (one plan vs. ICHRA), the federal Small Business Health Care Tax Credit (up to 50% via SHOP and IRS Form 8941), and the cost trade-offs between traditional group plans and ICHRA reimbursement arrangements.

Is small business health insurance required in Idaho?

Not for businesses with fewer than 50 full-time equivalent employees (FTEs). Small business health insurance Idaho law requires is limited to the federal ACA employer mandate, which applies only to businesses with 50+ FTEs — those employers must offer affordable minimum-value coverage or face penalties starting at approximately $3,340 per full-time employee (minus the first 30) for 2026. Idaho does not have a separate state employer mandate. Businesses under 50 FTEs can choose whether or not to offer coverage.

How many employees do I need to qualify for a group plan in Idaho?

Idaho’s small group market covers businesses with 1 to 50 employees. Even a sole proprietor with one W-2 employee can purchase a group plan. For SHOP enrollment through Your Health Idaho, you must enroll at least 70% of eligible employees and have your work site in Idaho. Businesses with no employees (sole proprietors only) can enroll as individuals through Your Health Idaho and may qualify for premium tax credits. Learn about individual enrollment through Your Health Idaho →

Which carriers offer small group plans in Idaho?

Blue Cross of Idaho, Regence Blue Shield, SelectHealth, Mountain Health CO-OP, Molina, Moda, PacificSource, and St. Luke’s all offer small group plans in Idaho — though carrier availability varies by county. Blue Cross of Idaho is the only carrier with small group plans available in all 44 counties. For businesses in rural counties, confirming carrier availability by zip code is essential before comparing costs.

Can I offer different plans to different employees?

With a traditional group plan, all employees are typically on the same plan or can choose from a small menu of options offered by the employer. With an ICHRA, each employee receives a fixed reimbursement and chooses their own individual plan — which means different employees can be on different carriers and different plan types based on their location and preferences. This flexibility makes ICHRA particularly useful for small business health insurance Idaho employers with workers spread across multiple counties.

What is the Small Business Health Care Tax Credit?

The federal tax credit covers up to 50% of the employer’s premium contributions (35% for tax-exempt organizations). To qualify, your business must have fewer than 25 FTEs, pay average wages of approximately $67,000 or less, and contribute at least 50% of employee-only premiums. You must enroll through Your Health Idaho’s SHOP program and claim the credit on IRS Form 8941. The credit is available for up to two consecutive years and phases out as business size and wages increase.

Is ICHRA or a group plan cheaper for my Idaho business?

It depends on your workforce. ICHRA tends to be more cost-effective when employees have varying healthcare needs (some want Bronze, others need Gold), when employees are spread across different Idaho counties with different carrier options, or when the employer wants to set a fixed budget regardless of premium increases. Traditional group plans tend to be better when all employees are in one location with strong carrier options and the employer wants to control the specific coverage offered. A licensed broker can model both scenarios for your specific business at no cost.

Idaho Health Insurance Resources

Find the Right Idaho Group Plan for Your Business

Licensed agents from ForHealthInsurance.com compare small business health insurance Idaho options from Blue Cross of Idaho, Regence, and all 8 carriers in your county across Idaho’s 44 counties — at no extra cost to your business.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Idaho residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.