Private Health Insurance in Arkansas 2026: Off-Exchange & PPO Plans

Private health insurance in Arkansas covers any individually purchased plan — whether through the HealthCare.gov marketplace or directly from a carrier off the exchange. For most Arkansans under 400 percent of the federal poverty level, the marketplace is the right starting point because premium tax credits make on-exchange plans far cheaper. For the roughly 12,000 middle- and upper-income Arkansans above that threshold, or for buyers who want PPO network access and year-round enrollment without an open enrollment window, private off-exchange coverage is often the better path. This guide covers who should skip the marketplace, what off-exchange PPO plans look like in Arkansas, HSA-eligible options, self-employed deductions, and how to enroll.

What are you looking for?

On-Marketplace vs Off-Marketplace Private Health Insurance in Arkansas

Both on-exchange and off-exchange plans qualify as private health insurance in Arkansas and must comply with all ACA requirements — essential health benefits, no pre-existing condition exclusions, no annual or lifetime limits. The single deciding factor for most buyers is subsidy eligibility. On-exchange plans access federal premium tax credits; off-exchange plans do not. Everything else — plan design, carrier options, ACA protections — is largely the same.

| Feature | On-Marketplace (HealthCare.gov) | Off-Marketplace (Direct) |

|---|---|---|

| Federal subsidy (APTC) access | ✅ Yes — if income 100–400% FPL | ❌ No |

| Cost-sharing reductions (CSR) | ✅ Yes — Silver plans, 138–250% FPL | ❌ No |

| Enrollment window | Nov 1 – Jan 15 (or SEP) | Year-round, any time |

| ACA essential health benefits | ✅ Required | ✅ Required |

| Pre-existing condition protection | ✅ Full ACA protection | ✅ Full ACA protection |

| PPO plan availability | Limited (2 carriers) | Broader selection |

| HSA-eligible plans | Some Bronze plans qualify | Yes — full HDHP lineup |

| Self-employed premium deduction | ✅ 100% deductible | ✅ 100% deductible |

The simple rule: If household income falls between 100 percent and 400 percent of the federal poverty level in 2026 and you’re not covered by an employer plan or Medicare, the marketplace is almost always cheaper after subsidies — even with the 46 percent Silver load. If income exceeds 400 percent FPL (about $63,840 single), or you need coverage outside the open enrollment window without a qualifying event, off-exchange private insurance is the right path.

Who Should Buy Private Health Insurance Off the Arkansas Marketplace

Four buyer groups in Arkansas consistently find off-marketplace private health insurance a better fit than the on-exchange lineup. The common thread: either the subsidy doesn’t apply, or the on-exchange HMO products don’t match their network needs.

| Buyer Profile | Why Off-Exchange Wins | Key Advantage |

|---|---|---|

| Income above 400% FPL (~$63,840 single) | No subsidy on or off exchange — sticker comparison only | PPO network, year-round enrollment |

| Self-employed / 1099 in Bentonville, Little Rock | 100% premium deduction applies either way; PPO better for specialist access | HSA-eligible HDHP + tax deduction |

| Missed open enrollment, no qualifying event | On-exchange enrollment closed until Nov 1; off-exchange open now | Immediate coverage, no wait |

| Need nationwide or out-of-state coverage | On-exchange HMOs restrict to AR network; PPO BlueCard works nationally | BlueCard coverage in all 50 states |

| Want specialist access without referrals | Most AR on-exchange plans are HMOs requiring PCP referrals | PPO direct specialist access |

| COBRA bridge between jobs | Off-exchange often cheaper than COBRA continuation premiums | ACA plan at lower cost than COBRA |

Scenario — Bentonville tech contractor, age 35, $85,000 income: Income at 532% FPL — no premium tax credit on or off the exchange. On-exchange Bronze HMO: ~$450/mo with in-state-only network. Off-exchange ArkBCBS PPO Bronze: ~$486/mo with BlueCard nationwide coverage and no referral requirements. Cost difference: ~$36/mo for a plan that covers specialist visits in Dallas or Chicago without a referral. For a contractor who travels between Arkansas, Texas, and Illinois for clients, the PPO math is clear.

HSA-Eligible Plans for Private Health Insurance in Arkansas

Health Savings Accounts (HSAs) are one of the most tax-efficient tools available to self-employed Arkansans and individuals buying private health insurance. An HSA works alongside a qualifying High-Deductible Health Plan (HDHP): contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free — a triple tax advantage unavailable with any other savings vehicle.

| HSA Detail | 2026 Figure | Notes |

|---|---|---|

| Individual HSA contribution limit | $4,300 | IRS 2026 limit |

| Family HSA contribution limit | $8,550 | IRS 2026 limit |

| Catch-up contribution (age 55+) | +$1,000 | Added to individual or family limit |

| Minimum HDHP deductible (individual) | $1,650 | IRS 2026 threshold |

| Minimum HDHP deductible (family) | $3,300 | IRS 2026 threshold |

| HDHP out-of-pocket max (individual) | $8,300 | IRS 2026 limit |

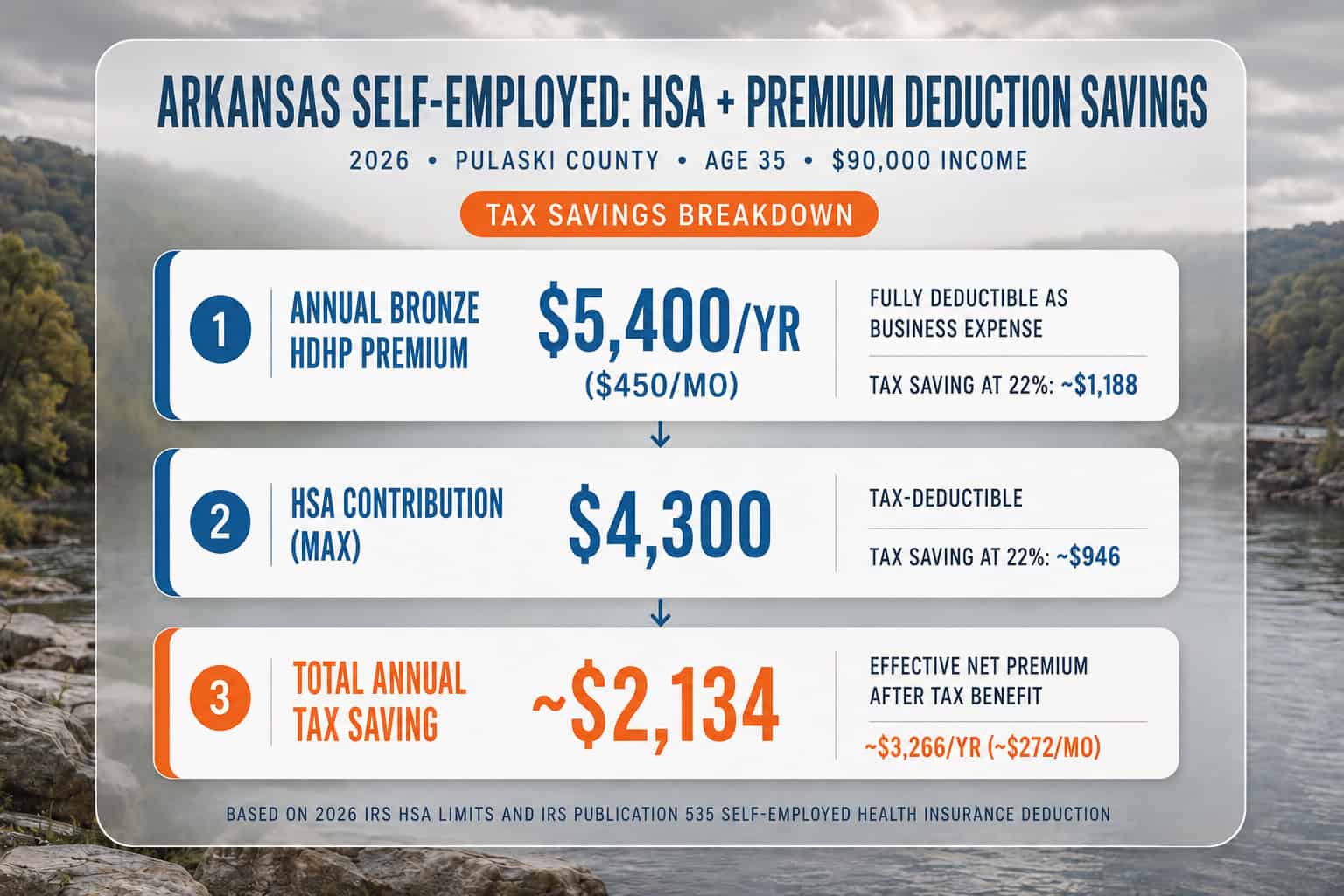

Most Bronze plans in Arkansas meet the HDHP deductible threshold — the average Arkansas Bronze deductible of $7,180 far exceeds the $1,650 minimum. Arkansas buyers pairing a Bronze HDHP with an HSA can contribute up to $4,300 pre-tax in 2026, reducing effective coverage costs significantly. A 35-year-old in Pulaski County on an off-exchange Bronze HDHP at $450/mo who maxes out an HSA at $4,300 reduces taxable income by $4,300 — a $946 federal tax saving at a 22 percent marginal rate, partially offsetting the annual premium cost of $5,400.

HSA + self-employed premium deduction combined: A self-employed Arkansas resident buying a private Bronze HDHP can deduct 100 percent of the annual premium as a business expense (IRS Publication 535) and contribute $4,300 to an HSA. On a $90,000 net self-employment income, those two deductions alone reduce federal taxable income by roughly $9,700 — saving approximately $2,100 in federal taxes at a 22 percent marginal rate. This combination is not available to W-2 employees on employer plans.

Get a Private Health Insurance Quote for Arkansas

Compare off-marketplace PPO plans and HSA-eligible options side by side with on-exchange alternatives. ForHealthInsurance.com runs both comparisons in one quote — licensed brokers, no extra cost, year-round enrollment.

Get a Quote Call 888-215-4045How to Enroll in Private Health Insurance in Arkansas

Enrolling in off-marketplace private health insurance in Arkansas has no enrollment window — coverage is available any day of the year. The process is simpler than HealthCare.gov enrollment: no subsidy application, no income verification. The Arkansas Insurance Department rate tool lists 2026 carrier rates by county. A licensed broker quotes multiple carriers and submits the application in one session.

- Determine whether off-exchange makes sense. If household income falls between 100 percent and 400 percent FPL and you don’t need immediate coverage outside the open enrollment window, run an on-exchange comparison first using the HealthCare.gov premium subsidy estimator. The 46 percent Silver load may mean a Gold plan on the marketplace beats any off-exchange option on after-subsidy cost. If income exceeds 400 percent FPL or you need coverage today, proceed with off-exchange.

- Choose a carrier and plan type. Arkansas BlueCross BlueShield offers the broadest statewide PPO network with BlueCard nationwide coverage. Ambetter offers a competitive PPO lineup in Pulaski, Benton, and Washington counties. For HSA-eligible HDHP coverage, most Bronze plans from either carrier qualify.

- Confirm your coverage start date. Off-exchange plans typically start the first of the month following enrollment, though some carriers offer mid-month start dates. There is no December 15 deadline or January 1 requirement.

- Complete the carrier application. Requires basic demographic information, current address, Social Security number, and payment method. No income documentation required (no subsidy to verify). Most applications are approved same-day or within 24 hours.

- Set up your HSA if applicable. Open an HSA at a bank or financial institution once your HDHP coverage is active. Contributions can begin the first month coverage is effective. Keep contributions at or below the 2026 IRS limits ($4,300 individual, $8,550 family).

The IRS Publication 535 covers the self-employed health insurance deduction in full. The IRS Publication 969 covers HSA rules and contribution limits. Both apply to Arkansas residents buying private individual coverage regardless of carrier or metal tier.

Private Health Insurance Costs in Arkansas — Off-Exchange vs On-Exchange

For buyers who receive no subsidy, the cost comparison between on-exchange and off-exchange private health insurance in Arkansas comes down to plan design and network. Sticker prices are often similar because carriers price on and off the exchange using the same actuarial base — the primary differences are PPO availability and plan variety. The table below compares representative 2026 options for a 40-year-old in Pulaski County with no subsidy.

| Plan | Type | Monthly Premium | Deductible | Network |

|---|---|---|---|---|

| Octave Exp. Bronze (on-exchange) | POS | ~$345/mo | ~$7,500 | AR BCBS in-state |

| Health Advantage Bronze (on-exchange) | HMO | ~$470/mo | ~$7,180 | AR BCBS in-state HMO |

| ArkBCBS Bronze PPO (off-exchange) | PPO | ~$486/mo | ~$7,000 | BlueCard — nationwide |

| Ambetter Bronze PPO (off-exchange) | PPO | ~$547/mo | ~$6,469 | Centene network + OON |

| Ambetter Gold PPO (off-exchange) | PPO | ~$731/mo | ~$1,022 | Centene + OON, low deductible |

For a buyer who needs nationwide coverage — a traveling consultant between Little Rock and Dallas, or a Bentonville professional working with national retail clients — the $141/mo premium difference between Octave’s POS plan and ArkBCBS’s PPO represents about $1,692/year for BlueCard access in all 50 states. Whether that’s worth it depends on how often out-of-state care is actually needed. Not sure whether a PPO or HMO fits your situation? The PPO vs HMO comparison guide breaks down the network and cost trade-offs in detail. For buyers who stay in Arkansas and stay in-network, Octave’s POS plan is nearly always the cheapest option.

Frequently Asked Questions About Private Health Insurance in Arkansas

What is private health insurance in Arkansas?

Private health insurance in Arkansas refers to individually purchased ACA-compliant plans bought through the HealthCare.gov marketplace or directly from a carrier off the exchange. Both types cover the 10 ACA essential health benefits and carry no pre-existing condition exclusions. On-marketplace plans can access federal premium tax credits; off-marketplace plans cannot — but enroll year-round without a qualifying life event requirement.

Can I buy individual health insurance in Arkansas outside of open enrollment?

Yes. Off-marketplace individual health insurance in Arkansas is available year-round — no open enrollment window and no qualifying life event required. On-marketplace coverage through HealthCare.gov is limited to the November 1 through January 15 open enrollment window or a Special Enrollment Period. Arkansas residents who miss open enrollment without a qualifying event can purchase ACA-compliant off-exchange coverage immediately.

Who should buy private health insurance off the Arkansas marketplace?

Off-marketplace private health insurance in Arkansas makes the most sense for buyers earning above 400 percent of the federal poverty level (about $63,840 single in 2026) who receive no premium tax credit; buyers who want PPO network access beyond the HMO-heavy on-exchange lineup; self-employed Arkansans who want an HSA-eligible plan with a 100 percent premium deduction; and buyers who need coverage immediately outside the open enrollment window.

Can self-employed Arkansans deduct health insurance premiums?

Yes. Self-employed Arkansas residents — sole proprietors, single-member LLC owners, S-corp shareholders, and 1099 contractors — can deduct 100 percent of health insurance premiums paid for themselves, a spouse, and dependents as an above-the-line deduction on federal taxes under IRS Publication 535. This deduction applies whether the plan is purchased on or off the marketplace and does not require itemizing.

Are HSA-eligible plans available for private health insurance in Arkansas?

Yes. HSA-eligible High-Deductible Health Plans are available both on and off the Arkansas marketplace. A plan qualifies as HDHP if the deductible meets the 2026 IRS minimum of $1,650 for individual coverage. Most Arkansas Bronze plans exceed this threshold. The 2026 HSA contribution limit is $4,300 for individual coverage and $8,550 for family coverage, with a $1,000 catch-up for those 55 and older.

Related Arkansas Health Insurance Resources

Explore the rest of the Arkansas guide — the statewide overview, small business coverage, affordability, carrier comparisons, and the individual marketplace.

Full 2026 overview — ARHOME, ARKids, marketplace, and all coverage paths.

Arkansas Small BusinessGroup PPO, ICHRA, and QSEHRA options for Arkansas employers.

Arkansas Costs & Silver LoadAfter-subsidy pricing by income and why Gold beats Silver in 2026.

Best Arkansas Health PlansAll 6 carriers compared — premium, quality, network, and PPO availability.

Arkansas MarketplaceEnrollment windows, deadlines, and subsidy eligibility on HealthCare.gov.

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required.

Get Private Health Insurance Quotes for Arkansas

ForHealthInsurance.com compares off-marketplace PPO plans, HSA-eligible Bronze options, and on-exchange alternatives side by side. Year-round enrollment, licensed Arkansas brokers, no extra cost.

Get a Quote Call 888-215-4045Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Arkansas residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.