Small Business Health Insurance in Connecticut 2026: Group Plans, SHOP, ICHRA & Mini-COBRA

Small business health insurance in Connecticut runs through more paths than most states — traditional small group plans from five or more carriers, the Access Health CT SHOP marketplace for the federal tax credit, ICHRA for employer-defined dollar allowances, and QSEHRA for the smallest teams. Only 27 percent of Connecticut businesses with fewer than 50 employees currently offer health benefits — well below the 55 percent national average — a gap that creates a meaningful competitive advantage for employers who do. Small group rates increased about 11 percent for 2026, compared to the 16.8 percent individual market increase. This guide covers the full Connecticut small business health insurance landscape — carrier options, SHOP, ICHRA, mini-COBRA, the tax credit, and how to choose the right structure for a Connecticut employer in 2026.

What does your business need?

Connecticut Small Business Coverage Options at a Glance

Connecticut small employers have four main coverage structures for small business health insurance in Connecticut in 2026: traditional group plans from five or more carriers, the Access Health CT SHOP marketplace for the federal tax credit, ICHRA for employer-defined dollar allowances, and QSEHRA for the smallest teams. Connecticut’s SHOP marketplace remains active with carrier participation — a meaningful advantage for employers pursuing the two-year federal tax credit, since many states have lost SHOP carrier participation entirely.

| Option | Who It Fits | 2026 Cost Control | Tax Credit Available? |

|---|---|---|---|

| Traditional group plan | 10–50 employees; stable workforce | Shared premium; fixed renewal | Only through SHOP (2 yr max) |

| SHOP marketplace (Access Health CT) | Under 50 FTEs seeking tax credit | Group plan via AHCT SHOP portal | ✅ Up to 50% of premiums |

| ICHRA | Any size; variable or multi-county workforce | Fixed monthly allowance per employee | No direct credit; fully tax-deductible |

| QSEHRA | Under 50 FTEs; no existing group plan | Capped: $529.17/mo individual, $1,066.67/mo family | No direct credit; tax-deductible |

Group Plan Costs and Carriers in Connecticut for 2026

Connecticut’s small group market for small business health insurance in Connecticut features a broader carrier lineup than the two-carrier individual marketplace — Anthem BCBS CT, ConnectiCare, Harvard Pilgrim, Cigna, and UnitedHealthcare all compete for small employer business. Small group rates increased approximately 11 percent for 2026, well below the 16.8 percent individual market increase. Fairfield County premiums typically run higher than Hartford County due to provider contracting and network pricing differences.

| Coverage Level | Avg Annual Employer Cost | Avg Monthly per Employee | Typical Employer Share |

|---|---|---|---|

| Single (employee-only) | ~$7,500–$8,500/yr | ~$625–$710/mo | ~84% of premium |

| Family coverage | ~$22,000–$26,000/yr | ~$1,833–$2,167/mo | ~75% of premium |

| 2026 small group rate increase | ~11% over 2025 | — | — |

| Fairfield County vs Hartford premium diff. | ~10–15% higher in Fairfield | ~$60–$100/mo premium variance | — |

Group enrollment is year-round in Connecticut: Unlike the individual marketplace which runs on an annual open enrollment schedule, small group health insurance in Connecticut is not tied to an annual enrollment date — employers can start group coverage on a rolling basis any month of the year. This makes offering coverage more accessible for new or growing Connecticut businesses that did not plan around a November enrollment window.

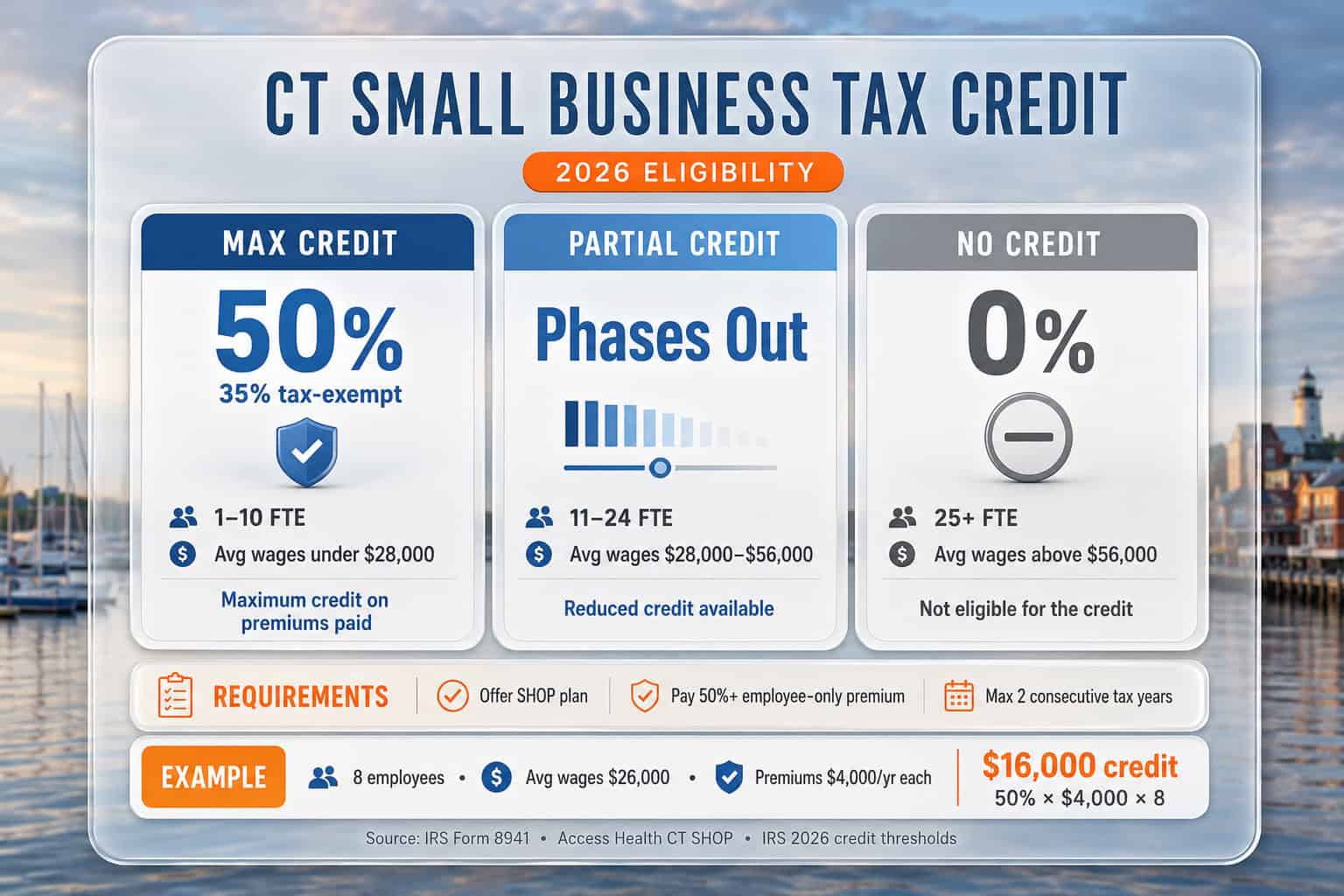

The SHOP Marketplace and Small Business Tax Credit in Connecticut

Access Health CT operates a SHOP marketplace for small employers — and unlike many states that lost SHOP carrier participation, Connecticut’s SHOP remains active with participating carriers. The SHOP marketplace is the gateway to the federal Small Business Health Care Tax Credit, which covers up to 50 percent of premiums paid for qualifying employers. To claim the credit, coverage must be purchased through a SHOP plan — direct-to-carrier group plans do not qualify.

| Criterion | Maximum Credit Threshold | Phase-Out Ceiling |

|---|---|---|

| FTE employee count | 10 or fewer | 25 FTEs (credit fully phases out) |

| Average annual wages | Below ~$28,000 | ~$56,000 (credit fully phases out) |

| Employer premium contribution | 50%+ of employee-only premium | Required for any credit |

| Plan type | SHOP plan required | Direct-to-carrier plans do not qualify |

| Maximum credit (for-profit) | 50% of premiums paid | 2 consecutive years only |

| Maximum credit (tax-exempt) | 35% of premiums paid | 2 consecutive years only |

Scenario — New Britain retailer, 8 employees, avg wages $26,000: This employer qualifies for the maximum 50 percent credit. If premiums run $4,000 per year per employee, total annual premium outlay is $32,000. The two-year tax credit value: $16,000 per year × 2 years = $32,000 in total federal tax credits. After the two-year credit period ends, the employer can evaluate whether ICHRA provides better long-term cost structure. The SHOP route is most valuable for the first two years; the credit disappears after that and the full group premium cost applies.

Get a Small Business Health Insurance Quote for Connecticut

ForHealthInsurance.com compares Connecticut direct-to-carrier group plans, SHOP options, and ICHRA structures for small employers — checking tax credit eligibility at no extra cost. Licensed brokers, no carrier preference.

Get a Quote Call 888-215-4045ICHRA — The Modern Alternative for Connecticut Employers

Connecticut employers with staff spread across Fairfield County, Hartford, and New Haven — where premiums and network fit vary widely by region — increasingly choose ICHRA over a single traditional group plan for small business health insurance in Connecticut. An ICHRA lets the employer set a fixed monthly allowance per employee class; each employee then shops for their own plan through Access Health CT or off-exchange and submits premiums for tax-free reimbursement. The Department of Labor EBSA guide covers ICHRA and QSEHRA rules alongside group plan obligations.

| Feature | Traditional Group Plan | ICHRA |

|---|---|---|

| Employer contribution cap | Open-ended (% of premium) | Fixed allowance set by employer |

| Employee plan choice | Employer selects plan(s) | Each employee chooses own plan |

| IRS contribution cap (2026) | No cap | No cap |

| Tax treatment | Employer deducts premiums | Reimbursements tax-free for both |

| Participation minimums | Yes — typically 70% of eligible | None |

| Multi-county workforce | Single plan, varied network fit | Each employee picks local plan |

| Subsidy interaction | Employees ineligible for marketplace subsidies | Ineligible if ICHRA is affordable |

| Access Health CT integration | Through SHOP portal | Employees can use AHCT marketplace |

For Connecticut employers with employees in Fairfield County earning above the subsidy threshold alongside Hartford employees who qualify for marketplace credits, ICHRA’s class-based contribution structure can be set to allow lower-income employees to retain marketplace subsidy eligibility. Employees can shop through the Access Health CT marketplace guide to find plans that work with their ICHRA allowance. See the Connecticut private health insurance guide for how affordability thresholds interact with ICHRA design.

Connecticut Mini-COBRA and ACA Employer Rules

Connecticut small employers face two distinct sets of continuation coverage rules. Federal COBRA covers employers with 20 or more employees — requiring continuation coverage after qualifying events for up to 18 months. Connecticut’s state mini-COBRA law extends comparable protections to employees of businesses with fewer than 20 workers, filling the gap federal COBRA leaves. This makes Connecticut one of a minority of states that protects small employer employees from losing coverage without a continuation option.

| Rule | Applies To | Duration | Cost to Employee |

|---|---|---|---|

| Federal COBRA | Employers with 20+ employees | Up to 18 months | Full premium + 2% admin fee |

| Connecticut mini-COBRA | Employers with fewer than 20 employees | Up to 18 months | Full premium + small admin fee |

| ACA employer mandate | 50+ FTE employers (ALEs) | Ongoing obligation | Employer pays; 9.96% affordability threshold |

| Offering coverage (under 50 FTEs) | Optional | — | Employer sets contribution |

The ACA employer shared responsibility mandate applies only to Connecticut businesses with 50 or more full-time equivalent employees. Businesses under that threshold — the vast majority of Connecticut small employers in Bridgeport, New Haven, Hartford, and the Fairfield County suburbs — face no legal requirement to offer coverage. The competitive case for offering small business health insurance in Connecticut comes from the state’s tight labor markets: Access Health CT small business research shows only 27 percent of Connecticut small employers offer health benefits, meaning employers who do offer coverage stand out significantly. The IRS Form 8941 is used to claim the SHOP tax credit at filing.

Frequently Asked Questions About Connecticut Small Business Coverage

Are Connecticut small businesses required to offer health insurance?

No. Connecticut employers with fewer than 50 full-time equivalent employees are not required by the ACA to offer health insurance. The employer mandate applies only to businesses with 50 or more FTEs. Only 27 percent of Connecticut businesses with fewer than 50 employees currently offer coverage — well below the 55 percent national average — meaning employers who do offer small business health insurance in Connecticut stand out in competitive hiring markets like Hartford, Stamford, Bridgeport, and New Haven.

What is Connecticut mini-COBRA?

Connecticut mini-COBRA is a state law extending COBRA-like continuation coverage rights to employees of businesses with fewer than 20 workers — a population federal COBRA does not cover. Under Connecticut mini-COBRA, employees who lose employer-sponsored coverage due to job loss, reduced hours, or other qualifying events can continue their group coverage for up to 18 months by paying the full premium plus a small administrative fee. Connecticut is one of a minority of states with this protection for small business employees.

How does the small business health care tax credit work in Connecticut?

The Small Business Health Care Tax Credit covers up to 50 percent of premiums for Connecticut employers with fewer than 25 FTE employees, average wages below approximately $56,000, and payment of at least 50 percent of employee-only premium costs through a SHOP plan. The credit is available for two consecutive tax years only and is most valuable for employers with 10 or fewer employees averaging wages below $28,000. Tax-exempt organizations qualify for 35 percent.

What is ICHRA and how does it work for Connecticut small businesses?

An ICHRA lets Connecticut employers of any size reimburse employees tax-free for individual health insurance premiums up to a fixed monthly allowance — with no IRS cap. Each employee buys their own ACA-compliant plan through Access Health CT or off-exchange. ICHRA works well for Connecticut businesses with employees in multiple counties where carrier network preferences differ, eliminating group plan participation minimums, annual renewal risk, and COBRA obligations.

How much does small business health insurance cost in Connecticut?

Small group health insurance in Connecticut increased approximately 11 percent for 2026, below the 16.8 percent individual market increase. Average employer cost for employee-only coverage runs $625 to $710 per month, with employers typically covering about 84 percent of the single-coverage premium. Fairfield County premiums trend 10–15 percent higher than Hartford County due to provider contracting — an important consideration for businesses in Stamford, Greenwich, or Westport.

Related Connecticut Health Insurance Resources

Explore the rest of the Connecticut guide — the statewide overview, affordability, carrier comparisons, the Access Health CT marketplace, and private off-exchange options.

The complete guide to health insurance options across Connecticut for 2026.

Affordable Connecticut CoverageHow subsidies and Covered Connecticut lower premiums for those who qualify.

Best Health Insurance in ConnecticutAnthem, ConnectiCare, and Cigna compared on price and provider network.

Connecticut MarketplaceEnrollment windows, deadlines, and subsidies on the Access Health CT marketplace.

CT Private & Off-ExchangeOff-exchange and private plan options for Connecticut residents wanting flexibility.

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required.

Get Small Business Health Insurance Quotes for Connecticut

ForHealthInsurance.com compares Connecticut group plans, SHOP options, and ICHRA structures for small employers — checking tax credit eligibility and QSEHRA limits in one session. Licensed brokers, no carrier preference, no extra cost.

Get a Quote Call 888-215-4045Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Connecticut businesses. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.