Private Health Insurance in Connecticut 2026: Off-Exchange PPO & Individual Plans

Private health insurance in Connecticut covers any individually purchased ACA-compliant plan — whether through Access Health CT or directly from a carrier off the exchange. For most Connecticut residents earning below 500 percent of the federal poverty level, the marketplace is the right starting point because Covered CT, state Temporary Premium Assistance, and federal premium tax credits make on-exchange plans significantly cheaper. For the substantial population above that threshold — especially in Fairfield County, Greenwich, Stamford, and Westport where household incomes routinely exceed $100,000 — private off-exchange coverage typically delivers better value than sticker-priced on-exchange HMOs. This guide covers who should buy private health insurance in Connecticut off the marketplace, what off-exchange plans cost, HSA options, self-employed deductions, and why Anthem PPO matters more in Connecticut than in most states.

What are you looking for?

On-Marketplace vs Off-Marketplace Private Health Insurance in Connecticut

Both on-exchange and off-exchange plans qualify as private health insurance in Connecticut with full ACA protections. The deciding factor is subsidy eligibility. On-exchange plans through Access Health CT access federal tax credits, Covered CT, and state Temporary Premium Assistance — worth hundreds per month for eligible buyers. Off-exchange plans access none of those programs but enroll year-round and offer Anthem PPO with BlueCard nationwide network that on-exchange HMOs cannot match.

| Feature | On-Marketplace (Access Health CT) | Off-Marketplace (Direct from Anthem) |

|---|---|---|

| Federal subsidy (APTC) access | ✅ Yes — if income 100–400% FPL | ❌ No |

| Covered CT ($0 coverage) | ✅ Yes — 138–175% FPL | ❌ No |

| State Temporary Assistance | ✅ Yes — 100–200% and 400–500% FPL | ❌ No |

| Enrollment window | Nov 1 – Jan 31 (or SEP) | Year-round, any time |

| ACA essential health benefits | ✅ Required | ✅ Required |

| PPO plan availability | Anthem PPO only | Anthem PPO — full lineup |

| BlueCard nationwide network | On Anthem PPO plans | On Anthem PPO plans |

| HSA-eligible HDHP plans | Some Bronze plans qualify | Full HDHP lineup available |

| Self-employed premium deduction | ✅ 100% deductible | ✅ 100% deductible |

The Connecticut subsidy threshold: Unlike most states where the on-exchange vs off-exchange decision hinges at 400% FPL (~$62,600 single), Connecticut’s Temporary Premium Assistance extends partial help through 500% FPL (~$78,250 single). Buyers between 400–500% FPL should call Access Health CT at 1-855-805-4325 before going off-exchange — the state assistance may make the marketplace cheaper than it appears online. For full enrollment details on the state exchange, see the Access Health CT marketplace guide.

Who Should Buy Private Health Insurance Off the Connecticut Marketplace

Private health insurance in Connecticut off the marketplace makes the most sense for buyers who either receive no subsidy or need year-round enrollment flexibility. Connecticut’s layered subsidy programs — Covered CT, federal APTC, and Temporary Premium Assistance — cover the vast majority of residents under 500 percent FPL. The buyers for whom off-exchange is genuinely the better path fall into four clear groups.

| Buyer Profile | Why Off-Exchange Wins | Key Advantage |

|---|---|---|

| Income above 500% FPL (~$78,250 single) | No subsidy on or off exchange — sticker comparison only | PPO network; year-round enrollment |

| Self-employed in Fairfield County / Stamford | 100% premium deduction either way; PPO needed for NYC specialists | BlueCard covers NYC hospitals in-network |

| Missed OEP, no qualifying event | Access Health CT enrollment closed until Nov 1; off-exchange open now | Immediate coverage, no wait |

| Need nationwide or NYC coverage | On-exchange HMOs restrict to CT network; Anthem PPO BlueCard works nationally | BlueCard covers 95% of U.S. News Best Hospitals |

| Want specialist access without referrals | Most CT on-exchange plans are HMO/POS requiring PCP referrals | PPO direct specialist access |

| COBRA bridge between jobs | Off-exchange often cheaper than COBRA continuation premiums | Full ACA coverage at lower cost than COBRA |

The Stamford Health network dispute — March 2026: In March 2026, Stamford Health announced a potential exit from UnitedHealthcare commercial networks, affecting HMO enrollees who had no out-of-network coverage path. HMO plans cover out-of-network care only in emergencies — a network dispute leaves HMO members choosing between paying full out-of-pocket rates or traveling to in-network facilities. Anthem PPO holders faced no such constraint: the BlueCard out-of-network benefit covers non-emergency care at a known cost share regardless of local network disruptions. For Fairfield County buyers, PPO’s out-of-network protection is not theoretical — it’s a documented 2026 risk in their own county.

Off-Exchange vs On-Exchange Cost Comparison for Connecticut Buyers

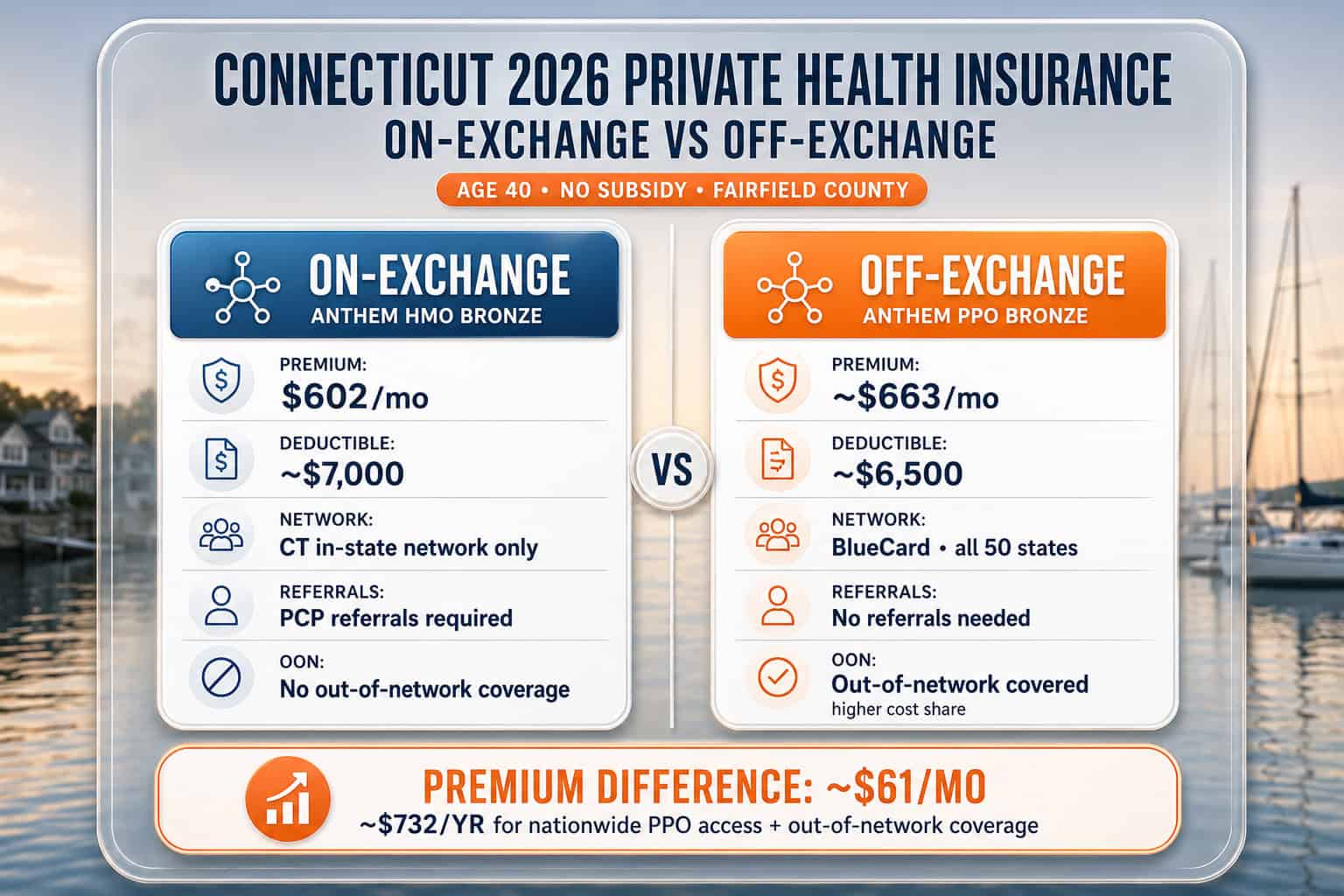

For buyers who receive no subsidy, the cost comparison between on-exchange and off-exchange private health insurance in Connecticut comes down to plan type and network. Anthem prices its on-exchange HMO and off-exchange PPO products using similar actuarial bases — the premium difference between an on-exchange HMO and an off-exchange PPO for the same metal tier is often $60–$130 per month, representing the cost of PPO flexibility and BlueCard nationwide access.

| Plan | Type | Monthly Premium (Age 40) | Deductible | Network |

|---|---|---|---|---|

| Anthem Bronze HMO (on-exchange) | HMO | ~$602/mo | ~$7,000 | Connecticut only — referrals required |

| Anthem Silver PPO (on-exchange) | PPO | ~$729/mo | ~$4,802 | CT + BlueCard nationwide |

| Anthem Bronze PPO (off-exchange) | PPO | ~$663/mo | ~$6,500 | CT + BlueCard nationwide |

| Anthem Gold PPO (off-exchange) | PPO | ~$988/mo | ~$2,000 | CT + BlueCard nationwide |

| ConnectiCare Bronze POS (on-exchange) | POS | ~$719/mo | ~$6,800 | Hartford + New Haven focused |

Scenario — Greenwich hedge fund analyst, age 38, $185,000 income: Income at 1,159% FPL — no subsidy of any kind. On-exchange Anthem HMO Bronze: $602/mo, CT-only network, referrals required. Off-exchange Anthem PPO Bronze: ~$663/mo, BlueCard covers New York-Presbyterian and NYU Langone as in-network facilities. Monthly difference: $61. Annual difference: $732 for nationwide PPO access and direct specialist visits at Manhattan cardiologists, orthopedic surgeons, and oncology centers without navigating a Connecticut HMO referral chain. For a high-income professional, the math is clear.

Get a Private Health Insurance Quote for Connecticut

ForHealthInsurance.com compares off-marketplace Anthem PPO plans and HSA-eligible options side by side with on-exchange alternatives — checking subsidy eligibility first. Licensed Connecticut brokers, year-round enrollment, no extra cost.

Get a Quote Call 888-215-4045HSA Plans and Self-Employed Deductions for Connecticut Buyers

Self-employed Connecticut residents — particularly the large 1099 and LLC professional population in Fairfield County — have access to two overlapping tax advantages that make private health insurance significantly cheaper on an after-tax basis. The 100 percent federal self-employed health insurance deduction and the HSA triple tax benefit can together reduce effective annual coverage costs by $2,000–$4,000 depending on income bracket and plan selection.

| Tax Benefit | 2026 Amount | Requirement | CT State Tax |

|---|---|---|---|

| Self-employed premium deduction | 100% of premiums paid | Net self-employment income; IRS Pub 535 | CT conforms — deductible on state return |

| HSA individual contribution limit | $4,300 | Must be on qualifying HDHP | CT conforms — state tax deductible |

| HSA family contribution limit | $8,550 | Family HDHP coverage | CT conforms — state tax deductible |

| HSA catch-up (age 55+) | +$1,000 | Age 55 or older | CT conforms |

| HDHP minimum deductible (individual) | $1,650 | IRS 2026 threshold for HSA eligibility | — |

Connecticut is one of the states that fully conforms to federal HSA tax treatment — contributions are deductible on both federal and Connecticut state income tax returns under Connecticut Department of Revenue Services rules. The self-employed premium deduction is governed by IRS Publication 535. Most Bronze plans in Connecticut qualify as HDHPs since average deductibles of $6,500–$7,000 far exceed the $1,650 IRS minimum. A Stamford LLC owner on an off-exchange Bronze HDHP at $663/mo who maxes out the HSA at $4,300 deducts both the $7,956 annual premium and $4,300 HSA contribution — reducing federal and state taxable income by $12,256 total.

CT state tax deductibility: Connecticut conforms to federal HSA treatment, meaning contributions to an HSA are deductible on the Connecticut Form CT-1040 just as they are federally. This is not universal — some states like California and New Jersey do not recognize HSA deductions. Connecticut’s conformity means the HSA benefit applies at both the federal and state level, increasing the effective tax saving for Connecticut residents in the 6.99% top marginal state bracket.

How to Enroll in Private Health Insurance in Connecticut Off the Marketplace

Off-marketplace private health insurance in Connecticut enrolls year-round directly through Anthem — no access to Access Health CT required, no open enrollment window, no qualifying event needed. The enrollment process is simpler than the marketplace because no subsidy application is involved. Coverage typically starts the first of the month following enrollment, though some plans offer mid-month starts.

Confirm off-exchange is the right path

Run a subsidy check first using the KFF subsidy calculator. If income falls below 500 percent FPL, call Access Health CT at 1-855-805-4325 to check Temporary Premium Assistance eligibility before going off-exchange — the state subsidy may make the marketplace cheaper.

Compare HMO vs PPO

For buyers above the subsidy threshold, compare Anthem’s on-exchange HMO sticker price against the off-exchange PPO. The typical difference is $60–$130/month for Bronze tier. Decide whether BlueCard nationwide access, direct specialist visits, and out-of-network protection justify the difference for your situation.

Choose metal tier and HDHP status

If HSA contribution is a priority, confirm the selected plan meets the 2026 HDHP minimum deductible of $1,650. Most Bronze plans qualify. Gold plans with $2,000 deductibles typically also qualify.

Complete the Anthem direct application

Available at anthem.com/ct or through a licensed broker. Requires basic demographic information, Connecticut address, Social Security number, and payment method. No income documentation required. Most applications approve same-day.

Open an HSA account

Available at most banks and financial institutions once HDHP coverage is active. Begin contributing up to $4,300 (individual) or $8,550 (family) for 2026. Contributions are tax-deductible on both federal and Connecticut state returns.

For a full comparison of PPO plan structures, deductible options, and BlueCard network details, the PPO vs HMO guide covers the trade-offs that matter most for Connecticut buyers choosing between plan types.

Frequently Asked Questions About Private Health Insurance in Connecticut

What is private health insurance in Connecticut?

Private health insurance in Connecticut refers to individually purchased ACA-compliant plans bought through Access Health CT or directly from a carrier off the exchange. Both types cover the 10 ACA essential health benefits with no pre-existing condition exclusions. On-marketplace plans access federal tax credits, Covered CT, and state Temporary Premium Assistance. Off-marketplace plans enroll year-round without an open enrollment window and typically offer broader Anthem PPO networks.

Can I buy individual health insurance in Connecticut outside of open enrollment?

Yes. Off-marketplace individual health insurance in Connecticut is available year-round directly from Anthem — no open enrollment window and no qualifying life event required. Access Health CT enrollment is limited to November 1 through January 31 or a Special Enrollment Period. Connecticut residents who miss open enrollment without a qualifying event can purchase ACA-compliant off-exchange Anthem coverage immediately with no waiting period beyond the standard first-of-month effective date.

Who should buy private health insurance off the Connecticut marketplace?

Off-marketplace private health insurance in Connecticut makes the most sense for buyers above 500 percent FPL (~$78,250 single) who receive no subsidy; Fairfield County and Stamford corridor professionals who need Anthem PPO and BlueCard for NYC specialist access; self-employed residents who want an HSA-eligible HDHP with the 100 percent premium deduction; and buyers who need coverage immediately outside the open enrollment window without a qualifying event.

Can self-employed Connecticut residents deduct health insurance premiums?

Yes. Self-employed Connecticut residents can deduct 100 percent of health insurance premiums for themselves, a spouse, and dependents as an above-the-line federal deduction under IRS Publication 535. Connecticut conforms to federal HSA tax treatment, so HSA contributions are also deductible on the Connecticut state return — unlike California and New Jersey, which do not recognize HSA deductions. The combination of the premium deduction and HSA contribution can reduce taxable income by $10,000–$15,000 for a high-earning self-employed Connecticut resident.

Why do Fairfield County residents often choose off-marketplace Anthem PPO?

Fairfield County has a high concentration of self-employed professionals earning above the 500 percent FPL subsidy ceiling. At sticker prices, Anthem’s on-exchange HMO and off-exchange PPO are often within $60–$130/month of each other. The PPO provides BlueCard nationwide network access for NYC specialists, out-of-network coverage during travel, and protection when local network disputes arise — as demonstrated by the March 2026 Stamford Health network exit situation that affected HMO members in Fairfield County.

Related Connecticut Health Insurance Resources

Explore the rest of the Connecticut guide — the statewide overview, small business coverage, affordability, carrier comparisons, and the Access Health CT marketplace.

The complete guide to health insurance options across Connecticut for 2026.

Connecticut Small BusinessGroup plans, the SHOP tax credit, and ICHRA for Connecticut employers.

Affordable Connecticut CoverageHow subsidies and Covered Connecticut lower premiums for those who qualify.

Best Health Insurance in ConnecticutAnthem, ConnectiCare, and Cigna compared on price and provider network.

Connecticut MarketplaceEnrollment windows, deadlines, and subsidies on the Access Health CT marketplace.

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required.

Get Private Health Insurance Quotes for Connecticut

ForHealthInsurance.com compares off-marketplace Anthem PPO, HSA-eligible Bronze plans, and on-exchange alternatives in one session. Licensed Connecticut brokers, year-round enrollment, no extra cost.

Get a Quote Call 888-215-4045Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Connecticut residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.