Individual Health Insurance in DC: A Complete 2026 Guide for Self-Employed Residents

Individual health insurance in DC works differently than in any state because the District operates an all-marketplace structure — every ACA-compliant individual and family plan is sold exclusively through DC Health Link. For DC’s substantial self-employed population, freelancers, independent contractors, and pre-Medicare residents, that means DC Health Link is the single path to coverage. This guide explains how the DC individual market works for 2026, who buys this kind of coverage, how to compare CareFirst and Kaiser individual plans, tax considerations for self-employed enrollees, and how to enroll.

What brings you to DC individual coverage today?

What “Individual Health Insurance” Means in DC’s All-Marketplace Structure

Individual health insurance DC residents buy is coverage purchased directly by a single person or family — not through an employer, Medicaid, or Medicare. In DC, every ACA-compliant individual and family plan is sold exclusively through DC Health Link, the District’s state-based marketplace. This all-marketplace structure is unique among U.S. jurisdictions — most states have both on-exchange and off-exchange individual markets, but DC closed its off-exchange channel.

The all-marketplace structure shapes every individual coverage decision in the District. A DC resident cannot purchase ACA-compliant coverage directly from CareFirst BlueCross BlueShield or Kaiser Permanente outside DC Health Link. Carriers are not legally permitted to sell individual or small group plans to DC residents through any channel other than the exchange operated by the DC Health Benefit Exchange Authority. The framework was set by the Health Benefit Exchange Authority Establishment Act of 2011 and consolidated under DC Code §31-3171.04, which made DC the only jurisdiction in the country to operate as a pure single-channel ACA marketplace.

For 2026, the DC individual market holds 27 plans from two carriers — CareFirst BlueCross BlueShield offers both HMO and PPO products under the BlueChoice brand, and Kaiser Permanente offers HMO plans only. UnitedHealthcare participates in DC Health Link but only in the Small Business Marketplace (SHOP), serving employer groups with 1 to 50 employees. Individual shoppers will not see UHC plans on DC Health Link. Non-ACA products like short-term limited duration insurance or fixed indemnity coverage may be available outside DC Health Link, but these carry significant coverage gaps and do not satisfy the individual mandate where it still applies.

What this means in practice: if you’re a DC resident shopping for your own coverage, your decision tree is simple — DC Health Link is the destination, and CareFirst and Kaiser are your two carrier choices. Off-exchange shopping is not an option for comprehensive individual coverage in the District.

Who Buys Individual Health Insurance in DC

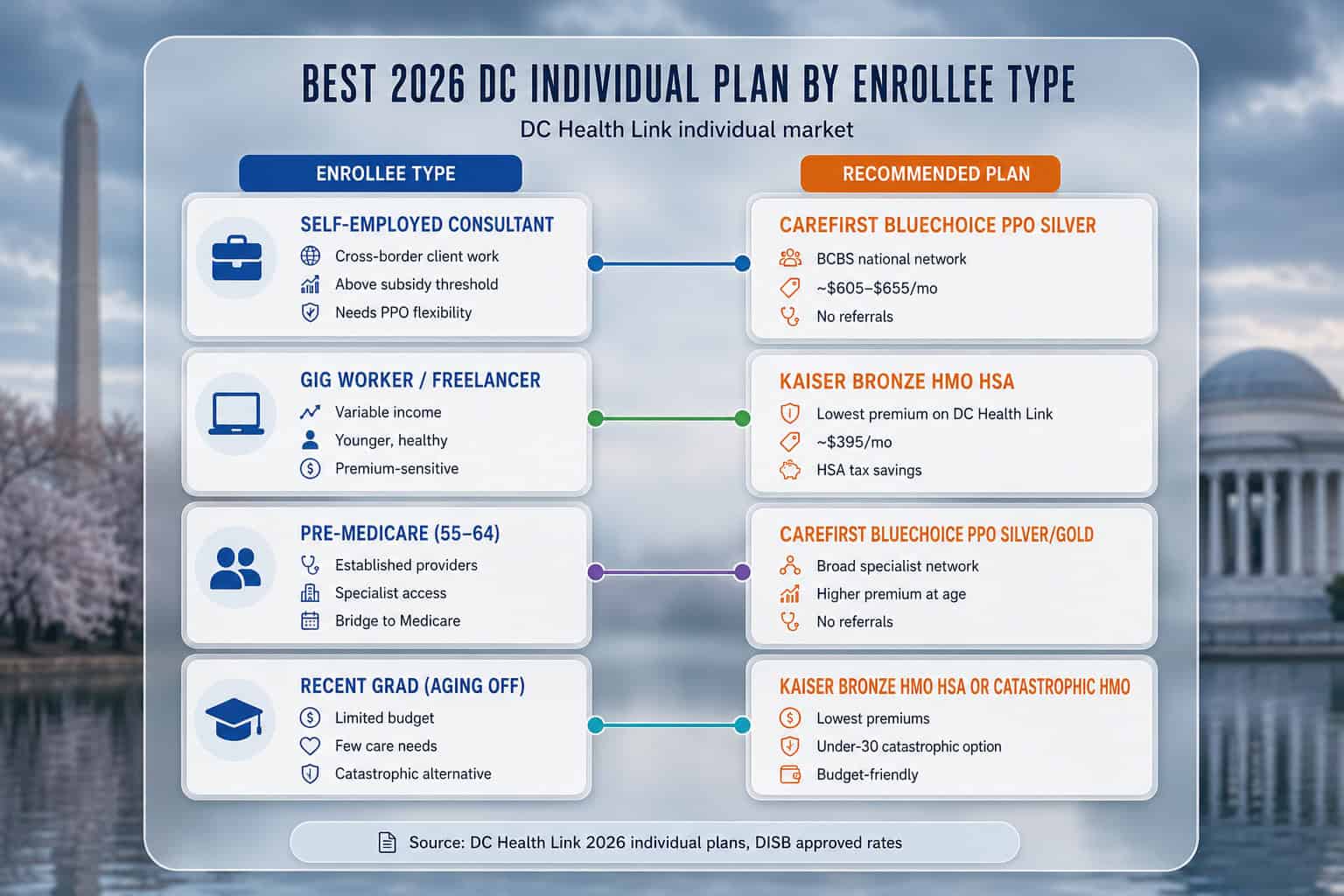

DC has one of the highest concentrations of self-employed workers in the country thanks to the District’s consulting, lobbying, advocacy, journalism, and creative economies. Individual health insurance DC enrollees on DC Health Link skew heavily toward these self-employed professionals, plus independent contractors, gig workers, freelancers, pre-Medicare retirees, and recent graduates aging off parents’ plans. Each group has different cost sensitivities and provider needs that shape the right plan choice for individual health insurance DC residents will use throughout the year.

The self-employed share of DC Health Link individual enrollment is structurally elevated compared to other markets. Federal contractors who work as 1099 consultants, policy researchers at small think tanks, freelance journalists covering the federal government, communications consultants serving advocacy organizations, attorneys in solo practice, and creative professionals — designers, photographers, videographers serving DC’s nonprofit and advocacy sector — all rely on DC Health Link for coverage. Many of these professionals have substantial incomes that place them above the federal subsidy thresholds, which is part of why only about 28% of DC Health Link enrollees receive premium tax credits versus 93% nationally.

Self-employed consultants

Often above subsidyFederal contractors working as 1099s, policy consultants, freelance journalists. Often above subsidy thresholds. Typically choose CareFirst PPO for cross-border MD/VA client meetings, or Kaiser Bronze HSA for tax-advantaged cost minimization.

Independent contractors and gig workers

Premium-sensitiveDesigners, photographers, ride-share drivers, delivery workers, food service contractors. Income variability makes premium predictability important. Bronze plans paired with HSAs work well for younger gig workers without dependents.

Recent graduates aging off parents’ plans

Under-26DC’s young professional population turning 26 and losing dependent coverage. Catastrophic plans available for those under 30 if Bronze premium is still too high. Kaiser Bronze HMO HSA often the lowest-cost path.

Pre-Medicare bridge coverage

Ages 55–64DC residents ages 55–64 who left a job before Medicare eligibility at 65. COBRA is one path, but individual DC Health Link coverage is often cheaper. CareFirst PPO Silver popular for broader specialist access at older ages.

Recent moves to DC

60-day SEPNew DC residents who moved from another state for work. Moving triggers a 60-day Special Enrollment Period on DC Health Link. CareFirst and Kaiser plans require re-enrollment — coverage from other states does not transfer.

Spouses without employer coverage

Single-person planOne partner has employer health insurance; the other works independently or for an employer that doesn’t offer coverage. DC Health Link individual plan covers just the uninsured spouse — often more affordable than adding the spouse to the employer family plan.

Comparing CareFirst and Kaiser Individual Plans for 2026

The DC individual market for 2026 offers 27 plans across two carriers. CareFirst BlueCross BlueShield provides HMO, PPO, and HSA-Bronze options through DC Health Link, with the PPO accessing the BCBS national network. Kaiser Permanente offers HMO plans only across all four metal tiers, with the lowest individual health insurance DC premiums in the market starting around $395 per month for a 40-year-old. The choice often comes down to whether you need cross-state network access in Maryland or Virginia.

Individual health insurance DC shoppers approach the comparison differently than employer-group members. Without an HR department vetting carriers in advance, individual enrollees must check their own doctors against each network, verify their prescriptions are on the formulary, confirm specialists are accessible, and compare premium against the deductible and out-of-pocket maximum they’re realistically likely to hit. According to CMS Marketplace Open Enrollment data, DC’s two-carrier individual market is among the most concentrated in the country, which actually simplifies the decision — there are fewer combinations to evaluate.

| Plan | Carrier | Type | Est. Premium (Age 40) | Deductible | Best For |

|---|---|---|---|---|---|

| BlueChoice HSA Bronze | CareFirst BCBS | HMO | ~$410–$440/mo | ~$7,000 | HSA savings, regional DC-area network |

| BlueChoice PPO Silver | CareFirst BCBS | PPO | ~$605–$655/mo | ~$4,500 | MD/VA cross-border care, no referrals |

| BlueChoice PPO Gold | CareFirst BCBS | PPO | ~$720–$785/mo | ~$2,000 | Frequent care, low deductible, national network |

| Kaiser Bronze HMO HSA | Kaiser Permanente | HMO | ~$395/mo | ~$7,500 | Lowest premium, HSA-eligible, integrated care |

| Kaiser Silver HMO | Kaiser Permanente | HMO | ~$495/mo | ~$5,500 | Subsidy benchmark, balanced cost-sharing |

| Kaiser Gold HMO | Kaiser Permanente | HMO | ~$605/mo | ~$2,500 | Chronic condition management, lower deductible |

Compare DC Individual Plans for 2026

A licensed agent matches your situation to the right CareFirst or Kaiser plan, checks subsidy eligibility, and completes DC Health Link enrollment. No cost to you.

Tax Considerations for Self-Employed DC Individual Enrollees

Self-employed DC residents enrolled in individual health insurance DC Health Link plans qualify for two tax mechanisms: the self-employed health insurance deduction (100% of premiums deducted above-the-line on federal returns) and federal premium tax credits if income qualifies. The two mechanisms interact and must be calculated together. DC also requires income tax filing on top of federal returns, with the District generally following federal treatment of health insurance.

The self-employed health insurance deduction is an above-the-line deduction on Schedule 1 of Form 1040, available to anyone who is self-employed, a partner in a partnership, or a more-than-2% S-corporation shareholder, and who is not eligible for employer-subsidized coverage through their own or a spouse’s employer. The deduction covers 100% of premiums paid for individual or family coverage, with no AGI threshold or itemization requirement. For a DC freelancer paying $7,200 annually for a CareFirst Silver PPO ($600/month), the full $7,200 reduces federal taxable income — saving roughly $1,600 to $2,400 in federal income tax depending on bracket, plus self-employment tax savings.

Federal premium tax credit (APTC) interacts with the self-employed deduction in a specific way. If you receive an advance premium tax credit through DC Health Link, you can only deduct premiums net of the credit — not the gross premium. The reconciliation happens at tax time on IRS Form 8962, where actual annual income is reconciled against the income reported when you enrolled. Most self-employed DC enrollees with subsidy eligibility benefit from running through both calculations carefully — a tax professional or accountant familiar with self-employed health insurance is worth the cost.

For DC tax filers specifically: the District generally conforms to federal treatment of the self-employed health insurance deduction. DC residents file the DC D-40 tax return alongside federal Form 1040, and the federal AGI reduction flows through to DC taxable income. DC’s marginal tax rates run from 4% to 10.75%, so reducing federal AGI by $7,200 in deductible premiums typically saves an additional $400 to $775 in DC income tax.

Common Individual Coverage Scenarios for DC Residents

Real-world DC individual coverage decisions vary by income, household composition, and what coverage you need. A 28-year-old freelance designer in H Street faces different tradeoffs than a 55-year-old consultant bridging to Medicare in Chevy Chase. The four scenarios below walk through how individual health insurance DC enrollees in different situations actually navigate the 27-plan DC Health Link individual market.

Priya, 29, freelance UX designer in NoMa, earning $62,000 (about 420% FPL):

Above the standard subsidy cliff. Without ARPA subsidy extension, Priya pays full unsubsidized premium. Kaiser Bronze HMO HSA at ~$395/month is her cheapest option — $4,740/year before tax effects. The self-employed deduction reduces federal AGI by the full $4,740, saving roughly $1,000–$1,400 in combined federal and DC income tax. After tax effects, real net cost is closer to $3,400/year. CareFirst BlueChoice HSA Bronze at ~$425/month would cost slightly more but adds PPO-style network flexibility if she takes contract work in MD or VA. Premium-sensitive freelancers like Priya can also review the lowest-cost paths laid out in our guide to affordable health insurance in DC, which breaks down the cheapest Kaiser and CareFirst Bronze options on DC Health Link.

Marcus, 38, independent policy consultant in Mount Pleasant, earning $95,000 (about 645% FPL):

Well above subsidy thresholds — full unsubsidized premium. Marcus chooses CareFirst BlueChoice PPO Silver at ~$625/month ($7,500/year) for cross-border client meetings in Bethesda and Arlington and access to specialists at MedStar Washington Hospital Center and GW Hospital. Self-employed deduction reduces federal AGI by full $7,500, saving approximately $2,250 in federal income tax (22% bracket) plus $500–$600 in DC income tax. Real net cost after taxes: roughly $4,650/year. The PPO premium difference over Kaiser Bronze pays for itself the first time he sees an out-of-network specialist in network instead.

Linda, 58, semi-retired attorney bridging to Medicare in Chevy Chase DC, household income $72,000 (about 360% FPL for a single):

In the subsidy range for 2026. The benchmark Silver plan costs roughly $830/month at her age (Linda is 58, so age factor pushes premiums about 1.6x the age-40 rates). After APTC at 360% FPL, her expected contribution drops to approximately $510/month. She chooses CareFirst BlueChoice PPO Gold at ~$890/month sticker, ~$570/month after subsidy — paying about $60 more per month than benchmark to lock in lower deductible exposure on her existing cardiology and orthopedic care providers at Sibley Memorial and Suburban Hospital in Bethesda.

Devon and Jay, married couple both 33, both freelance creatives in Bloomingdale, household $108,000 (about 540% FPL for two):

Just above the standard subsidy cliff. Without ARPA extension, both pay full unsubsidized premium. As a married couple filing jointly, they save by jointly enrolling in one family plan. CareFirst BlueChoice Silver HMO family plan at roughly $1,100/month covers both — $13,200/year. Combined self-employed deductions for both partners reduce federal AGI by the full $13,200, saving roughly $2,900 in federal income tax (24% bracket) plus $1,000+ in DC income tax. Kaiser Silver HMO family at roughly $980/month would save about $120/month if both are comfortable with the Kaiser closed network.

How to Enroll in Individual DC Health Link Coverage

Individual health insurance DC enrollment follows a five-step DC Health Link path: create an account, complete the eligibility application, review subsidy and program eligibility, compare 2026 CareFirst and Kaiser plans, and enroll by the deadline. Open enrollment for 2026 runs November 1, 2025 through January 31, 2026 — longer than the federal HealthCare.gov window. Special Enrollment Periods open year-round for qualifying life events, including DC’s pregnancy SEP that most states don’t recognize.

Create or sign into your DC Health Link account

Visit dchealthlink.com and create an individual account. Self-employed and freelance enrollees use the individual portal — not the SHOP portal, which is for employers. Returning users sign in with existing credentials.

Complete the eligibility application

Self-employed applicants report their projected annual income from Schedule C or 1099 work. Be conservative with income projection — reporting too low and earning more triggers subsidy clawback at tax time. Report household size, citizenship status, and any current coverage.

Review eligibility results

DC Health Link routes you to the right program: federal premium tax credit if income qualifies, DC Medicaid if under 215% FPL, the new Healthy DC Plan if you fall in the qualifying band, or full-price individual marketplace if above all thresholds.

Compare CareFirst and Kaiser plans

Filter the 27 individual plans by premium, deductible, doctor network, and prescription coverage. Self-employed enrollees should check whether existing providers are in-network on each plan — Kaiser HMO restricts to Kaiser facilities; CareFirst PPO offers BCBS national network reach.

Enroll and confirm coverage start

Select a plan and submit enrollment. Plans selected by December 15 take effect January 1, 2026. Plans selected between December 16 and January 31 take effect February 1 or March 1. DC Health Link sends confirmation; the carrier mails member ID cards within 7–10 business days.

FAQ About Individual Health Insurance in DC

DC residents shopping for individual health insurance DC coverage ask the same six questions: what individual coverage means in DC, how self-employed residents enroll, whether private coverage exists outside DC Health Link, what 2026 costs look like, whether premiums are tax-deductible, and what happens when moving out of DC. The answers below cover the practical decision points for any DC household considering individual coverage on DC Health Link.

What is individual health insurance in DC?

Individual health insurance in DC is coverage purchased by a single person or family directly — not through an employer, Medicaid, or Medicare. In DC, all individual ACA-compliant plans are sold exclusively through DC Health Link. The District operates an all-marketplace structure, meaning there is no off-exchange individual market the way most states have.

How do self-employed DC residents get health insurance?

Self-employed DC residents enroll in individual health insurance through DC Health Link at dchealthlink.com. They choose from 27 individual plans for 2026 across CareFirst BlueCross BlueShield and Kaiser Permanente. Self-employed enrollees may deduct premiums as a business expense on Schedule SE, and federal premium tax credits are available for those who qualify based on income.

Can I buy private health insurance in DC outside of DC Health Link?

No, not for ACA-compliant comprehensive coverage. DC operates an all-marketplace individual market — all ACA-qualifying individual and family plans are sold exclusively through DC Health Link. Non-ACA products like short-term limited duration insurance or fixed indemnity plans may be available outside DC Health Link but carry significant coverage gaps.

How much does individual health insurance cost in DC for 2026?

Individual health insurance premiums in DC for 2026 range from approximately $395 per month for Kaiser Bronze HMO to $925 per month for CareFirst PPO Platinum, for a 40-year-old before subsidies. The average individual premium runs roughly $582 per month following DISB’s approved average 8.7% rate increase for 2026.

Are individual health insurance premiums tax deductible for self-employed DC residents?

Yes. Self-employed individuals in DC who are not eligible for an employer-subsidized plan can deduct 100% of their health insurance premiums on federal tax returns through the self-employed health insurance deduction. This is an above-the-line deduction available regardless of whether you itemize. Premium tax credits received through DC Health Link must be reconciled separately on IRS Form 8962.

What happens to my individual DC coverage if I move out of DC?

Moving out of DC triggers a Special Enrollment Period in your new state. CareFirst and Kaiser DC Health Link plans don’t transfer — you must enroll in a new marketplace plan through your new state’s exchange or HealthCare.gov. Moving into DC from another state similarly opens a 60-day SEP to enroll on DC Health Link.

DC Health Insurance Resources

Explore the rest of the DC guide — the statewide overview, the DC Health Link marketplace, carrier comparisons, and nationwide PPO coverage.

The complete guide to health insurance options across the District for 2026.

DC Health Insurance MarketplaceEnrollment windows, deadlines, and subsidies on DC Health Link.

Best Health Insurance in DCCareFirst and Kaiser compared on price and provider network.

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required.

Get Individual DC Coverage Help for 2026

A licensed agent compares CareFirst and Kaiser individual plans, confirms subsidy eligibility, and completes DC Health Link enrollment. Free service for DC self-employed and individual shoppers.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving District of Columbia residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.