DC Health Insurance Marketplace: A Complete 2026 Guide to DC Health Link

The District of Columbia runs its own health insurance marketplace called DC Health Link — not HealthCare.gov. This guide to the DC health insurance marketplace explains how DC Health Link works, what plans are available for 2026, how subsidies and cost-sharing reductions work in the District, the small business marketplace for employer groups, and when DC residents can enroll throughout the year.

What brings you to the DC marketplace today?

I want to understand DC Health Link

What it is and how it differs from HealthCare.gov

Read the basics ↓What DC Health Link Is (And Why It’s Not HealthCare.gov)

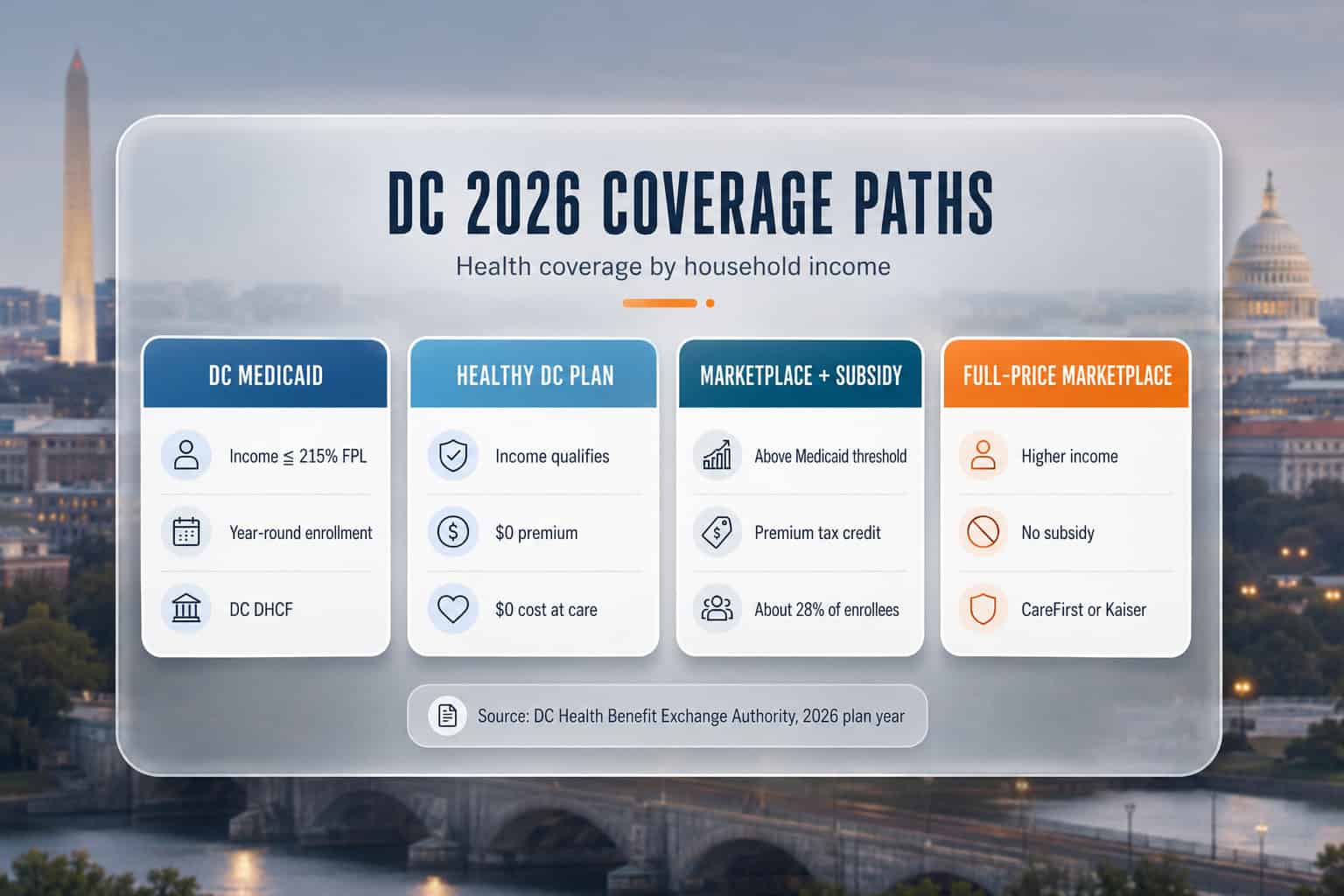

DC Health Link is the DC health insurance marketplace — a state-based exchange operated by the DC Health Benefit Exchange Authority (HBX). DC residents enroll in individual and family ACA plans exclusively through DC Health Link — not HealthCare.gov. For 2026, DC Health Link offers 27 individual plans from CareFirst BlueCross BlueShield and Kaiser Permanente, plus 161 small group plans across three carriers.

DC built its own marketplace because the Affordable Care Act gave states the option to run state-based exchanges instead of using the federal HealthCare.gov platform. The Health Benefit Exchange Authority Establishment Act of 2011 created HBX, and DC Health Link launched for the 2014 plan year. Today DC is one of 21 jurisdictions running fully state-based marketplaces — alongside California’s Covered California, New York State of Health, and Pennie in Pennsylvania.

What makes DC distinct from those other state-based marketplaces is that DC also closed its off-exchange individual market. In most states, residents can buy ACA-compliant individual coverage either through the state marketplace or directly from a carrier off-exchange. DC chose a different structure: all individual and small group ACA plans must be sold through DC Health Link. CareFirst, Kaiser, and UnitedHealthcare cannot sell individual or SHOP coverage to DC residents through any other channel.

DC residents shopping for individual coverage: there is no separate “off-exchange” option to compare against DC Health Link. Every ACA-compliant individual plan a DC resident can buy is on the marketplace.

How to Use DC Health Link to Shop and Enroll

Shopping on DC Health Link follows a five-step path: create an account at dchealthlink.com, complete an eligibility application, see which programs you qualify for (marketplace with subsidy, DC Medicaid, or the new Healthy DC Plan), compare 2026 plans from CareFirst and Kaiser, and enroll by the deadline. The DC Health Link Customer Service line at (855) 532-5465 helps with any step, and licensed agents can complete the entire process at no cost to the consumer.

Create your DC Health Link account

Visit dchealthlink.com and create an individual account. You’ll provide your name, address, contact information, and create login credentials. Returning users sign in with their existing account.

Complete the eligibility application

Provide household size, income, citizenship or immigration status, and current coverage status. The application determines whether you qualify for premium tax credits, cost-sharing reductions, DC Medicaid, or the Healthy DC Plan.

Review your eligibility results

DC Health Link routes you to the correct program. Marketplace shoppers see plans with subsidies applied. Medicaid-eligible applicants are routed to District Direct (the DC Department of Health Care Finance portal). Healthy DC applicants confirm income eligibility. If cost is your main concern, our guide to affordable health insurance in DC breaks down every low-cost path — Medicaid, Healthy DC, and subsidized plans — by income band.

Compare 2026 plans

For individual marketplace, compare CareFirst HMO, CareFirst PPO, and Kaiser HMO plans across Bronze, Silver, Gold, and Platinum tiers. Filter by monthly premium, deductible, doctor network, and prescription coverage. DC Health Link shows your subsidy-adjusted prices, not sticker prices.

Enroll by the deadline

Select a plan, confirm your premium, and submit enrollment. December 15 deadlines mean January 1 coverage starts. January 31 deadlines mean February 1 or March 1 coverage. DC Health Link sends confirmation, and your carrier mails your member ID card within 7–10 business days.

Plans Available on DC Health Link for 2026

The DC Health Link individual marketplace offers 27 plans for 2026 across two carriers and three product types: CareFirst BlueChoice HMO, CareFirst BlueChoice PPO, and Kaiser Permanente HMO. Plans are available at all four metal tiers — Bronze, Silver, Gold, and Platinum — plus Catastrophic for eligible enrollees under 30 and HSA-qualified Bronze options. New for 2026, all Bronze plans on DC Health Link are HSA-eligible.

The 27 individual plan count held steady from 2025, while small group plans dropped by 10, from 171 to 161 across the three SHOP carriers. The number of carriers in the individual market also held at two — CareFirst and Kaiser have anchored the DC health insurance marketplace since launch, and the District has not seen new carriers enter the individual market in recent plan years. According to CMS Marketplace Open Enrollment data, this two-carrier individual market is one of the most concentrated in the country among state-based exchanges.

For 2026, DC Health Link added the Healthy DC Plan as a coverage option for qualified DC residents, alongside the standard marketplace plans. Per the DC Health Link homepage, the Healthy DC Plan provides quality health coverage with no monthly premium and no cost at the point of care. Eligibility is income-based and limited to DC residents who meet specific criteria. The plan sits between DC Medicaid (covering adults up to 215% FPL) and the subsidized marketplace, filling a gap for residents whose income exceeds Medicaid limits but who still need no-cost coverage.

| Plan Type | Carriers | Network Style | Best For |

|---|---|---|---|

| CareFirst BlueChoice HMO | CareFirst BCBS | Local HMO with PCP and referrals | Lower premiums, DC-area providers |

| CareFirst BlueChoice PPO | CareFirst BCBS | BCBS national network, no referrals | MD/VA cross-border care, travel |

| CareFirst BlueChoice HSA Bronze | CareFirst BCBS | HMO or PPO with HSA-qualified deductible | Tax-advantaged savings, low premium |

| Kaiser Permanente HMO | Kaiser | Closed Kaiser network — integrated care | Lowest premiums, single medical home |

| Kaiser HSA-Qualified Bronze | Kaiser | Kaiser HMO with HSA deductible | Lowest-premium HSA option |

| Catastrophic | CareFirst BCBS | HMO with essential health benefits | Under-30 enrollees, hardship exemptions |

Compare 2026 DC Health Link Plans

See CareFirst and Kaiser plans side by side with a licensed agent. No cost to you.

Subsidies and Cost Help Through DC Health Link

DC Health Link applies the same federal premium tax credit and cost-sharing reduction rules as HealthCare.gov, but uptake is lower in DC because the District’s median income is higher. About 28% of DC Health Link individual enrollees received premium tax credits in the most recent enrollment cycle, compared to roughly 93% nationally. DC Medicaid covers adults up to 215% of FPL — one of the most generous expansion thresholds in the country.

The federal premium tax credit (APTC) is calculated against the second-lowest-cost Silver plan on DC Health Link, scaled so that the benchmark Silver costs a defined percentage of household income. Tax credit reconciliation happens at tax time on IRS Form 8962, where actual annual income is compared to the income reported at enrollment and any difference is settled. Cost-sharing reductions further reduce out-of-pocket exposure for Silver plan enrollees between 100% and 250% of FPL.

DC’s lower subsidy uptake reflects the District’s demographic reality. The DC metropolitan area has the highest median household income of any U.S. region, and a significant share of DC Health Link enrollees — federal workers, lobbyists, consultants, nonprofit professionals — fall above the standard subsidy ranges. Subsidy uptake on DC Health Link is documented in the KFF State Exchange Profile for DC and updated annually based on DC Health Benefit Exchange Authority enrollment reports.

Scenario — Single adult in Petworth earning $48,000 (about 330% FPL):

At 330% of FPL, this resident qualifies for a federal premium tax credit. The benchmark Silver plan on DC Health Link costs approximately $550/month before subsidy. After APTC calculation, the resident’s expected contribution is roughly $370/month — a saving of about $180/month, or $2,160 per year. The resident can apply the credit to any DC Health Link plan, including lower-premium Bronze options or higher-coverage Gold plans.

DC Health Link Small Business Marketplace (SHOP)

The DC Health Link Small Business Marketplace is the small-employer side of the DC health insurance marketplace, serving employer groups with 1 to 50 employees in the District. For 2026, three carriers participate in SHOP — CareFirst BlueCross BlueShield, Kaiser Permanente, and UnitedHealthcare — across 161 small group plans. SHOP operates separately from individual coverage but uses the same DC Health Link platform. Employers enroll the group; individual employees cannot buy SHOP plans directly.

DC Health Link’s SHOP is structurally different from individual coverage in two ways. First, it adds UnitedHealthcare as a third carrier — UHC participates only in SHOP for 2026, not the individual market. UHC’s SHOP offerings include Choice Plus (a PPO with broad national access and no referrals), Core Essential (network-only HMO-style coverage without referrals), and OCI HMO (regional coordinated care with a primary doctor). Second, SHOP gives employers control over plan selection, employee contribution levels, and benefit design — choices that don’t exist in the individual market.

Small group rates for 2026 were approved by the DC Department of Insurance, Securities and Banking (DISB) at an average 9.5% increase, slightly higher than the 8.7% individual market increase. CareFirst filed average increases of 10.1% for HMO plans and 8.4% for PPO plans on the small group side. The full filings are available through DISB’s rate filings portal. Small group plan count dropped from 171 in 2025 to 161 for 2026, with all three carriers trimming their plan portfolios slightly.

Special Enrollment Periods on DC Health Link

DC Health Link recognizes the standard federal qualifying life events that open a Special Enrollment Period (SEP) — loss of other coverage, marriage, birth or adoption, moving to DC, and income changes affecting subsidy eligibility — plus a DC-specific trigger: pregnancy. DC is one of a small group of U.S. jurisdictions that treats becoming pregnant (not just giving birth) as a qualifying event. Most SEPs allow 60 days from the event to enroll.

The pregnancy SEP is one of the most distinctive features of the DC health insurance marketplace. Most states only count birth, adoption, or foster placement — meaning a pregnant person without coverage must wait through the entire pregnancy until the baby is born to enroll, leaving the pregnancy uncovered. DC Health Link allows a pregnant DC resident to enroll at any point during pregnancy, with coverage starting the first of the following month. The DC Health Benefit Exchange Authority adopted this expansion to reduce uninsured pregnancies, and a small group of state-based marketplaces have since followed — including New York, New Jersey, and Maryland under a 2023 expansion.

Loss of Other Coverage

Losing job-based coverage, COBRA expiring, aging off a parent’s plan at 26, losing DC Medicaid eligibility. 60-day SEP window from loss date.

Household Changes

Marriage, divorce, birth, adoption, or foster placement. 60-day window. Coverage typically starts the first of the following month.

Moving to DC

Permanent move to the District from another state or country. 60-day window. Must establish DC residency to enroll on DC Health Link.

Pregnancy

DC-specificBecoming pregnant qualifies as a life event in DC, even before giving birth. Enrollment available throughout pregnancy with coverage starting the first of the following month.

Income Changes

Significant income changes that affect subsidy eligibility — gaining or losing access to APTC or DC Medicaid. Documentation required.

Other Qualifying Events

Release from incarceration, becoming a U.S. citizen, gaining membership in a federally recognized tribe, exceptional circumstances determined by HBX.

Frequently Asked Questions About the DC Marketplace

Shoppers on the DC health insurance marketplace ask the same questions repeatedly: is DC Health Link the same as HealthCare.gov, how many plans are available, when can I enroll, do subsidies work, is there a small business marketplace, and what qualifies for Special Enrollment. The answers below cover what every DC resident or small employer should know before using DC Health Link for 2026 coverage.

Is the DC health insurance marketplace the same as HealthCare.gov?

No. The District of Columbia operates its own state-based marketplace called DC Health Link, run by the DC Health Benefit Exchange Authority. DC residents do not use HealthCare.gov. All individual and small business ACA-compliant plans in the District are sold through DC Health Link at dchealthlink.com.

How many plans are available on the DC marketplace for 2026?

DC Health Link offers 27 individual plans and 161 small group plans for the 2026 plan year. Individual plans come from CareFirst BlueCross BlueShield and Kaiser Permanente. Small group plans add UnitedHealthcare as a third carrier for employer groups with 1 to 50 employees.

When can I enroll on DC Health Link for 2026?

Open enrollment for 2026 coverage runs November 1, 2025 through January 31, 2026 — two weeks longer than the federal HealthCare.gov window. Enrollments completed by December 15 take effect January 1. Enrollments between December 16 and January 31 take effect February 1 or March 1.

Can I get subsidies on DC Health Link?

Yes. Federal premium tax credits and cost-sharing reductions are available through DC Health Link using the same eligibility rules as HealthCare.gov. About 28% of DC Health Link individual enrollees receive premium tax credits, compared to 93% nationally — reflecting the District’s higher median income.

Does DC have a small business marketplace?

Yes. The DC Health Link Small Business Marketplace (often called SHOP) serves employer groups with 1 to 50 employees. CareFirst BlueCross BlueShield, Kaiser Permanente, and UnitedHealthcare all participate in SHOP for 2026, with 161 small group plans total.

What qualifies for a Special Enrollment Period on DC Health Link?

Standard qualifying life events include losing other coverage, marriage, birth or adoption, moving to DC, and certain income changes affecting subsidy eligibility. DC also recognizes pregnancy as a qualifying event — a distinction shared by only a small group of state-based marketplaces.

DC Health Insurance Resources

Explore the rest of the DC guide — the statewide overview, carrier comparisons, individual plans for the self-employed, and nationwide PPO coverage.

The complete guide to health insurance options across the District for 2026.

Best Health Insurance in DCCareFirst and Kaiser compared on price and provider network.

Individual Health Insurance in DCDC Health Link coverage for the self-employed, freelancers, and contractors.

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required.

Enroll Through DC Health Link With Licensed Help

A licensed DC agent compares CareFirst and Kaiser plans, confirms your subsidy eligibility, and completes DC Health Link enrollment at no cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving District of Columbia residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.