Small Business Health Insurance in Maine: 2026 Group Plans & Options

Maine small businesses have a unique advantage when shopping for group health insurance — the state’s merged individual and small group market means employers share a risk pool with individual buyers, stabilized by the MGARA reinsurance program. This guide covers group plan carriers, the SHOP tax credit, ICHRA alternatives, and how the merged market affects what small employers pay in 2026.

What does your business need?

Small Business Health Insurance Options in Maine

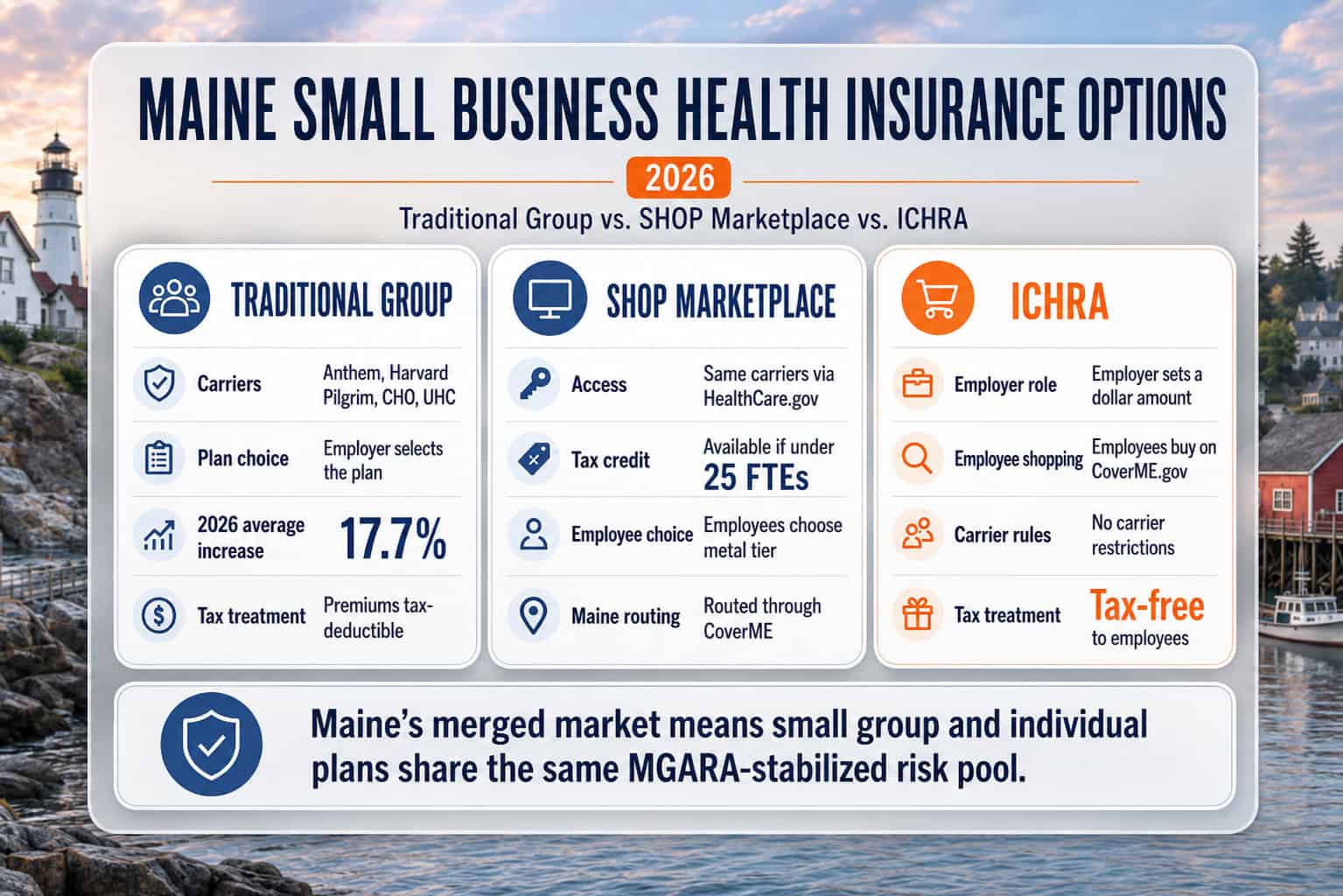

Maine small businesses with 1–50 employees can offer coverage through three primary channels: traditional small group plans from carriers including Anthem, Harvard Pilgrim, Community Health Options, and UnitedHealthcare; the SHOP marketplace through HealthCare.gov for tax credit eligibility; or an Individual Coverage Health Reimbursement Arrangement (ICHRA) that reimburses employees for individual plan premiums on CoverME.gov. The small group market saw a weighted average rate increase of 17.7% for 2026 — lower than the individual market’s 23.9% increase.

| Option | Eligible Businesses | Carriers in Maine | Tax Credit Eligible | Employee Choice |

|---|---|---|---|---|

| Traditional small group | 1–50 FTE | Anthem, Harvard Pilgrim, CHO, UHC, Mending | No (unless through SHOP) | Employer selects plan; employees enroll |

| SHOP marketplace | 1–50 FTE | Same carriers, via HealthCare.gov | Yes — under 25 FTE + avg wages under $58,000 | Employees may choose from available metal tiers |

| ICHRA | Any size | Any — employees choose their own on CoverME | No (but contributions are tax-free) | Full employee choice — CoverME.gov or off-exchange |

| QSEHRA | Under 50 FTE, no group plan | Any — employees choose their own | No (but contributions are tax-free) | Full employee choice; max $6,350/individual in 2026 |

For many Maine small businesses, the ICHRA model is gaining traction — particularly among employers with employees spread across multiple counties where carrier availability and pricing differ. A traditional group plan locks all employees into one carrier, but a Saco restaurant with staff living in Cumberland, York, and Oxford counties could set a $400/month ICHRA allowance and let each employee choose the best plan for their location on CoverME.gov. The employer’s cost is fixed at $400/employee regardless of which carrier or tier each employee selects.

Maine’s Merged Market: How It Benefits Small Businesses

Since 2023, Maine has merged its individual and small group health insurance markets into a single risk pool — one of only a handful of states to do so. Small group premiums are now set using the combined claims experience of both pools, stabilized by the MGARA reinsurance program that covers 60% of eligible high-cost claims for 2026. The merged market was designed to help small businesses, which previously faced higher rate volatility in a smaller standalone pool.

Before the merger, Maine’s small group market was shrinking — enrollment was declining and premiums were rising faster than the individual market. The MGARA reinsurance program, which had only covered the individual market since 2019, was extended to the merged pool when the markets combined. This gave small business health insurance in Maine access to the same reinsurance protections that had already stabilized individual market rates. The Maine Bureau of Insurance estimated that extending reinsurance to the small group market would reduce premiums compared to what they would have been in a standalone pool.

For 2026, the small group market saw a weighted average rate increase of 17.7% — significantly lower than the individual market’s 23.9%. Carrier-specific small group increases ranged from UnitedHealthcare’s 8.1%–8.4% (the lowest) to Mending’s 32.2% (the highest, from a small base). Anthem, the largest small group carrier with approximately 25,784 covered lives, approved a 16.0% increase. Harvard Pilgrim’s small group rates increased 19.2%–20.4% depending on plan type.

MGARA and small group rates

The MGARA reinsurance program covers 60% of eligible high-cost claims in 2026 (down from 75% in 2024–2025). Without MGARA, small group premiums would be approximately 10–15% higher. The program is funded through federal pass-through savings and a per-member-per-month assessment on carriers — not through employer contributions. Small business owners benefit from MGARA without needing to do anything beyond purchasing a qualified small group plan.

Small Group Carriers in Maine for 2026

Six carriers offer small business health insurance in Maine for the small group market in 2026: Anthem Health Plans of Maine (HMO/PPO, 25,784 lives, 16.0% increase), Harvard Pilgrim Health Care (HMO, 9,346 lives, 20.4% increase), HPHC Insurance Company (PPO, 2,163 lives, 19.2% increase), Community Health Options (HMO/PPO, 6,341 lives, 21.5% increase), UnitedHealthcare (HMO/PPO, 1,354 combined lives, 8.1%–8.4% increase), and Mending (HMO, 141 lives, 32.2% increase). Aetna exited the Maine small group market in 2025.

Anthem Health Plans of Maine

16.0%HMO & PPO · 25,784 covered lives

The largest small group carrier in Maine with roughly 57% of covered lives — more than the next three carriers combined. Offers the broadest provider network statewide and both HMO and PPO group options, making it the default choice for most southern and central Maine employers.

Harvard Pilgrim Health Care

20.4%HMO · 9,346 covered lives

The second-largest small group carrier in Maine, strongest in the southern counties. Its HMO group plans pair with the HPHC Insurance Company PPO arm for employers wanting out-of-network flexibility for their teams.

Community Health Options

21.5%HMO & PPO · 6,341 covered lives

Maine’s only member-led nonprofit carrier, based in Lewiston. Offers both HMO and PPO small group plans and competes statewide, with particular strength among Maine-headquartered small employers who prefer a local carrier.

UnitedHealthcare

8.1%–8.4%HMO & PPO · 1,354 covered lives

Posted the lowest 2026 small group rate increases in Maine by a wide margin. Smaller local footprint than Anthem or Harvard Pilgrim, but worth a quote for cost-sensitive employers willing to evaluate a less established in-state network.

| Carrier | Plan Types | 2025 Covered Lives | 2026 Rate Increase |

|---|---|---|---|

| Anthem Health Plans of Maine | HMO, PPO | 25,784 | 16.0% |

| Harvard Pilgrim Health Care | HMO | 9,346 | 20.4% |

| HPHC Insurance Company | PPO | 2,163 | 19.2% |

| Community Health Options | HMO, PPO | 6,341 | 21.5% |

| UnitedHealthcare | HMO, PPO | 1,354 | 8.1%–8.4% |

| Mending (formerly Taro Health) | HMO | 141 | 32.2% |

Anthem dominates the Maine small group market with approximately 57% of covered lives — more than the next three carriers combined. For small businesses in southern and central Maine, this usually means Anthem offers the broadest provider network and the most competitive group rates. UnitedHealthcare, while smaller in Maine, posted the lowest 2026 rate increases and may offer competitive pricing for businesses willing to evaluate a less established local network. The carrier comparison guide covers individual market network details that apply to small group plans as well, since both markets share the same provider contracts under Maine’s merged market.

Compare Maine Small Business Health Plans

See group plan options from Anthem, Harvard Pilgrim, CHO, and UnitedHealthcare. Check SHOP tax credit eligibility and explore ICHRA alternatives for your Maine business.

Small Business Health Care Tax Credit in Maine

Of Maine’s roughly 150,000 small businesses, those that purchase coverage through the SHOP marketplace may qualify for the federal Small Business Health Care Tax Credit — worth up to 50% of the employer’s premium contributions (35% for tax-exempt organizations). To qualify, the business must have fewer than 25 full-time equivalent employees, pay average annual wages under $58,000, and cover at least 50% of employee-only premium costs. The credit is claimed on the employer’s federal tax return using IRS Form 8941.

The maximum credit applies to businesses with 10 or fewer FTEs and average wages under $30,000, then phases out as employee count approaches 25 and wages approach $58,000. Tax-exempt Maine organizations — including nonprofits, religious organizations, and community health centers — can claim up to 35% as a refundable credit. Small business health insurance in Maine through the SHOP marketplace is accessed via HealthCare.gov’s SHOP portal, which handles small group enrollment for Maine.

Example: Lewiston Auto Repair Shop

A Lewiston auto repair shop with 7 full-time employees averaging $32,000/year in wages purchases SHOP coverage, contributing $500/month per employee toward Anthem Silver small group premiums. Annual employer contribution: $42,000. The Small Business Health Care Tax Credit at approximately 45% (phased based on wages) returns roughly $18,900 — reducing the effective employer cost to $23,100, or about $275/month per employee. Without the credit, the employer pays $500/month per employee — nearly double.

ICHRA — An Alternative to Traditional Group Plans in Maine

An Individual Coverage Health Reimbursement Arrangement (ICHRA) is an alternative to traditional small business health insurance in Maine: employers set a fixed monthly amount per employee — say $400 or $500 — which workers use to buy their own individual plan on CoverME.gov or off-exchange. Contributions are tax-deductible for the business and tax-free to the employee. ICHRAs work well in Maine because the merged market lets those individual plans benefit from the same MGARA reinsurance that stabilizes group rates.

The ICHRA model solves a specific problem for small business health insurance in Maine: geographic carrier variation. While southern Maine counties like Cumberland and York have four carriers competing on CoverME.gov, northern counties like Aroostook and Piscataquis have only three — and provider networks differ significantly. A Brunswick manufacturing company with 12 employees spread across Cumberland, Sagadahoc, and Lincoln counties could set a $450/month ICHRA allowance and let each employee choose the carrier that best covers their local providers, rather than locking everyone into a single group plan network. Employees earning under 400% of the federal poverty level may also pair their allowance with marketplace subsidies — the low-cost coverage and subsidy options guide covers how those CoverME.gov savings work for individual Maine buyers.

ICHRA works well when

Employees are spread across multiple Maine counties with different carrier availability. The business wants predictable, fixed monthly costs. Employees have diverse healthcare needs and prefer choosing their own plan type and metal tier on CoverME.gov. Some employees may qualify for individual market subsidies.

Traditional group works well when

All employees are in the same county with the same carrier options. The business qualifies for the SHOP tax credit (under 25 FTE, wages under $58,000). Employees prefer having the employer handle plan selection. The employer wants to offer a single plan with uniform benefits across all staff.

How to Set Up Small Business Health Insurance in Maine

Setting up small business health insurance in Maine involves four decisions: coverage type (group plan, SHOP, or ICHRA), carrier selection (Anthem, Harvard Pilgrim, CHO, UnitedHealthcare, or Mending for group plans), contribution level (minimum 50% of employee-only premiums for SHOP tax credit eligibility), and enrollment timing. Small group plans in Maine can start any month — there is no restriction to open enrollment periods. A licensed enrollment assistant can run quotes across all carriers at no cost to the business.

Determine your employee count and budget

Count full-time equivalent employees (30+ hours/week). Maine businesses under 25 FTE with average wages under $58,000 should evaluate SHOP for the tax credit. Businesses with 1–5 employees may find ICHRA or QSEHRA more cost-effective than traditional group rates — particularly if employees qualify for subsidies on CoverME.gov.

Choose a coverage approach

Traditional group plan (employer selects carrier and plan), SHOP via HealthCare.gov (employees may choose metal tier, tax credit available), or ICHRA (employer sets dollar amount, employees buy their own plans on CoverME.gov). Each has different administrative and cost implications — and Maine’s merged market means individual plans purchased through ICHRA carry the same MGARA reinsurance benefits as group plans.

Get quotes from Maine small group carriers

For group plans: provide employee census data (ages, zip codes, tobacco status) for accurate quotes from Anthem, Harvard Pilgrim, CHO, UnitedHealthcare, and Mending. Anthem typically offers the most competitive small group rates in Maine with the broadest network. UnitedHealthcare posted the lowest 2026 rate increases at 8.1%–8.4%.

Enroll and communicate to employees

Group plans can start the first of any month — no open enrollment restriction. SHOP enrollment goes through HealthCare.gov’s small business portal. For ICHRA, set up the arrangement with a third-party administrator and communicate the monthly allowance to employees so they can select individual plans on CoverME.gov. Coverage activates once the first premium payment clears.

Frequently Asked Questions About Maine Small Business Health Insurance

Is health insurance required for small businesses in Maine?

No. Maine has no state employer mandate requiring businesses to offer health insurance. The federal ACA employer mandate applies only to Applicable Large Employers with 50 or more full-time equivalent employees. Maine businesses with fewer than 50 FTEs can offer small business health insurance voluntarily without penalty for not providing it. The vast majority of Maine businesses fall below the 50-FTE threshold.

What is Maine’s merged market and how does it affect my group plan?

Since 2023, Maine has merged its individual and small group health insurance markets into a single risk pool, stabilized by the MGARA reinsurance program. This means small group premiums are based on the combined claims experience of both markets rather than the small group pool alone — which was previously smaller and more volatile. MGARA covers 60% of eligible high-cost claims for 2026, reducing premiums by approximately 10–15% below what they would be without reinsurance. This benefits small employers without any action on their part.

Which carriers offer small group plans in Maine?

Six carriers serve the Maine small group market for 2026: Anthem Health Plans of Maine (largest, ~57% market share), Harvard Pilgrim Health Care, HPHC Insurance Company (Harvard Pilgrim’s PPO arm), Community Health Options, UnitedHealthcare (lowest 2026 rate increases at 8.1%–8.4%), and Mending (formerly Taro Health). Aetna exited the Maine small group market in 2025. Anthem offers both HMO and PPO options with the broadest provider network.

What is the Small Business Health Care Tax Credit?

The tax credit is worth up to 50% of the employer’s premium contributions (35% for tax-exempt organizations) for small businesses purchasing coverage through the SHOP marketplace. To qualify, the business must have fewer than 25 full-time equivalent employees, pay average annual wages under $58,000, and cover at least 50% of employee-only premiums. The maximum credit applies to businesses with 10 or fewer FTEs and average wages under $30,000. Claimed on the federal tax return using IRS Form 8941.

What is an ICHRA and how does it work for Maine small businesses?

An Individual Coverage Health Reimbursement Arrangement lets employers set a fixed monthly dollar amount per employee for health insurance. Employees use that allowance to buy their own individual plan through CoverME.gov or off-exchange. Employer contributions are tax-deductible and tax-free to employees. ICHRAs are well-suited to Maine businesses with employees across multiple counties where carrier availability varies. Because of Maine’s merged market, individual plans purchased on CoverME carry the same MGARA reinsurance benefits as group plans.

How much does small group health insurance cost in Maine for 2026?

Small business health insurance in Maine varies by employee ages, county, carrier, and metal tier. The small group market saw a weighted average rate increase of 17.7% for 2026 — lower than the individual market’s 23.9%. Anthem, the largest small group carrier, approved a 16.0% increase. UnitedHealthcare had the lowest increases at 8.1%–8.4%. Businesses qualifying for the SHOP tax credit can reduce effective costs by up to 50% of their premium contributions. ICHRA costs are fixed at whatever monthly amount the employer sets.

More Maine Health Insurance Guides

Maine’s merged individual and small group market, MGARA reinsurance, and CoverME.gov shape every coverage decision a small employer makes. These guides cover the statewide overview, top carriers and PPO options, marketplace enrollment, and nationwide PPO plans for businesses with multi-state staff.

Plans, carriers, costs, and enrollment across the Pine Tree State.

Top Maine Carriers & PPO PlansAnthem, Harvard Pilgrim, and Community Health Options compared.

CoverME.gov Marketplace & EnrollmentHow to enroll on Maine’s state exchange, deadlines, and life events.

Nationwide PPO Health InsuranceOut-of-network flexibility and broader provider access nationwide.

Find Small Business Health Insurance for Your Maine Team

Compare group plans, SHOP tax credit eligibility, and ICHRA options for your Maine business. Licensed enrollment assistance at no cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Maine businesses. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.