Affordable Health Insurance in Michigan: 2026 Low-Cost Coverage Options

Affordable health insurance in Michigan for 2026 comes from three sources: premium tax credits on HealthCare.gov (which 90% of Michigan marketplace enrollees qualify for), Healthy Michigan Plan Medicaid for households under 133% FPL, and cost-sharing reductions that lower deductibles and copays for Silver plan enrollees under 250% FPL. Approximately 2.4 million Michiganders are enrolled in Medicaid and Healthy Michigan Plan combined. For marketplace enrollees seeking affordable health insurance in Michigan, average subsidies exceed $380/month, bringing the typical Michigan Silver plan from $486/month to approximately $106/month after subsidy.

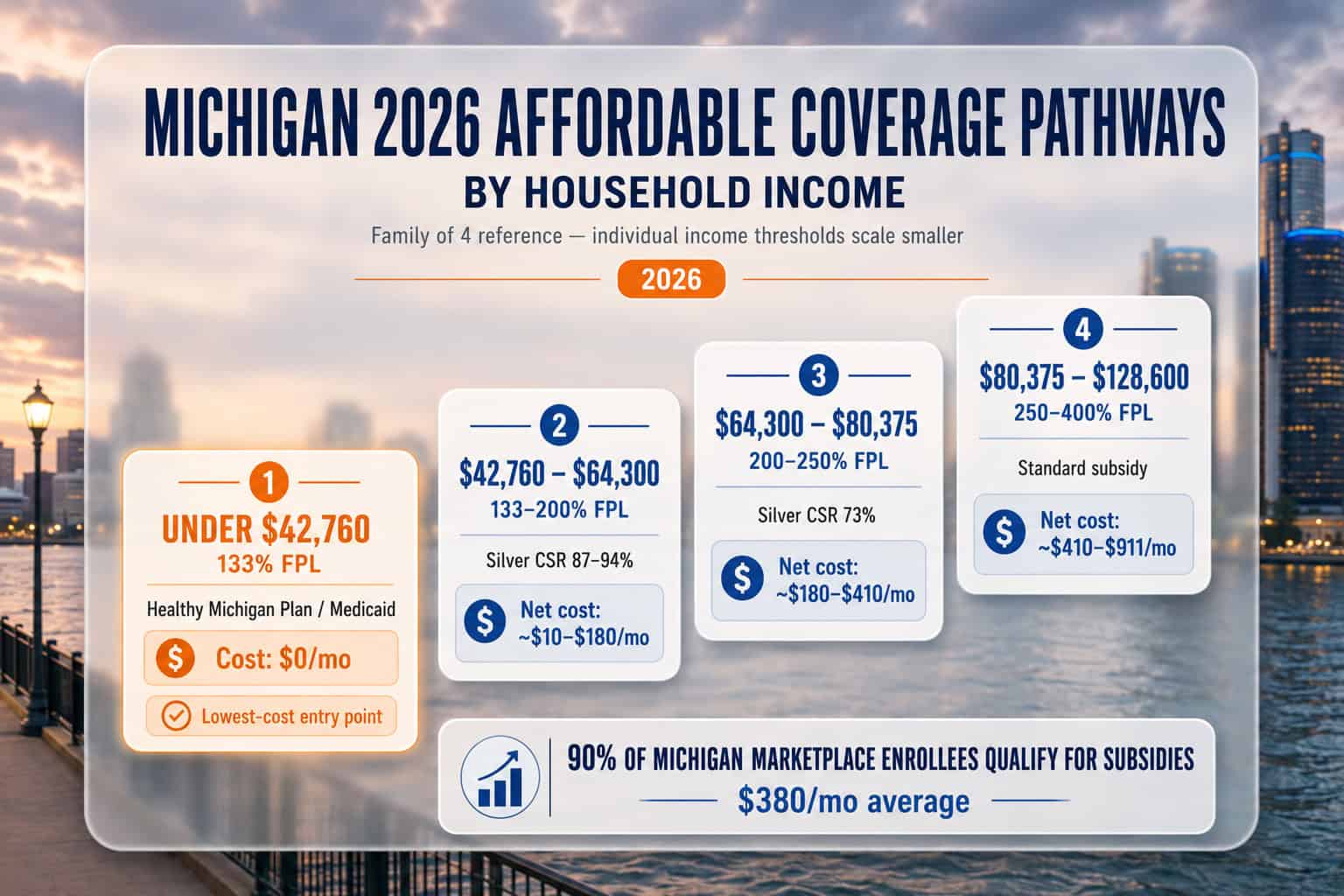

Which affordable path fits your household?

Premium Tax Credits — Michigan’s Biggest Affordability Tool

Approximately 90% of Michigan marketplace enrollees qualify for premium tax credits — one of the highest subsidy participation rates in the nation. The average subsidy is about $380/month, making affordable health insurance in Michigan accessible for most working households. A typical $486/month Silver plan drops to roughly $106/month after subsidy. Eligibility depends on household income relative to the Federal Poverty Level, household size, and the benchmark Silver plan cost in your county.

| Household Size | 100% FPL (minimum) | 400% FPL (threshold) | Expected Contribution at 400% |

|---|---|---|---|

| 1 person | ~$15,650 | ~$62,600 | 8.5% of income ($443/mo) |

| 2 people | ~$21,150 | ~$84,600 | 8.5% of income ($599/mo) |

| 3 people | ~$26,650 | ~$106,600 | 8.5% of income ($755/mo) |

| 4 people | ~$32,150 | ~$128,600 | 8.5% of income ($911/mo) |

| 5 people | ~$37,650 | ~$150,600 | 8.5% of income ($1,067/mo) |

Michigan’s subsidy participation rate of 90% reflects the state’s demographic and economic profile — a large working middle-class population with household incomes falling in the subsidy-eligible range between approximately $20,000 and $125,000 for a family of four. Premium tax credits work by capping the amount a household pays for the benchmark (second-lowest-cost) Silver plan as a percentage of income. Under enhanced subsidies in effect through 2025, households earning up to 400% FPL paid no more than 8.5% of income for the benchmark plan, and the subsidy extended above 400% FPL to prevent the historical “subsidy cliff.”

Enhanced subsidy expiration risk: Enhanced premium tax credits enacted under the American Rescue Plan and extended by the Inflation Reduction Act are scheduled to expire. Without Congressional extension, the pre-2021 subsidy structure returns — cutting off eligibility entirely at 400% FPL and hitting older Michiganders hardest. An estimated 40,000 Michigan families currently enrolled through HealthCare.gov would no longer qualify for subsidies under the old rules. Modeling your 2026 and 2027 income carefully with an enrollment assistant can preserve thousands of dollars in subsidies.

Cost-Sharing Reductions (CSR) on Silver Plans

Beyond premium tax credits, Michiganders earning under 250% FPL who enroll in a Silver plan on HealthCare.gov qualify for Cost-Sharing Reductions — additional subsidies that lower deductibles, copays, and out-of-pocket maximums. A Wayne County household earning $35,000 (about 233% FPL) can see their Silver plan deductible reduced from approximately $4,000 to around $800, and their out-of-pocket max cut roughly in half. CSR is automatic when enrolling in a Silver plan — no separate application required.

Cost-sharing reductions are one of the most valuable but least-understood affordability tools. Bronze plans have lower premiums than Silver, but Bronze plans don’t qualify for CSR — so a subsidized Silver plan often has both lower premiums AND lower deductibles than a Bronze plan for households under 250% FPL. A Kent County family earning $55,000 typically pays less overall for a Silver CSR plan than a Bronze plan with the same subsidy applied. Always compare Silver CSR options first if household income is below 250% FPL.

| Income Level (2026) | CSR Plan Variant | Silver Deductible | Out-of-Pocket Max |

|---|---|---|---|

| Under 150% FPL | Silver 94% CSR | ~$100–$500 | ~$2,500–$3,100 |

| 150%–200% FPL | Silver 87% CSR | ~$500–$1,500 | ~$3,100–$3,500 |

| 200%–250% FPL | Silver 73% CSR | ~$2,000–$3,500 | ~$6,700–$7,050 |

| Above 250% FPL | Standard Silver (no CSR) | ~$4,000–$5,500 | ~$9,450 |

Healthy Michigan Plan and Medicaid

Healthy Michigan Plan is Michigan’s Medicaid expansion program covering adults ages 19–64 with household income up to 133% of the Federal Poverty Level — approximately $20,783 for a single adult or $42,760 for a family of four in 2026. Approximately 2.4 million Michiganders are enrolled in Medicaid and Healthy Michigan Plan combined. Coverage is comprehensive with low copays and no monthly premium for most enrollees. Apply through MDHHS; year-round enrollment available.

Healthy Michigan Plan covers essential health benefits comparable to ACA marketplace plans — preventive care, hospitalization, prescriptions, mental health, maternity, and pediatric care. Small copays apply for some services, and higher-income Healthy Michigan Plan enrollees (100–133% FPL) may contribute modest monthly premiums capped at 2% of income. Medicaid (traditional) covers households under 100% FPL, children under CHIP, pregnant women, seniors, and people with disabilities. Combined, the two programs provide Michigan’s largest source of free or low-cost health coverage.

The transition between Healthy Michigan Plan and marketplace coverage matters enormously for Michigan households whose income fluctuates. Losing Medicaid eligibility due to an income increase triggers a Special Enrollment Period on HealthCare.gov, and premium tax credits typically make affordable health insurance in Michigan nearly free for households just above 133% FPL. Apply for Healthy Michigan Plan through Michigan Department of Health and Human Services. The Michigan marketplace guide covers the SEP triggers and enrollment timing.

DALL-E prompt:

Filename: mi-affordable-coverage-pathways-2026.jpg

Tool: ChatGPT / GPT Image

Scene type: Data visual — income pathway ladder

State anchor: Michigan — 2026 affordable coverage pathways by income

═══ CONTENT ═══

Title: “Michigan 2026 Affordable Coverage Pathways by Household Income”

Subtitle: “Family of 4 reference — individual income thresholds scale smaller”

Layout: Four ascending income tiers as labeled cards, lowest income at the bottom rising to highest

Tier 1 (bottom): “Under $42,760 (133% FPL)” — Healthy Michigan Plan / Medicaid — Cost: $0/mo

Tier 2: “$42,760 – $64,300 (133–200% FPL)” — Silver CSR 87–94% — Net cost: ~$10–$180/mo

Tier 3: “$64,300 – $80,375 (200–250% FPL)” — Silver CSR 73% — Net cost: ~$180–$410/mo

Tier 4 (top): “$80,375 – $128,600 (250–400% FPL)” — Standard subsidy — Net cost: ~$410–$911/mo

Footer line: “90% of Michigan marketplace enrollees qualify for subsidies — $380/mo average”

═══ DESIGN SYSTEM ═══

Premium Infographic System: soft shadows under tier cards and ladder rails, subtle bevel/edge lighting, consistent top-left light source, layered surfaces. Strong title hierarchy (bold, spaced, centered), clean numeric emphasis (dollar amounts and percentages larger and heavier), consistent spacing between tiers. Card-based layout with rounded corners and padding, grid-aligned, an ascending-ladder motif connecting the tiers. Minimal embedded indicators (small income-scale marks).

Color treatment: Apply the brand primary color (teal-blue) as a gradient fill across the tier cards, deepening toward the top. Apply the brand accent color (warm orange) to the lowest-cost Healthy Michigan tier (the $0 entry point the eye should land on). Supporting color: any single mid-tone color from the analogous blue-green/blue-violet families OR the triadic warm red/burgundy/mustard/gold families, medium-low saturation, used only for a subtle divider or the top-tier accent. Pair with a light cream or parchment background (not pure white). Do not select a supporting color that competes with the brand orange accent. Do not display any color name or color code on the image.

═══ HARD RULES (non-negotiable) ═══

• Exact dimensions: 1200×800px — no deviation

• No text overflow — all tier labels and cost callouts must fit inside their cards with comfortable padding

• Proportional data scaling — the four tiers read as an ascending income ladder, aligned to a common baseline

• No spelling errors in any text — double-check every word

• No human subjects

• No flat grey tables, harsh outlines, or misaligned spacing

• No design specifications, color codes, RGB values, or prompting instructions may appear as visible text in the final image. Treat all color references as paint instructions, never as content.

Get Your After-Subsidy Michigan Coverage Quote

See exactly what you’ll pay after premium tax credits. A licensed enrollment assistant can confirm Healthy Michigan Plan eligibility, check Silver CSR options, and find the lowest-cost plan for your household.

Lowest-Cost Michigan Marketplace Plans for 2026

The lowest-cost plans for affordable health insurance in Michigan for 2026 vary by county. In west Michigan (Kent, Ottawa, Kalamazoo counties), Priority Health typically offers the lowest Silver premium at approximately $445/month for a 40-year-old before subsidies — thanks to its 14.4% rate increase (lowest among major Michigan carriers). In southeast Michigan, Meridian (Ambetter) and Blue Care Network compete for the lowest HMO premiums. BCBS PPO is the highest-priced Silver option but the only statewide PPO choice.

Finding affordable health insurance in Michigan starts with one key idea: for subsidized Michiganders, “lowest cost” is determined by after-subsidy price, not sticker price. Premium tax credits adjust based on the benchmark Silver plan — so a Bronze plan may have a $0 or near-$0 after-subsidy premium for some households while Gold plans may cost only modestly more. The smartest way to compare is on total annual cost — premiums plus deductibles plus expected copays — rather than the monthly premium number alone, since a slightly higher premium often buys a far lower deductible that saves money for anyone who uses care during the year. For a side-by-side look at how the major insurers stack up on price and network, the Michigan carrier ranking guide compares BCBSM, Priority Health, Blue Care Network, and Meridian directly.

Under 250% FPL

Choose SilverSilver plans unlock Cost-Sharing Reductions that dramatically lower deductibles and out-of-pocket maximums. A subsidized Silver plan typically costs less overall than Bronze for households under 250% FPL because of the CSR structure.

Over 250% FPL

Compare tiersWithout CSR, Bronze plans have the lowest premiums but the highest deductibles. Silver plans cost more monthly but have lower deductibles. Calculate total annual cost assuming moderate use — often Bronze wins for healthy enrollees, Silver wins for those with regular prescriptions or chronic conditions.

West Michigan

Priority HealthPriority Health offers the lowest Silver premium in Kent, Ottawa, Muskegon, and Kalamazoo counties, integrated with Corewell Health and Bronson Healthcare networks. Its 14.4% rate increase was the lowest among major Michigan carriers for 2026.

Detroit Metro

BCN or MeridianBlue Care Network (BCBS HMO affiliate) and Meridian (Ambetter) typically offer the lowest HMO premiums in Wayne, Oakland, and Macomb counties. Both are strong value options for Michiganders who don’t need out-of-network coverage or PPO flexibility.

Example: Wayne County Family of 4, $58,000 Income

A Wayne County family of 4 (two adults 36 and 38, two children ages 8 and 10) earns $58,000 — approximately 180% FPL. Their 2026 options: Blue Care Network Silver family plan at approximately $1,245/month full price minus approximately $1,090/month in premium tax credits = about $155/month after subsidy. Because the household is under 200% FPL, the Silver plan includes Cost-Sharing Reductions that reduce the deductible from approximately $4,000 to roughly $700 per person. Total annual cost (premium + deductible if fully used + copays) is dramatically lower than Bronze for a family of 4.

Affordability Strategies for Michigan Households

Beyond subsidies and Healthy Michigan Plan, several strategies help households find affordable health insurance in Michigan for 2026: accurate income projection (underestimating means owing back at tax time; overestimating means paying too much upfront), HSA contributions to reduce MAGI, strategic use of Roth vs. traditional retirement withdrawals for early retirees, and rechecking subsidy eligibility after life events that change household income.

Income projection is the single most important affordability lever. Premium tax credits are calculated based on projected annual household income, not current paycheck. Self-employed Michiganders, gig workers, and households with variable income should project conservatively and update HealthCare.gov mid-year if circumstances change. The IRS reconciles subsidies at tax time using Form 8962 — if actual income exceeded projection, the difference is owed back; if actual income fell below projection, additional credits are refunded.

For households near the 133% FPL threshold — the Healthy Michigan Plan boundary — small income changes have outsized effects on coverage. A Detroit household at $42,500 qualifies for Healthy Michigan Plan. At $43,000 they qualify for marketplace coverage with approximately $400/month in subsidies. Either pathway is affordable, but the administrative process differs. HSA contributions (which reduce MAGI) or deductible traditional IRA contributions can be used strategically to keep households within the preferred pathway — especially for Michiganders whose marketplace network is stronger than their local Medicaid HMO network. The CMS Premium Tax Credit flow chart walks through the eligibility logic step by step.

Frequently Asked Questions About Affordable Michigan Coverage

What’s the cheapest health insurance in Michigan for 2026?

Free coverage through Healthy Michigan Plan is available for adults earning under 133% FPL — approximately $20,783/year for a single adult. For marketplace enrollees, Priority Health typically offers the lowest Silver premium in west Michigan at approximately $445/month before subsidies. After premium tax credits, 90% of Michigan marketplace enrollees pay significantly less than sticker price — average net cost is approximately $106/month.

How do I qualify for Michigan marketplace subsidies?

Premium tax credit eligibility depends on household income relative to the Federal Poverty Level. Households earning between 100% and 400% FPL (approximately $15,650 to $62,600 for a single adult or $32,150 to $128,600 for a family of four) typically qualify. Enhanced subsidies extended eligibility above 400% FPL through 2025. Apply through HealthCare.gov to calculate your subsidy automatically.

Who qualifies for Healthy Michigan Plan?

Healthy Michigan Plan covers adults ages 19–64 with household income up to 133% FPL — approximately $20,783 for a single adult or $42,760 for a family of four in 2026. Coverage includes essential health benefits with low copays and no monthly premium for most enrollees. Apply through the Michigan Department of Health and Human Services; year-round enrollment is available regardless of Open Enrollment.

What are Cost-Sharing Reductions in Michigan?

Cost-Sharing Reductions (CSR) are additional subsidies that lower deductibles, copays, and out-of-pocket maximums for enrollees under 250% FPL who choose a Silver plan on HealthCare.gov. CSR is automatic — no separate application needed. A Wayne County household earning $35,000 can see their Silver plan deductible reduced from approximately $4,000 to around $800 through CSR. Only Silver plans qualify for CSR.

Can I get affordable Michigan health insurance if I earn too much for a subsidy?

Households above 400% FPL face the full premium without enhanced subsidy extension. Strategies include: choosing the lowest-premium Bronze plan, using an HSA-eligible high-deductible plan paired with HSA contributions, comparing off-exchange plans for potentially different options, or considering ICHRA if self-employed with employees. A licensed broker can run scenarios based on specific household income and preferences.

What happens if my income changes during 2026?

Report income changes to HealthCare.gov immediately. Income increases reduce your premium tax credit (you’ll owe less or nothing back at tax time). Decreases increase your subsidy. Ignoring changes creates a surprise tax bill in April. Household changes — marriage, divorce, new dependent, someone aging off Medicaid — also affect subsidies and should be reported promptly.

Michigan Health Insurance Resources

Explore related guides for Michigan marketplace enrollment, strategies for finding affordable coverage, top carrier comparisons, small business and group plans, and PPO options to help navigate health insurance decisions across the Great Lakes State.

Plans, costs, carriers, and enrollment basics for the whole state.

Marketplace & EnrollmentHow to enroll on HealthCare.gov, deadlines, and qualifying life events.

Small Business & Group PlansSHOP, ICHRA, and group coverage options for Michigan employers.

PPO Health Insurance PlansNationwide out-of-network flexibility for specialists and travel.

Find Affordable 2026 Coverage for Your Michigan Household

See your exact after-subsidy cost, check Healthy Michigan Plan eligibility, and compare Silver CSR plans. Free, licensed enrollment assistance at no cost to you.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Michigan residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.