Cheap Health Insurance in Alaska: Lowest-Cost Options for 2026

Alaska’s unsubsidized premiums are the highest in the country — but most residents never pay them. During the 2025 plan year, 89% of Alaska marketplace enrollees received subsidies averaging $1,008/month, bringing the average net premium down to $115/month. For 2026, subsidy amounts are smaller than prior years following the expiration of enhanced federal subsidies, but significant help is still available for households earning under 400% FPL. This guide focuses on cheap health insurance in Alaska for 2026: which plan types cost the least, who qualifies for $0 premiums, and where the real trade-offs are.

What are you looking for?

Cheapest Health Insurance Plans in Alaska

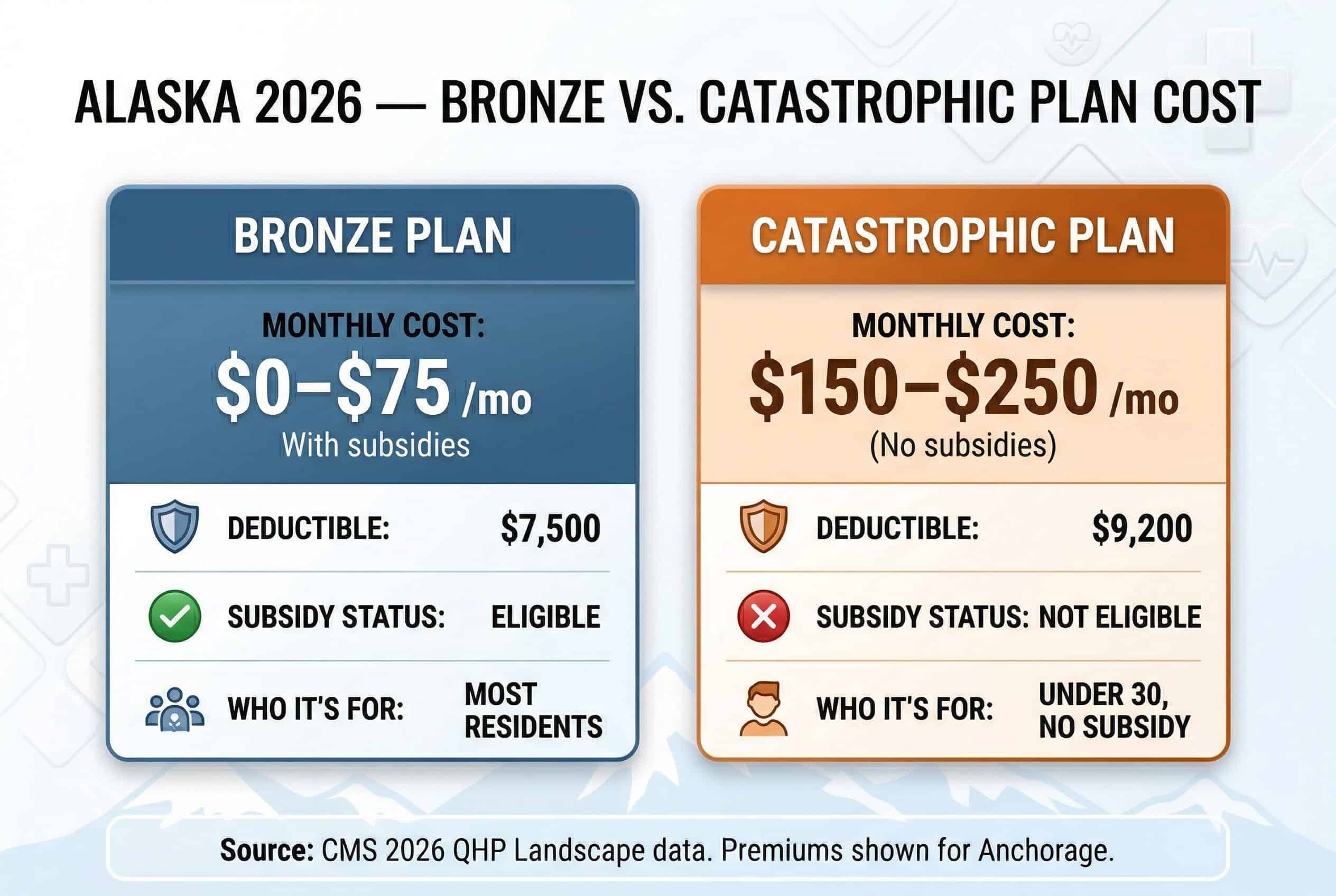

According to CMS marketplace data, the cheapest health insurance in Alaska falls into three categories: Bronze marketplace plans (lowest premiums for most residents after subsidies), Catastrophic plans (lowest sticker price for those under 30), and Medicaid (free for qualifying low-income residents). Bronze plans typically win on total cost because subsidies dramatically reduce premiums while Catastrophic plans receive no subsidy help.

| Plan Type | Monthly (Before Subsidies) | Monthly (After Subsidies) | Deductible | Best For |

|---|---|---|---|---|

| Bronze Plan | $485/mo (40 y/o) | $0–$75/mo | $7,500 | Most subsidy-eligible residents |

| Catastrophic Plan | $225/mo (28 y/o) | No subsidies available | $9,200 | Under 30, no subsidy eligibility |

| Medicaid | $0 | $0 | $0 | Income under 138% FPL |

| Bronze HSA Plan | $460/mo (40 y/o) | $0–$60/mo | $7,500 | Self-employed, tax-advantaged savings |

Premiums shown are pre-subsidy estimates for reference ages. Actual costs vary by income, zip code, and plan selection. Source: CMS 2026 QHP Landscape data.

⚠ 2026 Subsidy Changes

Enhanced federal subsidies that were in place from 2021–2025 expired at the end of 2025 and were not extended by Congress. For 2026, the subsidy cliff is back at 400% FPL ($78,200 single) — households above that threshold receive no premium tax credits. Residents shopping for cheap health insurance in Alaska who were subsidy-eligible in 2025 may still qualify but will generally receive smaller credits than last year. Always run a current quote through HealthCare.gov to see your actual 2026 subsidy amount.

Subsidized Bronze plans are the cheapest health insurance option in Alaska for most residents. The math changes only for those ineligible for subsidies (income above 400% FPL) or young adults under 30 who prefer Catastrophic coverage.

Who Qualifies for the Cheapest Rates

According to HHS poverty guidelines, the cheapest health insurance rates in Alaska go to residents who qualify for maximum subsidies — generally those earning 100–200% of the federal poverty level. At these income levels, Bronze plans often cost $0/month after tax credits. Even residents earning up to 400% FPL typically pay under $100/month for Bronze coverage thanks to Alaska’s exceptionally high subsidy amounts.

$0/Month Bronze

100–200% FPLIncome Range: $19,550–$39,100 (single person)

Who Qualifies: Individuals at 100–200% FPL receive subsidies large enough to reduce Bronze premiums to $0. This includes part-time workers, gig economy participants, and self-employed individuals with modest income.

The Catch: $7,500 deductible before most coverage kicks in. Preventive care is free.

$25–$50/Month Bronze

200–300% FPLIncome Range: $39,100–$58,650 (single person)

Who Qualifies: Individuals at 200–300% FPL. Subsidies cover most of the premium. Common for full-time workers at moderate wages or seasonal workers averaging mid-range income.

The Catch: Same high deductible. Consider Silver CSR if income is under 250% FPL.

$75–$150/Month Bronze

300–400% FPLIncome Range: $58,650–$78,200 (single person)

Who Qualifies: Individuals at 300–400% FPL. Subsidies still provide significant help. Includes many professionals, skilled tradespeople, and small business owners.

The Catch: Approaching the subsidy cliff at 400% FPL — earning $78,201 means paying full price.

$485+/Month (Full Price)

Above 400% FPLIncome Range: Above $78,200 (single person)

Who Qualifies: Nobody “qualifies” — this is the unsubsidized rate. Residents above 400% FPL pay full premiums, making Alaska the most expensive state for unsubsidized coverage.

Alternative: Consider Catastrophic (if under 30) or employer coverage if available.

Bronze vs. Catastrophic: Which Is Actually Cheaper

According to HealthCare.gov plan categories, Bronze plans beat Catastrophic plans on price for anyone who qualifies for subsidies — which is 89% of Alaska marketplace enrollees. Subsidies apply to Bronze, Silver, and Gold plans but not Catastrophic coverage. A subsidized Bronze plan at $0–$50/month costs less than an unsubsidized Catastrophic plan at $150–$250/month, making Bronze the cheapest health insurance in Alaska for most residents.

| Feature | Bronze Plan | Catastrophic Plan |

|---|---|---|

| Subsidy Eligible | ✓ Yes | ✗ No |

| Typical Monthly Cost (with subsidies) | $0–$75/mo | $150–$250/mo (no subsidies) |

| Deductible | $7,500 | $9,200 |

| Out-of-Pocket Maximum | $9,200 | $9,200 |

| Free Primary Care Visits | Preventive only | 3 visits/year before deductible |

| Age Restriction | None | Under 30 (or hardship exemption) |

| Best For | Most residents | Young, healthy, no subsidies |

When Catastrophic Plans Make Sense

When shopping for cheap health insurance in Alaska, Catastrophic coverage wins only in narrow circumstances: adults under 30 who earn too much for subsidies (above $78,200 single) or who have income below 100% FPL but don’t qualify for Medicaid. In these cases, the $150–$250/month Catastrophic premium beats the $485/month unsubsidized Bronze. For everyone else, subsidized Bronze costs less.

Real Examples: What Cheap Coverage Actually Costs

Abstract numbers don’t capture what cheap health insurance looks like in practice. These real-world examples show what Alaska residents at different income levels actually pay for marketplace coverage — and how the cheapest option varies by situation.

Example 1: Tanya, Barista, Age 26, $24,000/Year Income

The Situation: Tanya works at a coffee shop in Anchorage without employer coverage. At 123% FPL, she qualifies for substantial subsidies.

Her Options:

- Bronze plan: $0/month after $485 subsidy

- Silver plan with CSR: $45/month with $500 deductible (vs. standard $4,500)

The Choice: Tanya chose the $0 Bronze plan since she rarely needs care beyond annual checkups (covered free as preventive). If she expected to use more healthcare, the $45 Silver CSR would provide better value despite the premium.

Example 2: Mike, Electrician, Age 34, $52,000/Year Income

The Situation: Mike runs a one-man electrical business in Fairbanks. At 266% FPL, he qualifies for moderate subsidies but not cost-sharing reductions.

His Options:

- Bronze plan: $85/month after subsidies ($7,500 deductible)

- Bronze HSA plan: $75/month after subsidies (HSA-compatible for tax savings)

- Silver plan: $205/month after subsidies ($4,500 deductible)

The Choice: Mike selected the Bronze HSA plan at $75/month. He contributes $300/month to his HSA, deducts those contributions on Schedule 1, and uses the funds for occasional urgent care visits. His effective cost after tax savings: approximately $50/month.

Example 3: Sarah, Software Developer, Age 29, $85,000/Year Income

The Situation: Sarah works remotely from Juneau for a Seattle company that doesn’t offer health insurance. At 435% FPL, she’s above the subsidy cliff.

Her Options:

- Bronze plan: $485/month (no subsidies, full price)

- Catastrophic plan: $195/month (no subsidies, but lower base price)

The Choice: Sarah chose the Catastrophic plan at $195/month — saving $290/month compared to Bronze. Since she’s healthy and under 30, the higher deductible ($9,200 vs. $7,500) is acceptable for the premium savings of $3,480/year.

Check Your Subsidy Amount

Subsidy amounts vary by zip code, income, and household size. Enter your information to see which Bronze and Catastrophic plans are available in your area.

How to Get the Cheapest Health Insurance in Alaska

Finding cheap health insurance in Alaska requires understanding how subsidies work and timing enrollment strategically. The difference between paying $0/month and $500/month often comes down to where you enroll, when you enroll, and which plan type you select.

Enroll Through HealthCare.gov

Step 1Subsidies only apply to marketplace plans — not plans bought directly from Premera. According to HealthCare.gov, even residents earning $50,000+ still receive substantial subsidies in Alaska. Always check before assuming you don’t qualify.

Choose Bronze for Lowest Premiums

Step 2If the only goal is the cheapest monthly payment, Bronze wins. After subsidies, Bronze plans cost $0–$75/month for most Alaska residents. Accept the $7,500 deductible as catastrophic protection and use free preventive care for routine needs.

Consider HSA-Compatible Bronze

Step 3Bronze HSA plans cost slightly less than standard Bronze and allow tax-deductible Health Savings Account contributions. Self-employed individuals can deduct both premiums and HSA contributions, potentially saving $2,000–$4,000 in taxes annually.

Review Plans Every Year

Step 4Premiums, subsidies, and plan designs change annually. Spend 30 minutes during Open Enrollment comparing options — savings of $50–$200/month are common when switching. The cheapest plan last year may not be cheapest this year.

What Cheap Health Insurance in Alaska Covers

Cheap health insurance in Alaska covers the same essential health benefits as expensive plans — the difference is how costs are shared. All marketplace plans must cover doctor visits, hospitalization, prescriptions, maternity care, mental health services, preventive care, emergency services, lab work, pediatric services, and rehabilitation. No Alaska marketplace plan can exclude pre-existing conditions or impose lifetime coverage limits.

Free Before Deductible

Preventive- Annual wellness exams

- Immunizations

- Preventive screenings (mammograms, colonoscopies, etc.)

- Contraception

- Pediatric preventive care

After $7,500 Deductible

Routine Care- Doctor visits for illness or injury

- Urgent care

- Prescription drugs

- Lab work and imaging

- Specialist visits

Major Medical

After Deductible- Hospitalization

- Surgery

- Emergency room

- Maternity and newborn care

- Mental health and substance abuse treatment

Financial Protection

ACA Guarantee- Out-of-pocket maximum: $9,200

- No lifetime limits

- No coverage caps

- Pre-existing conditions covered

- All 10 essential health benefits required

⚠ The Trade-Off with Cheap Plans

The $7,500 deductible on Bronze plans means paying full price for most non-preventive care until that threshold is met. A single ER visit or minor surgery can cost $2,000–$5,000 out of pocket. Cheap health insurance in Alaska works best for healthy individuals who primarily need catastrophic protection and preventive care. Those expecting regular healthcare usage may find Silver plans more cost-effective overall despite higher premiums.

Frequently Asked Questions About Cheap Health Insurance in Alaska

Alaska residents searching for cheap health insurance frequently ask about the lowest-cost plan types, subsidy eligibility, Bronze vs. Catastrophic pricing, and what budget-friendly coverage actually includes under ACA marketplace rules for 2026.

What is the cheapest health insurance in Alaska?

Catastrophic plans offer the lowest premiums for adults under 30, starting around $200/month before subsidies. For subsidy-eligible residents, Bronze plans often cost $0–$50/month after tax credits. Many Alaskans pay nothing for Bronze coverage once subsidies are applied.

Can I get free health insurance in Alaska?

Yes. Alaska Medicaid provides free coverage for residents earning up to 138% of the federal poverty level ($26,979 for a single person in 2026). Additionally, many residents earning $20,000–$35,000 qualify for subsidies that reduce Bronze plan premiums to $0/month through HealthCare.gov.

How can I lower my health insurance cost in Alaska?

The most effective strategies include: enrolling through HealthCare.gov to access subsidies (89% of Alaska enrollees receive them), choosing Bronze or Catastrophic plans for lowest premiums, pairing high-deductible plans with HSA accounts for tax savings, and reviewing options annually since prices and subsidies change each year.

Is Bronze or Catastrophic insurance cheaper in Alaska?

For subsidy-eligible residents, Bronze plans are usually cheaper because subsidies apply to Bronze but not Catastrophic plans. A Bronze plan might cost $0–$50/month after subsidies, while Catastrophic plans cost $150–$250/month with no subsidy help. Catastrophic plans are only cheaper for those who don’t qualify for subsidies.

What does cheap health insurance actually cover in Alaska?

All Alaska marketplace plans — including the cheapest Bronze options — cover the 10 essential health benefits: doctor visits, hospitalization, prescriptions, maternity care, mental health, preventive care (free before deductible), emergency services, lab work, pediatric services, and rehabilitation. The difference is cost-sharing, not coverage breadth.

Why is health insurance so expensive in Alaska without subsidies?

Alaska has the highest unsubsidized premiums in the nation due to limited carrier competition (Premera holds the majority of market share), vast geography requiring expensive medical transport, a small population spread across remote areas, and high healthcare delivery costs. Federal subsidies offset these factors for most residents.

Related Alaska Coverage Guides

Explore guides covering marketplace enrollment, subsidy strategies, carrier reviews, plan comparisons, and affordability resources for Alaska residents.

Complete overview of all coverage types in the state.

Marketplace EnrollmentHow to enroll, deadlines, and qualifying life events.

Affordable CoverageSubsidy strategies, CSR benefits, and cost comparisons.

Best Plans ComparedCarrier reviews and plan recommendations by situation.

Premera Blue Cross AlaskaThe dominant carrier in Alaska’s individual market.

PPO PlansFlexibility for specialists and out-of-state care.

Alaska Bronze and Catastrophic Plan Pricing

Finding the cheapest health insurance in Alaska starts with checking subsidy eligibility. Premiums and subsidy amounts differ by region, income level, and household size. Enter your details to see actual plan pricing for your area.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Alaska residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.