Private Medical Insurance Florida: Carriers, Costs & Coverage for 2026

Private medical insurance in Florida opens doors that marketplace plans often cannot — broader doctor networks, faster specialist appointments, and benefits that go well beyond the basics. These plans cost more, but for many Florida residents, the trade-off in access and flexibility makes the difference. This guide breaks down what private coverage actually looks like in 2026, which carriers operate in the state, what it costs at different ages, and how enrollment works.

What are you looking for?

Benefits of Private Medical Insurance in Florida

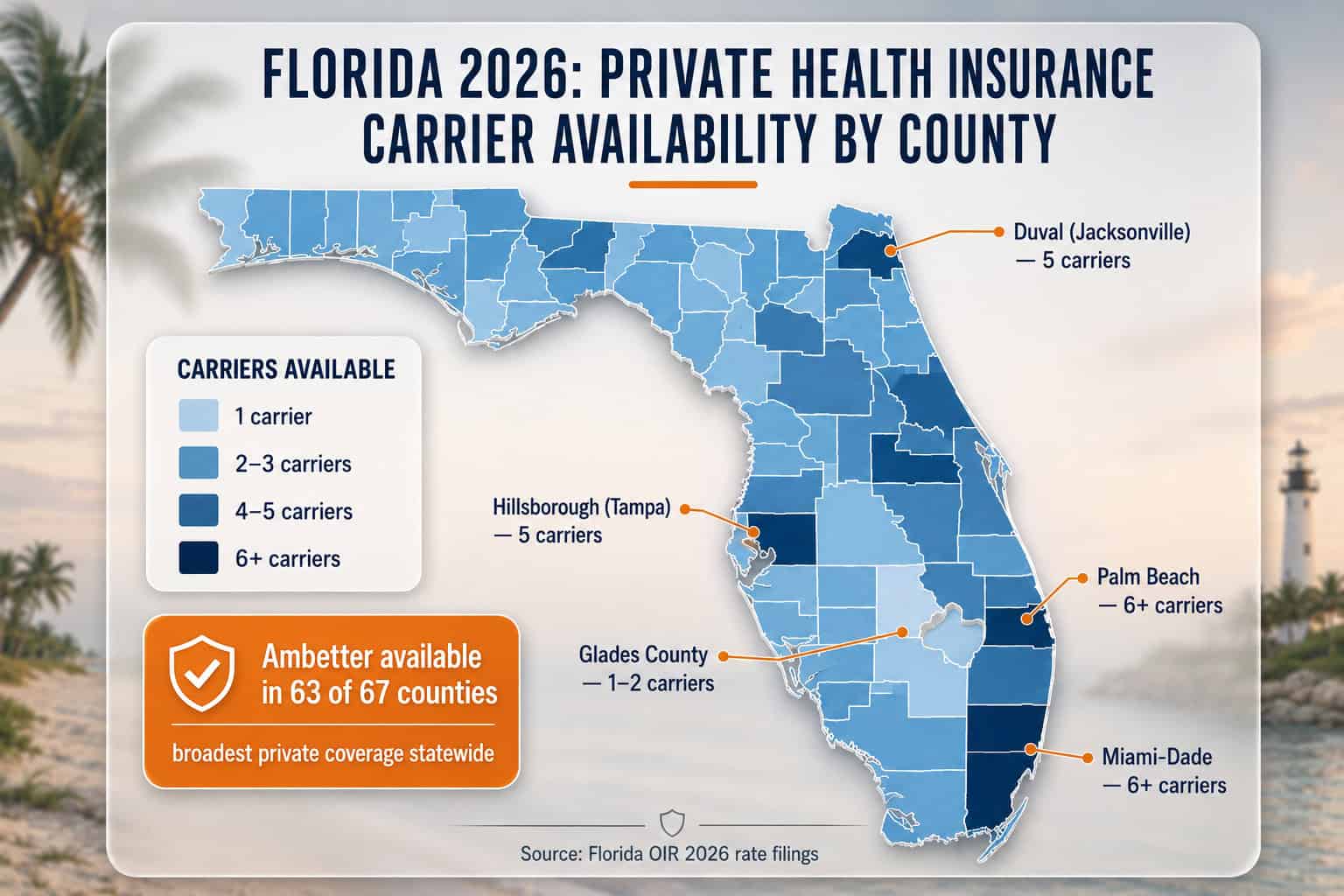

Private medical insurance in Florida provides broader provider networks than marketplace plans — including premium facilities like Mayo Clinic Jacksonville and Cleveland Clinic Florida — plus year-round enrollment, faster specialist access, and enhanced benefits beyond ACA minimums. More than sixteen private carriers operate in Florida as of 2026, giving residents significant choice in coverage levels and network size according to the Florida Office of Insurance Regulation.

In Florida’s private insurance market, that breadth translates to named carrier options — UnitedHealthcare, Florida Blue, Cigna, Ambetter (Centene), Oscar Health, and Molina Healthcare among others — giving residents real choice in network structure and coverage design. According to the Florida Office of Insurance Regulation, eighteen companies write in Florida’s individual health insurance market as of 2026, with sixteen offering coverage through the marketplace and additional carriers operating off-exchange only — a market depth that most southeastern states cannot match.

Bigger Doctor Networks

Premium AccessPrivate plans often include hospitals and specialists that do not accept marketplace insurance, such as Mayo Clinic Jacksonville and Cleveland Clinic Florida. Policyholders can typically see specialists without referrals and experience shorter wait times measured in days rather than weeks.

Enhanced Coverage

Beyond ACABeyond essential health benefits, private plans frequently include international travel coverage, alternative medicine (chiropractic, acupuncture), executive health screenings, and enhanced mental health services that go further than marketplace minimums.

Dedicated Customer Service

ConciergeMany private carriers assign a dedicated account manager who coordinates care, expedites claims, and provides 24/7 nurse advice lines. This replaces the standard call-center experience common with marketplace plan support.

Year-Round Enrollment

No DeadlineUnlike marketplace plans restricted to Open Enrollment or qualifying life events, most private medical insurance in Florida accepts applications any time of year. Coverage can start within days of approval rather than waiting for the first of the following month.

Private vs. Marketplace Insurance in Florida

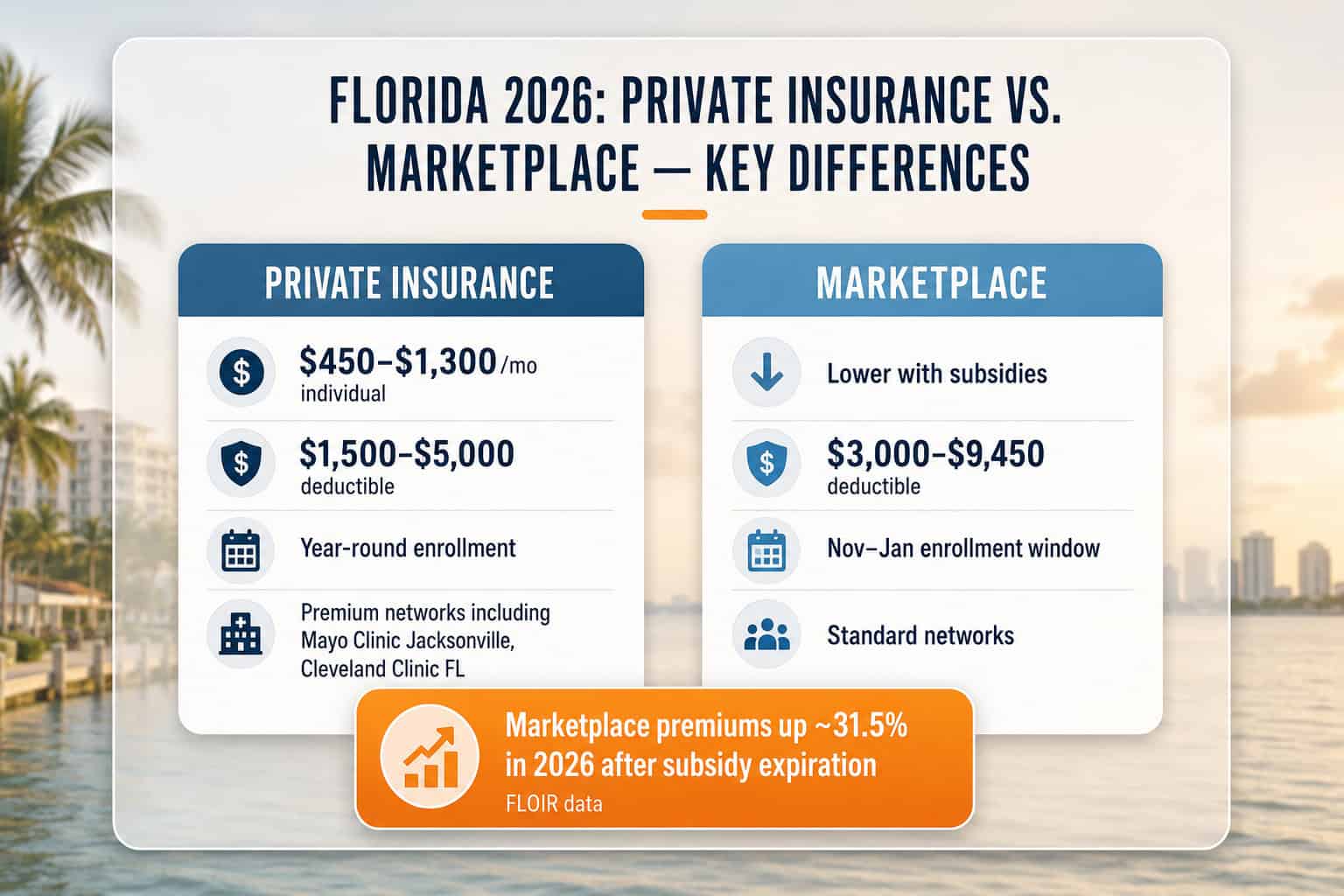

Private medical insurance in Florida typically offers broader networks and faster access to care, while marketplace plans through HealthCare.gov win on price for those who qualify for subsidies. Following the expiration of enhanced federal premium tax credits at the end of 2025, marketplace premiums increased approximately 31.5% on average for many Floridians according to FLOIR rate filings, narrowing the cost gap between private and subsidized coverage significantly.

⚠️ 2026 Subsidy Update

Enhanced federal subsidies expired at the end of 2025, causing marketplace premiums to rise substantially for many Florida residents. As of early 2026, Congress is still considering reinstatement — but no extension has been enacted. Anyone who previously qualified for low-cost marketplace coverage may find private insurance more competitive now or at least worth comparing side by side.

| Feature | Private Medical Insurance | Marketplace Plans | Advantage |

|---|---|---|---|

| Provider Networks | Broader, premium networks | Standard networks | Private Insurance |

| Customer Service | Dedicated support | Standard call centers | Private Insurance |

| Monthly Premiums | $450–$1,300 individual | Lower with subsidies | Marketplace (with subsidies) |

| Coverage Options | Enhanced benefits included | Essential health benefits | Private Insurance |

| Enrollment Timing | Year-round enrollment | Limited enrollment periods | Private Insurance |

| Deductibles | $1,500–$5,000 typical | $3,000–$9,450 typical | Private Insurance |

Real Example: Tampa Couple, Ages 52 and 54

A Tampa couple in their 50s compared options after the 2025 subsidy expiration. Their marketplace Silver plan rose to $1,170/month with a $6,500 deductible. A private PPO from a major Florida carrier came in at $1,380/month with a $2,500 deductible and their cardiologist in-network (who did not accept the marketplace plan). The $210/month difference delivered better access and lower total out-of-pocket costs. Individual results vary based on age, location, and health needs.

Types of Private Health Insurance Available in Florida

Florida residents can choose from four types of private health insurance — individual plans ($450–$900/month), family plans ($1,400–$2,800/month for a family of four), short-term coverage ($150–$400/month for temporary gaps up to 364 days), and supplemental policies ($30–$150/month). Each serves a different need, with individual plans the most common choice for self-employed residents or those between jobs in 2026.

Individual Private Plans

$450–$900/moFor self-employed residents or those between jobs, individual private plans offer year-round enrollment with perks like dental and vision often built in. Florida carriers price these at $450–$900/month depending on age and coverage level. Florida self-employed professionals who also employ others may benefit from group coverage instead — see the Florida small business health insurance guide for ICHRA and traditional group options.

Family Private Plans

$1,400–$2,800/moFamily plans bundle all members under one policy. Pediatric dental and vision are included by law, and many private plans add orthodontic coverage and family wellness programs. Expect $1,400–$2,800/month for a family of four.

Short-Term Private Insurance

$150–$400/moFor temporary gaps, short-term plans in Florida last up to 364 days at $150–$400/month. These skip some ACA requirements and do not cover pre-existing conditions, but serve as a bridge between jobs or coverage periods.

Supplemental Private Insurance

$30–$150/moSupplemental plans fill gaps in existing coverage with better dental, vision, critical illness payouts, or accident protection. These typically run $30–$150/month and can offset thousands in unexpected costs when paired with a primary plan.

Cost of Private Medical Insurance in Florida

Private medical insurance in Florida costs between $450 and $1,300 per month for individual coverage in 2026, based on age, county, and plan type according to Florida OIR rate filings. Family plans range from $1,400 to $3,200 monthly. These premiums exceed subsidized marketplace plans but often deliver lower deductibles and broader networks that reduce total out-of-pocket spending over the plan year.

Private medical insurance in Florida costs between $450 and $1,300 per month for individual coverage in 2026, based on age, county, and plan type according to Florida OIR rate filings. Family plans typically range from $1,400 to $3,200 monthly. These premiums run higher than subsidized marketplace plans, but often deliver lower deductibles and broader networks that reduce total out-of-pocket spending over the plan year.

| Coverage Type | Monthly Premium Range | Typical Deductible | Best For |

|---|---|---|---|

| Individual | $450–$1,300 | $1,500–$5,000 | Self-employed, between jobs |

| Family (4 members) | $1,400–$3,200 | $3,000–$8,000 | Families wanting premium networks |

| Short-Term | $150–$400 | $2,500–$10,000 | Temporary coverage gaps |

| Supplemental | $30–$150 | Varies by type | Gap coverage for existing plans |

What Affects Premium Pricing

Age is the largest factor. A 30-year-old might pay $500/month for the same plan that costs a 55-year-old $1,050/month. Location also matters significantly — Miami-Dade and Hillsborough counties tend to run higher than rural areas. Deductible choice swings pricing too: selecting a $5,000 deductible lowers the monthly premium compared to a $1,500 deductible on the same plan.

Is the Extra Cost Worth It?

In Florida, the answer depends heavily on county and healthcare usage. A Miami-Dade resident paying $1,050/month for a BCBS POS Silver plan on the marketplace after subsidies expired might find that a private UnitedHealthcare PPO at $1,200/month delivers a $2,500 deductible instead of $6,500 — a breakeven after just two specialist visits. In contrast, a healthy 30-year-old in Alachua County with no ongoing conditions would likely save thousands annually on a marketplace Bronze plan priced at roughly $420/month before subsidies.

Payment Options

Most Florida private carriers — including UnitedHealthcare, Cigna, and Florida Blue — accept monthly, quarterly, or annual payments, with modest discounts for annual upfront payment. Several plans, particularly Ambetter’s Expanded Bronze offerings in Florida, qualify as high-deductible health plans (HDHPs) eligible for Health Savings Account pairing. HSA-compatible plans are especially popular among Florida’s large self-employed population, allowing tax-free dollars to offset deductibles that average $2,500–$5,000 on private coverage.

Compare Private Insurance Options in Florida

Private medical insurance in Florida ranges from $450 to $1,300/month for individuals in 2026. Compare personalized quotes from top Florida carriers side by side — coverage options vary by age, county, and health needs.

Top Private Health Insurance Companies in Florida

Florida’s private insurance market features six major carriers for 2026 — UnitedHealthcare for the largest network, Cigna for international coverage, Ambetter (Centene) for the lowest premiums across 63 of 67 counties, Florida Blue for statewide local networks, Molina Healthcare for South Florida value coverage, and Oscar Health for digital-first members. Aetna exited Florida’s individual market entirely at end of 2025.

Florida’s private medical insurance market includes national carriers like UnitedHealthcare and Cigna alongside Florida-based options like Florida Blue and fast-growing marketplace competitors like Ambetter and Molina. Each carrier offers different strengths in network size, specialty access, and premium pricing for 2026. The NAIC complaint index and financial stability ratings help evaluate carrier reliability.

⚠️ 2026 Carrier Change

Aetna (CVS Health) exited the Florida individual market entirely at the end of 2025 — both marketplace and off-exchange plans. Former Aetna members needed to select new coverage during Open Enrollment. Aetna remains available only through employer-sponsored group plans in Florida.

UnitedHealthcare

Largest NetworkThe largest provider network in Florida, ideal for residents who travel the state or want maximum doctor choice. Strong PPO and EPO options with nationwide coverage and robust telehealth services.

Best for: Network size and flexibility

Cigna

Global CoverageStands out for international coverage and mental health benefits. Strong wellness programs and preventive care incentives. Popular with Florida residents who travel abroad frequently.

Best for: International travelers and mental health

Ambetter (Centene)

Lowest CostAvailable in 63 of Florida’s 67 counties, Ambetter consistently offers some of the lowest premiums in the state. Strong option for cost-conscious residents who can work within a more focused provider network.

Best for: Budget-friendly premiums and broad county availability

Florida Blue

Local ExpertiseFlorida’s largest health insurer with deep local networks across all 67 counties. Offers some private-only enhanced benefit plans beyond standard marketplace options.

Best for: Florida-specific networks and local support

Molina Healthcare

Value CoverageGrowing presence across Florida with competitive pricing and a focus on essential coverage. Strong in South Florida markets with streamlined plan options that keep out-of-pocket costs manageable.

Best for: Affordable coverage in South Florida markets

Oscar Health

Tech-ForwardA technology-first carrier with a user-friendly app, included 24/7 telemedicine, and concierge care teams assigned to each member. Growing presence across Florida metro areas in 2026.

Best for: Telemedicine and digital-first experience

How Carriers Are Evaluated

Key comparison factors include financial stability (can the carrier pay claims reliably), customer satisfaction scores from NAIC complaint data, the size and depth of the Florida provider network, and claims processing speed.

Enrollment and Application Process

Private medical insurance in Florida is available year-round through FL OIR-licensed carriers — no Open Enrollment window required. Most applicants receive approval within 2–5 business days, and coverage can begin as quickly as 48 hours after approval depending on the carrier. This makes private coverage the fastest option for Floridians relocating from other states, aging off a parent’s plan, or losing employer coverage mid-year.

Florida’s large retiree and transplant population makes year-round access particularly valuable. Unlike the marketplace, where missing the January 15 deadline means waiting until the following November, Florida carriers like UnitedHealthcare, Cigna, and Florida Blue accept private plan applications on any business day. For recent arrivals from high-cost states like New York or California, this flexibility often determines whether coverage starts before or after a major medical event.

What Applicants Need

Florida applicants typically need: government-issued ID, Social Security number, and income documentation (particularly relevant post-2025 with subsidy expiration affecting more Floridians moving to private coverage). Some carriers operating in Florida — Oscar Health and Cigna among them — have fully digital applications that complete in under 20 minutes. Others, like certain Florida Blue off-exchange plans, may require a brief phone verification step.

About Underwriting

In Florida’s private market, underwriting practices vary by carrier. ACA-compliant plans — including most Florida Blue, UnitedHealthcare, and Ambetter off-exchange offerings — cannot use health history to deny coverage or set rates under federal law. Short-term plans from carriers like Golden Rule (UnitedHealthcare) and Pivot Health do use medical underwriting and may exclude pre-existing conditions. For healthy Floridians in their 30s and 40s, underwritten short-term plans can run $150–$300/month — well below ACA-compliant options — but carry meaningful coverage gaps.

When Coverage Starts

Florida private carriers routinely activate coverage within 48–72 hours of approval — compared to marketplace plans that begin on the 1st of the month following enrollment, sometimes 30+ days away. For a Floridian who loses employer coverage on a Friday, a private plan from UnitedHealthcare or Cigna can be active by Monday. This speed advantage is especially significant in Florida, where the state’s large gig economy and tourism-driven workforce creates frequent mid-year coverage gaps that marketplace enrollment windows simply cannot accommodate.

Florida Health Insurance Resources

Compare plan types, coverage levels, and carrier availability statewide

Best Health Insurance in FloridaTop-rated carriers, network comparison, and plan types by county

Affordable Florida Health InsuranceSubsidies, CSR savings, and low-cost plan options for 2026

Short-Term Health Insurance FloridaTemporary and bridge coverage options for Floridians

Florida Health Insurance MarketplaceHealthCare.gov enrollment, deadlines, and subsidy details

Florida PPO Health InsurancePPO coverage options and provider flexibility statewide

Small Business Health Insurance FloridaGroup plans, SHOP enrollment, and ICHRA options for FL employers

Blue Cross Blue Shield of FloridaFlorida Blue plans, networks, and coverage by county

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required

Frequently Asked Questions About Private Medical Insurance in Florida

Common questions Florida residents ask about private medical insurance — including how it compares to marketplace plans, year-round enrollment availability, pre-existing condition coverage, costs by age and county, and prescription drug benefits in 2026.

What is the difference between private and marketplace insurance in Florida?

Marketplace plans through HealthCare.gov offer subsidies for qualifying applicants but have limited enrollment periods and sometimes smaller provider networks. Private plans cost more but allow year-round enrollment, often include bigger networks with premium hospitals, and may add benefits like international coverage. The right choice depends on budget, healthcare needs, and provider preferences.

Can Florida residents sign up for private insurance any time of year?

Yes. Year-round enrollment is one of the biggest advantages of private medical insurance. There is no need to wait for the November Open Enrollment period like the marketplace. Applications can be submitted any day, and coverage could start within a week of approval.

Does private insurance cover pre-existing conditions in Florida?

Many plans do, especially ACA-compliant private plans. Some non-ACA plans might exclude pre-existing conditions for a waiting period. Being upfront about health history during the application process ensures the best match and avoids claim denials later.

How much does private medical insurance cost in Florida?

Individual private medical insurance in Florida ranges from $450 to $1,300 per month in 2026, depending on age, county, and plan type. Family plans typically run $1,400 to $3,200 monthly. Costs vary significantly based on deductible choice, network type, and additional benefits selected.

Can policyholders see any doctor with private insurance?

In most cases yes, but checking the specific plan’s network first is important. Private plans typically have bigger networks than marketplace plans, and many offer out-of-network coverage at a higher cost share. If a specific doctor or hospital is required, agents can verify network participation before enrollment.

Does private insurance in Florida cover prescriptions?

Yes, and often more comprehensively than marketplace plans. Private plans frequently include broader drug formularies (the list of covered medications), lower copays for brand-name drugs, and mail-order pharmacy options that reduce costs on maintenance medications.

Compare Private Insurance Options in Florida

Compare personalized quotes from Florida’s top private carriers side by side. Coverage options vary by age, county, and health needs — reviewing multiple carriers helps identify the right fit.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Florida residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.