Short-Term Health Insurance in Florida: Costs, Rules & When It Makes Sense

Short-term health insurance in Florida fills a gap that marketplace plans don’t always cover — the months between jobs, the wait for employer benefits, or that stretch after aging off a parent’s plan. But these policies work very differently from ACA coverage, and the cost savings aren’t always what they appear to be once you factor in what’s excluded. This guide walks through how short-term plans actually work in Florida, what they cost versus the alternatives, and how to tell whether one fits your situation.

What brings you here today?

What Is Short-Term Health Insurance?

These temporary plans in Florida provide medical coverage lasting 3 to 12 months for residents between traditional health plans. According to the Florida Office of Insurance Regulation (OIR), these medically underwritten plans can extend up to 36 months with renewals. Premiums typically run $150–$300 per month but exclude pre-existing conditions.

Unlike ACA marketplace plans, short-term coverage does not meet minimum essential coverage requirements and is not sold through HealthCare.gov. Florida’s 4.7 million marketplace enrollees — the highest of any state — all have access to guaranteed-issue ACA plans; short-term applicants face medical underwriting and can be denied. Benefits under short-term plans are significantly more limited, with annual caps and pre-existing condition exclusions that ACA plans prohibit.

Cost Comparison: Short-Term vs. ACA Plans

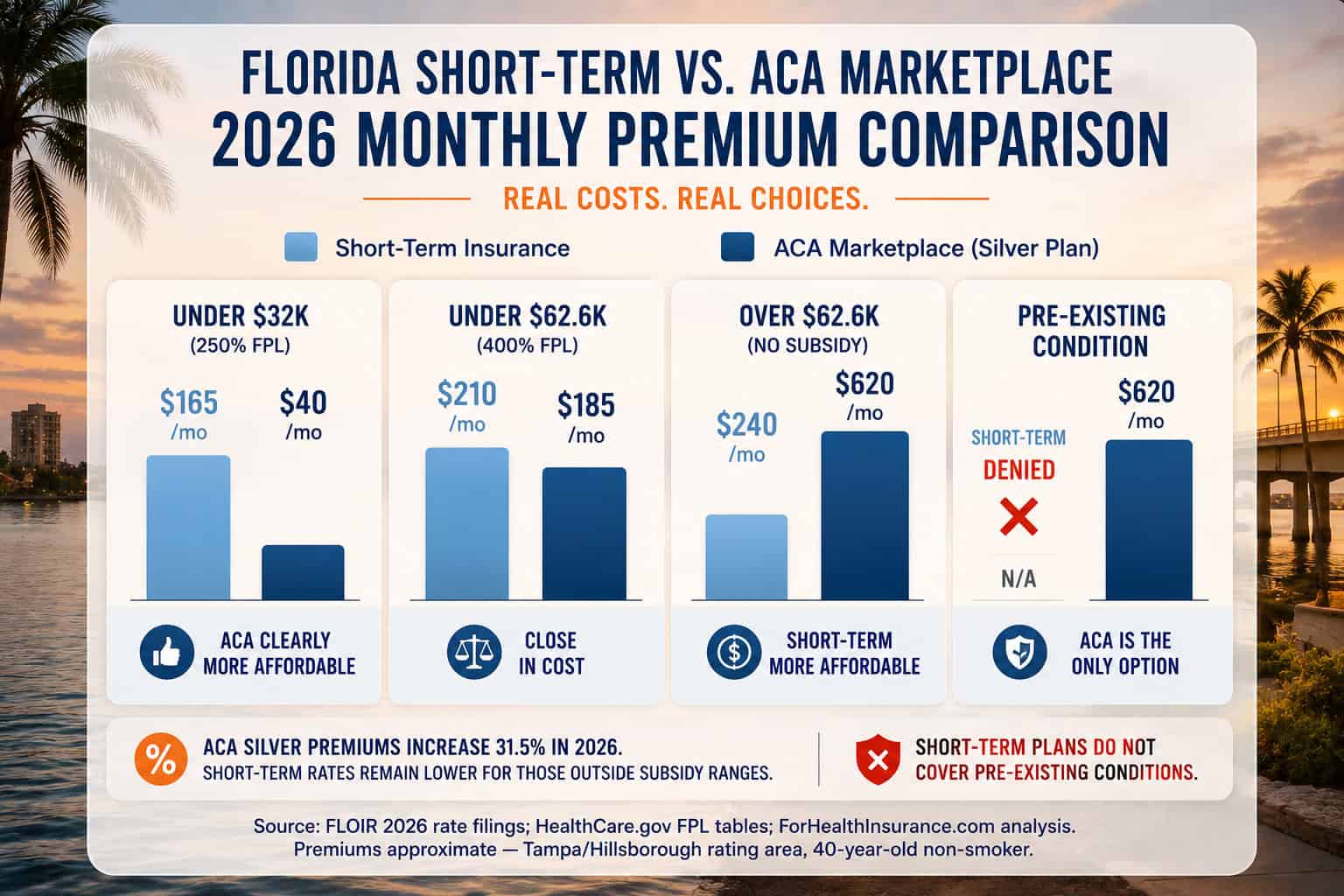

Short-term coverage in Florida costs $150–$300 per month for healthy applicants, roughly 50–70% less than unsubsidized ACA premiums. ACA subsidies still exist in 2026 under original rules, but the enhanced credits expired in December 2025 — meaning fewer residents qualify and those who do receive smaller amounts. For Floridians with income below 400% of the federal poverty level (~$62,600), subsidized ACA plans still likely cost less than short-term coverage. For those above that threshold, the cost comparison shifts significantly.

Short-Term Insurance

$150–$300/moTypical premium for healthy applicants. Medically underwritten — approval not guaranteed.

- ✓ 50–70% lower than unsubsidized ACA

- ✓ Fast approval, starts within days

- ✗ Pre-existing conditions excluded

- ✗ Limited or no prescription coverage

- ✗ Annual and lifetime benefit caps

ACA Marketplace Plans

$80–$300/moWith subsidies (income under ~$62,600). Guaranteed issue — no medical underwriting. Premiums higher than 2025 after enhanced credit expiration.

- ✓ Comprehensive coverage

- ✓ Pre-existing conditions covered

- ✓ Preventive care at no cost

- ✓ Prescription drug coverage included

- ✗ Enrollment periods apply

Real Cost Examples by Profile

| Profile | Short-Term | ACA After Subsidy | Better Value |

|---|---|---|---|

| 25-year-old, $35K income, healthy | $125/mo | $110/mo | ACA |

| 35-year-old, $55K income, healthy | $185/mo | $280/mo | Short-Term* |

| 45-year-old, $75K income, healthy | $275/mo | $650/mo (no subsidy) | Short-Term* |

| 55-year-old, $45K, diabetes | Denied | $210/mo | ACA only |

*Lower premium but significantly less coverage. Pre-existing conditions excluded. Florida short-term plans carry annual benefit caps — commonly $250,000–$1M — versus no lifetime limits on ACA plans.

Check Your Subsidy Eligibility First

Florida marketplace premiums rose an average of 31.5% for 2026 per FLOIR rate filings. Residents earning under $62,600 (400% FPL individual) still qualify for subsidies — compare real after-subsidy estimates to see if ACA coverage beats short-term pricing for your situation.

Compare Options Call 888-215-4045Is Short-Term the Right Fit?

Short-term health insurance in Florida works best for healthy individuals facing a temporary gap of one to six months — between jobs, waiting for employer benefits, or aging off a parent’s plan. It is not appropriate for anyone with pre-existing conditions, ongoing prescriptions, or potential pregnancy. For residents earning under ~$62,600 who still qualify for ACA subsidies, marketplace plans typically offer stronger protection at a comparable cost.

When Short-Term Works

Appropriate- ✓ Between jobs: 1–3 month gap before new employer coverage starts

- ✓ Missed enrollment: Need coverage until the next Open Enrollment period

- ✓ Recent graduate: Aged off a parent plan with a job starting soon

- ✓ Pre-Medicare: Retiring early and waiting for age 65 eligibility

When to Avoid Short-Term

Not Recommended- ✗ Any pre-existing conditions (diabetes, asthma, heart disease, depression)

- ✗ Regular prescription medications

- ✗ Possible pregnancy during coverage period

- ✗ Income under ~$62,600 (likely subsidy-eligible for ACA under 2026 rules)

- ✗ Need for mental health or behavioral health services

Critical Coverage Limitations

Short-term plans in Florida have significant gaps compared to comprehensive Florida health insurance. Florida OIR permits these plans to carry annual and lifetime benefit caps, exclude pre-existing conditions, and skip the 10 ACA essential health benefits — protections that apply to all 16 carriers on the Florida marketplace. Anyone considering short-term coverage should understand these exclusions before enrolling:

- Pre-existing conditions excluded: Diabetes, heart disease, cancer history, asthma, depression, and most chronic conditions are not covered

- Limited prescription coverage: Many plans exclude drugs entirely or carry high copays (fixed per-visit fees)

- Benefit caps: Annual and lifetime maximums mean one serious illness can exceed coverage limits

- No preventive care requirement: Routine screenings may require full out-of-pocket payment

- Mental health often excluded: Unlike ACA plans, short-term coverage is not required to include behavioral health services

- No maternity coverage: Pregnancy is excluded from virtually all short-term plans in Florida

Need Help Deciding?

Florida offers 16 marketplace carriers for 2026 alongside short-term options. For residents above $62,600 (400% FPL), short-term can cost $350–$450 less per month — but coverage gaps are significant. Compare your specific zip code and income to find the right fit.

Get Personalized Comparison Call 888-215-4045How to Apply and Florida Regulations

Applying for short-term health insurance in Florida involves completing a health questionnaire and passing medical underwriting, typically within 24–48 hours. Under Florida OIR regulations, insurers can issue initial terms up to 364 days with total coverage extending to 36 months through renewals — longer than most states allow. Applicants with pre-existing conditions face exclusions or denial; Florida OIR data shows approximately 15–20% of individual short-term applications result in exclusions or modified offers. Unlike the federal marketplace, there are no restricted enrollment windows for these plans in Florida.

Complete Health Questionnaire

Provide accurate medical history including current conditions, medications, and recent treatments. Inaccuracies can void the policy retroactively.

Await Underwriting Decision

Most carriers return a decision within 24–48 hours. Approval is not guaranteed — recent hospitalizations or chronic conditions may result in denial.

Review Exclusions Carefully

Check the exclusion list before accepting. Every pre-existing condition identified during underwriting will be excluded from coverage.

Pay First Premium

Verify your doctors are in-network before paying. Coverage is not active until the first premium payment is received by the carrier.

Florida Short-Term Insurance Rules (2026)

Florida’s short-term plan regulations are more flexible than in many other states — the OIR permits longer terms, medical underwriting, and benefit caps that are restricted or banned elsewhere. States such as California, New York, and New Jersey ban short-term plans entirely; Florida allows 364-day initial terms and full 36-month duration through renewals. The National Association of Insurance Commissioners (NAIC) tracks these rules state by state, and Florida ranks among the most permissive nationwide:

| Regulation | Florida Rule |

|---|---|

| Maximum initial term | Up to 364 days |

| Maximum total duration | Up to 36 months with renewals |

| Medical underwriting | Permitted |

| Pre-existing exclusions | Permitted |

| Benefit caps | Permitted (annual and lifetime) |

Frequently Asked Questions About Short-Term Health Insurance in Florida

These temporary plans cover gaps between jobs, missed enrollment windows, and pre-Medicare transitions — but with 4.7 million Floridians enrolled in marketplace plans for 2025, most residents have ACA options worth comparing first. The questions below address the most common concerns Florida residents have about eligibility, cost, and coverage for temporary health plans.

Will short-term insurance cover pre-existing conditions?

No. Any condition diagnosed or treated before enrollment is excluded. This includes chronic diseases, mental health conditions, and ongoing health issues. The ACA marketplace is the only option that guarantees coverage regardless of medical history.

Is short-term actually cheaper than ACA marketplace plans?

It depends on income. In 2026, with enhanced premium tax credits expired, ACA after-subsidy costs have roughly doubled compared to 2025. Florida residents with income under ~$62,600 (400% FPL) still qualify for subsidies but receive less help than before. For higher earners who no longer qualify, unsubsidized ACA premiums can exceed $500–$650/month — making short-term plans significantly cheaper for healthy individuals needing temporary coverage.

Can I be denied short-term coverage in Florida?

Yes. Short-term plans use medical underwriting. Recent hospitalizations, chronic conditions, or certain medications can result in denial or exclusions for specific conditions.

Does short-term count as minimum essential coverage?

No. These temporary plans do not qualify as minimum essential coverage under the Affordable Care Act. Some employers and government programs may not accept it as proof of insurance.

What happens if I get sick during short-term coverage?

New conditions that develop during the policy term are generally covered, subject to plan limits and benefit caps. However, once the plan ends, that condition becomes “pre-existing” for any subsequent short-term policy and would be excluded.

How long can I keep short-term coverage in Florida?

Initial terms last up to 364 days. With renewals, total coverage can extend to 36 months. However, each renewal may trigger new underwriting, and conditions that developed during the prior term can be excluded.

Florida Health Insurance Resources

Complete guide to all Florida coverage options for 2026.

Best Health Insurance in FloridaTop carriers ranked and compared for the Florida marketplace.

Affordable Florida Health InsuranceBudget-friendly options, subsidy calculator, and savings strategies.

Private Medical Insurance FloridaPrivate options outside the ACA marketplace in Florida.

Florida Health Insurance MarketplaceHealthCare.gov enrollment, Open Enrollment dates, and 16-carrier lineup.

Florida PPO Health InsurancePPO options for broader provider access statewide.

Small Business Health Insurance FloridaGroup plans, ICHRA, and level-funded options for Florida employers.

Blue Cross Blue Shield of FloridaFlorida’s largest health insurance carrier reviewed.

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required.

Find the Right Coverage for Your Situation

Florida short-term plans run $150–$300/month; unsubsidized ACA plans average $500–$650/month after the 31.5% 2026 rate increase. For residents above $62,600 income, the gap is significant. Compare zip code and income to find which fits.

Compare All Options Call 888-215-4045Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Florida residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.