Hawaii Health Insurance: 2026 Guide to Plans, Costs and Coverage

Hawaii has the lowest uninsured rate of any state in the nation — approximately 4% — roughly one-quarter the national average. That figure traces directly to a 1974 state law requiring employers to provide health coverage, making the Hawaii health insurance market fundamentally different from every other state. Whether coverage comes through an employer, the federal marketplace, or a Medicaid program called Med-QUEST, most Hawaii residents have a clear path to coverage. This guide covers every Hawaii health insurance option available for 2026.

What brings you here today?

Why Hawaii Has the Lowest Uninsured Rate in the United States

Hawaii’s ~4% uninsured rate — the lowest in the country — is driven by the Prepaid Health Care Act of 1974, a state law requiring employers to provide health coverage to employees working 20 or more hours per week. This mandate predates the Affordable Care Act by 36 years and covers the majority of Hawaii’s working population. Combined with Medicaid expansion through Med-QUEST, very few Hawaii residents fall through the coverage gap.

The Hawaii Prepaid Health Care Act (PHCA) is unlike any law in the other 49 states. Passed in 1974 during a period of state-level health reform, it requires employers to pay at least 50% of the premium for employees who work 20 or more hours weekly — a threshold stricter than the ACA’s 30-hour federal standard. The law was grandfathered when the ACA passed in 2010, meaning Hawaii is exempt from the ACA’s employer shared responsibility provisions but maintains its own, older mandate with broader part-time coverage reach.

The PHCA covers the majority of Hawaii’s employed population — including part-time workers who meet the 20-hour threshold. According to the U.S. Census Bureau’s health insurance reports, Hawaii health insurance coverage rates have consistently ranked first or second best nationally for over a decade, a direct result of the PHCA’s breadth. For the small share of residents without employer coverage — the self-employed, those working fewer than 20 hours, and those between jobs — the federal marketplace and Med-QUEST fill the remaining gap. Employers navigating PHCA obligations, group plan options, and local carriers like UHA and HMAA can find a full breakdown in the Hawaii small business health insurance guide.

How Health Insurance Works in Hawaii

Most Hawaii residents receive health coverage through their employer under the Prepaid Health Care Act. Those without employer coverage can access the federal marketplace at HealthCare.gov, qualify for Med-QUEST (Hawaii’s Medicaid program), or purchase off-exchange plans directly from carriers like HMSA. Hawaii uses HealthCare.gov after the state’s own exchange, Hawaii Health Connector, shut down in 2015.

Hawaii’s health insurance market operates in three distinct tiers. The largest is the employer market, where the PHCA requires most working residents to receive coverage through their job. The second tier is Med-QUEST, Hawaii’s Medicaid program for residents earning up to 138% of the Federal Poverty Level — approximately $20,800 for a single adult in 2026. The third, smallest tier is the individual market, which includes both on-exchange plans purchased through HealthCare.gov and off-exchange plans purchased directly from carriers.

Hawaii’s individual marketplace is notably small compared to other states. With the PHCA covering most employed residents and Med-QUEST covering low-income residents, only approximately 25,000–30,000 Hawaii residents purchase marketplace plans — a small fraction of the state’s 1.4 million population. This context matters when evaluating carrier options and plan availability: Hawaii’s individual market is supplemental by design, not the primary coverage pathway. For enrollment dates, subsidy eligibility, and plan comparison tools, see the Hawaii health insurance marketplace guide.

Hawaii Health Connector history

Hawaii launched a state-based exchange in 2013 but it shut down in 2015 after exhausting federal grants and facing enrollment shortfalls. Hawaii now uses HealthCare.gov — the federal marketplace — for ACA individual and family plan enrollment. Open Enrollment for 2026 ran November 1, 2025 through January 15, 2026.

Hawaii Health Insurance Carriers: HMSA, Kaiser, and Island Options

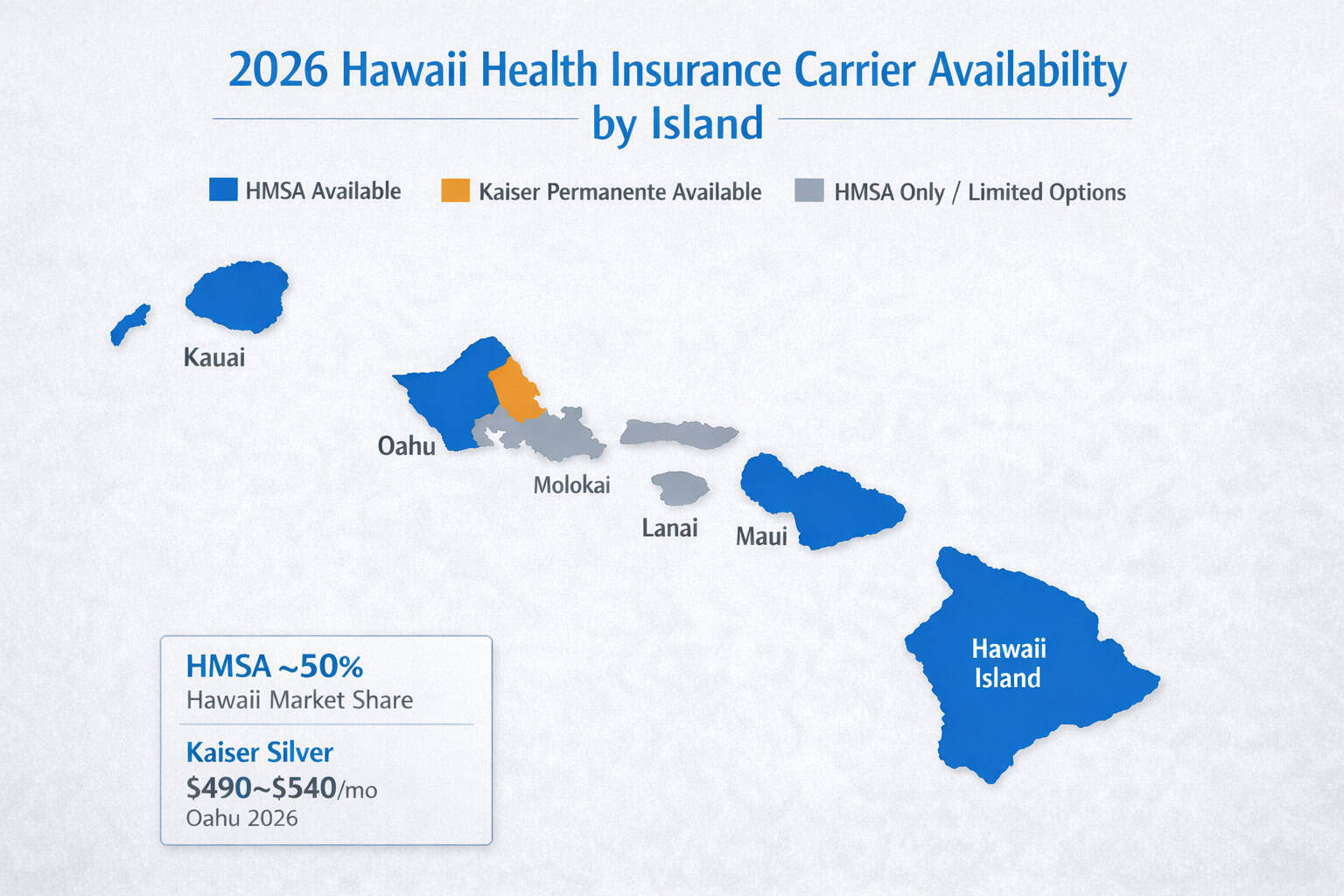

Hawaii’s individual insurance market is dominated by two carriers: HMSA (Hawaii Medical Service Association), a nonprofit BCBS affiliate founded in 1938 that serves all six major islands and holds roughly 50% of the market, and Kaiser Permanente Hawaii, an HMO-only carrier primarily serving Oahu. Carrier availability varies significantly by island — residents of Maui, Hawaii Island, and Kauai have fewer options than those on Oahu.

HMSA — Hawaii Medical Service Association

- BCBS affiliate — largest carrier in Hawaii since 1938

- Nonprofit; serves all major islands

- Offers PPO and HMO plans on and off exchange

- BlueCard PPO network: national coverage for mainland travel

- Off-exchange HMSA PPO available direct for non-subsidy-eligible residents

Kaiser Permanente Hawaii

- Integrated model — insurance and medical facilities combined

- Primarily Oahu; limited neighbor island presence

- No PPO option — must use Kaiser network

- Competitive premiums; high quality ratings

- Best suited to Oahu residents comfortable with coordinated care

Other Hawaii Carriers

- AlohaCare: Med-QUEST managed care; Medicaid population

- Ohana Health Plan: Med-QUEST managed care

- UHA (University Health Alliance): Employer/group plans

- HMAA: Hawaii Management Alliance Association — employer plans

Island geography is the defining factor in Hawaii’s carrier market. Oahu residents have access to both HMSA and Kaiser on the exchange, plus off-exchange options. Residents of Maui, Hawaii Island, and Kauai primarily rely on HMSA — Kaiser’s integrated facility network is concentrated on Oahu and does not extend to neighbor islands. Molokai and Lanai have extremely limited carrier availability, making HMSA the practical default for most residents on those two islands. Across all six major islands, HMSA is the only carrier with a statewide presence.

Individual and Marketplace Plans in Hawaii

Hawaii residents without employer coverage can access the ACA marketplace at HealthCare.gov, where HMSA and Kaiser offer Bronze, Silver, Gold, and Platinum plans. Enhanced premium tax credits that boosted subsidies from 2021 through 2025 expired on December 31, 2025, meaning many marketplace enrollees face higher net premiums in 2026. Residents earning up to 138% FPL ($20,800 for a single adult) may qualify for Med-QUEST at no cost.

The four income pathways for Hawaii residents without employer coverage follow a clear progression — shaped by PHCA coverage gaps, Med-QUEST income thresholds, and HMSA’s position as the only carrier serving all islands:

Med-QUEST (Medicaid)

For residents earning up to 138% FPL (~$20,800 single, ~$43,100 for a family of four in 2026). Hawaii is a Medicaid expansion state. No monthly premium. Managed through AlohaCare, Ohana Health Plan, and other MCOs.

Subsidized Marketplace Plans

For residents earning 138%–400% FPL. Premium tax credits reduce monthly costs significantly. Available through HealthCare.gov. Enhanced credits that reduced costs 2021–2025 expired December 31, 2025 — 2026 premiums are higher for many enrollees.

Unsubsidized Marketplace Plans

For residents earning above 400% FPL (~$62,400 single). Full premium applies. On-exchange plans still offer value through standardized coverage and network access. HMSA and Kaiser both available on exchange for Oahu residents.

Off-Exchange HMSA Plans — PPO

For residents above subsidy thresholds or who prefer PPO flexibility. HMSA offers PPO plans directly without going through HealthCare.gov. Access to BlueCard national network — valuable for inter-island travelers and residents who visit the mainland regularly.

Special Enrollment Periods remain available year-round for qualifying life events — including loss of employer coverage, marriage, birth of a child, and relocation to a new island. According to HealthCare.gov’s Special Enrollment guidelines, most qualifying events trigger a 60-day enrollment window. For Hawaii residents who lose employer coverage — a common scenario for those working seasonally or in the state’s large tourism industry — SEP enrollment is the primary on-ramp to marketplace coverage outside open enrollment. Self-employed residents and those between jobs can explore off-exchange and COBRA alternatives in the individual health insurance guide for Hawaii.

How Much Does Health Insurance Cost in Hawaii?

Before subsidies, a 40-year-old Hawaii resident can expect to pay approximately $380–$460 per month for a Bronze plan, $490–$600 for Silver, and $600–$730 for Gold through the marketplace in 2026. Hawaii’s island geography and small risk pool contribute to premiums that run higher than many mainland states. After premium tax credits, income-qualifying enrollees can reduce those costs substantially.

| Metal Tier | Avg. Monthly Premium (Age 40) | Deductible (Approx.) | Out-of-Pocket Max |

|---|---|---|---|

| Bronze | $380–$460/month | $6,500–$9,100 | $9,100 |

| Silver | $490–$600/month | $3,500–$6,000 | $9,100 |

| Gold | $600–$730/month | $1,000–$3,000 | $8,700 |

| Platinum | $730–$880/month | $0–$500 | $4,000 |

Sample 2026 HMSA and Kaiser plan rates for a 40-year-old non-tobacco user on Oahu. HMSA Silver premiums on Oahu run approximately $490–$540/month before subsidies; neighbor island rates may differ. Sourced from HealthCare.gov Hawaii plan data.

Bronze Plans

~$380–$460/mo

Lowest premiums, highest out-of-pocket costs. Best for healthy residents who primarily want catastrophic protection. Not eligible for cost-sharing reductions.

Silver Plans

~$490–$600/mo

The only tier eligible for cost-sharing reductions (CSRs) for residents earning 138%–250% FPL. CSRs can reduce a Silver plan’s deductible to under $1,000 for qualifying incomes — often the best value for subsidy-eligible Hawaii residents.

Gold Plans

~$600–$730/mo

Higher premiums, lower out-of-pocket costs. Better value for frequent doctor visits, ongoing prescriptions, or planned procedures — especially for Hawaii residents with predictable, ongoing care needs.

Real Scenario: Honolulu Resident, Age 38, $42,000 Income

A 38-year-old freelance graphic designer living in Honolulu earning $42,000 annually (approximately 270% FPL) qualifies for premium tax credits under 2026 income thresholds. Before credits, a Silver HMSA plan might run $520/month. After applying premium tax credits, the estimated monthly cost drops to approximately $195–$240/month — depending on plan selection and county. Silver plans at this income level also carry cost-sharing reductions that lower the deductible significantly below the standard Silver tier.

For a deeper look at subsidy calculations, Med-QUEST eligibility thresholds, and strategies for lowering out-of-pocket costs across all islands, see the affordable health insurance guide for Hawaii.

Compare Hawaii Health Insurance Plans for 2026

HMSA and Kaiser offer 2026 plans across Bronze, Silver, Gold, and Platinum tiers on HealthCare.gov. Residents earning up to $20,800 (single) may qualify for Med-QUEST at no cost. Enter your ZIP code to see island-specific options and check subsidy eligibility.

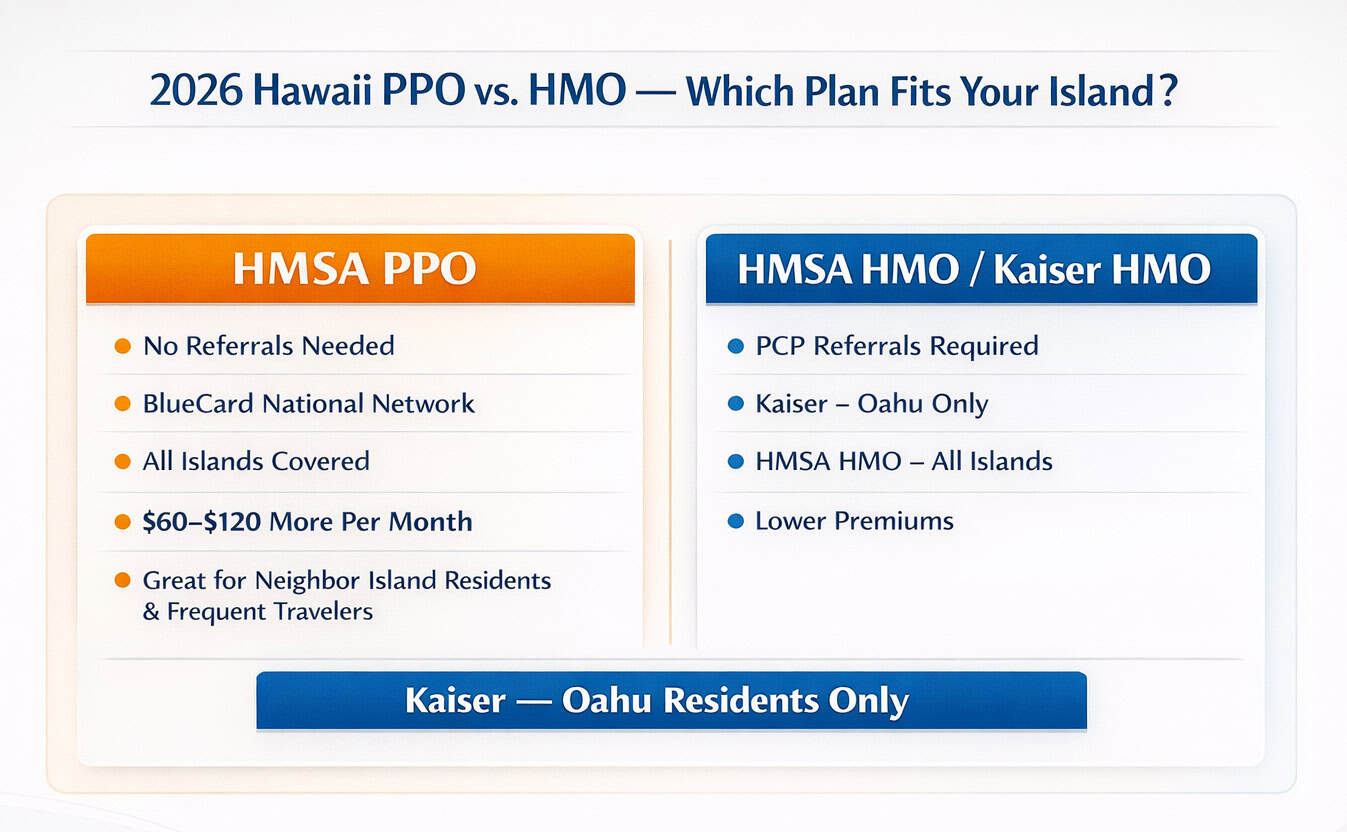

Plan Types: PPO vs. HMO in Hawaii

Hawaii’s individual market offers two primary plan types: HMSA’s PPO plans, which allow residents to see any doctor in HMSA’s statewide and national BlueCard network without referrals, and HMO plans from both HMSA and Kaiser Permanente, which require care coordination through a primary care doctor. For Hawaii residents who travel frequently between islands or to the mainland, the HMSA PPO’s national BlueCard network provides significant practical advantages.

The HMSA vs. Kaiser decision in Hawaii comes down to three practical factors: island of residence, travel patterns, and preferred level of care coordination. Kaiser is only a realistic option for Oahu residents given its integrated facility network on that island; Maui, Hawaii Island, Kauai, Molokai, and Lanai residents are effectively choosing between HMSA HMO and HMSA PPO as their only two carrier options.

HMSA PPO Plans

- See any HMSA network provider without a referral

- BlueCard PPO: national network access for mainland travel

- Available on all major islands through HMSA’s statewide network

- Off-exchange HMSA PPO available for non-subsidy-eligible residents

- Higher premiums than HMO plans — typically 15–25% more per month

HMO Plans

- Requires a primary care physician who coordinates referrals

- Lower premiums than PPO — typically $60–$120/month less

- Kaiser HMO: primarily Oahu; integrated facilities

- HMSA HMO: available on all islands through HMSA network

- Limited or no coverage outside Hawaii without emergency exception

For Oahu residents with stable healthcare needs who rarely travel to the mainland, an HMO — either Kaiser or HMSA — often delivers better value. For neighbor island residents, self-employed professionals who travel regularly, or anyone who sees specialists on a different island, the HMSA PPO’s flexibility and BlueCard national network justify the premium difference. A licensed agent can compare specific 2026 HMSA PPO and HMO plan costs by island to identify the lowest total cost option for a given situation. See the full Hawaii carrier comparison for a side-by-side breakdown of HMSA PPO vs. Kaiser HMO for 2026.

Coverage for Families in Hawaii

Families in Hawaii access coverage through the same three pathways as individuals — employer coverage under the PHCA, Med-QUEST for lower-income households, and marketplace or off-exchange plans for those above Medicaid thresholds. A family of four earning up to approximately $43,100 may qualify for Med-QUEST. Families above that threshold but below $104,800 (400% FPL for a family of four) qualify for subsidized marketplace plans.

Family coverage in Hawaii carries some unique considerations. Children who age off a parent’s employer plan at 26 — a common transition — may need to navigate the individual market for the first time. Given Hawaii’s small marketplace and HMSA’s dominant position, most families end up comparing HMSA plans at different metal tiers rather than switching between carriers.

For families with children, the Children’s Health Insurance Program (CHIP) covers children in households earning too much for Medicaid but still within qualifying ranges. In Hawaii, CHIP is administered through the Med-QUEST program and covers children in families earning up to 312% FPL. The Hawaii Med-QUEST Division manages both Medicaid and CHIP enrollment for the state.

Best For: Families Needing Maximum Flexibility

HMSA PPO plan — off-exchange or on-exchange depending on subsidy eligibility. Allows specialist visits and inter-island care without referrals. BlueCard network covers mainland care for families who travel.

Best For: Families Prioritizing Lower Premiums

HMSA HMO or Kaiser HMO (Oahu only). Requires PCP coordination but delivers savings of $60–$120/month per adult compared to PPO. Well-suited to families with predictable, routine care needs.

Best For: Low-Income Families

Med-QUEST covers families earning up to 138% FPL at no premium cost. CHIP covers children in families up to 312% FPL. Apply through Med-QUEST Division or HealthCare.gov.

Best For: Families with Subsidy Eligibility

Silver marketplace plan through HealthCare.gov. Cost-sharing reductions (138%–250% FPL) can reduce deductibles dramatically. Silver is often the best value tier for subsidy-eligible families in Hawaii.

Frequently Asked Questions About Hawaii Health Insurance

The following questions address the most common concerns Hawaii residents have about health insurance coverage, enrollment, costs, and plan options for the 2026 plan year.

What is the Hawaii Prepaid Health Care Act?

The Hawaii Prepaid Health Care Act (PHCA) is a 1974 state law requiring employers to provide health insurance to employees who work 20 or more hours per week. Employers must contribute at least 50% of the premium cost. The PHCA predates the Affordable Care Act by 36 years and is the primary reason Hawaii has the lowest uninsured rate in the country — approximately 4%. Hawaii is grandfathered from the ACA’s employer mandate, but the PHCA’s 20-hour threshold is stricter in some respects than the ACA’s 30-hour threshold.

Does Hawaii have its own health insurance exchange?

No. Hawaii launched its own state exchange — the Hawaii Health Connector — in 2013, but it shut down in 2015 after exhausting federal startup grants and failing to achieve sustainable enrollment. Hawaii health insurance shoppers now use the federal marketplace at HealthCare.gov for ACA individual and family plan enrollment. Hawaii residents can shop, compare, and enroll in HMSA and Kaiser marketplace plans through HealthCare.gov during Open Enrollment and Special Enrollment Periods. See the full Hawaii marketplace guide for enrollment dates and subsidy details.

What is Med-QUEST?

Med-QUEST is Hawaii’s Medicaid program. It provides health coverage at no premium cost to Hawaii residents earning up to 138% of the Federal Poverty Level — approximately $20,800 for a single adult in 2026. Hawaii is a Medicaid expansion state, meaning adults without children can also qualify based on income alone. Med-QUEST is managed through private managed care organizations including AlohaCare and Ohana Health Plan. Applications can be submitted through the Hawaii Med-QUEST Division directly or through HealthCare.gov.

Which health insurance carriers are available in Hawaii?

The two primary individual market carriers in Hawaii are HMSA (Hawaii Medical Service Association) — a BCBS affiliate that serves all islands — and Kaiser Permanente Hawaii, an HMO-only carrier primarily serving Oahu. HMSA holds roughly 50% of the market and offers both PPO and HMO plans on and off exchange. For employer and group coverage, UHA (University Health Alliance) and HMAA (Hawaii Management Alliance Association) are also significant local carriers. Carrier availability varies by island — Oahu has the widest selection.

Do I need health insurance in Hawaii if I have employer coverage?

If an employer provides coverage that meets the PHCA’s minimum requirements, that satisfies the coverage requirement. Hawaii does not have a state individual mandate requiring residents to carry coverage — there is no state-level penalty for being uninsured as of 2026 (the federal individual mandate penalty was eliminated in 2019). However, PHCA-covered employees cannot opt out of employer coverage if their employer offers it.

Can I get a PPO plan in Hawaii?

Yes. HMSA offers PPO plans both on the HealthCare.gov marketplace and off-exchange directly from HMSA. The HMSA PPO provides access to HMSA’s statewide network on all major islands, plus the BlueCard PPO national network for coverage on the mainland — useful for Hawaii residents who travel or have family on the mainland. Kaiser Permanente is HMO-only and does not offer a PPO option. For a full comparison of PPO and HMO plans available in Hawaii for 2026, see the Hawaii carrier comparison guide.

What happened to the enhanced ACA subsidies in 2026?

The enhanced premium tax credits introduced by the American Rescue Plan Act and extended through the Inflation Reduction Act expired on December 31, 2025. These enhanced credits had significantly reduced marketplace premiums for many Hawaii residents from 2021 through 2025. For 2026, standard ACA subsidy rules apply — residents earning between 100% and 400% FPL qualify for premium tax credits, but the additional boosts that made plans more affordable at higher incomes are no longer available. Hawaii residents who relied on enhanced credits may see notable premium increases for 2026.

Hawaii Health Insurance Guides

Compare HMSA PPO vs. Kaiser HMO — island-by-island carrier availability for 2026

Affordable Health Insurance in HawaiiMed-QUEST eligibility, subsidy calculator, and lowest-cost plan options by island

Small Business Health Insurance in HawaiiPHCA employer obligations, group plans, UHA and HMAA — Hawaii’s unique employer market

Individual Health Insurance in HawaiiCoverage for self-employed, part-time workers, and those between jobs in Hawaii

Hawaii Health Insurance MarketplaceHow HealthCare.gov works in Hawaii, open enrollment dates, and subsidy eligibility

PPO Health Insurance PlansCompare PPO plans nationwide — provider flexibility, BlueCard network, and no-referral coverage

Find the Right Hawaii Health Insurance Plan

From Med-QUEST at $0 premium for incomes up to $20,800, to subsidized HMSA Silver plans through HealthCare.gov, to off-exchange HMSA PPO for higher-income residents — Hawaii has a coverage pathway for every situation. Get a free quote to compare your 2026 options by island.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Hawaii residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.