Self-Employed Health Insurance in Texas (2025 Guide)

Whether you’re a freelancer, contractor, gig worker, or sole proprietor, this guide breaks down your best health insurance options in Texas. Learn how to compare plans, lower your costs, and get the coverage you need.

What Are Your Health Insurance Options If You’re Self-Employed in Texas?

As a self-employed Texan, you can choose from several coverage options depending on your income, health needs, and preferred provider access:

- PPO Plans: Greater provider flexibility, including out-of-network care. Often preferred by consultants, digital professionals, and those traveling frequently.

- HSA-Compatible High Deductible Plans: Ideal for those who want lower monthly premiums and tax savings.

- ACA Marketplace Plans: Subsidy-eligible plans through HealthCare.gov with Bronze, Silver, Gold, and Platinum tiers.

- Short-Term Plans: Temporary coverage, often used between jobs or before major life events. Note: These plans don’t include ACA protections.

Some Texans also explore direct primary care memberships or healthcare cost sharing ministries, though these are not considered comprehensive health insurance under the ACA.

It’s important to consider your network preferences, medication needs, and financial risk tolerance when choosing a plan. PPOs often work best for people who want the freedom to see out-of-network providers without referrals.

Why Many Self-Employed Texans Choose PPO Plans

PPO (Preferred Provider Organization) plans remain a top choice for self-employed Texans because of their flexibility. Unlike HMOs, PPOs allow you to:

- See specialists without needing a referral

- Use out-of-network doctors (nationwide coverage in many cases)

- Choose from broad provider networks ideal for remote workers and consultants

Many freelancers and gig workers value this freedom, especially when their income allows for a plan with higher premiums and lower restrictions. PPOs are also a strong fit for Texans who travel frequently or need access to specific specialists.

Learn more about PPO plans in Texas »

How Much Does Self-Employed Health Insurance Cost in Texas?

Premiums can vary based on age, ZIP code, tobacco use, and the type of plan you choose. Below are average monthly premiums for a 40-year-old self-employed Texan in Dallas:

- Bronze PPO Plan: $410–$460/month

- Silver PPO Plan: $480–$530/month

- High Deductible HSA Plan: $330–$390/month

Tax credits may significantly reduce these premiums depending on your income. See the next section for details.

Some carriers in Texas also offer plan customization tools that allow you to adjust deductibles, copays, and specialist access levels to better fit your budget. Speak with a licensed broker to compare those side-by-side.

Premiums are only part of the picture. You’ll also want to compare total out-of-pocket exposure, including deductibles, coinsurance, and out-of-pocket maximums, especially if you expect to use care regularly throughout the year.

Can Self-Employed Texans Get Health Insurance Subsidies?

Yes. If you buy a plan through the ACA Marketplace, you may qualify for subsidies that lower your premium and out-of-pocket costs. Your eligibility depends on your projected income for the year, not last year’s tax return.

- Premium Tax Credits to reduce monthly premiums

- Cost-Sharing Reductions (CSRs) if you choose a Silver plan and meet certain income thresholds

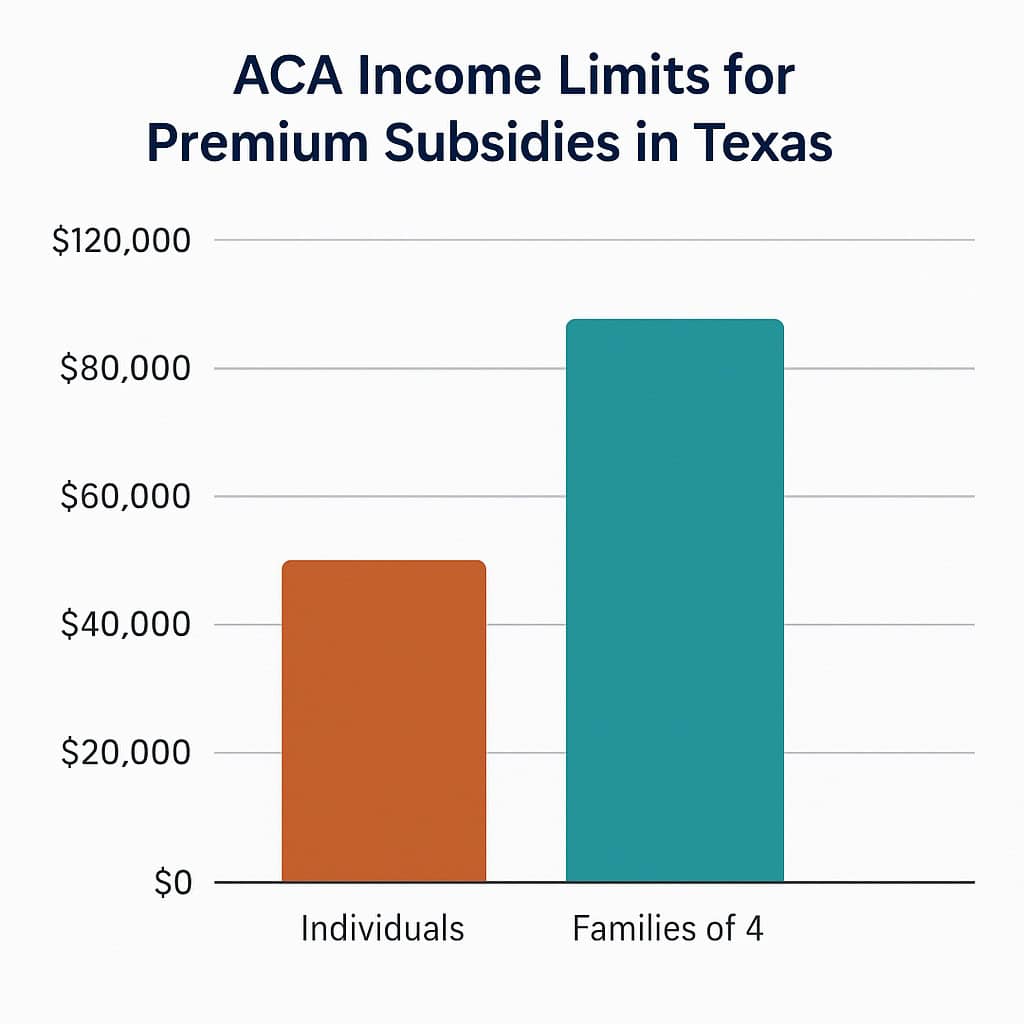

For 2025, a single self-employed individual in Texas can qualify for subsidies with an income up to approximately $58,320. For a family of four, the limit is around $120,000. Your household size and age also affect your subsidy level.

You can apply for subsidies during open enrollment or during a qualifying life event using HealthCare.gov or a licensed broker.

Are Health Insurance Premiums Tax Deductible for the Self-Employed?

Yes. If you report self-employment income, you can typically deduct 100% of your health insurance premiums, including premiums for your spouse and dependents, directly from your taxable income. This applies whether you itemize or not.

This deduction is especially valuable when combined with an HSA-compatible plan, allowing you to reduce both your taxable income and your healthcare spending. Keep records of your premiums and HSA contributions for tax filing purposes.

Note that this deduction is claimed on IRS Form 1040, not Schedule C. You must also meet criteria regarding income levels and employer-sponsored plan eligibility.

Real Example: Freelance Designer in Austin

Michelle, a 35-year-old freelance web designer in Austin, chose an HSA-compatible PPO plan with a $5,000 deductible and a $350/month premium. With premium tax credits, she reduced her monthly cost to $190 and contributes $2,000 annually to her HSA for additional savings.

She also uses telehealth services for routine care, which her plan covers with a $15 copay. For Michelle, flexibility and predictable costs matter most, and this plan helps her manage both.

Her experience underscores the value of working with a broker, someone who helped her compare multiple plans based on doctor network, hospital access, and anticipated out-of-pocket costs.

Frequently Asked Questions

Can I write off my health insurance as a freelancer in Texas?

Yes. If you report self-employment income and are not eligible for an employer plan, you can deduct your premiums from your taxable income.

Should I choose a PPO or HMO if I’m self-employed?

PPOs offer more flexibility, especially if you travel or see specialists. HMOs may be cheaper but require referrals and in-network care.

Is it better to use the Marketplace or a private broker?

Using a broker gives you access to both Marketplace and off-exchange plans. They can help compare all options and ensure you’re getting subsidies if eligible.

Can I qualify for coverage year-round or only during open enrollment?

If you’re self-employed and just starting out or leaving a job, you may qualify for a special enrollment period. Otherwise, the annual open enrollment window applies.

Related Texas Guides

- Texas Health Insurance Overview

- Texas PPO Health Insurance Plans

- Short-Term Health Insurance in Texas

- National Guide: Self-Employed Health Insurance

Need Help Choosing a Plan?

Sorting through health insurance options as a self-employed professional can be time-consuming, but you don’t have to do it alone. Our licensed brokers are here to guide you through every step, from comparing PPO networks to identifying HSA-compatible options that match your budget and tax goals.

Click below to compare your personalized quotes or speak directly with a licensed broker who understands the Texas market.