Self-Employed Health Insurance Texas 2026: 1099 Guide

Self-employed health insurance Texas options for 2026 cover four primary paths: HealthCare.gov marketplace plans with Advanced Premium Tax Credit subsidies for 1099 contractors below 400% of federal poverty level, off-exchange PPO plans for higher-income self-employed Texans, HSA-eligible HDHP plans for the strongest tax-deduction stack, and short-term limited-duration coverage for bridge periods between projects. Self-employed Texans can deduct 100% of qualifying premiums on Schedule 1 of Form 1040 — making coverage roughly 22–32% cheaper net-of-tax for most freelancers and sole proprietors.

What brings you here today?

Self-Employed Health Insurance Options in Texas

Self-employed Texans have four primary coverage paths in 2026: HealthCare.gov marketplace plans for 1099 contractors below 400% of federal poverty level (the default for most), off-exchange directly from carriers for PPO plans HealthCare.gov doesn’t sell in Texas, HSA-eligible HDHP plans for the strongest combined tax benefit, and short-term limited-duration coverage for project gaps. Single-member LLCs and freelancers with employees may also qualify for SHOP small-group plans.

The Texas self-employed coverage market is shaped by two structural facts that don’t apply to W-2 employees. First, Texas uses HealthCare.gov rather than a state-based exchange — meaning 1099 contractors in Harris County, Travis County, and Bexar County all apply through the federal portal, not a Texas-run system. Second, HealthCare.gov in Texas certifies only HMO and EPO plans from carriers like Ambetter, Molina, and BCBSTX for individual coverage — no individual PPO products — so self-employed Texans who want out-of-network coverage or no-referral specialist access at Memorial Hermann or MD Anderson typically go off-exchange.

The economic case for self-employed health insurance Texas coverage is also distinct from W-2 employment. A 1099 contractor pays the full premium with no employer contribution, but recovers 100% of qualifying premiums as an above-the-line deduction on Schedule 1 of IRS Form 1040 — reducing both federal income tax and the self-employment tax base. For a self-employed Texan in the 22% federal bracket paying 15.3% self-employment tax, the deduction can cut effective premium cost by 22–32%. This makes coverage choices and projected business income reporting decisions worth careful attention every November during open enrollment.

The four-path self employed health insurance Texas decision

Most self-employed Texans pick between HealthCare.gov marketplace (subsidized below 400% of federal poverty level), off-exchange PPO (above subsidy ceilings or specialist-intensive care), HSA-eligible HDHP (maximum tax stacking), and short-term limited-duration (bridge coverage only). The right self employed health insurance Texas choice depends on projected Schedule C income, provider preferences, and how comfortable the household is with deductible exposure. A licensed Texas broker can model all four self employed health insurance Texas paths against your specific income projection in a 30-minute call.

The Self-Employment Health Insurance Tax Deduction

Self-employed Texans deduct 100% of qualifying health, dental, and long-term care insurance premiums for themselves, spouses, and dependents as an above-the-line deduction on Schedule 1 of IRS Form 1040 (line 17 for 2026). The deduction reduces Adjusted Gross Income (AGI), lowering federal income tax and the self-employment tax base. Eligibility requires net self-employment earnings from a Schedule C business, partnership, or S-corporation — and the deduction is capped at net business income for the year.

The self-employment health insurance deduction is one of the most valuable tax breaks available to Texas 1099 contractors and sole proprietors. Unlike W-2 employees who pay health insurance with pre-tax payroll deductions, self-employed Texans pay BCBSTX, Ambetter, or Cigna premiums with after-tax dollars — then claim the deduction on their federal return. The deduction is above the line, reducing AGI before the standard deduction is applied. For a self-employed Texan in Houston earning $65,000 net Schedule C income, the deduction on a $7,200 annual premium saves approximately $2,664 in combined federal and self-employment tax — effectively reducing the net premium cost from $600/month to roughly $378/month.

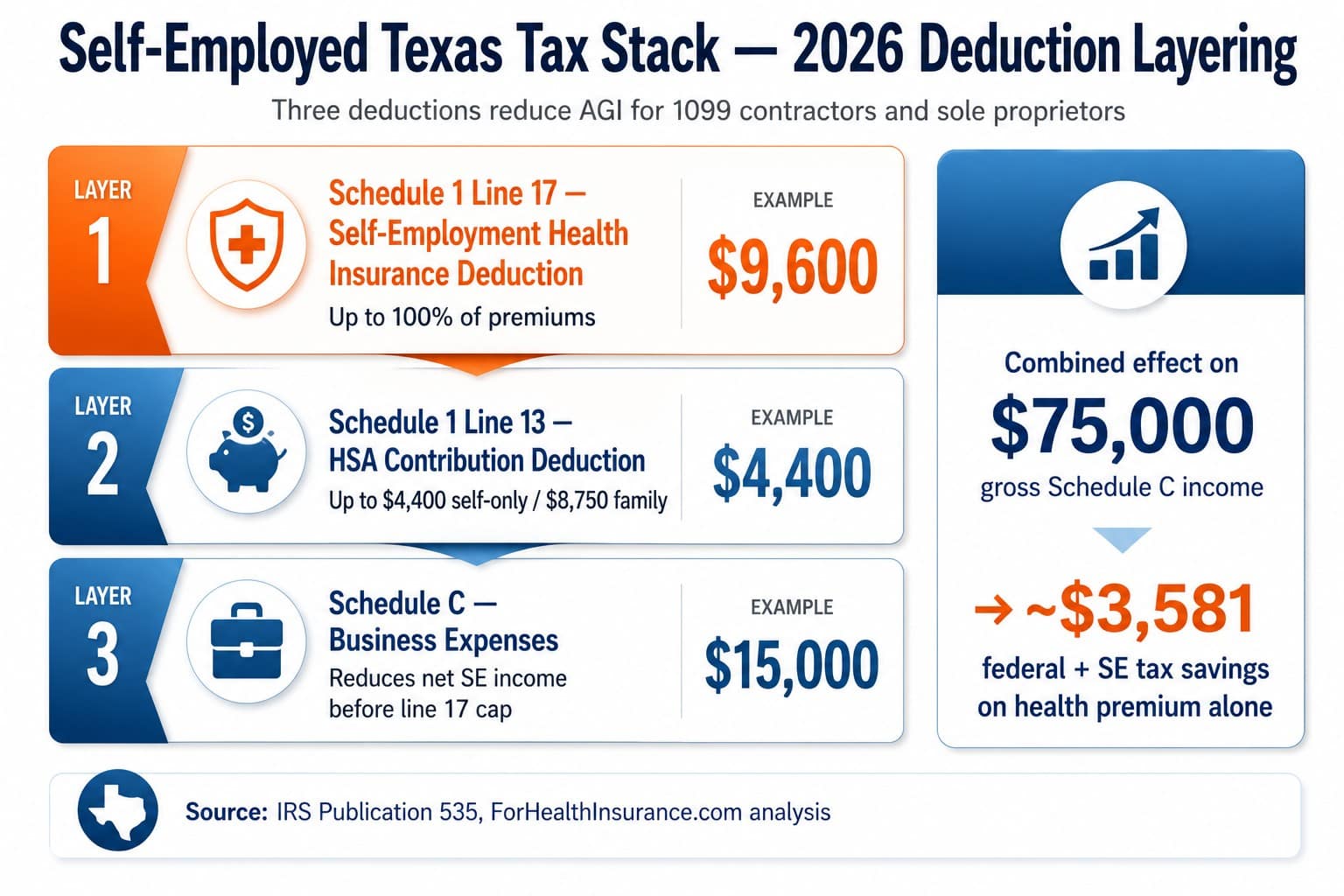

For a self-employed Texan earning $75,000 net from a Schedule C business and paying $9,600 annually in health insurance premiums, the deduction reduces AGI by $9,600 — saving roughly $2,112 in federal income tax (at the 22% marginal bracket) plus reducing the self-employment tax base, which adds another $1,469 in savings on the 15.3% combined rate. Total tax savings on $9,600 of premiums: approximately $3,581, making the effective net-of-tax premium cost closer to $6,019. Texans should consult IRS Publication 535 for the official rules and limitations.

| Self-Employed Texas Scenario | Annual Premium | Estimated Tax Savings | Net-of-Tax Cost |

|---|---|---|---|

| 1099 contractor, $50,000 net, single, BCBSTX Silver | $7,200 | $2,160 (30%) | $5,040 |

| Freelancer, $75,000 net, single, Cigna PPO off-exchange | $9,600 | $3,581 (37%) | $6,019 |

| Sole proprietor, $100,000 net, family of 4, BCBSTX Gold | $22,800 | $8,436 (37%) | $14,364 |

| Single-member LLC, $150,000 net, single, UHC PPO + HSA | $11,400 | $4,218 (37%) | $7,182 |

| S-corp owner, $200,000 net, family of 4, off-exchange PPO | $26,400 | $9,768 (37%) | $16,632 |

Tool: ChatGPT / GPT Image

Layout type: Tax deduction stack visualization (data visual)

State anchor: Texas — 2026 self-employed tax deduction layering

═══ CONTENT ═══

Title: “Self-Employed Texas Tax Stack — 2026 Deduction Layering”

Subtitle: “Three deductions reduce AGI for 1099 contractors and sole proprietors”

Three stacked cards in a vertical stack showing layered tax savings:

Layer 1 (top): “Schedule 1 Line 17 — Self-Employment Health Insurance Deduction — Up to 100% of premiums” — example $9,600

Layer 2 (middle): “Schedule 1 Line 13 — HSA Contribution Deduction — Up to $4,400 self-only / $8,750 family” — example $4,400

Layer 3 (bottom): “Schedule C — Business Expenses — Reduces net SE income before line 17 cap” — example $15,000

Side panel: “Combined effect on $75,000 gross Schedule C income → ~$3,581 federal + SE tax savings on health premium alone”

Footer: “Source: IRS Publication 535, ForHealthInsurance.com analysis”

═══ DESIGN SYSTEM (PIS) ═══

Soft shadows + bevel lighting + top-left light source + layered cards

Bold title hierarchy + large numerics + consistent spacing

#407297 gradient fills (not flat) + #f87c25 accent on the line 17 layer (the primary deduction)

Card-based + rounded corners (12px) + grid-aligned

Minimal icon indicators

White background, professional editorial feel

═══ HARD RULES ═══

• Exact dimensions: 1200×800px

• All text spelled correctly — Schedule 1, Schedule C, IRS Publication 535

• Layered stack must visually convey hierarchy — line 17 on top, sized largest

• Avoid: flat grey tables, harsh borders, Canva-style, cheap vector look

HealthCare.gov for Self-Employed Texans

HealthCare.gov is the primary coverage path for most self-employed Texans because business net income after Schedule C deductions usually falls within Advanced Premium Tax Credit (APTC) eligibility ranges — 138%–400% of federal poverty level. The projected MAGI submitted on the marketplace application drives subsidy amount, and self-employed Texans should update HealthCare.gov mid-year whenever projected income changes by more than $5,000 to avoid reconciliation shock on Form 8962 at tax time.

The income projection step is where self-employed Texans most often go wrong. HealthCare.gov asks for projected MAGI for the coverage year — not last year’s tax return. For a self-employed Texan, MAGI starts with Schedule C net income, then adds taxable interest, dividends, capital gains, and other items. A Dallas-Fort Worth freelancer projecting $38,000 net income sits at approximately 252% of the 2026 federal poverty level — qualifying for both APTC subsidies and Cost-Sharing Reductions on a Silver plan from BCBSTX or Ambetter. That same contractor projecting $62,000 — above the $60,240 single-adult subsidy ceiling — shifts entirely to off-exchange options with no APTC available.

For 2026 coverage in Texas, the federal poverty level thresholds are approximately $15,060 (100% FPL, single adult) up to $60,240 (400% FPL, single) — and $31,200 (138% FPL, family of 4) up to $124,800 (400% FPL, family of 4). Buyers of self employed health insurance Texas plans projecting MAGI within those bands qualify for APTC subsidies that reduce monthly premium directly. CSR cost-sharing reductions on Silver-tier plans further lower deductibles and out-of-pocket maximums for households below 250% FPL. The official HealthCare.gov portal is the only legitimate marketplace enrollment channel for Texas — off-exchange enrollment forfeits subsidy eligibility.

Update your income projection mid-year to avoid tax-time surprises

The single biggest tax-time surprise for self-employed Texans is APTC reconciliation on Form 8962. If your actual MAGI exceeds your HealthCare.gov projection by enough to drop you into a higher subsidy tier (or out of subsidy eligibility entirely), the IRS will claw back excess APTC at tax time — potentially several thousand dollars owed. Update your projected income in your HealthCare.gov account whenever quarterly business revenue trends $5,000 or more above your original projection. The portal recalculates APTC in real time and adjusts your monthly subsidy going forward, avoiding the year-end claw-back.

Example: Austin Freelance UX Designer, Age 34

A 34-year-old freelance UX designer in Travis County projects $42,000 in Schedule C net income for 2026 — approximately 279% of the federal poverty level for a single adult. At that income, she qualifies for APTC subsidies on HealthCare.gov. An Ambetter Silver plan before subsidies runs approximately $498/month; after her estimated $362/month APTC credit, her net premium is roughly $136/month. She claims the full $1,632 in annual net premiums as an above-the-line deduction on Schedule 1 of Form 1040, reducing her AGI and saving an additional $490 in federal and self-employment tax at the 22% combined rate — bringing effective annual coverage cost to approximately $1,142 for a Silver plan with CSR-enhanced cost-sharing.

Off-Exchange PPO for Higher-Income Self-Employed Texans

Self employed health insurance Texas buyers projecting MAGI above 400% of federal poverty level lose APTC subsidy eligibility — eliminating the marketplace cost advantage and making off-exchange PPO a competitive comparison. For self employed health insurance Texas buyers above the subsidy ceiling, off-exchange PPO plans from BCBSTX, Cigna, UnitedHealthcare, Aetna, and Humana offer broader networks, out-of-network coverage, and no-referral specialist access — features unavailable on HealthCare.gov HMO and EPO plans in Texas.

The economic logic for self employed health insurance Texas coverage shifts above the 400% FPL ceiling. A self-employed Texan projecting $75,000 net Schedule C income (single adult) is above the $60,240 subsidy ceiling — the 400% FPL cliff reinstated for 2026 — and receives no APTC subsidy on HealthCare.gov. At full price, the gap between marketplace HMO/EPO and off-exchange PPO narrows considerably, often justifying the PPO premium for the network flexibility. At full price, the gap between marketplace HMO/EPO and off-exchange PPO narrows considerably, often justifying the PPO premium for the network and out-of-network flexibility.

For buyers of self employed health insurance Texas coverage considering PPO products, the comprehensive Texas PPO Plans guide covers the five-carrier landscape (BCBSTX, Cigna, Aetna, UnitedHealthcare, Humana), Texas hospital system contracting, premium tier structures, and the 26-rating-area pricing variation. The self-employment health insurance deduction applies to off-exchange premiums identically to marketplace premiums — Schedule 1 line 17 doesn’t distinguish where coverage was purchased, only that it’s qualifying coverage.

Get a Self-Employed Texas Quote

A licensed Texas broker compares HealthCare.gov subsidized plans against off-exchange PPO options for 1099 contractors and sole proprietors — with projected MAGI modeling, Schedule 1 deduction estimates, and provider verification at Memorial Hermann, Houston Methodist, Baylor Scott & White, and Texas Health Resources. Free, no obligation.

HSA-Eligible HDHP: The Self-Employed Tax Stack

Self employed health insurance Texas buyers using HSA-eligible HDHP plans typically receive the strongest combined tax benefit, especially those above marketplace subsidy ceilings. The high-deductible plan carries lower monthly premium than a comparable Silver or Gold plan, and contributions to the linked Health Savings Account are deductible on Schedule 1 separately from the self-employment health insurance deduction. The 2026 HSA contribution limit is $4,400 for self-only coverage and $8,750 for family coverage, with an additional $1,000 catch-up for age 55+.

The HSA mechanism works as a triple-tax-advantaged account: contributions are tax-deductible (above the line), investment growth inside the HSA is tax-free, and qualified medical withdrawals are tax-free. For buyers of self employed health insurance Texas coverage, this stacks against the Schedule 1 line 17 health insurance deduction without offset — the two deductions are separate line items on Schedule 1, so a 1099 contractor can claim both in the same year. A self-employed Texan paying $7,200 in annual premiums on an HSA-eligible HDHP and contributing the full $4,400 to the HSA reduces AGI by $11,600 — saving roughly $4,300 in combined federal and self-employment tax at the 22% bracket.

The trade-off is deductible exposure. An HSA-eligible HDHP in Texas typically carries a $1,700–$3,400 self-only deductible (the 2026 IRS minimum for HSA eligibility is $1,700 self-only / $3,400 family) and an out-of-pocket maximum up to $8,500 self-only / $17,000 family. Self-employed Texans choosing this path should fund the HSA aggressively in good income years to build a buffer against deductible exposure in bad years — the HSA balance rolls over indefinitely and follows the account holder regardless of plan changes or employment status.

Texas Carriers for Self-Employed Coverage

Self-employed Texans choose between two carrier groups depending on coverage path. On HealthCare.gov, Blue Cross Blue Shield of Texas (BCBSTX) leads on statewide network depth, with Ambetter and Oscar Health competing on lower premium. Off-exchange, Cigna, UnitedHealthcare, and BCBSTX dominate the PPO market for self-employed Texans above subsidy ceilings or needing PPO flexibility. The Texas Department of Insurance (TDI) publishes quarterly carrier complaint indices and rate filings.

Blue Cross Blue Shield of Texas (BCBSTX)

HealthCare.gov / StatewideThe most common HealthCare.gov choice for self-employed Texans needing broad statewide access. BCBSTX maintains the deepest network across Memorial Hermann, Houston Methodist, Baylor Scott & White, Texas Health Resources, and HCA Healthcare. Available across all Texas rating areas with Bronze, Silver, and Gold marketplace plans plus off-exchange PPO products for higher-income self-employed.

- HCSC parent / Texas Blues

- Largest marketplace network

- On- and off-exchange products

- BlueCard national reciprocity off-exchange

Ambetter (Centene)

HealthCare.gov / Low premiumAmbetter is a Centene marketplace brand offering lower-premium Bronze and Silver plans on HealthCare.gov — competitive for younger 1099 contractors and freelancers prioritizing low monthly cost. Network depth is narrower than BCBSTX, especially outside Houston and Dallas-Fort Worth metros. Strongest fit for self-employed Texans below 250% FPL who qualify for Cost-Sharing Reductions on Silver plans.

- Centene marketplace brand

- Lowest Bronze/Silver pricing

- Narrower hospital network

- CSR-friendly Silver lineup

Oscar Health

HealthCare.gov / Tech-friendlyOscar Health’s marketplace plans in Texas emphasize digital tools, telehealth, and concierge member services — features that appeal to remote-working 1099 contractors and freelancers comfortable navigating coverage through an app. Available in select Texas metros (Houston, San Antonio, Austin, Dallas-Fort Worth) with Bronze, Silver, and Gold plans. Network is narrower than BCBSTX but typically includes major metro hospital systems.

- Digital-first member experience

- Major Texas metros only

- Telehealth-integrated plans

- Mid-tier marketplace premium

Cigna

Off-exchange / Above subsidyCigna’s Open Access Plus PPO is widely chosen by self-employed Texans above 400% FPL who want PPO flexibility without subsidy. Strong in Houston, Dallas-Fort Worth, Austin, and San Antonio metros, with national reciprocity for 1099 contractors who travel. Premium runs higher than HealthCare.gov plans but covers out-of-network providers and skips PCP referrals for specialists.

- Open Access Plus PPO product

- Above-subsidy income focus

- Strong national reciprocity

- Metro-anchored Texas network

UnitedHealthcare of Texas

Off-exchange / NationalUnitedHealthcare Choice Plus PPO is the preferred off-exchange PPO for self-employed Texans who travel frequently or split time across states. UHC’s national network is broad enough that a Houston-based 1099 consultant working contracts in Atlanta, Denver, or New York stays in-network without switching plans. UHC contracts with most major Texas hospital systems and offers HSA-eligible HDHP variants.

- Choice Plus PPO product

- Strong national network

- HSA-eligible variants available

- Multi-state freelancer fit

Aetna & Humana

Small group / Single-member LLCAetna and Humana primarily serve self-employed Texans through small-group employer channels rather than individual products. A single-member LLC owner who hires even one employee may qualify for SHOP small-group coverage from Aetna or Humana — sometimes with better pricing than individual marketplace alternatives. Texas SHOP eligibility requires 1–50 employees plus the owner, with carrier-specific minimum participation rules.

- Small-group SHOP focus

- 1–50 employee LLCs eligible

- Group rate advantages

- Higher administrative complexity

Frequently Asked Questions

Common questions from self-employed Texans cover the Schedule 1 line 17 deduction rules, where 1099 contractors in Harris County, Travis County, and Tarrant County buy coverage, how to project MAGI on HealthCare.gov using Schedule C net income, whether HSA-eligible HDHP plans from BCBSTX or UnitedHealthcare beat a subsidized Ambetter Silver plan on total cost, and which Texas carriers best serve self-employed buyers above the $60,240 subsidy ceiling in 2026.

Can self-employed Texans deduct health insurance premiums?

Yes. Self-employed Texans can deduct 100% of health, dental, and qualified long-term care insurance premiums for themselves, their spouse, and dependents as an above-the-line deduction on Schedule 1 of IRS Form 1040 (line 17 for tax year 2026). The deduction reduces adjusted gross income (AGI), which in turn lowers federal income tax and self-employment tax base. Eligibility requires net self-employment earnings from a sole proprietorship, single-member LLC, partnership, or S-corporation, and the deduction is capped at your net business income for the year. Self-employed Texans cannot also be eligible for an employer-subsidized plan (through a spouse’s job, for example) during the same month — eligibility is calculated month by month.

Where do self-employed Texans buy health insurance?

Self employed health insurance Texas options include four primary coverage paths: HealthCare.gov for ACA marketplace plans with Advanced Premium Tax Credit subsidies (the default for most self-employed residents below 400% of federal poverty level), off-exchange directly from carriers for PPO plans not sold on the federal exchange in Texas, short-term limited-duration plans for bridge coverage between projects, and SHOP or direct group coverage for single-member LLCs with employees. Most self-employed Texans qualify for HealthCare.gov subsidies because business net income after deductions often falls below subsidy ceilings — the projected MAGI submitted on the marketplace application drives premium tax credit eligibility.

How do I report self-employment income on HealthCare.gov?

HealthCare.gov asks self-employed Texas applicants to project their Modified Adjusted Gross Income (MAGI) for the coverage year — not last year’s income. For a self-employed Texan, this means projecting gross business revenue minus business expenses (the Schedule C net income figure) plus any other taxable income. Many self-employed Texans underestimate income out of caution to maximize subsidies, then face Advanced Premium Tax Credit reconciliation on Form 8962 at tax time if actual income exceeds projection. Update HealthCare.gov mid-year whenever projected income changes by more than $5,000 to avoid reconciliation shock — Texas allows real-time income updates through the federal exchange portal.

Should self-employed Texans use HSA-eligible HDHP plans?

For many self-employed Texans, HSA-eligible HDHP plans deliver the strongest combined tax benefit. An HSA-qualified high-deductible plan typically carries lower monthly premium than a comparable Silver or Gold plan, and contributions to the linked Health Savings Account are deductible on Schedule 1 (separate from the self-employment health insurance deduction). The 2026 HSA contribution limit is $4,400 for self-only coverage and $8,750 for family coverage. Self-employed Texans combining the self-employment health insurance deduction, HSA contribution deduction, and Schedule C business expense deductions can stack three separate tax benefits against gross business income — particularly valuable for 1099 contractors above marketplace subsidy ceilings.

What is the best Texas health insurance carrier for self-employed?

The right carrier for a self-employed Texan depends on coverage path and provider preferences. Blue Cross Blue Shield of Texas (BCBSTX) leads on statewide network depth and is the most common HealthCare.gov choice for self-employed Texans needing access to Memorial Hermann, Houston Methodist, Baylor Scott & White, or Texas Health Resources facilities. Ambetter (Centene) and Oscar Health are competitive on HealthCare.gov for younger 1099 contractors prioritizing lower premium. Cigna and UnitedHealthcare lead off-exchange for self-employed Texans above subsidy ceilings who want PPO flexibility and national reciprocity. Aetna and Humana primarily serve self-employed Texans through small-group channels rather than individual.

Compare 2026 Self-Employed Texas Plans

A licensed Texas broker compares HealthCare.gov subsidized marketplace plans, off-exchange PPO products, and HSA-eligible HDHP options for 1099 contractors, freelancers, and sole proprietors — with projected MAGI modeling, Schedule 1 line 17 deduction estimates, and provider verification across Texas hospital systems. Free, no obligation.

Free self-employed Texas comparison — every coverage path in one call.

Explore Texas Coverage In Depth

Statewide overview of Texas health insurance — marketplace, Medicaid, and off-exchange options compared.

Texas Marketplace EnrollmentHealthCare.gov enrollment guide for Texas — APTC subsidies, open enrollment, and SEPs.

Individual Texas Health InsuranceIndividual plan options — marketplace, off-exchange PPO, and direct carrier enrollment.

Texas PPO PlansOff-exchange PPO options for self-employed Texans above subsidy ceilings — BCBSTX, Cigna, UHC.

Cheap Texas Health InsuranceLowest-cost Texas plans — subsidized Bronze and Silver, CHIP, and affordability by income tier.

Catastrophic Texas Health InsuranceLower-premium high-deductible coverage for self-employed Texans under 30 or with hardship exemptions.

Short-Term Texas Health InsuranceBridge coverage between contracts, post-employment gaps, and project-to-project freelance work.

Private Texas Health InsuranceOff-exchange private coverage for Texans above ACA subsidy thresholds.

Family Texas Health InsuranceFamily coverage for self-employed Texans with spouses and dependents on the same plan.

Texas Retiree Health InsurancePre-Medicare bridge ages 55–64 — TRS-Care, ERS, APTC subsidies, COBRA vs marketplace.

Texas Small Business Health InsuranceGroup plans for 1–50 employees — PPO, HMO, SHOP, and ICHRA options compared.

National PPO Health Insurance PlansNationwide PPO guidance applying across all 50 states — carriers, networks, and rate structures.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Texas residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.