Texas Health Insurance Marketplace 2026: HealthCare.gov Guide

The Texas health insurance marketplace is HealthCare.gov — Texas does not operate a state-based exchange. For 2026 coverage, approximately 3.2 million Texans enrolled through the federal portal, the highest total of any state, with 88% receiving Advanced Premium Tax Credit subsidies averaging $537 monthly. The marketplace offers HMO and EPO plans only — no PPO products. Texans above the subsidy ceiling or needing PPO access enroll off-exchange directly from carriers.

What brings you here today?

Texas Health Insurance Marketplace: The Federal Exchange

Texas uses the federal HealthCare.gov portal as its health insurance marketplace — not a state-based exchange. All Texas marketplace enrollment, subsidy calculation, plan comparison, and Special Enrollment Period applications happen through HealthCare.gov. Texas enrolled 3.2 million residents in marketplace plans for 2026, the highest count of any state, driven by expanded APTC subsidies that averaged $537 monthly per enrollee.

Texas is one of 30+ states that defaulted to the federal exchange rather than building a state-based marketplace when the ACA launched in 2014. The practical consequence for Texas residents: there is no Texas-specific enrollment portal, no Texas-specific customer service line for marketplace issues, and no state-level supplemental subsidies beyond the federal APTC and CSR. Everything runs through HealthCare.gov. The Texas Department of Insurance regulates the carriers selling plans on the marketplace — reviewing rate filings, network adequacy, and consumer complaints — but TDI has no role in the enrollment process itself, which is entirely federally administered by the Centers for Medicare and Medicaid Services.

Texas marketplace enrollment growth over the past three plan years has been substantial. The Inflation Reduction Act’s expanded APTC provisions — which eliminated the 400% FPL subsidy cliff through enhanced premium caps, extended through 2026 — have made marketplace coverage affordable for Texas households that previously faced full-price premiums. According to CMS 2026 Open Enrollment data, Texas led all states in new marketplace enrollment and in total enrollee count. The 3.2 million enrolled Texans represent roughly 11% of the state’s population — a meaningful but still-minority share of the 29 million residents, reflecting the large coverage gap and uninsured population that market expansion hasn’t reached.

Texas Marketplace Subsidies: APTC and CSR for 2026

Texas health insurance marketplace subsidies come in two forms: Advanced Premium Tax Credit (APTC), which reduces monthly premium directly for households earning 100%–400% of federal poverty level, and Cost-Sharing Reductions (CSR), which lower deductibles and out-of-pocket maximums on Silver-tier plans for households below 250% FPL. Texas marketplace enrollees average $537 monthly in APTC for 2026, with 88% of enrollees receiving at least some credit.

APTC eligibility runs from 100% FPL ($15,060 single adult, $31,200 family of four) to 400% FPL ($60,240 single, $120,000 family of four) for 2026. The credit is calculated as the difference between the full premium of the benchmark Silver plan in your Texas rating area and the maximum premium you’re expected to contribute — capped at a percentage of household income on a sliding scale. A 40-year-old Texan earning $40,000 in the Dallas-Fort Worth rating area is expected to contribute roughly 8.5% of income ($3,400/year, $283/month) toward the benchmark Silver premium. If the benchmark plan costs $510/month at full price, APTC covers the remaining $227. That same APTC applies to any metal tier selected — choosing Bronze over Silver gets the same dollar credit at lower premium, often producing near-zero or zero monthly cost.

CSR is a separate benefit layered on top of APTC, available only on Silver-tier plans for households below 250% FPL. CSR lowers the plan’s actuarial value — reducing the deductible from the standard Silver $5,500 to as low as $300 for households below 150% FPL, and lowering the out-of-pocket maximum from $9,450 to as low as $1,500. CSR is why households below 250% FPL should almost always choose Silver over Bronze even if Bronze appears cheaper on monthly premium — the deductible and MOOP savings on Silver CSR plans typically far outweigh the Bronze premium advantage. Apply at HealthCare.gov to receive both credits automatically with any qualifying plan selection.

| Texas Income (single adult, 2026) | APTC Available? | CSR Available? | Typical Net Monthly Premium |

|---|---|---|---|

| Below $15,060 (below 100% FPL) | No (coverage gap) | No | No affordable path |

| $15,060–$22,590 (100%–150% FPL) | Yes — maximum APTC | Yes — 94% CSR Silver | $0–$40/mo |

| $22,590–$30,120 (150%–200% FPL) | Yes — strong APTC | Yes — 87% CSR Silver | $20–$80/mo |

| $30,120–$37,650 (200%–250% FPL) | Yes — moderate APTC | Yes — 73% CSR Silver | $80–$170/mo |

| $37,650–$58,320 (250%–400% FPL) | Yes — partial APTC | No | $170–$340/mo |

| Above $58,320 (above 400% FPL) | No | No | $390–$520/mo full price |

Texas Marketplace Enrollment: Dates and How to Apply

The HealthCare.gov open enrollment period for 2027 Texas marketplace coverage opens November 1, 2026. Plans selected by December 15, 2026 take effect January 1, 2027; plans selected December 16 through January 15, 2027 take effect February 1, 2027. Outside open enrollment, Texans access marketplace coverage only through a qualifying Special Enrollment Period within 60 days of a triggering life event.

The Texas health insurance marketplace enrollment process at HealthCare.gov follows five steps. First, create or log into a HealthCare.gov account using a valid email address and Social Security number. Second, enter household information — household size, Texas zip code, and projected annual income (MAGI) for the coverage year. Third, review APTC and CSR eligibility calculations the portal generates automatically. Fourth, browse and compare available plans in your Texas rating area — filtered by carrier, metal tier, deductible, premium, and network. Fifth, select and enroll — coverage takes effect based on the enrollment date and the calendar rules above.

The most common Texas marketplace enrollment mistake is underestimating projected income to maximize subsidies, then facing APTC reconciliation on IRS Form 8962 at tax time when actual income exceeds projection. The reconciliation can produce a four-figure tax bill. A more reliable approach: use actual projected Schedule C net income for self-employed Texans, or projected W-2 income for employed Texans, and update HealthCare.gov mid-year if income trends significantly above or below the original projection. The Texas Department of Insurance offers a consumer help line for marketplace-related complaints and carrier disputes at the state level.

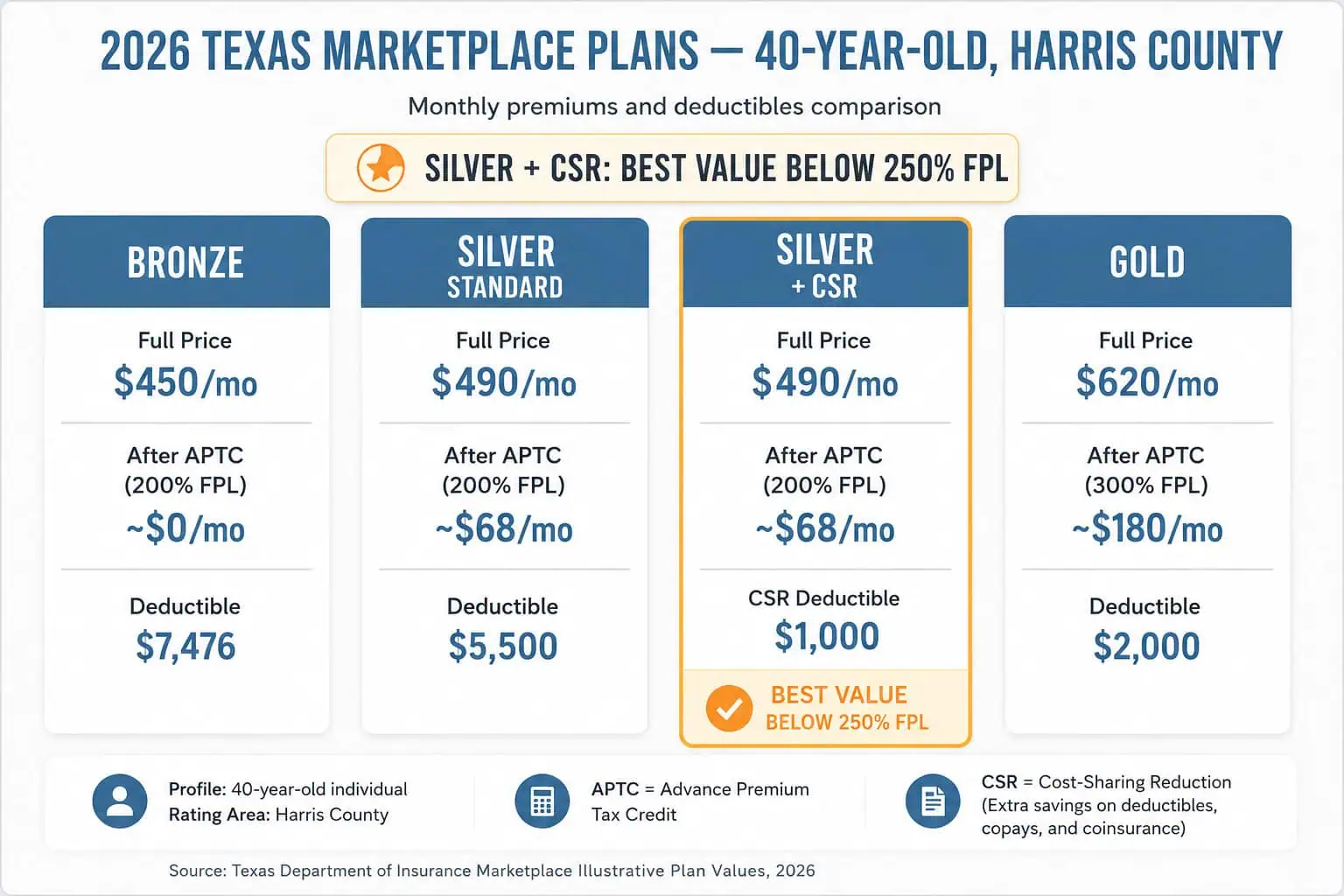

Texas Marketplace Plan Tiers: Bronze, Silver, Gold, Platinum

The Texas health insurance marketplace sells plans across four standard metal tiers — Bronze, Silver, Gold, Platinum — plus Catastrophic for qualifying under-30 enrollees or those with hardship exemptions. Tier selection determines the split between monthly premium and out-of-pocket costs at care time. For most subsidy-eligible Texans, Silver delivers the best total value due to CSR eligibility; Bronze makes sense for healthy households above 250% FPL who want the lowest monthly cost.

Bronze — Lowest premium, highest deductible

Bronze plans cover 60% of average medical costs with the enrollee covering 40%. Lowest monthly premium on HealthCare.gov — typically $390–$520/month at full price for a 40-year-old, often $0–$80 after APTC for qualifying households. Deductibles run $6,500–$7,500. Best fit: healthy Texans above 250% FPL who rarely use care and want the lowest monthly cost. Below 250% FPL, Silver CSR usually beats Bronze on total annual value.

Silver — Best total value for most Texans

Silver plans cover 70% of average costs — but with CSR below 250% FPL, effective actuarial value rises to 73%–94%. The CSR benefit is only available on Silver. Deductibles drop from $5,500 standard to as low as $300 with max CSR. Monthly premium after APTC runs $0–$340 depending on income. Best fit: any household below 250% FPL, and often the best choice through 400% FPL due to APTC dollar-for-dollar alignment with the benchmark Silver plan.

Gold — Lower deductible, higher premium

Gold plans cover 80% of average costs with deductibles typically $1,500–$2,500 and out-of-pocket maximums around $7,500. Higher monthly premium than Silver — typically $590–$720/month full price for a 40-year-old. Best fit: Texans with chronic conditions, regular prescriptions, or planned significant medical care who benefit from the lower deductible even at higher monthly cost. APTC applies to Gold the same way it applies to Silver — the credit amount stays fixed to the benchmark Silver calculation.

Catastrophic — Low premium, very high deductible

Catastrophic plans are available on HealthCare.gov for Texans under 30 or with a qualifying hardship exemption. The $10,600 deductible equals the 2026 federal out-of-pocket maximum — after which the plan covers 100% of in-network care. Three primary care visits and all ACA preventive services are covered before the deductible. No APTC subsidies apply. Premium runs $210–$280/month for a 25-year-old in major Texas metros. Best fit: healthy under-30 Texans above subsidy ceilings.

Example: Houston Warehouse Worker, Age 32 — Choosing Between Silver and Bronze

A 32-year-old warehouse worker in Harris County earns $29,000 annually — approximately 193% of the 2026 federal poverty level. At this income, he qualifies for both APTC and Cost-Sharing Reduction (CSR) subsidies on a Silver plan. On HealthCare.gov, an Ambetter Silver plan in his rating area runs approximately $498/month before subsidies. After his estimated $430/month APTC credit, his net premium is about $68/month. With CSR at 193% FPL, his Silver deductible drops from $5,500 to approximately $1,000 and his out-of-pocket maximum falls to roughly $3,500. The Bronze alternative: an Ambetter Bronze plan after APTC nets to approximately $0/month, but carries a $7,200 deductible with no CSR reduction. The math: at his income level, one unplanned ER visit or minor surgery would exceed his entire year of Silver premiums ($816). He chooses Silver for the cost-sharing protection.

Get a Texas Marketplace Plan Quote

A licensed Texas broker calculates your APTC and CSR subsidy eligibility, compares Bronze and Silver plans from BCBSTX, Ambetter, and Oscar Health by rating area, and checks whether off-exchange coverage would deliver better value for your household income and provider needs. Free, no obligation.

When Off-Exchange Beats the Texas Marketplace

The Texas health insurance marketplace makes sense for most Texans below 400% of federal poverty level because APTC subsidies dramatically reduce net premium. Above that ceiling, off-exchange enrollment opens access to PPO plans unavailable on HealthCare.gov in Texas — with out-of-network reimbursement, no-referral specialist access, and national carrier reciprocity that marketplace HMO and EPO plans do not offer.

The structural limitation of the Texas marketplace is its plan-type restriction. HealthCare.gov in Texas certifies only HMO and EPO products for individual coverage — no PPO plans. This is a carrier market decision rather than a regulatory one; Texas carriers price PPO premiums above the marketplace subsidy ceiling, making them economically unviable for on-exchange certification. The result: any Texan who needs true PPO access — out-of-network reimbursement, no gatekeeper referrals, national network reciprocity — cannot get it through the marketplace regardless of income. The off-exchange private market from BCBSTX, Cigna, UnitedHealthcare, Aetna, and Humana serves this segment exclusively.

For Texans above the 400% FPL subsidy ceiling ($60,240 single, $124,800 family of four in 2026), off-exchange enrollment costs roughly the same as full-price marketplace enrollment but adds PPO plan access. A 45-year-old Lubbock resident earning $75,000 pays full price either channel — $480/month for a marketplace BCBSTX Silver HMO or $650/month for a BCBSTX off-exchange PPO. The $170/month gap buys out-of-network coverage, no-referral specialist access, and BlueCard national reciprocity. For Texans who travel frequently, have providers at multiple Texas systems, or manage specialist-intensive care, that gap often justifies the off-exchange choice. For a detailed comparison of Texas PPO options, see the Texas PPO Plans guide covering all five major carriers, hospital system contracting, and 2026 premium ranges by rating area.

Texas Marketplace Carriers for 2026

Four carriers sell plans on the Texas health insurance marketplace for 2026: BCBSTX, Ambetter (Centene), Oscar Health, and UnitedHealthcare. Aetna exited the individual market entirely at end of 2025 and is no longer on HealthCare.gov in Texas. Availability varies by rating area across the state’s 26 geographic zones. BCBSTX has the broadest statewide presence; Ambetter leads on lowest Bronze and Silver premium across most Texas metros.

BCBSTX is the dominant marketplace carrier in Texas by enrollment, offering Bronze, Silver, and Gold plans across all 26 rating areas. Ambetter is the price-competitive alternative — typically $30–$70 lower monthly premium than BCBSTX for comparable tiers, with a narrower provider network concentrated in Houston, Dallas-Fort Worth, Austin, and San Antonio. Oscar Health serves Houston, Dallas-Fort Worth, Austin, and San Antonio with digital-first HMO and EPO plans and integrated telehealth. Note: Aetna exited the Texas individual market at end of 2025 — not available on HealthCare.gov for 2026. UnitedHealthcare is available in select Texas markets with competitive Gold tier pricing. Checking plan availability by your specific Texas zip code at HealthCare.gov is the only reliable way to confirm which carriers serve your rating area — carrier participation changes annually with each open enrollment cycle.

Frequently Asked Questions

Common questions about the Texas health insurance marketplace cover whether Texas has a state exchange (it does not — HealthCare.gov is the only portal), open enrollment dates for 2026 and 2027 coverage, what plans are available on the marketplace (HMO and EPO only — no PPO), how much APTC and CSR subsidies reduce premiums for Texas enrollees, and when off-exchange enrollment makes more sense than the marketplace.

Does Texas have its own health insurance marketplace?

No. Texas does not operate a state-based health insurance exchange. Texas residents enroll in ACA-compliant marketplace plans through the federal HealthCare.gov portal — the only legitimate marketplace enrollment channel for Texas. Texas is one of the largest states by population to rely entirely on the federal exchange. The Texas Department of Insurance regulates carrier rates and network adequacy, but the exchange itself is operated by the federal Centers for Medicare and Medicaid Services (CMS). For 2026 coverage, approximately 3.2 million Texans enrolled through HealthCare.gov — the highest marketplace enrollment total of any state.

When is open enrollment for the Texas health insurance marketplace in 2026?

The HealthCare.gov open enrollment period for 2026 Texas health insurance marketplace coverage ran from November 1, 2025 through January 15, 2026. Plans selected by December 15, 2025 took effect January 1, 2026; plans selected between December 16 and January 15 took effect February 1, 2026. Outside open enrollment, Texas residents can enroll through a qualifying Special Enrollment Period within 60 days of a triggering life event: job loss and loss of employer coverage, marriage, divorce, birth, adoption, moving to a new Texas rating area, or aging off a parent’s plan at 26. The next open enrollment for 2027 coverage opens November 1, 2026.

What plans are available on the Texas health insurance marketplace?

The Texas HealthCare.gov marketplace offers HMO and EPO plan types across Bronze, Silver, Gold, Platinum, and Catastrophic metal tiers. No individual PPO plans are sold on the Texas marketplace — Texans who want PPO coverage must enroll off-exchange directly from carriers such as BCBSTX, Cigna, or UnitedHealthcare. Marketplace carriers available in Texas include Blue Cross Blue Shield of Texas (BCBSTX), Ambetter (Centene), Oscar Health, and UnitedHealthcare, with availability varying by the state’s 26 geographic rating areas. Aetna exited the individual market at end of 2025 and is no longer available on the Texas marketplace for 2026. The most widely available carriers statewide are BCBSTX and Ambetter.

How much are Texas marketplace health insurance subsidies in 2026?

Texas marketplace enrollees receive an average Advanced Premium Tax Credit (APTC) of $667 per month for 2026 coverage according to CMS enrollment data, with 92% of Texas enrollees receiving at least some subsidy. APTC is available to households earning between 100% and 400% of federal poverty level — $15,060 to $60,240 for a single adult in 2026, and $31,200 to $124,800 for a family of four. Cost-Sharing Reductions (CSR) further lower deductibles and out-of-pocket costs for households below 250% FPL on Silver plans. A 40-year-old Texan earning $40,000 typically pays $80–$160 monthly for a Silver plan after APTC subsidies.

When does it make sense to go off-exchange instead of the Texas marketplace?

Off-exchange enrollment makes more sense than the Texas health insurance marketplace when a household’s income exceeds the 400% FPL APTC subsidy ceiling ($60,240 single or $124,800 family of four in 2026), because at full price both channels carry similar ACA-compliant coverage but off-exchange adds PPO access unavailable on HealthCare.gov in Texas. PPO plans from BCBSTX, Cigna, UnitedHealthcare, and Humana are only available off-exchange — providing out-of-network reimbursement, no-referral specialist access, and national reciprocity that marketplace HMO and EPO plans do not offer. For households that qualify for APTC, the Texas marketplace almost always delivers better value than off-exchange due to the subsidy benefit.

Compare 2026 Texas Marketplace Plans

A licensed Texas broker calculates your APTC and CSR subsidy eligibility, compares all available plans in your Texas rating area from BCBSTX, Ambetter, and Oscar Health, and models whether off-exchange PPO coverage would deliver better value for your household. Free, no obligation.

Free Texas marketplace comparison — subsidies, tiers, and off-exchange alternatives in one call.

Explore Texas Coverage In Depth

Statewide overview — marketplace, Medicaid gap, off-exchange, and carrier landscape.

Individual Texas Health InsuranceIndividual coverage paths — marketplace, off-exchange PPO, and direct carrier enrollment.

Texas PPO PlansOff-exchange PPO unavailable on HealthCare.gov — BCBSTX, Cigna, UHC compared.

Self-Employed Texas Health InsuranceMAGI projection, Schedule 1 deduction, and marketplace vs off-exchange for 1099 contractors.

Cheap Texas Health InsuranceLowest-cost marketplace plans — Bronze, Silver CSR, and CHIP for qualifying families.

Catastrophic Texas Health InsuranceUnder-30 marketplace plans — $10,600 deductible, hardship exemption.

Short-Term Texas Health InsuranceBridge coverage for gap periods — 36-month Texas STLD limit, UHC Golden Rule, Pivot.

Private Texas Health InsuranceOn-exchange vs off-exchange — the subsidy trade-off and direct carrier enrollment explained.

Family Texas Health InsuranceCHIP split-enrollment, marketplace family plans, and the ACA family glitch fix.

Texas Retiree Health InsurancePre-Medicare bridge ages 55–64 — TRS-Care, ERS, APTC subsidies, COBRA vs marketplace.

Texas Small Business Health InsuranceGroup plans for 1–50 employees — PPO, HMO, SHOP, and ICHRA options compared.

National PPO Health Insurance PlansNationwide PPO guidance applying across all 50 states — carriers, networks, and rate structures.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Texas residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.