Retiree Health Insurance Texas 2026: Pre-Medicare Guide

Retiree health insurance Texas options for adults ages 55–64 bridge the gap between employer coverage and Medicare eligibility at 65. The four primary paths are ACA marketplace plans on HealthCare.gov, COBRA continuation from a former employer, state retiree programs (ERS for state employees, TRS-Care for public school teachers), and off-exchange PPO plans. Full-price Silver premiums for a 62-year-old Texas retiree run $900–$1,200 monthly before subsidies — but APTC subsidies often reduce cost dramatically for retirees with lower retirement income.

What brings you here today?

The Pre-Medicare Coverage Gap in Texas

Texas retirees leaving employer coverage before 65 face a pre-Medicare gap of months to a decade — and with Texas’s 16.7% uninsured rate (highest in the nation per 2024 Census ACS data), going uninsured is a real risk. Medicare begins at 65 for most Texans. For the 55–64 window, retiree health insurance Texas options include ACA marketplace plans with APTC subsidies, COBRA continuation, TRS-Care for retired educators, ERS HealthSelect for state employees, and off-exchange PPO for above-subsidy households.

The pre-Medicare coverage gap is the defining financial planning challenge for early retirement in Texas. Employer-sponsored health insurance — the dominant coverage vehicle for working-age Texans — ends at retirement. COBRA preserves the same plan for up to 18 months at 102% of the full premium (employee share plus employer share plus 2% administrative fee). After COBRA expires, retiree health insurance Texas private-sector buyers have two primary ACA-compliant options: HealthCare.gov marketplace plans and off-exchange direct carrier enrollment. Texas has no state-based retiree health program for private-sector workers — unlike some other states with risk pools or retiree coverage bridges.

What makes the pre-Medicare gap particularly consequential in Texas is age-band pricing under ACA rules. The ACA permits up to a 3:1 premium ratio between the oldest and youngest enrollees — a 64-year-old can be charged up to 3 times the premium of a 21-year-old for the same plan. A Texas marketplace Silver plan priced at $440/month for a 40-year-old can cost $1,050–$1,200/month for a 64-year-old at full price. According to Kaiser Family Foundation analysis, Texas has among the highest full-price pre-Medicare marketplace premiums of any large state — driven by the older demographic profile in many Texas retiree markets and the state’s 26-rating-area premium variation.

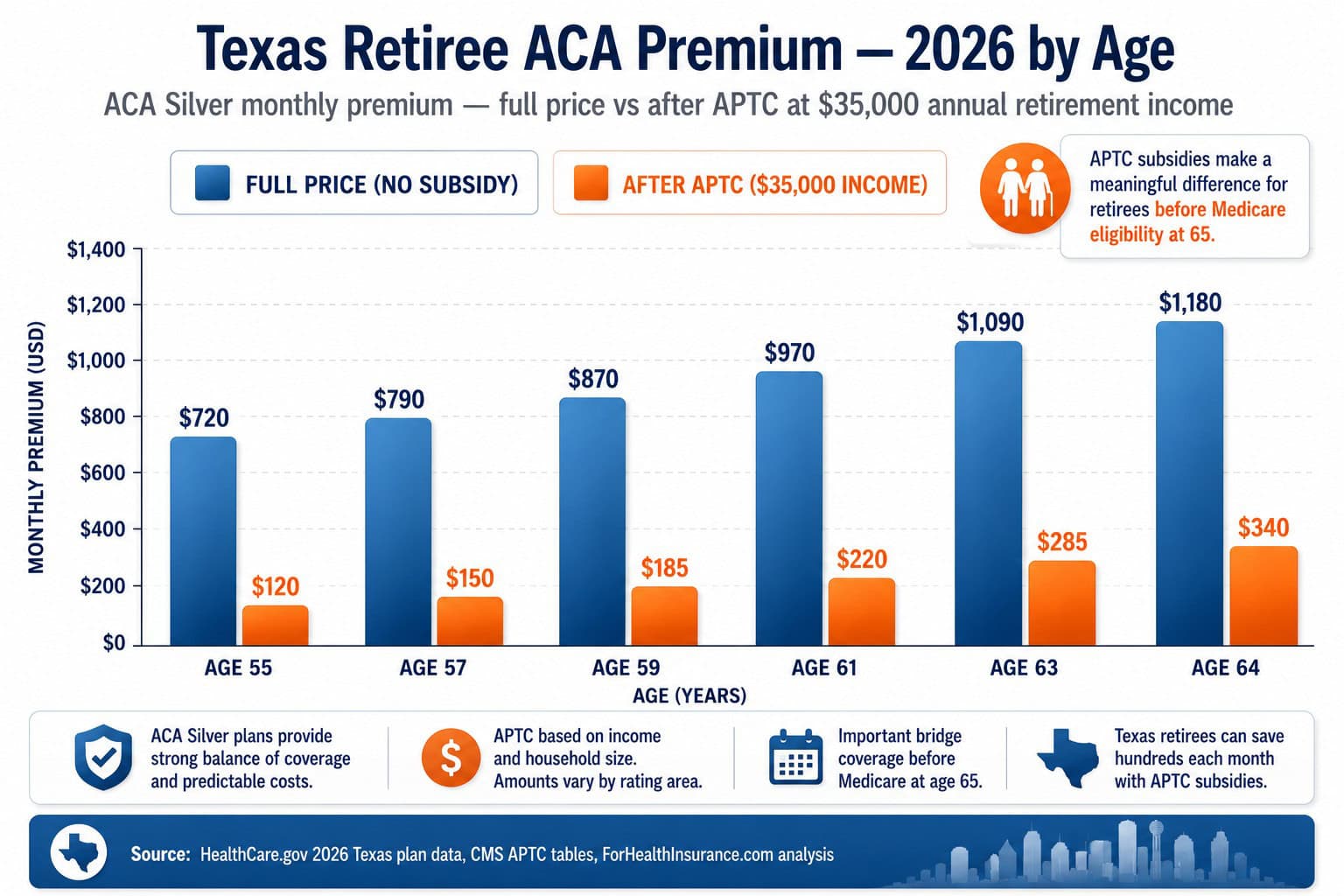

What Retiree Health Insurance Costs in Texas for 2026

Retiree health insurance Texas premiums in 2026 are significantly higher than working-age coverage due to ACA age-band pricing. Full-price ACA Silver premiums for a 62-year-old Texas retiree run $900–$1,200 monthly; Gold runs $1,100–$1,500. After Advanced Premium Tax Credit, a 62-year-old retiree with $35,000 annual income typically pays $150–$350 monthly for Silver. COBRA continuation for a 62-year-old typically runs $800–$1,600 monthly — the full employer plan premium with no employer subsidy.

| Texas Retiree Coverage Option | Typical Monthly Cost (age 62) | Duration | Best Fit For |

|---|---|---|---|

| ACA Silver — subsidized (HealthCare.gov) | $150–$350/mo (after APTC, $35K income) | Until Medicare at 65 | Early retirees with moderate income |

| ACA Silver — full price (HealthCare.gov) | $900–$1,200/mo | Until Medicare at 65 | Higher-income retirees, no APTC |

| ACA Gold — full price (HealthCare.gov) | $1,100–$1,500/mo | Until Medicare at 65 | Higher utilization retirees, rich benefits |

| COBRA continuation | $800–$1,600/mo | Up to 18 months | Active claims, pre-existing conditions, mid-year |

| Off-exchange PPO (direct carrier) | $950–$1,400/mo | Until Medicare at 65 | Above-subsidy income, PPO network needed |

| TRS-Care Standard (Texas teachers) | $200–$500/mo | Until Medicare at 65 | Eligible TRS retirees with 10+ years service |

| ERS retiree coverage (Texas state employees) | $100–$350/mo | Until Medicare at 65 | Eligible ERS retirees with qualifying service |

The APTC subsidy opportunity is often the most significant financial variable for Texas retirees. Many early retirees have dramatically reduced taxable income compared to their working years — particularly in the first few years before Social Security begins and before required minimum distributions from retirement accounts kick in. A 60-year-old Texas retiree drawing $38,000 annually from a Roth IRA (which counts as zero MAGI) and $5,000 from modest investment income reports $5,000 MAGI — potentially qualifying for maximum APTC and CSR subsidies on HealthCare.gov. Retiree health insurance Texas planning around MAGI projections is worth modeling carefully every November before open enrollment to optimize subsidy eligibility.

Example: San Antonio School District Retiree, Age 60 — TRS-Care vs Marketplace

A 60-year-old retired San Antonio ISD teacher with 28 years of service credit qualifies for TRS-Care Standard. Her TRS-Care Standard monthly premium runs approximately $380/month for individual coverage with a $1,000 deductible and access to Texas Children’s and UT Health San Antonio in-network. She also models the HealthCare.gov alternative: with $32,000 in annual retirement income (pension plus modest IRA withdrawals), she sits at approximately 212% of the 2026 federal poverty level. An Ambetter Silver plan on HealthCare.gov after APTC runs approximately $185/month in her Bexar County rating area — $195/month cheaper than TRS-Care Standard. However, her TRS-Care plan includes dental and vision riders at no additional premium, and her established rheumatologist at UT Health San Antonio is in-network on both plans. She chooses TRS-Care Standard for the ancillary coverage and network continuity, accepting the $2,340/year premium premium over the marketplace option.

Get a Texas Retiree Health Insurance Quote

A licensed Texas broker models APTC subsidy eligibility based on projected retirement income, compares ACA marketplace Silver and Gold plans from BCBSTX, Ambetter, and Oscar Health against COBRA continuation costs, and evaluates off-exchange PPO options for higher-income retirees. Free, no obligation.

Texas ERS and TRS-Care Retiree Programs

Texas state retirees have two distinct programs depending on their former employer. The Employees Retirement System of Texas (ERS) provides retiree health coverage for eligible state agency employees, with monthly premiums of $100–$350 for pre-Medicare retirees. The Teacher Retirement System of Texas (TRS) provides TRS-Care for eligible retired public school educators, with TRS-Care Standard premiums of $200–$500 monthly for retirees not yet eligible for Medicare. Both programs require qualifying years of service.

The Texas Employees Retirement System covers retired employees of state agencies, the Texas Department of Transportation, UT Austin, Texas A&M, and other ERS-participating employers — roughly 260,000 active retirees statewide. ERS retirees who meet age and service requirements receive access to HealthSelect of Texas at group rates running approximately $200–$450/month for individual pre-Medicare coverage — substantially below what private-sector retirees pay on the individual marketplace ($900–$1,200 full-price Silver). ERS retiree premiums are set annually by the Texas Legislature and administered through the Employees Retirement System of Texas. Dependent coverage is available at additional premium, and ERS retiree coverage transitions to ERS Medicare Advantage plans upon Medicare eligibility at 65.

TRS-Care is the Teacher Retirement System of Texas retiree health program for retired educators from Houston ISD, Dallas ISD, Austin ISD, and all Texas public school districts — covering roughly 260,000 TRS retirees and dependents statewide. TRS-Care Standard (for pre-Medicare retirees) runs approximately $200–$500/month depending on tier and dependent status; TRS-Care Medicare Advantage and Medicare Rx serve TRS retirees who become Medicare-eligible at 65. Eligibility requires at least 10 years of Texas public school service credit and meeting TRS age and service requirements under the Teacher Retirement System. TRS-Care premiums are set annually by the TRS board and run $500–$700/month below private marketplace Silver premiums for a 62-year-old — a significant financial advantage for Texas career educators.

TRS-Care vs HealthCare.gov marketplace for Texas teacher retirees

Texas teacher retirees eligible for TRS-Care face a specific enrollment decision: TRS-Care Standard premiums ($200–$500/mo) versus HealthCare.gov marketplace plans, which may carry APTC subsidies that bring cost below TRS-Care if retirement income is moderate. The key factor: TRS-Care enrollment is annual with specific open enrollment windows and cannot be freely dropped and re-enrolled year to year. Teacher retirees weighing marketplace alternatives should compare not just monthly premium but network access, deductible structures, and the long-term enrollment commitment before declining TRS-Care. Contact the Teacher Retirement System of Texas directly before making the TRS-Care vs marketplace decision — the tradeoffs are specific to each retiree’s income, age, and health utilization profile.

COBRA vs ACA Marketplace for Texas Retirees

Texas retirees choosing between COBRA continuation and HealthCare.gov marketplace coverage face a cost-and-continuity trade-off. COBRA preserves the same plan and providers for up to 18 months at full group premium — typically $800–$1,600 monthly for a 62-year-old. A subsidized ACA marketplace Silver plan may cost $150–$400 monthly for the same retiree at moderate income — but requires switching networks and resetting deductible accumulation mid-year if transitioning outside open enrollment.

The financial case for switching from COBRA to a marketplace plan is strongest when two conditions are met: the retiree qualifies for meaningful APTC subsidies (retirement income below 400% of federal poverty level), and the retiree’s current care situation doesn’t require continuity of mid-year deductible accumulation. A Kerrville-area Texas retiree who left their job in January, elected COBRA, and projects $38,000 in annual income for 2026 qualifies for substantial APTC — switching to a HealthCare.gov Silver plan in February during the COBRA-to-marketplace SEP (within 60 days of losing employer coverage) could save $500–$900 monthly. That $6,000–$10,800 annual savings often justifies the network transition.

COBRA makes more financial sense when the retiree has active claims, is mid-treatment with an ongoing deductible accumulation, has pre-existing conditions best served by the current network, or faces provider relationships at specific Texas facilities that are not in the available marketplace networks. A 64-year-old Texan managing a chronic condition at Memorial Hermann who retires in October and has met $6,000 of their deductible should strongly consider staying on COBRA through year-end — preserving the deductible accumulation and network continuity — then transitioning to HealthCare.gov on January 1. The HealthCare.gov SEP for losing job-based coverage is the key enrollment window: 60 days from the loss of coverage date.

Retiree Health Insurance Texas: Coverage Path Decision

The right retiree health insurance Texas path depends on former employer type (private sector vs TRS or ERS), retirement income relative to the $60,240 APTC ceiling, years until Medicare at 65, and provider relationships at systems like Methodist Hospital San Antonio or Houston Methodist. Private-sector retirees below $60,240 almost always benefit most from subsidized HealthCare.gov Silver; COBRA bridges the first 18 months when provider continuity matters.

Private-sector retiree, moderate income — ACA marketplace

A 60-year-old Texas Hill Country retiree with $40,000 annual income from pension and modest investment income qualifies for strong APTC subsidies on HealthCare.gov — likely reducing a $1,000/month Silver premium to $200–$350/month. Five years of retiree health insurance Texas coverage on subsidized marketplace plans saves $60,000–$80,000 versus full-price COBRA or off-exchange before Medicare. Requires no pre-existing condition that demands COBRA network continuity.

Private-sector retiree, high income — off-exchange PPO

A 63-year-old Texan with $180,000 annual income from business sale proceeds, investment distributions, and Social Security exceeds the 400% FPL APTC ceiling. Full-price marketplace Silver at $1,150/month versus a Cigna or UnitedHealthcare off-exchange PPO at $1,200–$1,400/month — the PPO premium difference is modest and gains national network, no-referral specialist access, and out-of-network reimbursement valuable for complex care management in the final years before Medicare.

Texas public school teacher — TRS-Care Standard

A 62-year-old retired teacher with 28 years of Texas public school service credit enrolls in TRS-Care Standard at $350/month — well below the $1,100/month full-price marketplace equivalent. TRS-Care’s group-rate advantage is the primary financial benefit of the Teacher Retirement System of Texas for pre-Medicare retirees. Worth comparing against marketplace APTC subsidies only if projected retirement income produces substantial subsidies that bring marketplace cost below TRS-Care premium.

Texas state employee retiree — ERS coverage

A 61-year-old retired Texas state agency employee with 20 years of service accesses ERS retiree health coverage at $180/month — approximately one-sixth the cost of comparable private-sector marketplace coverage. ERS retiree coverage is one of the most financially favorable retiree health insurance Texas options available, significantly outperforming marketplace and COBRA alternatives for eligible retirees. Enrollment is managed through the Employees Retirement System of Texas and transitions automatically to ERS Medicare Advantage at age 65.

Managing Income to Maximize Texas Retiree Subsidies

Texas retirees on Ambetter, BCBSTX, or Oscar marketplace plans can manage MAGI to optimize APTC. At $35,000 income (232% FPL), a 62-year-old Texan pays approximately $185–$350/month for Silver after subsidies. Roth IRA withdrawals, home equity proceeds, and gifts don’t count toward MAGI; traditional IRA distributions, pension, Social Security above threshold, and capital gains do. Timing withdrawals and Roth conversions to stay below $60,240 preserves subsidy eligibility — worth modeling each November before Texas open enrollment.

The MAGI management opportunity is unique to retirees in a way it isn’t for working-age enrollees. A 62-year-old Texas retiree with a substantial Roth IRA, a traditional IRA, a pension, and investment accounts has meaningful control over which income sources to draw in a given year. Pulling primarily from the Roth IRA (zero MAGI impact) in years before Social Security begins and before traditional IRA required minimum distributions kick in at age 73 can keep MAGI in favorable ACA subsidy bands — potentially $25,000–$45,000 for a single retiree, qualifying for $500–$800 monthly in APTC on retiree health insurance Texas Silver coverage for ages 60–64.

The cliff to avoid is the 400% FPL APTC subsidy cutoff — above $60,240 for a single Texas retiree in 2026, APTC drops to zero and full-price premiums apply. For a 62-year-old whose full-price Silver plan runs $1,100/month ($13,200/year), at $57,000 income (378% FPL) the APTC reduces annual cost to about 9.96% of income ($5,677) — an annual subsidy of approximately $7,500. At $60,241 income, APTC drops to zero and the full $13,200 applies. Careful income planning in November — before open enrollment and before any year-end distributions — can preserve substantial subsidy eligibility. A financial advisor familiar with ACA MAGI rules and a licensed Texas health insurance broker working in tandem can optimize both the income planning and the plan selection for pre-Medicare Texas retirees.

Frequently Asked Questions

Common questions from Texas retirees cover the 55–64 pre-Medicare gap, 2026 Silver premiums of $900–$1,200/month full-price versus $150–$350/month after APTC, TRS-Care Standard eligibility for Houston ISD and Dallas ISD retirees, ERS HealthSelect rates for UT Austin and TAMU retirees, how to manage MAGI below the $60,240 APTC ceiling, and when COBRA savings justify switching to Ambetter or BCBSTX marketplace coverage.

What are the health insurance options for Texas retirees before Medicare?

Texas retirees between ages 55 and 64 have four primary retiree health insurance Texas options before Medicare eligibility at 65: HealthCare.gov ACA marketplace plans (the most common path, often subsidized for early retirees with reduced income), COBRA continuation from the last employer plan (preserves existing coverage for up to 18 months at full premium), retiree health coverage through a former employer if offered, and for Texas state employees and teachers, the Employees Retirement System (ERS) or Teacher Retirement System TRS-Care retiree health programs. ACA marketplace plans are the most flexible option for private-sector retirees, with APTC subsidies often available if retirement income falls below 400% of federal poverty level.

How much does retiree health insurance cost in Texas for 2026?

Retiree health insurance Texas costs in 2026 run significantly higher than working-age coverage due to the ACA’s 3:1 age-band pricing rule — a 64-year-old pays up to 3 times the premium of a 21-year-old for the same plan. Full-price ACA Silver premiums for a 62-year-old Texas retiree run $900–$1,200 per month before subsidies; Gold plans run $1,100–$1,500. After Advanced Premium Tax Credit, a 62-year-old Texas retiree with $35,000 in annual retirement income (about 233% of federal poverty level) typically pays $150–$350 monthly for Silver coverage. COBRA continuation typically runs $800–$1,600 monthly for a 62-year-old, depending on the former employer’s plan.

What is TRS-Care for Texas teacher retirees?

TRS-Care is the Texas Teacher Retirement System’s retiree health insurance program for retired Texas public school educators and their eligible dependents. TRS-Care offers three coverage tiers: TRS-Care Standard (lower premium, higher cost-sharing), TRS-Care Medicare Advantage (for TRS retirees eligible for Medicare), and TRS-Care Medicare Rx (prescription drug coverage for Medicare-eligible TRS retirees). Eligibility requires at least 10 years of Texas public school service credit and meeting age and service requirements under the Teacher Retirement System of Texas. Monthly premiums for TRS-Care Standard for a retiree under 65 run $200–$500 depending on coverage tier and dependent status. TRS-Care is administered separately from HealthCare.gov — TRS retirees enroll directly through the Teacher Retirement System of Texas.

Can early retirees in Texas get ACA subsidies?

Yes — early Texas retirees are often some of the best candidates for Advanced Premium Tax Credit subsidies on HealthCare.gov. Many early retirees have significantly reduced income compared to their working years, placing them squarely within the ACA subsidy bands. A 60-year-old Texas retiree with $40,000 in annual income from pension, IRA withdrawals, or investment income is at about 267% of federal poverty level — qualifying for substantial APTC that can reduce a $1,100/month Silver premium to $200–$350/month. The key: Roth IRA withdrawals and home equity proceeds are not counted as MAGI; traditional IRA distributions, pension income, Social Security income above threshold, and capital gains are all included in the MAGI calculation used to determine APTC eligibility.

When should Texas retirees switch from COBRA to marketplace coverage?

Texas retirees should switch from COBRA to HealthCare.gov marketplace coverage when the APTC subsidy on a marketplace plan produces meaningful monthly savings versus COBRA’s full employer-plan premium. COBRA for a 62-year-old Texas retiree typically runs $900–$1,400 monthly; a subsidized HealthCare.gov Silver plan for the same retiree at $35,000 annual income might run $200–$350 monthly — a potential savings of $700–$1,200 per month. The trade-off: switching from COBRA to marketplace resets the deductible mid-year and may require provider network changes. COBRA expiration (at 18 months maximum) triggers a Special Enrollment Period for marketplace enrollment — Texas retirees approaching COBRA expiration should evaluate marketplace options at least 60 days before COBRA ends.

Compare 2026 Texas Retiree Health Insurance

A licensed Texas broker models APTC subsidy eligibility based on projected retirement income, compares ACA marketplace Silver and Gold plans against COBRA continuation and off-exchange PPO options, and evaluates TRS-Care and ERS program alternatives for qualifying Texas state retirees. Free, no obligation.

Free Texas retiree coverage comparison — marketplace, COBRA, PPO, and state programs in one call.

Explore Texas Coverage In Depth

Statewide overview of Texas health insurance — marketplace, Medicaid, and off-exchange options compared.

Texas Marketplace EnrollmentHealthCare.gov enrollment guide for Texas — APTC subsidies, open enrollment, and SEPs.

Individual Texas Health InsuranceIndividual plan options — marketplace, off-exchange PPO, and direct carrier enrollment.

Texas PPO PlansOff-exchange PPO for Texas retirees above subsidy ceilings — BCBSTX, Cigna, UHC.

Self-Employed Texas Health InsuranceCoverage for Texas retirees who continue consulting or self-employed work post-retirement.

Cheap Texas Health InsuranceLowest-cost Texas plans — subsidized Silver for lower-income early retirees.

Catastrophic Texas Health InsuranceUnder-30 hardship exemption plans — $10,600 deductible, for pre-retirement gap planning.

Short-Term Texas Health InsuranceBridge coverage for brief pre-Medicare gaps — COBRA alternative considerations.

Private Texas Health InsuranceOn-exchange and off-exchange private coverage options for Texas retirees.

Family Texas Health InsuranceFamily coverage for Texas retirees with spouses and dependents under 65.

Texas Small Business Health InsuranceGroup plans for 1–50 employees — for retirees who re-enter consulting or small business.

National PPO Health Insurance PlansNationwide PPO guidance applying across all 50 states — carriers, networks, and rate structures.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Texas residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.