Short-Term Health Insurance Texas 2026: Bridge Coverage

Short term health insurance Texas plans are non-ACA-compliant temporary coverage for healthy adults bridging gaps between employer plans, post-COBRA periods, or waiting for ACA open enrollment. Texas allows STLD plans up to 36 months total — one of the most permissive state regulatory environments. Premiums run $90–$250 monthly for a 30-year-old in 2026, but the savings come with significant trade-offs: no maternity, mental health, prescriptions, or pre-existing condition coverage, plus $1–$2 million lifetime caps.

What brings you here today?

Who Needs Short-Term Health Insurance in Texas

Short term health insurance Texas plans from UnitedHealthcare Golden Rule, BCBSTX, and Pivot Health work for healthy adults bridging brief gaps — a San Antonio professional between jobs for 60–90 days, a Houston contractor with a 30-day employer waiting period, or a Dallas resident aging off parental coverage at 26. Texas allows these plans up to 36 months under TDI oversight, making them more accessible here than in most states. The right use case is narrow.

The typical short term health insurance Texas buyer is a person caught between coverage options. A San Antonio professional laid off in February doesn’t qualify to enroll in HealthCare.gov until November open enrollment unless job loss triggers a Special Enrollment Period — which it usually does, but only for 60 days. After that window, short-term may be the only available coverage path for a healthy adult who declined or exhausted COBRA. A Dallas contract-to-hire employee starting a new job with a 60-day waiting period needs coverage during the gap. A Houston retiree-to-be aging into Medicare in 4 months needs interim protection. In each case, the plan length matches the predictable gap.

Texas’s regulatory environment makes short-term unusually accessible — the Texas Department of Insurance licenses and oversees all STLD carriers, publishing quarterly complaint indices and annual rate filings for each. Texas adopts the federal maximum 36-month duration, which means STLD plans here can run longer than in California (banned), New York (3-month cap), or Colorado (6-month cap). UnitedHealthcare Golden Rule plans in Harris County and Bexar County run approximately $120–$155/month for a 30-year-old on a Standard tier, while Pivot Health’s Basic tier starts around $90–$110/month in the same markets. The Texas Department of Insurance regulates carrier filings, rate adequacy, and complaint indices — providing oversight equivalent to fully-insured ACA carriers but without imposing the 10 essential health benefit requirements that define ACA-compliant plans.

Common Texas short-term coverage scenarios in 2026

The five most common use cases: (1) job loss with COBRA declined or exhausted, missed the 60-day Special Enrollment Period for HealthCare.gov; (2) contract-to-hire waiting period of 30–90 days at a new employer; (3) early retirement gap before Medicare eligibility at age 65; (4) recent college graduate aging off parental coverage at 26 with no employer plan yet; (5) gig worker or 1099 contractor projecting above-subsidy income who wants lower premium than full-price marketplace. In each case, the short-term plan covers a predictable, time-bounded gap — not as a long-term substitute for ACA-compliant coverage.

What Short-Term Plans Exclude vs ACA Coverage

Short term health insurance Texas plans are NOT ACA-compliant and typically exclude maternity care, prescription drug coverage at meaningful levels, mental health and substance use treatment, pre-existing conditions (12-24 month lookback), preventive care without cost-sharing, and pediatric dental and vision. Lifetime coverage limits are usually $1–$2 million versus the ACA’s unlimited annual and lifetime maximums.

The exclusions are the central trade-off of every short term health insurance Texas plan. The Affordable Care Act requires marketplace plans sold on HealthCare.gov in Texas — Bronze through Platinum tiers from Ambetter, BCBSTX, and Oscar Health — to cover 10 essential health benefits: ambulatory services, emergency, hospitalization, maternity, mental health and substance use, prescription drugs, rehabilitation, laboratory, preventive and wellness, and pediatric services. Short-term plans from UnitedHealthcare Golden Rule and Pivot Health are exempt from this requirement and almost always exclude or severely limit several of these categories — most critically maternity, mental health, and prescriptions.

Maternity is the highest-stakes exclusion. A pregnancy detected three months into a Texas short-term plan typically results in $30,000–$80,000+ of uncovered prenatal, delivery, and postpartum care. Mental health and substance use treatment exclusions affect Texans managing depression, anxiety, ADHD, or other ongoing conditions — short-term plans usually exclude or severely cap therapy, medication management, and inpatient care. Pre-existing condition exclusions apply with a 12–24 month lookback in most Texas short-term plans, meaning any condition you sought treatment for in the past 1–2 years won’t be covered. Prescription drug coverage on short-term plans typically caps at $1,500–$3,000 annually with discount-card-level cost-sharing rather than the integrated formularies of ACA plans.

Read the policy exclusions before enrolling

Short-term plan exclusions vary significantly by carrier — what BCBSTX covers, UnitedHealthcare may exclude, and what Pivot Health limits, Everest may exclude entirely. Before enrolling in any short term health insurance Texas plan, read the policy summary of benefits and exclusions documents carefully. Pay specific attention to: pre-existing condition lookback period (12 vs 24 months), maternity coverage (almost always excluded), mental health treatment limits, prescription drug caps, lifetime maximum (typically $1M or $2M), pre-authorization requirements for major care, and out-of-network coverage rules. A 30-minute review prevents a $40,000 surprise on the first claim.

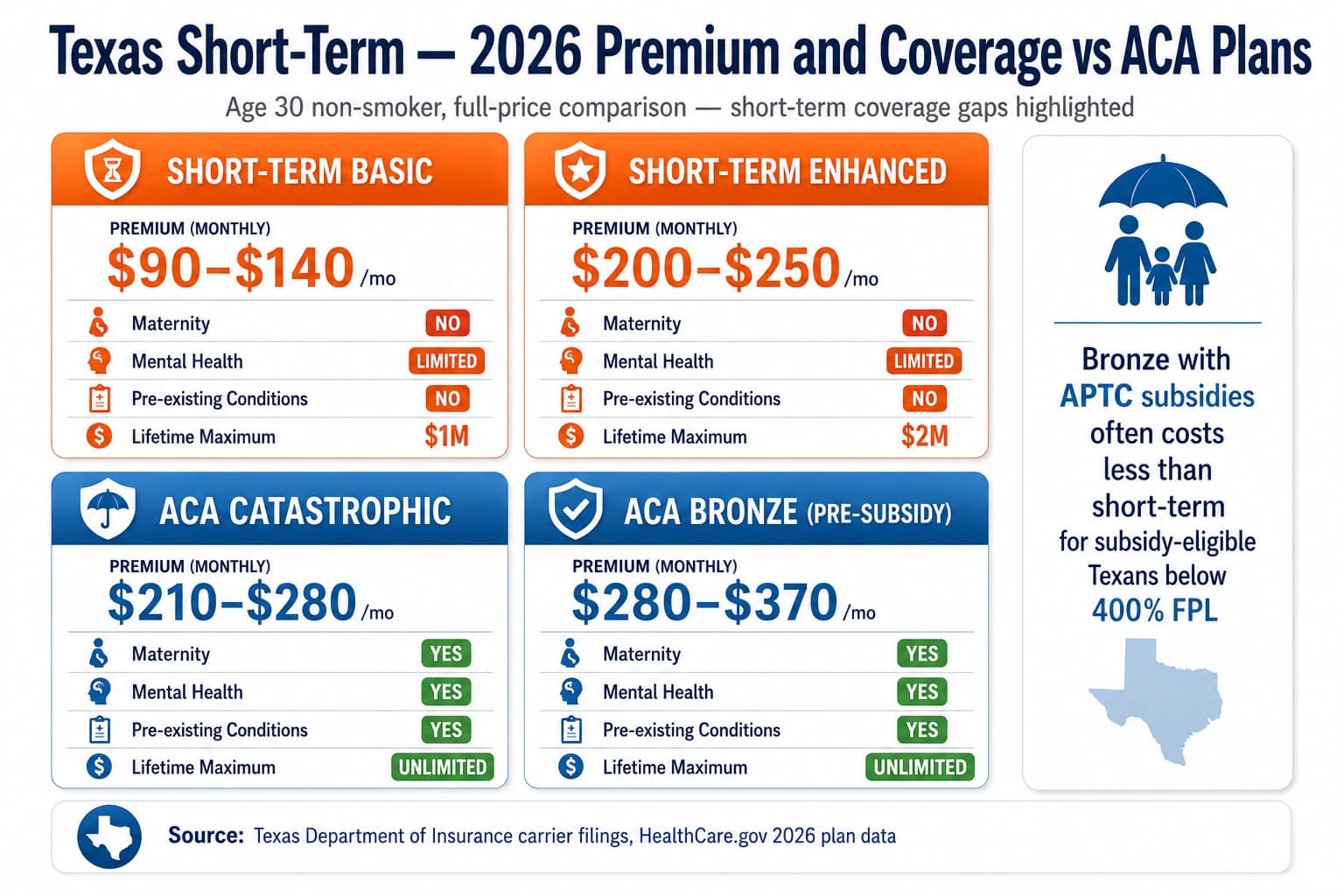

2026 Short-Term Plan Costs in Texas

Short term health insurance Texas premiums in 2026 typically run $90–$250 monthly for a 30-year-old non-smoker, with rate variation by carrier, deductible selection, and applicant health status. UnitedHealthcare Golden Rule and Pivot Health compete on lowest premium; BCBSTX runs higher with broader provider access. Premiums increase significantly with age — a 55-year-old typically pays $200–$450 monthly for equivalent coverage. Medical underwriting means carriers can deny applications or charge higher rates.

| Texas Short-Term Plan Tier | Monthly Premium (age 30) | Deductible | Lifetime Maximum |

|---|---|---|---|

| Basic / Low-cost STLD | $90–$140/mo | $5,000–$7,500 | $750,000–$1,000,000 |

| Standard STLD | $140–$200/mo | $2,500–$5,000 | $1,000,000–$1,500,000 |

| Enhanced STLD | $200–$250/mo | $1,000–$2,500 | $1,500,000–$2,000,000 |

| For comparison — ACA Bronze (age 30) | $280–$370/mo (pre-subsidy) | $7,476 avg | Unlimited |

| For comparison — ACA Catastrophic (age 25–29) | $210–$280/mo | $10,600 | Unlimited |

The $90–$140 short-term premium range looks attractive next to $280–$370 unsubsidized Bronze — until you account for what’s excluded. A subsidy-eligible Texan often pays $40–$80 monthly for Bronze after Advanced Premium Tax Credit, which is below even the cheapest short-term plan. Short term health insurance Texas economics work best for Texans above the 400% federal poverty level subsidy ceiling who can’t take advantage of marketplace subsidies — but those same Texans are typically in better financial position to absorb a major medical event under an ACA-compliant plan with unlimited lifetime coverage. The arithmetic favors short-term primarily in narrow gap-coverage scenarios, not as a long-term insurance strategy.

Example: Dallas IT Contractor, Age 32 — Job Gap Coverage Decision

A 32-year-old Dallas IT contractor loses his employer plan on March 31 and starts a new contract role with a 90-day waiting period — meaning his new employer plan begins July 1. He has a 90-day gap. His COBRA continuation premium is $980/month for his existing employer PPO. A UnitedHealthcare Golden Rule Standard STLD plan in Dallas runs approximately $155/month with a $2,500 deductible and a $1,250,000 lifetime maximum. He’s healthy, no chronic conditions, no planned procedures. The math: $980 × 3 = $2,940 COBRA vs $155 × 3 = $465 short-term — a $2,475 savings over the gap. He accepts the trade-off: maternity and mental health exclusions don’t apply to his situation, and the 90-day window is short enough that the pre-existing condition lookback is unlikely to matter. Short-term wins for his specific scenario.

Get a Short-Term Texas Plan Quote

A licensed Texas broker compares short-term plans from UnitedHealthcare Golden Rule, BCBSTX, Pivot Health, and Everest — with coverage exclusion analysis, deductible scenarios, and a check on whether a subsidized ACA marketplace plan would actually deliver better total value. Free, no obligation.

Texas Allows 36-Month Short-Term Plans

Texas is one of the most permissive states for short-term health insurance duration, allowing STLD plans up to 36 months — the federal maximum. California bans short-term entirely; New York caps at 3 months; Colorado at 6 months. In Texas, a 30-year-old in Austin or Dallas can hold a UnitedHealthcare Golden Rule STLD plan at approximately $120–$155/month for up to 36 cumulative months, issuing in 30-day, 90-day, 6-month, or 12-month increments with renewals to the limit.

The 36-month rule is a function of federal STLD regulations restored during the Trump administration’s 2018 rule changes, which Texas adopted in full. Under federal rules administered by the Centers for Medicare & Medicaid Services (CMS), states can permit short-term plans up to 12 months initial duration with up to 24 additional months of renewal — a cumulative 36 months. Texas adopts the federal maximum without further state restriction, making it among the most STLD-friendly markets in the country. California bans short-term plans entirely; New York limits duration to 3 months; Colorado caps at 6 months — residents of those states who move to Texas regain access to full 36-month STLD coverage under TDI licensing.

The practical implication is that a Texan in Houston or Fort Worth facing a long gap — say, a 2-year contract-to-perm employment period or an early retirement bridge to Medicare — can stack short-term coverage from UnitedHealthcare Golden Rule or Everest through the full 36 months at roughly $120–$250/month depending on age and tier. However, the 36-month limit applies per insured individual, not per plan. A Texan who enrolled in a 12-month STLD plan in January 2024 has used 12 months of the 36-month total — they have 24 months remaining if they want to renew or switch to a Pivot Health or BCBSTX plan. Once cumulative duration hits 36 months, the insured must transition to ACA-compliant coverage through HealthCare.gov. The Texas Department of Insurance (TDI) tracks STLD enrollment, complaints, and rate filings for all Texas-licensed STLD carriers.

Texas Short-Term Carriers Compared

Five carriers dominate short term health insurance Texas availability in 2026: UnitedHealthcare Golden Rule, BCBSTX, Pivot Health, Everest, and Independence American Insurance — all TDI-licensed with annual rate filings. Golden Rule Standard plans run approximately $120–$155/month for a 30-year-old across all 26 Texas rating areas; Pivot Health Basic plans start around $90–$110/month in Houston and Dallas-Fort Worth; BCBSTX STLD runs $30–$70 above Golden Rule with Memorial Hermann and Baylor Scott & White in-network access.

UnitedHealthcare (Golden Rule)

National / LargestUnitedHealthcare’s Golden Rule subsidiary is the largest STLD carrier nationally and the most common choice for Texas short-term buyers. Plans are available across all 26 Texas rating areas with flexible duration options (30-day, 90-day, 6-month, 12-month increments). Network access piggybacks on UHC’s Choice Plus PPO infrastructure, providing broader provider reach than smaller STLD carriers. Standard pre-existing condition lookback is 12 months.

- National scale / largest STLD carrier

- UHC Choice Plus network access

- 12-month pre-existing lookback

- Statewide Texas availability

Blue Cross Blue Shield of Texas (BCBSTX)

Texas / Network breadthBCBSTX offers STLD plans across Texas with the broadest provider network — same hospital system access as marketplace BCBSTX plans (Memorial Hermann, Houston Methodist, Baylor Scott & White, Texas Health Resources, HCA Healthcare). Premium runs $30–$70 higher than UnitedHealthcare Golden Rule but the network depth means in-network access is rarely a problem. 24-month pre-existing condition lookback is stricter than some competitors.

- HCSC Texas Blues

- Broadest Texas hospital network

- Higher STLD premium

- 24-month pre-existing lookback

Pivot Health

Low-cost / FlexiblePivot Health is a Phoenix-based STLD carrier with competitive premium across most Texas metros. Strong fit for younger Texans prioritizing lowest monthly cost. Pivot’s product line includes multiple deductible tiers and add-on rider options (accidental injury, telehealth, prescription discount cards). Network access is narrower than BCBSTX or UHC Golden Rule — verify in-network status of any preferred Texas provider before enrolling.

- Lowest premium tier

- Multiple deductible options

- Optional rider add-ons

- Narrower provider network

Everest Reinsurance / Everest Re Group

Customizable / NicheEverest’s Texas STLD products focus on customizable deductible structures with higher lifetime caps than basic plans — up to $2 million on enhanced tiers. Stronger fit for older Texans (45–64) bridging to Medicare or buyers wanting more comprehensive interim coverage. Premium typically falls between Pivot and BCBSTX. Pre-existing condition lookback is 24 months standard.

- Customizable deductibles

- Higher $2M lifetime caps

- Pre-Medicare gap specialist

- 24-month pre-existing lookback

Independence American Insurance

Smaller carrier / NicheIndependence American is a smaller niche STLD carrier with Texas presence in select rating areas. Plans target healthy adults with low expected utilization at competitive premium. Network access varies by metro and is generally narrower than UHC or BCBSTX. Best fit when Pivot Health is unavailable in a specific Texas rating area or when premium quote comparisons show meaningful savings.

- Niche / smaller scale

- Competitive premium

- Variable metro availability

- Narrower provider network

Texas Department of Insurance Oversight

Reminder / TDI oversightAll Texas STLD carriers file rates annually with the Texas Department of Insurance and are subject to TDI complaint review and market conduct examination. The TDI consumer portal publishes carrier complaint indices and rate filings — useful for comparing carriers beyond marketing materials. STLD carriers in Texas must also comply with federal rules limiting duration to 36 months cumulative per insured.

- TDI rate filing oversight

- Quarterly complaint index publication

- 36-month federal duration cap

- Same regulatory body as ACA carriers

Short-Term vs Catastrophic vs Marketplace in Texas

For Texans choosing between short term health insurance Texas plans, ACA catastrophic plans, and marketplace Bronze coverage, the decision depends on age, income, expected utilization, and gap duration. Short-term wins on monthly premium but loses on coverage scope. Catastrophic is ACA-compliant but requires under-30 age or hardship exemption. Bronze with subsidies often beats both on net cost for subsidy-eligible Texans below 400% FPL.

Short-term — Best for healthy gap-coverage scenarios

A 32-year-old Dallas IT contractor between jobs for 3 months chooses a $130/mo Pivot Health STLD plan. Healthy, no chronic conditions, no anticipated medical needs — the $390 total cost beats $880 quarterly COBRA premium with comparable network access for routine care. Maternity, mental health, and pre-existing exclusions don’t matter because none apply. Best fit: healthy adults, predictable gap, no anticipated claims.

Catastrophic — Better than short-term when age qualifies

A 27-year-old Austin software developer above the 400% FPL subsidy ceiling chooses ACA catastrophic at $230/mo over short-term at $170/mo. The $60/mo premium gap pays for ACA-compliant coverage including maternity, mental health, prescriptions, and unlimited lifetime maximum — protection short-term doesn’t provide. Best fit: under-30 Texans willing to trade $60–$100 monthly for ACA-compliant protection.

Bronze with APTC — Best for subsidy-eligible Texans

A 35-year-old Houston nurse earning $42,000 (about 280% FPL) qualifies for substantial APTC on Bronze, reducing the $330/mo Bronze premium to $110/mo after subsidies. Same plan, dramatically lower cost than short-term’s $140/mo Standard tier — plus ACA-compliant coverage. Best fit: subsidy-eligible Texans regardless of age, willing to enroll during open enrollment or a qualifying SEP.

COBRA — The expensive but seamless option

A 50-year-old Plano executive laid off with ongoing prescription medications and a recent specialist relationship pays $920/mo for COBRA continuation rather than $250/mo short-term — COBRA preserves the existing plan, network, deductible accumulation, and pre-existing condition coverage. Short-term’s pre-existing exclusion would deny coverage for the ongoing condition. Best fit: Texans with active claims or pre-existing conditions valuing continuity over premium savings.

Frequently Asked Questions

Common questions from Texas short-term buyers cover the 36-month TDI-regulated duration limit, what UnitedHealthcare Golden Rule and Pivot Health exclude versus HealthCare.gov Bronze plans from Ambetter and BCBSTX, 2026 premium ranges ($90–$250/month at age 30 across Harris County, Tarrant County, and Travis County), which gap scenarios actually justify short-term over subsidized ACA marketplace coverage, and whether Texas residents can enroll year-round without an open enrollment window.

How long can a short-term health plan last in Texas?

Texas allows short-term limited-duration insurance plans up to 36 months total, including renewals — the maximum permitted under current federal rules. This contrasts with states like California, New York, and Colorado that either ban short-term plans entirely or restrict duration to 90 days or less. Texas STLD plans typically issue in 30-day, 90-day, 6-month, or 12-month increments, with the option to renew up to the cumulative 36-month limit. After 36 months, a Texas resident must transition to ACA-compliant coverage through HealthCare.gov or off-exchange. The 36-month limit applies per insured individual, not per plan.

What does short-term health insurance in Texas not cover?

Short-term health insurance Texas plans are NOT ACA-compliant and typically exclude maternity care, prescription drug coverage at meaningful levels, mental health and substance use treatment, pre-existing conditions (with a 12-24 month lookback period in most plans), preventive care without cost-sharing, and pediatric dental and vision. Coverage limits are usually capped at $1 million to $2 million lifetime versus the ACA’s unlimited annual and lifetime maximums. Many short-term plans also exclude or severely limit physical therapy, durable medical equipment, organ transplants, and certain specialist care. Read the policy summary carefully before enrolling — exclusions vary significantly by carrier.

How much does Texas short-term health insurance cost in 2026?

Short-term plan premiums in Texas for 2026 typically run $90 to $250 per month for a 30-year-old non-smoker, with rate variation by carrier, deductible selection, and applicant health status. UnitedHealthcare (Golden Rule), BCBSTX, Pivot Health, and Everest are the largest STLD carriers serving Texas. Premiums increase significantly with age — a 55-year-old typically pays $200 to $450 per month for equivalent coverage. Unlike ACA marketplace plans, short-term plans are medically underwritten, meaning carriers can deny coverage or charge higher rates based on health history. Advanced Premium Tax Credit subsidies do not apply to short-term plans.

Who should consider Texas short-term health insurance?

Short-term health insurance Texas plans work for healthy adults bridging brief coverage gaps with no anticipated medical needs — between job loss and a new employer plan starting date, after COBRA expires before ACA open enrollment, waiting for Medicare eligibility, recent college graduates aging off parental coverage, and gig workers between contracts who don’t qualify for ACA subsidies. Short-term should NOT replace ACA-compliant coverage for households with chronic conditions, planned pregnancies, ongoing prescriptions, mental health treatment needs, or pre-existing conditions — the exclusions and lifetime caps create significant financial exposure on a single qualifying event.

Can I buy short-term health insurance in Texas anytime?

Yes. Short-term health insurance Texas plans are available year-round with no open enrollment restriction, unlike HealthCare.gov ACA plans which are limited to the November 1 through January 15 open enrollment window or qualifying special enrollment periods. Most Texas short-term plans can issue an effective date as quickly as the day after application approval, making them useful for immediate coverage needs. The trade-off: short-term carriers medically underwrite each application, so denial or higher rates based on health history are possible. The Texas Department of Insurance regulates short-term carrier filings, rate adequacy, and consumer complaints.

Compare 2026 Short-Term Texas Plans

A licensed Texas broker compares short-term plans from UnitedHealthcare Golden Rule, BCBSTX, Pivot Health, Everest, and Independence American — with coverage exclusion analysis, deductible scenarios, and a check on whether subsidized ACA marketplace coverage would deliver better total value. Free, no obligation.

Free Texas short-term comparison — bridge coverage strategy in one call.

Explore Texas Coverage In Depth

Statewide overview of Texas health insurance — marketplace, Medicaid, and off-exchange options compared.

Texas Marketplace EnrollmentHealthCare.gov enrollment guide for Texas — APTC subsidies, open enrollment, and SEPs.

Individual Texas Health InsuranceIndividual plan options — marketplace, off-exchange PPO, and direct carrier enrollment.

Texas PPO PlansOff-exchange PPO for Texans above subsidy ceilings — BCBSTX, Cigna, and UnitedHealthcare compared.

Self-Employed Texas Health Insurance1099 contractors and freelancers — HealthCare.gov subsidies, HSA-HDHP, and Schedule 1 deduction.

Cheap Texas Health InsuranceLowest-cost Texas plans — subsidized Bronze and Silver, CHIP, and affordability by income tier.

Catastrophic Texas Health InsuranceUnder-30 and hardship exemption plans — ACA-compliant alternative to short-term coverage.

Private Texas Health InsuranceOff-exchange private coverage for Texans above ACA subsidy thresholds.

Family Texas Health InsuranceFamily coverage strategies — CHIP, marketplace plans, and bridge coverage for dependents.

Texas Retiree Health InsurancePre-Medicare bridge ages 55–64 — TRS-Care, ERS, APTC subsidies, COBRA vs marketplace.

Texas Small Business Health InsuranceGroup plans for 1–50 employees — PPO, HMO, SHOP, and ICHRA options compared.

National PPO Health Insurance PlansNationwide PPO guidance applying across all 50 states — carriers, networks, and rate structures.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Texas residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.