Private Health Insurance Texas 2026: Individual Plans

Private health insurance Texas plans for 2026 are available through two channels: HealthCare.gov for ACA-compliant coverage with Advanced Premium Tax Credit subsidies, and off-exchange directly from carriers including BCBSTX, Cigna, and UnitedHealthcare. Texas uses the federal marketplace rather than a state-based exchange, and roughly 3.2 million Texans enrolled in private marketplace plans for 2026 coverage. Subsidized on-exchange Silver plans average $67 monthly for qualifying enrollees; off-exchange private PPO plans run $510–$1,000+ monthly for the same age.

What brings you here today?

What Private Health Insurance Means in Texas

Private health insurance Texas refers to individually purchased coverage not tied to an employer — spanning HealthCare.gov plans from Ambetter, BCBSTX, and Oscar Health, and off-exchange plans from BCBSTX, Cigna, and UnitedHealthcare. Texas runs on the federal exchange across 26 rating areas, and with 3.2 million marketplace enrollees for 2026 — the largest state total nationally — Texas is the country’s biggest private individual insurance market.

The term “private health insurance Texas” covers a wide spectrum. At one end, a Dallas professional buying a subsidized BCBSTX Silver plan on HealthCare.gov is purchasing private insurance — the plan is issued by a private carrier, not the government, and the ACA subsidy is a tax credit applied at enrollment. At the other end, a Houston business owner buying a Cigna off-exchange PPO plan directly from the carrier with no government interaction is also buying private health insurance Texas coverage. The distinction that matters financially is not whether the coverage is “private” but whether it’s enrolled on-exchange (APTC-eligible) or off-exchange (full premium, no subsidy).

Texas’s scale makes the private individual market structurally important nationally. With roughly 29 million residents and the highest uninsured rate of any U.S. state — approximately 5 million uninsured according to U.S. Census Bureau American Community Survey data — Texas accounts for a disproportionate share of national marketplace enrollment growth. The Centers for Medicare & Medicaid Services reported that Texas had the highest marketplace enrollment of any state for the 2026 open enrollment period, driven by expanded subsidy availability. Private health insurance Texas enrollment is concentrated in the Dallas-Fort Worth, Houston, Austin, and San Antonio metros, which account for roughly 65% of statewide ACA enrollment.

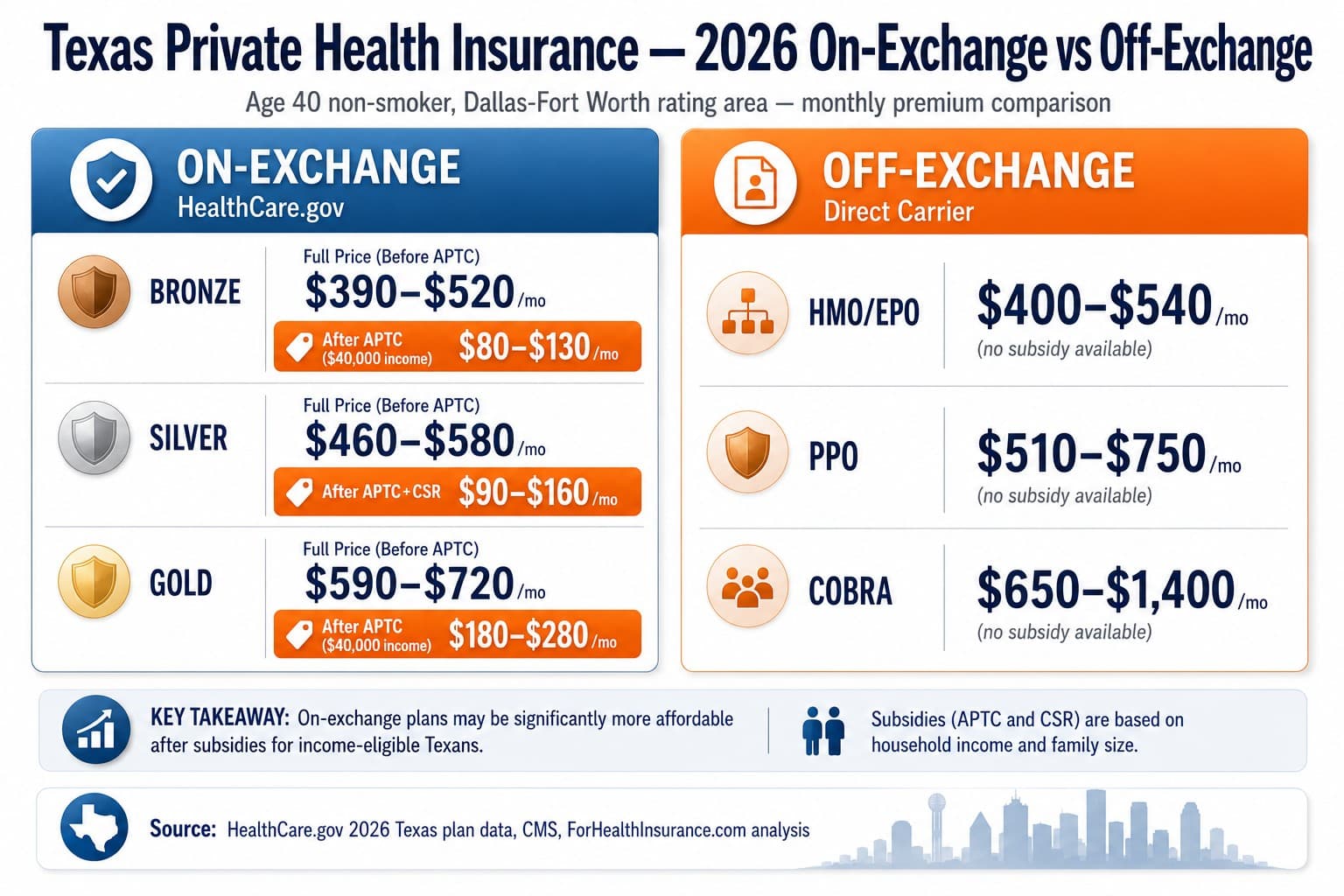

On-Exchange vs Off-Exchange Private Coverage

Texas private health insurance buyers choosing between HealthCare.gov on-exchange and off-exchange direct carrier enrollment face one core question: does the household qualify for Advanced Premium Tax Credit subsidies? Subsidy-eligible households (100%–400% FPL) almost always get better value on-exchange. Households above the subsidy ceiling — above $60,240 single or $124,800 family of four for 2026 — get identical coverage either channel, but off-exchange adds PPO access not available on HealthCare.gov in Texas.

On-exchange private health insurance Texas enrollment means purchasing through HealthCare.gov during the November 1 through January 15 open enrollment window or within 60 days of a qualifying special enrollment period event. The critical advantage: APTC subsidies that reduce monthly premium by $200–$600+ for qualifying households. Texas marketplace enrollees receive an average subsidy of $667 per month according to CMS 2026 enrollment data. The disadvantage for some Texans: HealthCare.gov in Texas offers only HMO and EPO plan types — no individual PPO plans. Texans who need PPO network access and out-of-network coverage cannot get it on HealthCare.gov in Texas.

Off-exchange private health insurance Texas enrollment means purchasing directly from a carrier — BCBSTX, Cigna, UnitedHealthcare, Aetna, Humana — or through a licensed broker who submits an application directly to the carrier. The carrier issues the policy without HealthCare.gov involvement. The advantage: broader plan selection including PPO products, year-round enrollment availability, and sometimes faster effective dates. The disadvantage: no APTC or CSR subsidy eligibility, meaning full-price premium applies regardless of income. For subsidy-eligible Texans, off-exchange typically costs $3,000–$8,000 more annually than equivalent on-exchange coverage.

The on-exchange vs off-exchange decision rule for Texas

If your projected 2026 household income is below $60,240 (single adult) or $124,800 (family of four at 400% of federal poverty level), enroll on HealthCare.gov — the APTC subsidy almost always outweighs the PPO trade-off. If your income is above those thresholds, off-exchange is worth comparing: you’ll pay full premium either channel, but off-exchange unlocks PPO products from BCBSTX, Cigna, and UnitedHealthcare that HealthCare.gov Texas doesn’t offer. This income-driven decision rule applies to over 95% of Texas private health insurance buyers.

What Private Health Insurance Costs in Texas for 2026

Private health insurance Texas premiums in 2026 vary by age, plan tier, rating area, and subsidy eligibility. A 40-year-old non-smoker pays full-price monthly premiums of $390–$520 for Bronze, $460–$580 for Silver, and $590–$720 for Gold before APTC. After subsidies, a 40-year-old earning $40,000 typically pays $80–$160 monthly for Silver. Texas has 26 geographic rating areas — Dallas-Fort Worth generally sees mid-range premiums among major Texas metros.

| Texas Private Plan Type | Monthly Premium (age 40, pre-subsidy) | Subsidy Eligible? | Best Fit For |

|---|---|---|---|

| On-exchange Bronze (HealthCare.gov) | $390–$520/mo | Yes — APTC applies | Subsidy-eligible, low utilization |

| On-exchange Silver + CSR (HealthCare.gov) | $460–$580/mo (pre-subsidy) | Yes — APTC + CSR | 138%–250% FPL, best total value |

| On-exchange Gold (HealthCare.gov) | $590–$720/mo (pre-subsidy) | Yes — APTC applies | Higher utilization, lower deductible |

| Off-exchange ACA HMO/EPO (direct carrier) | $400–$540/mo | No | Above-subsidy income, HMO network ok |

| Off-exchange PPO (direct carrier) | $510–$1,000+/mo | No | Above-subsidy income, PPO access needed |

| Off-exchange COBRA continuation | $650–$1,400+/mo | No | Pre-existing conditions, active claims |

Private health insurance Texas costs are also shaped by the state’s 26-rating-area structure — one of the most fragmented geographic rating systems in the country. Dallas-Fort Worth and Houston tend to see mid-range private premiums among Texas metros; Austin runs slightly higher for off-exchange products. Rural West Texas and the Rio Grande Valley typically carry the highest full-price premiums due to thinner provider networks and higher local claims experience. The rate variation means a Texan comparing private insurance Texas quotes should always use their specific zip code rather than statewide averages.

Example: Austin Software Engineer, Age 35 — On-Exchange vs Off-Exchange Decision

A 35-year-old software engineer in Travis County leaves a tech employer to go independent. His projected 2026 net Schedule C income is $68,000 — above the $60,240 single-adult APTC ceiling, so no HealthCare.gov subsidy applies. His options: an Ambetter Silver EPO on HealthCare.gov at full price runs approximately $545/month. A BCBSTX Blue Advantage PPO off-exchange runs approximately $820/month — $275/month more but includes out-of-network coverage and no referrals for specialist care at Seton Medical Center Austin (now Ascension Seton) or St. David’s. He also evaluates a BCBSTX Silver EPO off-exchange at $590/month — almost identical to the marketplace Silver but off-exchange, meaning it’s available year-round and doesn’t require HealthCare.gov enrollment. He chooses the off-exchange Silver EPO, saving $230/month versus the PPO while gaining year-round enrollment flexibility.

Get a Private Texas Health Insurance Quote

A licensed Texas broker compares on-exchange HealthCare.gov plans with off-exchange private options from BCBSTX, Cigna, and UnitedHealthcare — with full APTC subsidy calculation, provider verification, and on-exchange vs off-exchange cost modeling. Free, no obligation.

Texas Private Health Insurance Carriers for 2026

Texas private individual health insurance is available from four primary carriers on HealthCare.gov — BCBSTX, Ambetter, Oscar Health, and UnitedHealthcare — plus additional off-exchange options including Cigna, Humana, and regional carriers. BCBSTX dominates statewide with the broadest network, Ambetter leads on lowest on-exchange premium, and Cigna leads off-exchange PPO for above-subsidy households. Carrier availability varies by Texas rating area.

Blue Cross Blue Shield of Texas (BCBSTX)

On + off exchange / DominantBCBSTX is the dominant private health insurance Texas carrier in both the on-exchange marketplace and off-exchange direct markets. Statewide presence across all 26 rating areas, deepest provider contracting at Memorial Hermann, Houston Methodist, Baylor Scott & White, Texas Health Resources, and HCA Healthcare. On-exchange Silver and Bronze plans are the most common choice for subsidy-eligible Texans; off-exchange PPO plans serve higher-income households. BlueCard national reciprocity for off-exchange members.

- On-exchange and off-exchange products

- Broadest statewide network

- HCSC parent / Texas Blues

- BlueCard off-exchange reciprocity

Ambetter (Centene)

On-exchange / Lowest premiumAmbetter is Centene’s Texas marketplace brand and the dominant low-premium on-exchange private health insurance Texas option. Consistently lower Bronze and Silver premiums than BCBSTX across most Texas rating areas — the go-to choice for CSR-eligible Silver plans below 250% FPL. Network is narrower than BCBSTX, particularly in rural Texas, but adequate across Houston, Dallas-Fort Worth, Austin, and San Antonio metros. On-exchange only.

- On-exchange only

- Lowest on-exchange premium

- CSR Silver specialist

- Major metro network

Oscar Health

On-exchange / DigitalOscar’s on-exchange private plans are available in Houston, Dallas-Fort Worth, Austin, and San Antonio with digital member tools, 24/7 telehealth, and a concierge care team. Premium sits between Ambetter and BCBSTX. Strong fit for younger, digitally native Texas private insurance buyers who value app-based member management and integrated telehealth. Oscar contracts with major metro hospital systems but network is narrower than BCBSTX.

- Major Texas metros only

- Digital-first member experience

- Integrated telehealth

- Mid-range on-exchange premium

Cigna

Off-exchange / PPO leaderCigna’s Open Access Plus PPO is the leading off-exchange private health insurance Texas choice for above-subsidy households who need PPO flexibility. Available in Houston, Dallas-Fort Worth, Austin, and San Antonio metros with strong national reciprocity for Texans who travel or work across state lines. Off-exchange only in Texas — Cigna exited the Texas HealthCare.gov marketplace — making it a direct-carrier enrollment product through brokers.

- Off-exchange PPO only

- Strong national reciprocity

- Major Texas metros

- Above-subsidy income focus

UnitedHealthcare

On + off exchange / NationalUnitedHealthcare participates in select Texas HealthCare.gov rating areas and offers off-exchange Choice Plus PPO products statewide through brokers. On-exchange availability is more limited than BCBSTX or Ambetter — verify availability for your specific Texas rating area before comparing. Off-exchange UHC Choice Plus PPO carries the broadest national network of any Texas private health insurance carrier, a key differentiator for Texans who travel frequently or have multi-state care needs.

- Select rating areas on-exchange

- Choice Plus PPO off-exchange

- Broadest national network

- Strong multi-state reciprocity

Aetna

On-exchange / Select metrosAetna exited the individual health insurance market in Texas entirely at the end of 2025 — including both on-exchange HealthCare.gov plans and off-exchange individual enrollment. For 2026, Aetna is not available for individual private health insurance Texas enrollment. Aetna continues to operate through employer group plans and Medicare Advantage in Texas. Texans comparing individual coverage should focus on BCBSTX, Ambetter, Oscar, and UnitedHealthcare.

- Select rating area availability

- CVS/MinuteClinic integration

- Mid-range on-exchange premium

- Employer-focused off-exchange

Private vs Employer-Sponsored vs COBRA in Texas

Texas residents choosing between private individual coverage, continuing employer-sponsored insurance through COBRA, and returning to a new employer plan face a cost-and-continuity trade-off. COBRA preserves existing coverage but typically costs $650–$1,400+ monthly with no subsidies. Private on-exchange coverage replaces COBRA with ACA-compliant alternatives at potentially lower net cost for subsidy-eligible Texans. Private off-exchange preserves PPO access but at full premium.

Private on-exchange — Best for subsidy-eligible post-COBRA

A 38-year-old Dallas professional laid off from a job with a $1,100/month COBRA premium qualifies for APTC subsidies at $52,000 annual income (about 347% FPL). An on-exchange BCBSTX Silver plan drops to roughly $130/month after APTC — saving $11,640 annually versus COBRA continuation. The trade-off: switching networks and losing mid-year deductible accumulation. For above-subsidy households, COBRA’s seamless continuity is worth the premium premium.

Private off-exchange PPO — Best for above-subsidy, PPO-dependent

A 42-year-old Houston consultant earning $180,000 (well above the 400% FPL subsidy ceiling) has active specialist relationships at Memorial Hermann and a chronic condition requiring regular specialist visits without referrals. COBRA at $1,350/month preserves the current plan; a Cigna off-exchange PPO at $720/month replaces it with comparable in-network access and out-of-network flexibility at $7,560 in annual savings. Suitable when the specific providers are in the Cigna network.

COBRA continuation — Best for active claims or pre-existing conditions

A 45-year-old Austin marketing director recently diagnosed with a condition requiring ongoing specialist care is mid-treatment and has met $4,500 of the year’s deductible. Switching private insurance Texas plans mid-year resets the deductible. COBRA at $1,200/month preserves mid-year accumulation and current provider relationships — the premium difference pays for itself if treatment is ongoing. COBRA is generally the right choice when switching plans would reset deductible progress or disrupt active treatment.

New employer plan — Almost always best if available

A 36-year-old San Antonio professional with a new job offering a $280/month employer-sponsored plan (employer pays $600, employee pays $280) faces a straightforward decision: a $280 employer plan beats a $150 subsidized private marketplace plan when the employer contribution is factored in as total compensation. Declining employer coverage to enroll on HealthCare.gov forfeits the employer’s contribution — almost always a net financial loss unless the marketplace plan delivers significantly better network or coverage value.

How to Enroll in Private Health Insurance in Texas

Enrolling in private health insurance Texas requires choosing between HealthCare.gov (open November 1–January 15 for Ambetter, BCBSTX, and Oscar on-exchange plans) and direct enrollment for off-exchange BCBSTX, Cigna, or UHC products available year-round. Harris County, Travis County, and Bexar County residents apply through the same federal portal; off-exchange enrollment goes directly to the carrier or a licensed Texas broker.

For on-exchange private health insurance Texas enrollment, the process begins at HealthCare.gov — the only legitimate marketplace for Texas ACA-compliant coverage. Texas residents create an account, enter household income and composition, and receive real-time APTC calculations before selecting a plan. The enrollment portal automatically screens for Medicaid eligibility; Texans below 100% of federal poverty level are typically redirected (though the Texas Medicaid coverage gap means most childless adults won’t qualify). Open enrollment runs November 1 through January 15 for the following year’s coverage — plans selected by December 15 take effect January 1; plans selected between December 16 and January 15 take effect February 1.

For off-exchange private health insurance Texas enrollment, the application goes directly to BCBSTX, Cigna, UnitedHealthcare, or Humana — through the carrier’s website or a licensed Texas broker. Most off-exchange carriers issue a first-of-the-month effective date when the application is submitted by the 15th of the prior month, making mid-year enrollment straightforward. ACA-compliant off-exchange plans must accept any Texas applicant regardless of health status. The Texas Department of Insurance (TDI) licenses all private health insurance Texas carriers and publishes quarterly complaint indices for BCBSTX, Cigna, and UHC — a useful benchmark when comparing carrier service quality before enrolling.

Frequently Asked Questions

Common questions from Texas private insurance buyers cover whether to enroll through HealthCare.gov with Ambetter or Oscar versus off-exchange with BCBSTX or Cigna, what the $60,240 single-adult APTC ceiling means for Harris County and Travis County residents, 2026 premium ranges ($390–$820/month by tier and rating area), how off-exchange year-round enrollment compares to HealthCare.gov’s November–January window, and which carriers accept applications mid-year.

What is private health insurance in Texas?

Private health insurance Texas refers to individual or family health coverage purchased directly from a carrier or through a licensed broker, as opposed to employer-sponsored group coverage or government programs like Medicaid or Medicare. In Texas, private individual health insurance is available through two main channels: HealthCare.gov (the federal marketplace, where ACA-compliant plans qualify for Advanced Premium Tax Credit subsidies) and off-exchange directly from carriers such as BCBSTX, Cigna, and UnitedHealthcare. Both channels offer ACA-compliant private coverage — the difference is subsidy eligibility, which requires HealthCare.gov enrollment. Texas does not operate a state-based exchange; HealthCare.gov is the only marketplace option.

What is the difference between on-exchange and off-exchange private health insurance in Texas?

On-exchange private health insurance Texas plans are purchased through HealthCare.gov and may qualify for Advanced Premium Tax Credit subsidies that reduce monthly premium — available to households earning between 100% and 400% of federal poverty level (up to $60,240 single or $124,800 family of four in 2026). Off-exchange plans are purchased directly from a carrier — BCBSTX, Cigna, UnitedHealthcare, Humana — and do not qualify for APTC subsidies. The coverage is ACA-compliant on both channels. The practical consequence: Texans who qualify for APTC should almost always enroll on-exchange to capture subsidies that can reduce monthly premium by $200–$600 per month. Texans above the subsidy ceiling get no benefit from on-exchange enrollment and may prefer off-exchange for broader plan selection, including PPO products not sold on HealthCare.gov.

How much does private health insurance cost in Texas for 2026?

Private health insurance Texas costs in 2026 vary significantly by age, plan tier, rating area, and subsidy eligibility. A 40-year-old non-smoker can expect full-price monthly premiums of $390–$520 for Bronze, $460–$580 for Silver, and $590–$720 for Gold on HealthCare.gov before subsidies. After Advanced Premium Tax Credit, a 40-year-old earning $40,000 (about 267% of federal poverty level) typically pays $80–$160 monthly for Silver coverage. Off-exchange PPO plans for the same age run $510–$1,000+ monthly for equivalent coverage depending on tier. Texas operates 26 geographic rating areas — Houston, Dallas-Fort Worth, and Austin generally see lower premiums than rural West Texas or the Rio Grande Valley.

Can I buy private health insurance in Texas outside of open enrollment?

Outside of HealthCare.gov’s November 1 through January 15 open enrollment window, Texans can enroll in private on-exchange coverage only through a qualifying Special Enrollment Period triggered by a life event — job loss, marriage, divorce, birth, adoption, moving to a new rating area, or losing other coverage. SEP enrollment must be completed within 60 days of the qualifying event. Off-exchange ACA-compliant plans and off-exchange PPO plans are available year-round with no open enrollment restriction — carriers can issue an effective date any month of the year. Short-term limited-duration plans are also available year-round but are not ACA-compliant. The Texas Department of Insurance oversees private individual insurance carrier filings and consumer complaints.

Which carriers offer private individual health insurance in Texas?

Texas private individual health insurance is available from Blue Cross Blue Shield of Texas (BCBSTX), Ambetter (Centene), Oscar Health, Aetna, and UnitedHealthcare on HealthCare.gov, with availability varying by rating area. Off-exchange, BCBSTX, Cigna, UnitedHealthcare, and Humana offer individual ACA-compliant and non-compliant PPO products directly through carriers or licensed brokers. Note: Aetna exited the individual market in Texas at the end of 2025 and is no longer available for individual off-exchange enrollment in 2026. BCBSTX is the dominant private individual carrier in Texas with statewide presence on-exchange and off-exchange, contracting with Memorial Hermann, Houston Methodist, Baylor Scott & White, Texas Health Resources, and HCA Healthcare. Ambetter leads on lowest on-exchange Bronze premium in most Texas rating areas.

Compare 2026 Private Texas Health Insurance

A licensed Texas broker models on-exchange HealthCare.gov options against off-exchange private plans from BCBSTX, Cigna, and UnitedHealthcare — with APTC subsidy calculation, provider network verification, and on-exchange vs off-exchange cost comparison built in. Free, no obligation.

Free Texas private insurance comparison — on-exchange and off-exchange in one call.

Explore Texas Coverage In Depth

Statewide overview of Texas health insurance — marketplace, Medicaid, and off-exchange options compared.

Texas Marketplace EnrollmentHealthCare.gov enrollment guide for Texas — APTC subsidies, open enrollment, and SEPs.

Individual Texas Health InsuranceIndividual plan options — marketplace, off-exchange PPO, and direct carrier enrollment.

Texas PPO PlansOff-exchange PPO for Texans above subsidy ceilings — BCBSTX, Cigna, and UnitedHealthcare compared.

Self-Employed Texas Health Insurance1099 contractors and freelancers — HealthCare.gov subsidies, HSA-HDHP, and Schedule 1 deduction.

Cheap Texas Health InsuranceLowest-cost Texas plans — subsidized Bronze and Silver, CHIP, and affordability by income tier.

Catastrophic Texas Health InsuranceUnder-30 and hardship exemption plans — lowest ACA-compliant premium for eligible Texans.

Short-Term Texas Health InsuranceNon-ACA bridge coverage for Texans between employer plans or post-COBRA.

Family Texas Health InsurancePrivate family coverage — marketplace plans, off-exchange PPO, and CHIP for dependents.

Texas Retiree Health InsurancePre-Medicare bridge ages 55–64 — TRS-Care, ERS, APTC subsidies, COBRA vs marketplace.

Texas Small Business Health InsuranceGroup plans for 1–50 employees — PPO, HMO, SHOP, and ICHRA options compared.

National PPO Health Insurance PlansNationwide PPO guidance applying across all 50 states — carriers, networks, and rate structures.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Texas residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.