Family Health Insurance Texas 2026: Plans for Households

Family health insurance Texas options for 2026 center on three coverage paths: HealthCare.gov marketplace plans with household APTC and CSR subsidies, Texas CHIP for children under 19 in qualifying low-income families, and off-exchange plans for households above subsidy ceilings. A family of four earning $80,000 typically pays $300–$600 monthly for Silver marketplace coverage after subsidies; families with children below 200% FPL often save most by splitting coverage — CHIP for kids, marketplace for adults.

What brings you here today?

Texas Family Health Insurance Coverage Paths

Family health insurance Texas households navigate three primary coverage paths depending on income and household composition. Below 200% of federal poverty level, children qualify for Texas CHIP and adults qualify for heavily subsidized marketplace plans — split enrollment produces the lowest total household cost. Between 200% and 400% FPL, the full household enrolls in subsidized HealthCare.gov plans. Above 400% FPL, off-exchange direct carrier enrollment provides ACA-compliant coverage or PPO access without subsidy.

Texas family health insurance planning is more complex than single-adult coverage because household composition creates multiple eligibility pathways that don’t always point to the same plan. A family of four earning $65,000 might have children who qualify for Texas CHIP (below 200% FPL threshold of $62,400 for family of four) and adults who qualify for subsidized marketplace plans. Enrolling the children in CHIP and the adults in marketplace separately often produces lower total monthly cost than a single family marketplace plan covering everyone — because CHIP carries near-zero enrollment fees while marketplace family premiums scale with the number of covered members.

Texas’s Medicaid coverage gap complicates family coverage for the lowest-income households. Adults below 100% of federal poverty level fall into the gap — ineligible for Texas Medicaid (which covers adults only in very narrow categories) and ineligible for APTC subsidies on HealthCare.gov. Children in the same household below 200% FPL still qualify for CHIP regardless of adult eligibility — creating split-family situations where children have zero-cost CHIP and parents have no affordable coverage option. According to the Kaiser Family Foundation, Texas accounts for the largest share of family-level coverage gap households nationally.

Texas CHIP and the Split-Enrollment Strategy

Texas CHIP covers children under 19 in families seeking family health insurance Texas coverage below 200% of federal poverty level ($62,400 for a family of four in 2026) at near-zero cost — no monthly premium below 150% FPL, and a $35–$50 annual enrollment fee between 150% and 200% FPL. The split-enrollment strategy — CHIP for children, HealthCare.gov for adults — often produces the lowest total household monthly cost for qualifying Texas families.

The CHIP split-enrollment strategy works because the APTC subsidy for adults on HealthCare.gov is calculated based on total household income regardless of whether children are enrolled in CHIP or the marketplace. A Texas family of four with two adults earning $55,000 total qualifies for APTC on adult marketplace plans at roughly $200–$400 monthly combined after subsidy — meanwhile, the two children enroll in CHIP at $0–$50 per year enrollment fee. Total household coverage cost: roughly $200–$400 monthly for the adults plus near-zero for the children. If the same family enrolled everyone in a single HealthCare.gov family plan, the total marketplace premium after APTC would typically be $350–$600 monthly — more expensive than the split strategy.

Apply for Texas CHIP through YourTexasBenefits.com — the same portal handles CHIP, Medicaid, SNAP, and TANF applications simultaneously. HealthCare.gov also screens for CHIP eligibility during marketplace plan selection; families entering children on the HealthCare.gov application are automatically routed to CHIP if income qualifies. CHIP enrollment is year-round with no open enrollment window, and renewal happens annually with an eligibility review. CHIP covers all 10 ACA essential health benefits plus pediatric dental and vision care explicitly included — broader than the ACA minimum for adult marketplace plans.

CHIP age-out at 19 — what happens next

Children enrolled in Texas CHIP age out at 19 — their CHIP coverage ends at the end of the month they turn 19. Aging out of CHIP is a qualifying Special Enrollment Period event, giving the former CHIP enrollee a 60-day window to enroll in a HealthCare.gov marketplace plan. A 19-year-old transitioning off Texas CHIP can enroll in their own individual marketplace plan, join their parents’ existing marketplace plan as a dependent (if under 26), or enroll in an employer-sponsored plan if they have one. The SEP window begins on the date CHIP coverage ends — missing this window means waiting for the next open enrollment period.

Family Health Insurance Texas Costs for 2026

Family health insurance Texas premiums in 2026 depend on household size, adult ages, plan tier, rating area, and subsidy eligibility. A family of four — two adults age 40, two children — faces full-price Silver premiums of $1,400–$2,100 monthly before APTC. After subsidies, a family earning $80,000 typically pays $300–$600 monthly. The ACA caps family out-of-pocket exposure at $21,200 for 2026 for in-network covered services.

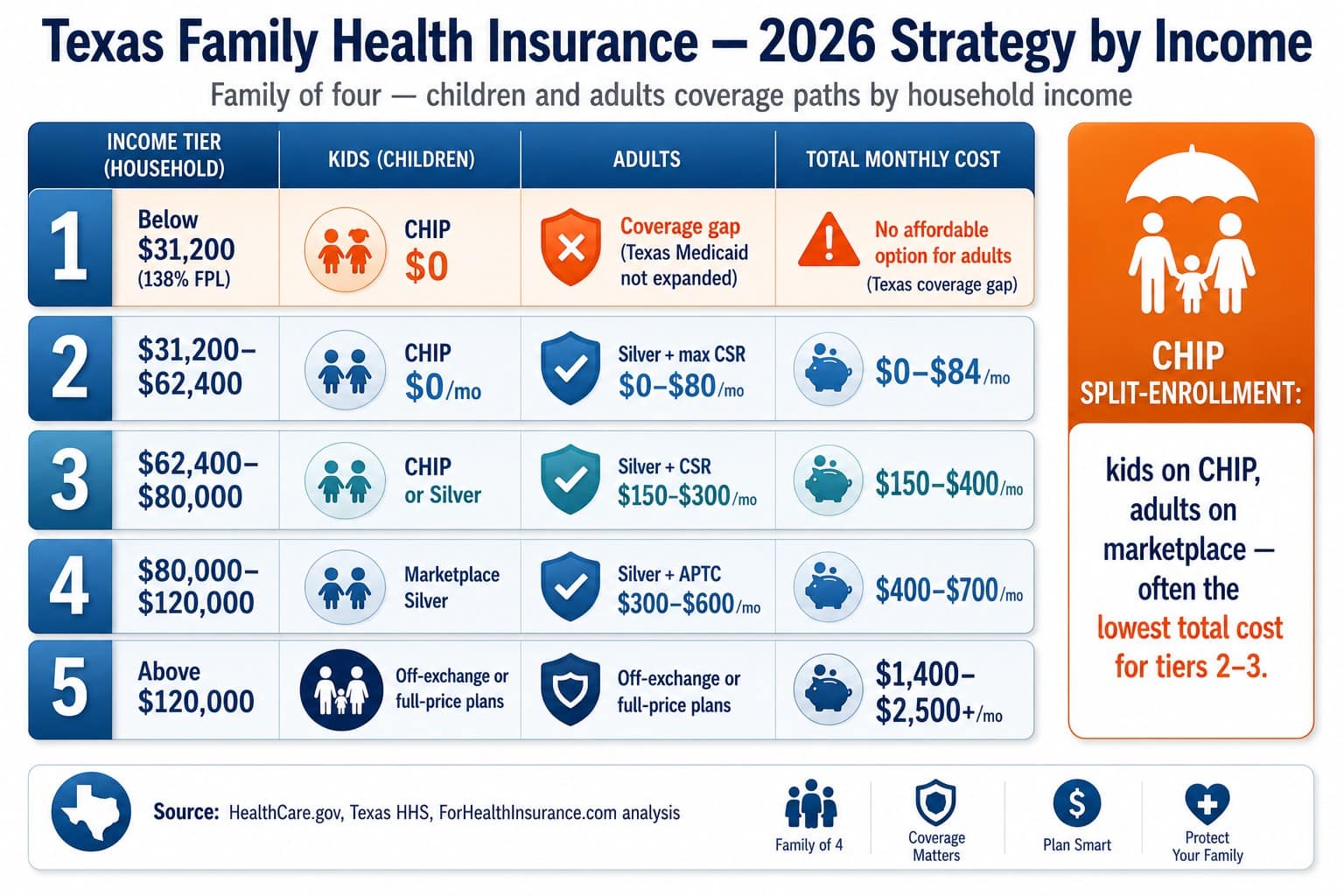

| Texas Family Income (family of 4) | Children’s Coverage | Adults’ Coverage | Typical Total Monthly Cost |

|---|---|---|---|

| Below $31,200 (138% FPL) | CHIP — $0/mo | Medicaid gap (adults uninsured) | $0 (children only) |

| $31,200–$62,400 (138%–200% FPL) | CHIP — $0–$4/mo | Silver + max CSR — $0–$80/mo adults | $0–$84/mo total |

| $62,400–$80,000 (200%–257% FPL) | Marketplace (Silver) or CHIP | Silver + CSR — $150–$300/mo adults | $150–$400/mo total |

| $80,000–$124,800 (257%–400% FPL) | Marketplace (Silver/Bronze) | Silver — $300–$600/mo adults | $400–$700/mo total |

| Above $124,800 (400%+ FPL) | Off-exchange or marketplace full-price | Full-price Gold or PPO | $1,400–$2,500+/mo total |

The ACA’s 3:1 age-band rating rule means children in a family plan are priced significantly lower than adults — typically at the lowest age-band rate. Adding two children to a Texas marketplace Silver plan typically increases monthly premium by $150–$300 total, versus $500–$800 for adding a second adult. This rating structure makes family plan premiums sensitive to adult ages: a 40-year-old parent pays substantially less than a 55-year-old parent for the same family plan. Texas operates 26 geographic rating areas — Austin (rating area 6), Houston (rating area 18), and Dallas-Fort Worth (rating area 8) generally see lower family health insurance Texas premiums than rural rating areas in West Texas and the Rio Grande Valley.

Example: McAllen Family of Four, Split-Enrollment Strategy

A McAllen (Hidalgo County) family of four — two parents aged 34 and 36, two children aged 6 and 9 — earns $52,000 annually in 2026, approximately 167% of the federal poverty level for a family of four. Both children qualify for Texas CHIP at this income level. CHIP enrollment costs $50/year total for both children with $3–$5 copays and no deductible. The parents enroll in an Ambetter Silver plan on HealthCare.gov. At 167% FPL, their Silver plan qualifies for Cost-Sharing Reduction: the deductible drops from approximately $5,500 to $700, and the out-of-pocket maximum falls to approximately $2,850. After their estimated $780/month APTC credit, their net premium is approximately $95/month. Total household coverage cost: approximately $1,190/year for the parents plus $50/year for both children via CHIP — compared to a full-price family Silver plan at approximately $1,680/month ($20,160/year) without subsidies.

Get a Texas Family Health Insurance Quote

A licensed Texas broker models CHIP eligibility for children, calculates APTC and CSR subsidies for adults, and compares family marketplace plans from BCBSTX, Ambetter, and Oscar Health — including split-enrollment strategy for qualifying households. Free, no obligation.

Maternity Coverage on Texas Family Plans

All ACA-compliant Texas family plans from Ambetter, BCBSTX, and Oscar cover maternity and newborn care as one of the 10 essential health benefits — prenatal visits, labor and delivery at Texas Children’s and UT Southwestern, postpartum care, and newborn care subject to plan deductible. Texas has one of the highest uninsured birth rates nationally, making pre-conception enrollment timing critical. Short-term plans sold in Texas exclude maternity entirely.

For Texas families planning a pregnancy, ACA-compliant marketplace coverage is the only reliable vehicle for maternity coverage. BCBSTX, Ambetter, Oscar Health, Aetna, and UnitedHealthcare marketplace plans in Texas all cover maternity under the 10 essential health benefit mandate. A typical Texas marketplace Silver plan covers prenatal visits at the plan’s specialist copay structure, inpatient delivery at the plan’s hospital coinsurance rate after deductible, and newborn care for the first few days at the same hospital stay rate. Average total out-of-pocket cost for a vaginal delivery at an Austin or Houston hospital under a Silver plan runs $2,000–$4,500 depending on deductible accumulation and plan tier.

A birth or adoption triggers a 60-day Special Enrollment Period on HealthCare.gov, allowing the Texas family to add the newborn or adopted child to an existing Ambetter, BCBSTX, or Oscar marketplace plan — or switch plans entirely. The SEP window begins on the date of birth or adoption placement. Texas families should contact HealthCare.gov or their carrier directly within that window: newborn coverage is backdated to the birth date when the carrier is notified promptly. Missing the 60-day window means waiting for the next open enrollment period, leaving a newborn uninsured or covered only under one parent’s existing plan.

Short-term plans exclude maternity — confirm before buying

Texas families of childbearing age who purchase short-term limited-duration insurance as a cost-saving measure face significant risk. Short-term plans sold in Texas are not required to cover maternity care, and virtually all exclude it entirely. A pregnancy detected after enrollment is treated as a pre-existing condition on renewal or a new short-term application. The $30,000–$80,000+ cost of prenatal care, delivery, and newborn care becomes entirely out-of-pocket without ACA-compliant coverage in place before conception. For Texas families planning or considering pregnancy, ACA-compliant coverage through HealthCare.gov or off-exchange is strongly recommended over short-term plans regardless of premium savings.

The ACA Family Glitch Fix and Texas Employer Coverage

The ACA family glitch fix — effective January 1, 2023 — changed how employer coverage affordability is calculated for family members. Before the fix, if an employer offered affordable employee-only coverage, the entire family was blocked from marketplace subsidies even if the family premium was unaffordable. After the fix, family members can qualify for marketplace APTC independently if the employer’s family premium exceeds 9.96% of household income — a significant change for Texas families with expensive family tier employer coverage.

Texas employers are not required by state law to offer health insurance to employees or their families — the ACA employer mandate applies only at 50+ full-time equivalent employees. Many Texas small employers offer group coverage to the employee only, leaving family members to find coverage independently. Even among larger Texas employers who offer family tier coverage, the employee’s share of the family premium can run $600–$1,200 monthly — well above the 9.96% household income affordability threshold for many Texas households.

The family glitch fix means Texas families should re-evaluate marketplace eligibility annually if they previously assumed employer coverage blocked subsidy access. A Dallas family of four where one parent has an employer plan with a $900/month family premium contribution earns $75,000 annually — the family premium represents 14.4% of household income, above the 9.96% threshold. Under post-2023 rules, the dependents may qualify for marketplace APTC subsidies independently even if the employee-only premium is affordable. The HealthCare.gov application performs this calculation automatically when employer coverage information is entered.

Texas Family Health Insurance Carriers for 2026

Texas family health insurance on HealthCare.gov is dominated by BCBSTX, Ambetter, and Oscar Health across the major metro rating areas. BCBSTX leads on network depth for families needing broad hospital access; Ambetter leads on lowest family plan premium; Oscar adds telehealth-integrated care for digitally-native families. Off-exchange, BCBSTX and UnitedHealthcare serve families above subsidy ceilings through direct carrier or broker enrollment.

Blue Cross Blue Shield of Texas (BCBSTX)

Statewide / NetworkBCBSTX is the dominant family health insurance Texas carrier with statewide network depth at Memorial Hermann, Houston Methodist, Baylor Scott & White, Texas Health Resources, and HCA Healthcare. Family Bronze, Silver, and Gold plans on HealthCare.gov plus off-exchange PPO products for above-subsidy households. BlueCard national reciprocity covers family members traveling or receiving care out-of-state. Broadest pediatric specialist network of any Texas marketplace carrier.

- Statewide family network

- Broadest pediatric specialist access

- On- and off-exchange products

- BlueCard national reciprocity

Ambetter (Centene)

Lowest premium / CSRAmbetter consistently offers the lowest family plan premiums on HealthCare.gov across Texas metro rating areas — the strongest choice for CHIP-ineligible families below 250% FPL seeking maximum subsidy on Silver CSR plans. Narrower provider network than BCBSTX, particularly outside Houston, Dallas-Fort Worth, Austin, and San Antonio. Strong pediatric network within contracted metros. Ideal family health insurance Texas option when premium minimization and CSR access are the primary goals.

- Lowest family plan premium

- CSR Silver specialist

- Major metro pediatric network

- On-exchange only

Oscar Health

Digital / TelehealthOscar’s family plans in Houston, Dallas-Fort Worth, Austin, and San Antonio include 24/7 telehealth and a dedicated family care team — features particularly useful for families with young children who need frequent routine care. Premium sits between Ambetter and BCBSTX. Oscar’s digital member platform simplifies adding dependents, managing multiple family members’ claims, and coordinating pediatric care. Strong fit for tech-comfortable Texas families in major metros.

- Major Texas metros only

- 24/7 telehealth included

- Digital family care team

- Mid-range family premium

Frequently Asked Questions

Common questions about family health insurance Texas cover the best plan for families in 2026, maternity coverage requirements on ACA plans, 2026 family premium ranges by household income, whether children can be on CHIP while parents use a marketplace plan, and how the ACA family glitch fix changed subsidy eligibility for families with expensive employer family-tier coverage.

What is the best family health insurance plan in Texas for 2026?

For most Texas families below 400% of federal poverty level ($124,800 for a family of four in 2026), the best family health insurance Texas option is a subsidized Silver plan on HealthCare.gov from BCBSTX, Ambetter, or Oscar Health — with Advanced Premium Tax Credit and Cost-Sharing Reduction subsidies applied. Silver with CSR for households below 250% FPL delivers the strongest combined premium and out-of-pocket value. Families whose children qualify for Texas CHIP (below 200% FPL for children under 19) should enroll the children in CHIP and the adults in marketplace plans separately — this split strategy often produces the lowest total household coverage cost. Above the subsidy ceiling, BCBSTX off-exchange Gold or PPO delivers the broadest family network across Texas hospital systems.

Does Texas family health insurance cover maternity care?

All ACA-compliant family health insurance Texas plans — on-exchange and off-exchange ACA plans — are required to cover maternity and newborn care as one of the 10 essential health benefits. This includes prenatal visits, labor and delivery, postpartum care, and newborn care subject to plan deductible and out-of-pocket costs. Texas marketplace plans from BCBSTX, Ambetter, Oscar, and UnitedHealthcare all include maternity coverage. Note: Aetna exited the Texas individual market at end of 2025 and is no longer available on HealthCare.gov for 2026. Short-term limited-duration plans sold in Texas are NOT ACA-compliant and typically exclude maternity care — a critical distinction for Texas families planning pregnancies. A birth or adoption also triggers a 60-day Special Enrollment Period, allowing Texas families to add the newborn to existing coverage or switch plans within 60 days of the event.

How much does family health insurance cost in Texas for 2026?

Family health insurance Texas costs in 2026 vary by household size, ages, plan tier, rating area, and subsidy eligibility. A family of four — two adults age 40, two children — can expect full-price monthly premiums of $1,400–$2,100 for Silver on HealthCare.gov before subsidies. After Advanced Premium Tax Credit, a family of four earning $80,000 (about 257% FPL) typically pays $300–$600 monthly for Silver coverage. The ACA’s family out-of-pocket maximum for 2026 is $21,200 — capping total annual exposure for covered in-network care. Texas CHIP covers children under 19 in qualifying families below 200% FPL at $0–$50 per year in enrollment fees, substantially reducing total household coverage cost when children qualify.

Can my children be on CHIP while I’m on a marketplace plan in Texas?

Yes. Texas families can split coverage — children enrolled in Texas CHIP and parents enrolled in a HealthCare.gov marketplace plan simultaneously. This split-enrollment strategy is often the most cost-effective approach for families earning below 200% of federal poverty level ($62,400 for a family of four in 2026). CHIP for eligible children costs $0–$50 per year in enrollment fees with $3–$5 copays; adults enroll in subsidized marketplace plans at income-adjusted APTC premium. The APTC calculation for the adults is based on household income regardless of whether children are enrolled in CHIP or the marketplace, so the parents’ subsidy is not affected by the children’s CHIP enrollment.

What is the ACA family glitch fix and how does it affect Texas families?

The ACA family glitch fix, effective January 1, 2023, changed how employer coverage affordability is evaluated for family members. Before the fix, if an employer offered affordable coverage to the employee (below 9.96% of household income for employee-only premium), the entire family was deemed ineligible for marketplace subsidies — even if the family premium was far above the affordability threshold. After the fix, family members can qualify for marketplace APTC independently if the employer’s family premium cost exceeds 9.96% of household income. For Texas families whose employer offers affordable employee-only coverage but expensive family coverage, the post-2023 fix means dependents may now qualify for subsidized HealthCare.gov plans for the first time.

Compare 2026 Texas Family Health Insurance

A licensed Texas broker checks CHIP eligibility for your children, calculates household APTC and CSR subsidies, models split-enrollment strategy, and compares family plans from BCBSTX, Ambetter, and Oscar Health by rating area. Family glitch fix evaluation included for employer-covered households. Free, no obligation.

Free Texas family coverage comparison — CHIP, marketplace, and off-exchange in one call.

Explore Texas Coverage In Depth

Statewide overview of Texas health insurance — marketplace, Medicaid, and off-exchange options compared.

Texas Marketplace EnrollmentHealthCare.gov enrollment guide for Texas — APTC subsidies, open enrollment, and SEPs.

Individual Texas Health InsuranceIndividual plan options — marketplace, off-exchange PPO, and direct carrier enrollment.

Texas PPO PlansOff-exchange PPO for Texas families above subsidy ceilings — BCBSTX, Cigna, UHC.

Self-Employed Texas Health InsuranceFamily coverage for 1099 contractors — HealthCare.gov subsidies, HSA-HDHP, and Schedule 1 deduction.

Cheap Texas Health InsuranceLowest-cost Texas plans — CHIP for children, subsidized Silver, and affordability by income tier.

Catastrophic Texas Health InsuranceUnder-30 plans — $10,600 deductible, hardship exemption, for young adults before family formation.

Short-Term Texas Health InsuranceBridge coverage for Texas families between employer plans — maternity exclusion caveat.

Private Texas Health InsuranceOn-exchange and off-exchange private family coverage options for Texas households.

Texas Retiree Health InsurancePre-Medicare bridge ages 55–64 — TRS-Care, ERS, APTC subsidies, COBRA vs marketplace.

Texas Small Business Health InsuranceGroup plans for 1–50 employees — PPO, HMO, SHOP, and ICHRA options compared.

National PPO Health Insurance PlansNationwide PPO guidance applying across all 50 states — carriers, networks, and rate structures.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Texas residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.