Cheap Texas Health Insurance 2026: Lowest-Cost Plans

Cheap health insurance Texas options for 2026 hinge on one structural reality: Texas did not expand Medicaid, leaving roughly 1.5 million low-income Texans in the coverage gap. For Texans above 100% of federal poverty level, the cheapest qualifying coverage is a subsidized HealthCare.gov Bronze plan from Ambetter, Oscar Health, or BCBSTX — typically $0–$80 monthly after subsidies for households under $35,000. Texas CHIP covers children under 19 in qualifying low-income families.

What brings you here today?

What “Cheap” Health Insurance Means in Texas

Cheap health insurance Texas shoppers typically have three real options in 2026: subsidized HealthCare.gov Bronze plans from Ambetter, Oscar Health, or BCBSTX with Advanced Premium Tax Credit applied; Texas CHIP for children under 19 in qualifying low-income families; and short-term or catastrophic plans for healthy adults willing to accept narrower coverage. The cheapest qualifying coverage depends on income — at $25,000 single income, expect $40–$80 monthly Silver with subsidies; at $50,000, expect $250–$340 Bronze; above $60,240, full-price applies.

The word “cheap” in cheap health insurance Texas carries different meanings depending on what’s left out. ACA-compliant marketplace coverage — Bronze, Silver, Gold, Platinum tiers sold on HealthCare.gov — meets the 10 essential health benefit minimums and protects against catastrophic medical costs, but full-price monthly premiums in Texas can run $390 to $520 for the lowest Bronze tier before subsidies. Cheap health insurance Texas plans below those numbers typically achieve the lower price by either applying federal subsidies (HealthCare.gov APTC + CSR) or by stripping coverage (short-term limited-duration, fixed-indemnity products, healthcare sharing ministries).

For most Texas households earning between 138% and 400% of federal poverty level, the practical cheapest coverage is a subsidized HealthCare.gov plan. The Advanced Premium Tax Credit can reduce monthly premium to $0 for the lowest-income enrollees and to $40–$120 monthly for households earning $25,000–$45,000 single or $50,000–$90,000 family of four. Below 100% FPL, Texas residents fall into the coverage gap — the state’s decision not to expand Medicaid leaves an estimated 1.5 million Texans with no affordable coverage path. Texas CHIP remains available for children under 19 in qualifying low-income families regardless of adult cheap health insurance Texas enrollment status.

The three categories of cheap Texas health insurance

(1) Subsidized ACA-compliant — Bronze and Silver plans on HealthCare.gov with APTC and CSR; the cheapest path for most Texas households below 400% FPL. (2) CHIP and family-based — Texas CHIP for kids under 19 with low-income family eligibility; near-free for qualifying families. (3) Non-ACA-compliant alternatives — short-term limited-duration plans, fixed indemnity, and catastrophic plans for adults under 30 with hardship exemption; cheaper monthly premium but with significant coverage gaps. The right choice depends on income, household composition, and willingness to accept narrower benefits.

The Texas Medicaid Coverage Gap

Texas is one of ten states that has not expanded Medicaid under the Affordable Care Act, leaving roughly 1.5 million Texans in the coverage gap — adults earning too much for traditional Texas Medicaid but too little for HealthCare.gov subsidies, which require income at or above 100% of federal poverty level ($15,060 single adult in 2026). Texans in the gap have no affordable coverage path and represent the largest single share of uninsured adults in any U.S. state.

The Texas Medicaid coverage gap is the single most important affordability fact for cheap health insurance Texas shoppers to understand. Traditional Texas Medicaid covers a narrow set of adult populations: parents below 17% of federal poverty level (one of the strictest thresholds in the country), pregnant women up to 198% FPL, people with qualifying disabilities, and low-income seniors. Childless adults at any income level are generally not eligible for Texas Medicaid. The Medicaid expansion provision of the ACA was designed to cover this population — adults below 138% FPL — but the Supreme Court’s 2012 NFIB v. Sebelius decision made expansion optional for states, and Texas has declined to expand every year since.

The practical consequence is that a single Texan earning $12,000 annually has no affordable coverage path under current law. They earn too much for parental Medicaid (which would require income below roughly $2,550 annually for a single parent), they aren’t pregnant or disabled, and they earn too little for HealthCare.gov APTC subsidies (which require minimum income of $15,060 for a single adult in 2026). The coverage gap is unique to non-expansion states — in California, New York, or Massachusetts, the same Texan would qualify for full Medicaid at zero monthly premium. According to the Kaiser Family Foundation, the Texas coverage gap is the largest in the nation by population, accounting for roughly 40% of all coverage-gap adults nationwide.

Coverage gap workarounds Texans actually use

Texans in the Medicaid gap rarely have great options, but a few partial paths exist. Texas CHIP still covers children under 19 in qualifying families regardless of adult coverage status — apply through Your Texas Benefits. Pregnancy Medicaid covers prenatal care for pregnant women up to 198% FPL. Federally Qualified Health Centers (FQHCs) provide sliding-scale primary care across Texas regardless of insurance status. Hospital district programs in Harris County, Bexar County, and Dallas County provide limited care to low-income uninsured adults. Some Texans deliberately project slightly higher income on HealthCare.gov to qualify for the lowest-cost subsidized Bronze plan (estimating $15,500 instead of $12,000) — this is legal as long as the projection is made in good faith, but actual income at year-end must reconcile on Form 8962.

HealthCare.gov Subsidies: How Much Texans Save

HealthCare.gov subsidies in Texas average $667 per month per enrollee for 2026 coverage based on CMS enrollment data, with 92% of Texas marketplace enrollees receiving at least some Advanced Premium Tax Credit. A single Texan earning $25,000 typically pays $40–$80 monthly for a Silver plan with Cost-Sharing Reductions after subsidies. A family of four earning $60,000 often pays $0–$120 monthly after combined APTC and CSR. Subsidies phase down between 250% and 400% federal poverty level.

The Advanced Premium Tax Credit and Cost-Sharing Reduction subsidies are the single largest driver of cheap health insurance Texas pricing. APTC reduces monthly premium directly and applies to plans at any metal tier — Bronze, Silver, Gold, or Platinum — though the dollar value is calculated against the second-lowest-cost Silver plan in your rating area (the “benchmark plan”). CSR is separate and applies only to Silver-tier plans for households below 250% FPL, lowering the deductible, out-of-pocket maximum, and coinsurance significantly. A Texan eligible for both subsidies typically gets the best total value on Silver, even when Bronze has a lower nominal premium.

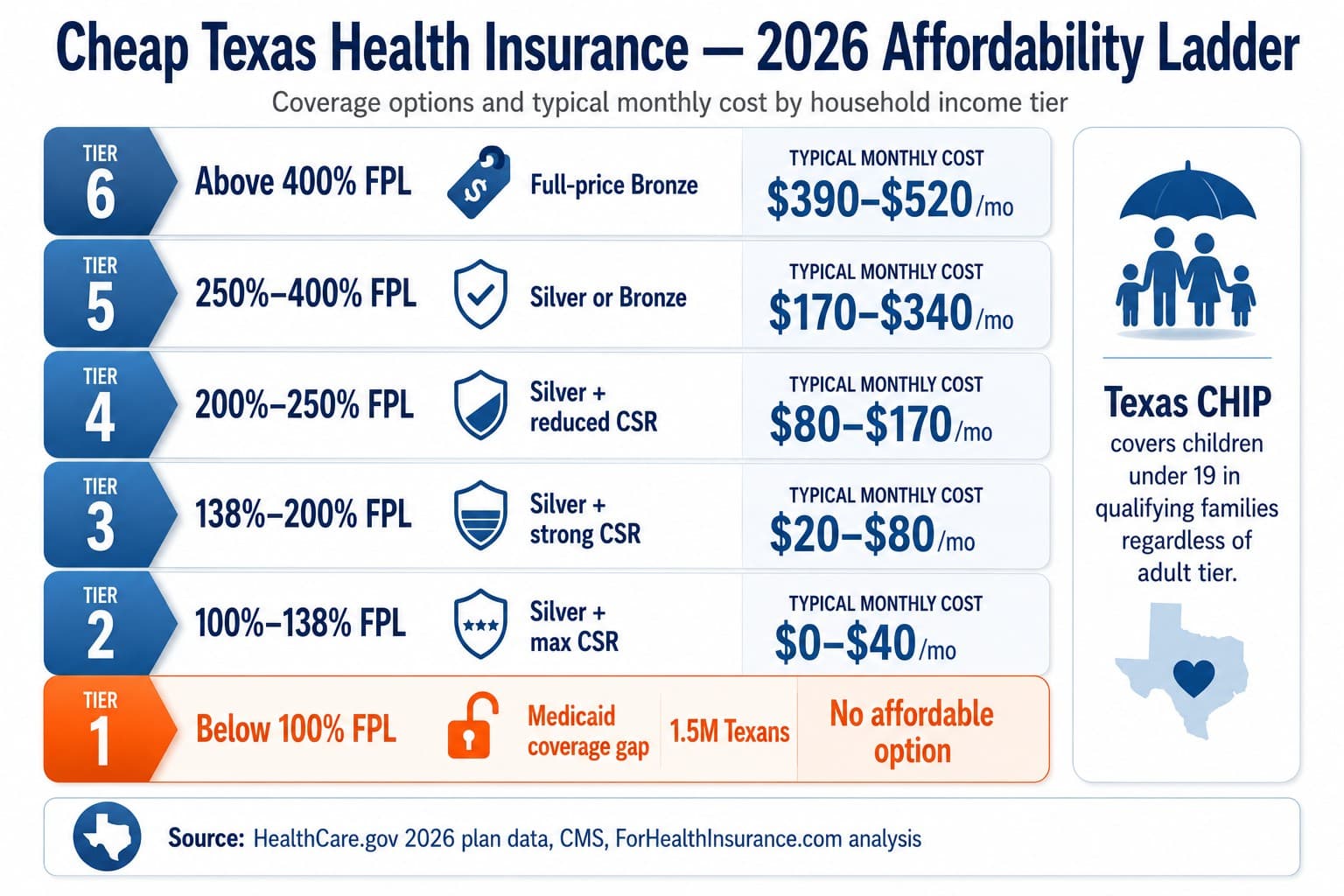

| Texas Income Tier (2026) | Typical Cheapest Cost | Best Plan Type | Subsidies Available |

|---|---|---|---|

| Below 100% FPL ($15,060 single) | No affordable coverage | Medicaid gap — see workarounds | None (Texas didn’t expand) |

| 100%–138% FPL ($15,060–$20,783 single) | $0–$40/mo | Silver + maximum CSR | Full APTC + 94% CSR |

| 138%–200% FPL ($20,783–$30,120 single) | $20–$80/mo | Silver + CSR | Full APTC + 87% CSR |

| 200%–250% FPL ($30,120–$37,650 single) | $80–$170/mo | Silver + reduced CSR | Partial APTC + 73% CSR |

| 250%–400% FPL ($37,650–$60,240 single) | $170–$340/mo | Silver or Bronze | Reduced APTC only |

| Above 400% FPL ($60,240+ single) | $390–$520/mo | Full-price Bronze | None |

The numbers above assume a 40-year-old non-smoker; younger Texans pay 10–25% less and older Texans 30–60% more for the same tier. Texas operates 26 separate geographic rating areas, so actual premiums vary by metro — Houston, Dallas-Fort Worth, and Austin generally see lower full-price premiums than rural West Texas or the Rio Grande Valley. The official HealthCare.gov portal is the only legitimate enrollment channel for subsidized Texas marketplace coverage — off-exchange enrollment forfeits APTC and CSR eligibility entirely.

Example: San Antonio Retail Worker, Age 38

A 38-year-old single retail worker in Bexar County earns $22,000 annually — approximately 146% of the 2026 federal poverty level. She does not qualify for Texas Medicaid (childless adults are ineligible at any income in Texas) but qualifies for full APTC and Cost-Sharing Reduction subsidies on HealthCare.gov. An Ambetter Silver plan in her rating area runs approximately $498/month before subsidies. After her estimated $445/month APTC credit, her net premium is roughly $53/month. With Silver CSR at 146% FPL, her deductible drops from approximately $5,500 to $850 and her out-of-pocket maximum falls to approximately $3,000 — delivering near-Gold plan benefits at Bronze-adjacent monthly cost. Total annual premium cost: approximately $636 before any medical spending.

Lowest-Premium Carriers for Texas Bronze Plans

For cheap health insurance Texas buyers comparing HealthCare.gov Bronze plans in 2026, the lowest-premium carriers are Ambetter (Centene), Oscar Health, and Blue Cross Blue Shield of Texas. Ambetter consistently leads on Bronze monthly premium across most Texas rating areas, while Oscar competes in major metros with digital-first member services. BCBSTX carries higher premium but offers the broadest provider network — important if specific hospital access matters.

Ambetter (Centene)

Lowest Bronze premiumAmbetter is Centene’s marketplace brand and the most common low-cost Bronze choice for cheap health insurance Texas buyers. Available across all Texas rating areas with consistently competitive Bronze monthly premium — often $30–$70 less than equivalent Oscar or BCBSTX Bronze for the same age and metro. Trade-off: narrower provider network than BCBSTX, with deeper contracting in Houston, Dallas-Fort Worth, and San Antonio metros than in rural Texas.

- Centene marketplace brand

- Lowest Bronze pricing statewide

- CSR-friendly Silver lineup

- Narrower hospital network

Oscar Health

Major metros / DigitalOscar offers Bronze and Silver plans in Houston, Dallas-Fort Worth, Austin, and San Antonio with digital member tools and 24/7 telehealth included. Bronze premium typically sits $10–$40 above Ambetter but below BCBSTX. Strong fit for younger Texans, gig workers, and first-time enrollees comfortable navigating coverage through an app. Network includes major metro hospital systems but is narrower than BCBSTX statewide.

- Major Texas metros only

- Digital-first member experience

- Integrated telehealth at no extra cost

- Mid-range Bronze pricing

Blue Cross Blue Shield of Texas (BCBSTX)

Statewide / Broadest networkBCBSTX Bronze plans carry the highest premium among the three main marketplace carriers but include the broadest provider network — Memorial Hermann, Houston Methodist, Baylor Scott & White, Texas Health Resources, and HCA Healthcare facilities. For cheap health insurance Texas buyers whose providers are at one of those systems, BCBSTX Bronze can still be the cheapest practical option after accounting for in-network access. Available across all 26 Texas rating areas.

- HCSC parent / Texas Blues

- Broadest statewide network

- Higher Bronze premium

- BlueCard national reciprocity

Scott & White Health Plan & CHRISTUS

Regional / Hospital-anchoredTwo Texas-headquartered regional carriers offering marketplace plans tied to specific hospital systems. Scott & White Health Plan (Baylor Scott & White) serves Central Texas around Temple, Killeen, Waco, and the Austin corridor. CHRISTUS Health Plan covers East Texas, South Texas, and parts of the Rio Grande Valley anchored at CHRISTUS facilities. Regional carriers occasionally offer the cheapest Bronze in specific Texas rating areas — worth checking on HealthCare.gov in those metros.

- Texas-headquartered regional carriers

- Hospital-system-anchored networks

- Region-specific competitive pricing

- Narrower statewide reach

Aetna

Exited Individual Market 2026Aetna exited the individual health insurance market entirely at the end of 2025 — including Texas marketplace plans. Aetna is no longer available for individual HealthCare.gov enrollment in 2026. Their primary Texas presence is now through employer group plans and Medicare Advantage for Texans 65+. Texas cheap health insurance shoppers on HealthCare.gov should compare Ambetter, Oscar, and BCBSTX as the active individual market carriers.

- Limited metro availability

- CVS/MinuteClinic integration

- Mid-range Bronze pricing

- Stronger in Medicare Advantage

UnitedHealthcare

Family-focusedUnitedHealthcare’s marketplace footprint in Texas is selective — not available in every rating area, and Bronze premiums run higher than Ambetter or Oscar. Where available, UHC offers strong national reciprocity for Texas families with college students out-of-state or split-household coverage needs. Most cheap health insurance Texas shoppers find Ambetter, Oscar, or BCBSTX more competitive on monthly premium for in-Texas coverage.

- Selective Texas metro availability

- Higher Bronze premium

- National network reciprocity

- Family multi-state strength

Get a Cheap Texas Health Insurance Quote

A licensed Texas broker compares Bronze and Silver plans from Ambetter, Oscar Health, BCBSTX, and regional carriers — with full APTC and CSR subsidy calculation based on your projected 2026 household income. Free, no obligation, and the subsidy work is done in 30 minutes.

Texas CHIP: Cheap Coverage for Children

Texas CHIP (Children’s Health Insurance Program) covers children under 19 in qualifying low-income families at no or low monthly cost. Families below 150% of federal poverty level typically pay no premium with $3–$5 copays per visit. Families between 150% and 200% FPL pay a $35–$50 annual enrollment fee. CHIP covers doctor visits, hospital stays, prescriptions, dental, vision, mental health, and immunizations. Apply through Your Texas Benefits — eligibility is reviewed annually.

For Texas families looking for cheap health insurance Texas options that cover their children specifically, CHIP is almost always the right answer when family income qualifies. The eligibility threshold is generous compared to adult Medicaid: a family of four earning up to $62,400 in 2026 (200% FPL) qualifies for CHIP coverage of all children under 19, regardless of whether the parents have insurance, are uninsured, or are in the Medicaid coverage gap. CHIP is jointly federally and state funded, administered by the Texas Health and Human Services Commission.

CHIP coverage is comprehensive — far broader than the minimum essential coverage requirements of ACA marketplace plans. Texas CHIP covers all 10 essential health benefits plus pediatric dental and vision care explicitly included. Network is built around community health centers, federally qualified health centers (FQHCs), and pediatric specialists across Texas. Enrollment is year-round (no annual open enrollment window) and renewal happens every 12 months with an eligibility review. Apply at YourTexasBenefits.com or by phone through 2-1-1 Texas — the application also screens for SNAP, TANF, and other low-income programs simultaneously.

When Short-Term and Catastrophic Plans Make Sense

Short-term limited-duration plans and catastrophic plans both deliver lower monthly premium than ACA-compliant marketplace coverage, but with significant trade-offs. Short-term plans in Texas run $90–$200 monthly versus $390+ for full-price Bronze, but exclude maternity, mental health, prescriptions, and pre-existing conditions. Catastrophic plans require age under 30 or a hardship exemption and cap routine care but cover catastrophic events at marketplace network levels.

Short-term limited-duration insurance is the cheapest monthly-premium category of health coverage available to Texas adults — but the cheap monthly premium reflects the coverage gaps. Short-term plans are not required to comply with the ACA’s 10 essential health benefits, so most exclude maternity care, mental health and substance use treatment, prescription drug coverage at meaningful levels, and any pre-existing condition care. Coverage caps are typically $1 million to $2 million lifetime versus the ACA’s unlimited annual and lifetime maximums. Texas allows short-term plans up to 36 months total duration after federal rule changes during the Trump administration.

Catastrophic plans are a different animal. Sold on HealthCare.gov to Texas adults under 30 or those qualifying for a hardship exemption, catastrophic plans carry the lowest premiums in the marketplace ($210–$310 monthly for a 25-year-old) but with a high deductible (typically the annual out-of-pocket maximum, $10,600 for 2026). Once the deductible is met, coverage kicks in at the same network rates as Bronze, Silver, and Gold plans. Catastrophic also includes three primary care visits per year before the deductible and full coverage of ACA preventive services — making them a defensible cheap health insurance Texas plan choice for healthy young adults who’d otherwise go uninsured.

Cheap monthly premium can become expensive at claim time

The trade-off with short-term and catastrophic plans is concentrated risk. A 28-year-old Texan paying $130 monthly for a short-term plan saves about $3,100 annually versus a full-price Bronze. But if that 28-year-old breaks an ankle skiing, gets diagnosed with a chronic condition, or becomes pregnant, the short-term plan’s exclusions and lifetime caps can leave them paying $15,000–$80,000+ out of pocket on a single event. Run the math against your actual health profile — a healthy adult with a savings buffer can absorb the risk; an adult with chronic conditions, a planned pregnancy, or no medical savings cannot. The Texas Department of Insurance recommends ACA-compliant coverage as the default for most Texas households.

Frequently Asked Questions

Common questions about cheap health insurance Texas options cover the lowest-cost qualifying plans for 2026, the Texas Medicaid coverage gap for low-income adults, how much HealthCare.gov subsidies actually save Texas marketplace enrollees, Texas CHIP eligibility and benefits for children under 19, and whether short-term limited-duration plans deliver real savings or just lower premium with higher claim risk.

What is the cheapest health insurance in Texas for 2026?

For most Texans, the cheapest qualifying health insurance is a subsidized HealthCare.gov Bronze plan from Ambetter, Oscar Health, or Blue Cross Blue Shield of Texas after Advanced Premium Tax Credit (APTC) is applied. A typical 40-year-old Texan earning $35,000 can pay $0–$50 per month for a Bronze plan after subsidies in 2026. Below $35,000 annual income, Texans should check eligibility for Cost-Sharing Reductions (CSR) on Silver plans, which substantially lower deductibles and out-of-pocket maximums — often a better value than the cheapest Bronze for low-to-moderate income households. The absolute cheapest path for parents is Texas CHIP for children under 19 in qualifying low-income families, which carries low or no monthly premium.

Does Texas have a Medicaid coverage gap?

Yes. Texas is one of ten states that has not expanded Medicaid under the Affordable Care Act, leaving roughly 1.5 million Texans in the coverage gap — adults earning too much to qualify for traditional Texas Medicaid (limited mostly to parents below 17% of federal poverty level, pregnant women, and people with disabilities) but too little to qualify for HealthCare.gov Advanced Premium Tax Credit subsidies, which require income at or above 100% of federal poverty level ($15,060 for a single adult in 2026). Texans in the coverage gap have no affordable coverage path and represent the largest single share of uninsured adults in any U.S. state. Children below 200% FPL still qualify for Texas CHIP regardless of the adult coverage gap.

How much can a Texan save with HealthCare.gov subsidies?

HealthCare.gov subsidies in Texas average $667 per month per enrollee for 2026 coverage based on CMS enrollment data, with 92% of Texas marketplace enrollees receiving at least some APTC. A single Texan earning $25,000 (about 166% of federal poverty level) typically pays $40–$80 per month for a Silver plan with CSR after subsidies, versus a full-price equivalent of $450–$520 monthly. A family of four earning $60,000 (about 192% FPL) often pays $0–$120 per month after APTC and CSR. Subsidies phase down between 250% and 400% FPL, then end above $60,240 single or $124,800 family of four — at which point full-price HealthCare.gov Bronze plans run $390–$520 for the lowest tier.

Is Texas CHIP free for my children?

Texas CHIP (Children’s Health Insurance Program) is free or low-cost for children under 19 in qualifying low-income families — generally below 200% of federal poverty level ($62,400 for a family of four in 2026). Families below 150% FPL typically pay no monthly premium, just small copays for doctor visits ($3–$5) and prescriptions ($0–$5). Families between 150% and 200% FPL pay an enrollment fee of $35–$50 per year per family plus the same small copays. CHIP covers doctor visits, hospital stays, prescriptions, dental, vision, mental health, and immunizations. Apply through Your Texas Benefits at YourTexasBenefits.com — eligibility is reviewed annually.

Should I buy short-term health insurance to save money in Texas?

Short-term limited-duration insurance plans in Texas are cheaper than ACA-compliant marketplace plans, often $90–$200 per month versus $390+ for full-price Bronze, but the savings come with significant trade-offs. Short-term plans are not required to cover the ACA’s 10 essential health benefits — they typically exclude maternity care, mental health, prescription drugs, and pre-existing conditions. Coverage limits are usually capped at $1–$2 million lifetime versus unlimited on marketplace plans. Texas allows short-term plans up to 36 months total. Short-term works for healthy Texans bridging brief gaps between employer coverage and a new job; it should not replace ACA-compliant coverage for households with ongoing health needs or chronic conditions.

Compare 2026 Cheap Texas Health Insurance Plans

A licensed Texas broker calculates your full APTC and CSR subsidy eligibility, then compares Bronze and Silver options from Ambetter, Oscar Health, BCBSTX, and Texas regional carriers — plus checks Texas CHIP eligibility for any children in your household. Free, no obligation, and the affordability math is done in one call.

Free Texas affordability comparison — subsidies, CHIP, and Bronze plans in one call.

Explore Texas Coverage In Depth

Statewide overview of Texas health insurance — marketplace, Medicaid, and off-exchange options compared.

Texas Marketplace EnrollmentHealthCare.gov enrollment guide for Texas — APTC subsidies, open enrollment, and SEPs.

Individual Texas Health InsuranceIndividual plan options — marketplace, off-exchange PPO, and direct carrier enrollment.

Texas PPO PlansOff-exchange PPO for Texans above subsidy ceilings — BCBSTX, Cigna, and UnitedHealthcare compared.

Self-Employed Texas Health Insurance1099 contractors and freelancers — HealthCare.gov subsidies, HSA-HDHP, and Schedule 1 deduction.

Catastrophic Texas Health InsuranceUnder-30 and hardship exemption plans — lowest ACA-compliant premium for eligible Texans.

Short-Term Texas Health InsuranceNon-ACA bridge coverage — cheaper monthly premium with major coverage trade-offs.

Private Texas Health InsuranceOff-exchange private coverage for Texans above ACA subsidy thresholds.

Family Texas Health InsuranceFamily coverage strategies — CHIP for children, marketplace plans, and combined household paths.

Texas Retiree Health InsurancePre-Medicare bridge ages 55–64 — TRS-Care, ERS, APTC subsidies, COBRA vs marketplace.

Texas Small Business Health InsuranceGroup plans for 1–50 employees — PPO, HMO, SHOP, and ICHRA options compared.

National PPO Health Insurance PlansNationwide PPO guidance applying across all 50 states — carriers, networks, and rate structures.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Texas residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.