Best Health Insurance in Alaska: 2026 Plans Compared

With only two carriers and some of the highest premiums in the country, Alaska’s health insurance market rewards careful comparison. The right plan depends heavily on where you live, how often you use care, and what you pay for prescriptions — and in Alaska, Gold plans frequently cost less than Silver, which flips the usual logic. This guide matches coverage options to real situations so residents can make a more confident decision heading into 2026.

What are you looking for?

Best Health Insurance Companies in Alaska

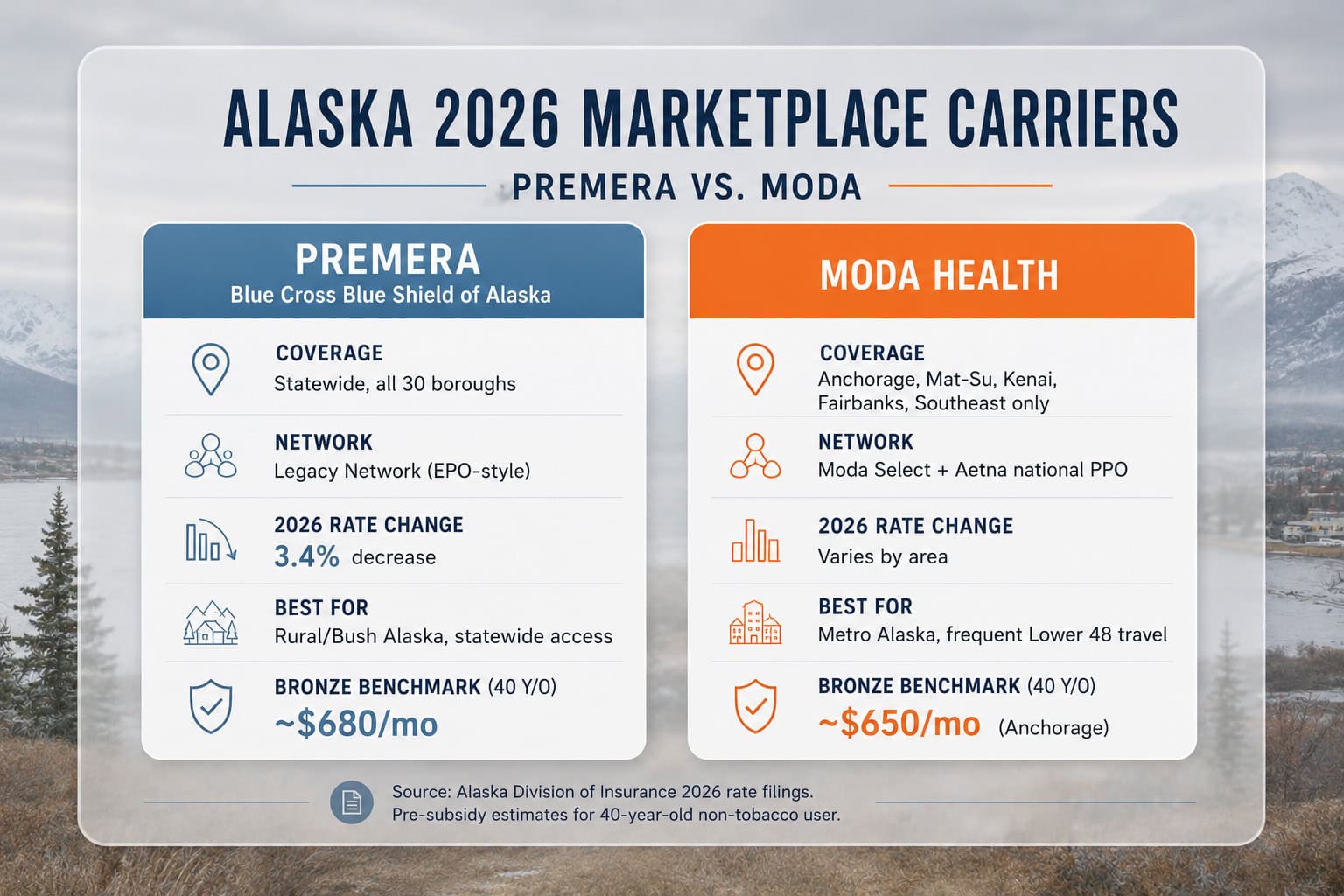

According to CMS marketplace data, two carriers offer the best health insurance plans in Alaska for 2026. Premera Blue Cross Blue Shield covers all boroughs statewide and enrolls the majority of marketplace participants. Moda Health returned to the Alaska marketplace and offers plans in the state’s most populated regions. For rural residents outside Moda’s service area, Premera is the only option.

Premera Blue Cross Blue Shield of Alaska

StatewideAll 29 boroughs • 4,000+ network providers • EPO-style plans • 3.4% rate decrease for 2026

Strengths

- Only carrier available in all Alaska boroughs, including rural and Bush regions

- Largest provider network in the state — virtually every doctor and hospital participates

- Strong coordination with Alaska Native Tribal Health Consortium facilities

- Telemedicine partnerships for remote area access

- Full range of Bronze, Silver, and Gold plans

Considerations

- No out-of-network coverage except emergencies (EPO-style plans)

- Out-of-state coverage requires advance coordination for non-emergencies

Moda Health Plan

Select Regions5 regions • PPO • Aetna national network

Strengths

- Available in Anchorage, Mat-Su, Kenai Peninsula, Fairbanks North Star, and Southeast Alaska

- PPO plans with access to Aetna national network for out-of-state care (expanded for 2026)

- Often cheaper than Premera for Bronze plans in the Anchorage area

- Moda Select Network with curated provider list for in-state care

Considerations

- Not available in rural or Bush Alaska — Premera is the only option in those areas

- Smaller in-state network compared to Premera

- Higher complaint rate relative to company size

Why Alaska Has Limited Carrier Competition

Alaska’s small population (around 733,000), vast geography, high healthcare delivery costs, and expensive medical transport requirements make the market challenging for national carriers. Moda returned to the marketplace after earlier withdrawals and now serves the state’s most populated boroughs. Still, residents in rural areas have only one carrier option, and overall competition remains limited compared to most states.

Best Alaska Health Insurance Plans by Metal Tier

According to HealthCare.gov plan categories, the best health insurance plan in Alaska depends on expected healthcare usage, income level, and tolerance for upfront costs versus monthly premiums. Bronze plans work best for healthy individuals who rarely need care. Silver plans with cost-sharing reductions offer the best value for lower-income residents. Gold plans suit those with predictable, ongoing healthcare needs. For the lowest-premium Bronze and Catastrophic options specifically, see cheap health insurance in Alaska.

| Metal Tier | Avg. Premium (40 y/o) | Typical Deductible | Out-of-Pocket Max | Best For |

|---|---|---|---|---|

| Bronze | $686–$733/mo | $4,300–$6,350 | $8,500–$10,600 | Healthy individuals, catastrophic protection |

| Silver | $1,025–$1,053/mo | $2,500–$3,000 | $4,750–$8,700 | Those qualifying for CSR (under 250% FPL) |

| Silver + CSR | Same as Silver* | $250–$1,500 | $2,850–$6,500 | Lower-income residents (under 250% FPL) |

| Gold | $882–$934/mo | $1,100–$1,500 | $4,600–$7,500 | Chronic conditions, frequent care, families |

*CSR plans use Silver-tier premiums but with significantly reduced deductibles and copays based on income. In Alaska, Gold plans are typically cheaper than Silver — an anomaly caused by how Alaska’s risk pool and plan pricing interact. Source: 2026 QHP Landscape data via CMS.

Best Health Insurance for Specific Situations

The best health insurance in Alaska varies based on individual circumstances. A young fisherman in Kodiak has different needs than a retired couple in Anchorage or a self-employed consultant in Fairbanks. Rather than declaring one “best” plan, matching coverage to situation produces better outcomes and lower total costs.

Best for Families

Silver / GoldRecommendation: Silver plan with cost-sharing reductions (if income qualifies) or Gold for families with young children needing frequent pediatric care.

Why: Families typically use more healthcare — well-child visits, sick visits, prescriptions. Silver CSR plans offer deductibles as low as $250 for families under 150% FPL, making them the strongest coverage value in Alaska for qualifying households.

Key feature: Pediatric dental and vision included in all ACA plans.

Best for Self-Employed

Bronze + HSARecommendation: Bronze plan paired with a Health Savings Account. Starting in 2026, all Bronze and Catastrophic marketplace plans are HSA-compatible.

Why: Self-employed individuals can deduct 100% of premiums on Schedule 1, plus contribute pre-tax dollars to HSAs ($4,400 individual / $8,750 family in 2026). Combined tax savings often exceed $3,000 annually.

Key feature: HSA funds roll over indefinitely and can be invested for long-term growth.

Best for Chronic Conditions

GoldRecommendation: Gold plan for predictable costs and lower prescription copays, especially for specialty medications.

Why: With chronic conditions, you’ll likely hit your deductible and out-of-pocket maximum anyway. Gold plans front-load coverage with lower deductibles ($1,100–$1,500 vs. $4,300–$6,350 for Bronze) and provide better prescription tiers.

Key feature: Review the formulary for your specific medications before enrolling.

Best for Remote Areas

Gold + TelehealthRecommendation: Any marketplace plan with strong telemedicine benefits; Gold tier if medical transport is a concern.

Why: Rural Alaska residents rely heavily on telemedicine for routine care. When in-person care requires travel to Anchorage or Fairbanks, lower deductibles reduce the financial burden of major procedures.

Key feature: Most marketplace plans in Alaska offer $0 telehealth visits for primary care before the deductible.

Best for Seasonal Workers

BronzeRecommendation: Bronze plan during fishing/tourism season; evaluate Medicaid eligibility during off-season based on annual income.

Why: Seasonal workers often have variable income. Bronze provides affordable catastrophic coverage during high-earning months. Some may qualify for Medicaid during lower-income periods.

Key feature: Special enrollment periods are available when income changes significantly.

Best for Early Retirees

SilverRecommendation: Silver plan for those aged 55–64, especially if income qualifies for subsidies and CSR benefits.

Why: Pre-Medicare retirees often have moderate healthcare needs and fixed incomes. Silver plans balance premiums with reasonable deductibles. Subsidies are particularly valuable given Alaska’s high base premiums.

Key feature: Age-based premium increases are capped under ACA rules.

Best Health Insurance in Alaska for Prescriptions

According to HealthCare.gov essential benefits, the best health insurance for prescription drugs in Alaska depends on medication type and cost. Gold plans consistently offer the lowest copays and broadest formulary access. Silver plans with cost-sharing reductions provide strong prescription benefits for qualifying lower-income residents. Bronze plans cover prescriptions but only after meeting the full deductible — potentially costing thousands before coverage begins.

| Drug Tier | Bronze Plan | Silver Plan | Gold Plan |

|---|---|---|---|

| Tier 1 (Generic) | After deductible | $15 copay | $10 copay |

| Tier 2 (Preferred Brand) | After deductible | $50 copay | $35 copay |

| Tier 3 (Non-Preferred) | After deductible | $100 copay | $75 copay |

| Tier 4 (Specialty) | After deductible | 25% coinsurance | 20% coinsurance |

Copay amounts are typical ranges across Premera and Moda plans and vary by specific plan. Bronze plans require meeting the full deductible before prescription coverage applies. Silver and Gold copays shown apply before deductible. Verify your specific medication costs using the carrier’s formulary tool before enrolling. Source: 2026 Summary of Benefits and Coverage documents via HealthCare.gov.

Real Example: Marcus, Fairbanks, Type 2 Diabetes, Age 52

The Situation: Marcus takes Ozempic ($900/month retail), metformin ($15/month generic), and lisinopril ($10/month generic). On a standard Bronze plan, he’d pay full price until meeting his $6,350 deductible.

The Analysis: On a Gold plan — which in Alaska often has lower premiums than Silver — Marcus pays copays for Ozempic immediately with no deductible required. Annual drug costs drop significantly compared to Bronze, where he’d pay thousands out of pocket before coverage begins.

The Result: For residents with predictable, expensive prescriptions, Gold plans frequently save thousands annually despite higher premiums. Running the numbers on actual prescriptions reveals the best health insurance option in Alaska for each situation.

Compare Alaska Health Plans Side by Side

Plan pricing, formularies, and subsidy amounts vary by income and household size. Enter your details to compare Alaska plan options side by side.

Healthcare Access by Alaska Region

The best health insurance plan also depends on where you live in Alaska. Urban Anchorage residents have access to multiple hospitals and specialists within minutes. Rural residents may travel hours or rely entirely on telemedicine and tribal health facilities. Understanding regional healthcare infrastructure helps determine the right coverage for your specific location.

| Region | Major Facilities | Specialist Access | Key Consideration |

|---|---|---|---|

| Anchorage / Mat-Su | Providence (401 beds), Alaska Regional (250 beds), Mat-Su Regional | Full specialty access | Most comprehensive care; benchmark for Alaska |

| Fairbanks / Interior | Fairbanks Memorial (152 beds), Bassett Army | Most specialties available | Some complex cases referred to Anchorage |

| Juneau / Southeast | Bartlett Regional (49 beds) | Limited; travel often required | Ferry/flight to Seattle for major procedures |

| Kenai Peninsula | Central Peninsula (49 beds), South Peninsula | Basic specialties | 2–3 hour drive to Anchorage for complex care |

| Rural / Bush Alaska | Village clinics, ANTHC facilities | Telemedicine primary | Medical transport coverage critical |

Facility data reflects major hospitals as of 2026. Bed counts are approximate. In regions served by both Premera and Moda (Anchorage/Mat-Su, Fairbanks, Kenai Peninsula, Southeast), residents can compare plans from both carriers. Rural and Bush Alaska residents are served only by Premera on the marketplace. Source: Alaska State Hospital and Nursing Home Association.

How to Choose the Best Health Insurance in Alaska

Selecting the best health insurance in Alaska requires evaluating four factors: expected healthcare usage, income and subsidy eligibility, provider preferences, and prescription needs. No single plan is universally the top option — the right choice depends on individual circumstances.

Estimate Healthcare Usage

Step 1Review last year’s medical expenses. Count doctor visits, prescriptions, and any procedures. If total out-of-pocket spending was under $2,000, Bronze plans likely save money. If spending exceeded $5,000, Gold plans may offer better value — especially in Alaska where Gold premiums are often lower than Silver.

Check Subsidy Eligibility

Step 2Enter household income and size to see estimated subsidies. According to HHS poverty guidelines, if income is under 250% FPL ($48,875 single, $100,475 family of four in Alaska), Silver plans with cost-sharing reductions often provide the best total value.

Verify Provider Access

Step 3Confirm current doctors are in-network for the chosen carrier. Premera covers most Alaska providers statewide, while Moda uses the Moda Select Network in its service areas. Check both carriers’ directories before enrolling to avoid surprise gaps.

Compare Prescription Costs

Step 4Use the carrier’s formulary tool to check coverage for current medications. Calculate annual drug costs under each metal tier. For expensive specialty drugs, Gold plans often save thousands despite covering more of the total cost.

Frequently Asked Questions About the Best Health Insurance in Alaska

Alaska residents frequently ask about carrier options, plan recommendations by situation, PPO availability, and prescription coverage differences across metal tiers. Below are answers to the most common questions about finding the best health insurance in Alaska for 2026.

What is the best health insurance company in Alaska?

Two carriers offer individual marketplace plans in Alaska for 2026: Premera Blue Cross Blue Shield (available statewide) and Moda Health (available in Anchorage, Mat-Su, Kenai Peninsula, Fairbanks North Star, and Southeast Alaska). Premera has the largest provider network and serves all boroughs. Moda offers PPO plans with national network access through Aetna, which benefits residents who need out-of-state care.

Which health insurance plan is best for families in Alaska?

Silver plans offer the best value for most Alaska families, especially those earning under 250% of the federal poverty level who qualify for cost-sharing reductions. A family of four earning $100,475 or less receives enhanced Silver benefits with deductibles as low as $500 instead of the standard $4,000.

What is the best health insurance for self-employed people in Alaska?

Self-employed Alaskans benefit most from Bronze HSA-compatible plans paired with Health Savings Accounts. The combination of low premiums, tax-deductible HSA contributions, and the self-employed health insurance deduction on Schedule 1 creates significant tax advantages while maintaining catastrophic protection.

Are there any PPO plans available in Alaska?

Moda Health offers PPO-style plans in select Alaska regions (Anchorage, Mat-Su, Kenai Peninsula, Fairbanks, Southeast) with access to the Aetna national network for out-of-state care. Premera offers EPO-style plans with broad in-state networks but no out-of-network coverage except for emergencies. For a full overview of PPO options, see our PPO health insurance plans guide.

Which Alaska health insurance plan has the best prescription coverage?

Gold-tier plans offer the best prescription coverage with lower copays and broader formularies. For residents with expensive specialty medications, Gold plans often save money despite higher premiums. Silver plans with cost-sharing reductions also provide strong drug coverage for qualifying lower-income residents.

What health insurance covers telemedicine in Alaska?

All Alaska marketplace plans from both Premera and Moda include telemedicine coverage, with most offering $0 telehealth visits for primary care before meeting the deductible. Telemedicine access is a key factor in choosing the best health insurance in Alaska given the state’s vast geography and limited rural provider access.

Alaska Health Insurance Resources

Complete 2026 overview — marketplace, Medicaid, and subsidy paths for Alaska residents

Alaska Marketplace EnrollmentHealthCare.gov enrollment steps, open enrollment dates, and Premera plan tiers

Affordable Coverage in AlaskaAlaska’s nation-leading subsidy averages and how to maximize financial assistance

Cheap Health Insurance in AlaskaLowest-cost 2026 Alaska plans — Bronze premiums, catastrophic options, and ways to cut monthly costs

Find the Best Alaska Health Insurance Plan

Premiums and subsidy amounts differ by region and income level. Enter your details to see actual plan pricing for your area.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Alaska residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.