Affordable Health Insurance in Alaska: Low-Cost Options for 2026

Alaska’s base premiums are the highest in the country, but the subsidy math here works differently than most states. Because benchmark premiums are so high, federal tax credits are correspondingly larger — and for most residents who shop through the marketplace, the gap between sticker price and what they actually pay for affordable health insurance is significant. For 2026, subsidy amounts are smaller than prior years following the expiration of enhanced federal credits, but meaningful help still exists for households earning under 400% FPL. This guide covers who qualifies, what it costs at different income levels, and which plan types offer the best value.

What are you looking for?

What Makes Health Insurance Affordable in Alaska

Premium tax credits through HealthCare.gov make affordable health insurance in Alaska possible by covering the gap between Alaska’s high benchmark premiums and what a household can reasonably pay based on income. Because Alaska’s benchmark premiums are the highest in the nation, qualified residents receive correspondingly larger subsidies than in most states.

⚠ 2026 Subsidy Changes

Enhanced federal subsidies in place from 2021–2025 expired at the end of 2025 and were not extended by Congress. The subsidy cliff is back at 400% FPL — households above $78,200 (single) receive no premium tax credits for 2026. Residents who were subsidy-eligible in 2025 may still qualify but will generally receive smaller credits. Always verify your 2026 amount through HealthCare.gov before selecting a plan.

Premium Tax Credits

Income-BasedFederal subsidies reduce monthly costs based on household income and apply automatically when purchasing through HealthCare.gov. Because Alaska’s benchmark premiums rank highest nationally, eligible residents receive larger credits than in most states — even with the 2026 reduction from prior years.

Cost-Sharing Reductions

Under 250% FPLHouseholds earning 100–250% FPL get lower deductibles, copays, and out-of-pocket maximums on Silver plans. A standard $4,000 deductible drops to $250–$500 with CSR benefits — making Silver often more affordable than Bronze for lower-income residents who use care regularly.

Alaska Native Benefits

Tribal MembersAlaska Native and American Indian members enrolled in marketplace plans face zero cost-sharing for services through tribal facilities. Special zero-premium plans are available at any income level when receiving care through the Alaska Native Tribal Health Consortium’s 250+ village clinics.

Medicaid Expansion

Under 138% FPLAlaska Medicaid covers residents earning up to 138% FPL ($26,979 individual, $55,462 family of four in 2026). Coverage includes no premiums and minimal cost-sharing, providing genuinely free health insurance for qualifying residents year-round.

How Much Does Affordable Health Insurance Cost in Alaska

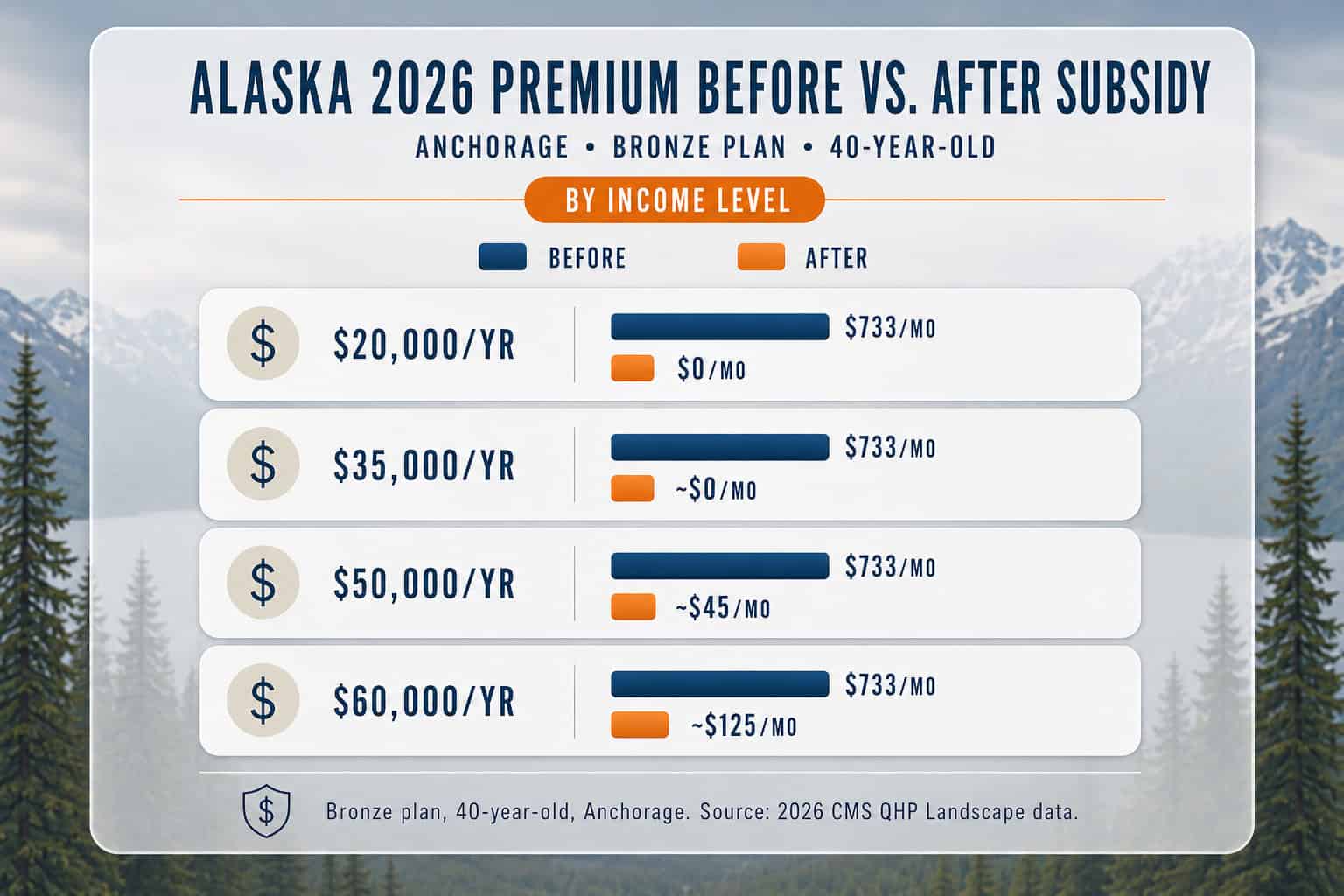

For most subsidy-eligible residents, marketplace coverage in 2026 costs between $0 and $200 per month. According to HealthCare.gov plan pricing, a 40-year-old in Anchorage pays approximately $1,025/month for a benchmark Silver plan before subsidies. After tax credits, lower-income residents often pay significantly less or nothing at all.

| Annual Income (Single) | % of FPL | Bronze Plan | Silver Plan | Gold Plan |

|---|---|---|---|---|

| $20,000 | 133% | $0/mo | $12/mo | $85/mo |

| $35,000 | 233% | $0/mo | $78/mo | $215/mo |

| $50,000 | 332% | $45/mo | $165/mo | $340/mo |

| $60,000 | 399% | $125/mo | $245/mo | $420/mo |

Estimated after-subsidy premiums for a 40-year-old non-tobacco user in Anchorage. Actual premiums vary by age, county, carrier, and plan. Gold plans in Alaska are often cheaper than Silver before subsidies. Source: 2026 QHP Landscape data via CMS.

For detailed enrollment information to find affordable health insurance, see the Alaska health insurance marketplace guide.

Most Affordable Health Insurance Options in Alaska

The most affordable health insurance options in Alaska include Bronze marketplace plans for healthy individuals, Silver plans with cost-sharing reductions for lower incomes, Medicaid for qualifying residents, and Catastrophic coverage for those under 30. The right choice depends on expected healthcare usage, income level, and tolerance for higher deductibles. For a direct comparison of the lowest-premium Bronze and Catastrophic plans, see cheap health insurance in Alaska.

When Silver Beats Bronze for Affordability

For residents earning under 200% FPL ($39,100 single, $80,380 family of four), Silver plans with cost-sharing reductions often provide more cost-effective coverage overall. While monthly premiums run $50–$75 higher, a CSR-enhanced Silver plan reduces the deductible from $6,350 to $500 — saving thousands if any significant medical care is needed during the year.

| Feature | Bronze | Silver + CSR | Catastrophic |

|---|---|---|---|

| Subsidy Eligible | ✓ Yes | ✓ Yes | ✗ No |

| Typical Monthly Premium | $0–$75/mo | $50–$150/mo | $150–$250/mo |

| Deductible | $6,350 | $250–$500 (with CSR) | $9,200 |

| Plan Covers | 60% of costs | Up to 94% with CSR | ~60% after deductible |

| Free Preventive Care | ✓ Yes | ✓ Yes | ✓ Yes (+ 3 primary visits) |

| Age Restriction | None | None | Under 30 only |

| Best When | You rarely use care | Income under 250% FPL | No subsidy eligibility |

Who Qualifies for Affordable Health Insurance Subsidies in Alaska

According to HealthCare.gov eligibility rules, Alaska residents earning between 100% and 400% of the federal poverty level qualify for premium tax credits that make affordable health insurance in Alaska accessible even with the state’s high base premiums. Because Alaska’s benchmark premiums rank among the highest nationally, subsidies are larger here than in most states even at the same income percentage.

| Household Size | 100% FPL | 200% FPL | 300% FPL | 400% FPL |

|---|---|---|---|---|

| 1 Person | $19,550 | $39,100 | $58,650 | $78,200 |

| 2 People | $26,530 | $53,060 | $79,590 | $106,120 |

| 3 People | $33,510 | $67,020 | $100,530 | $134,040 |

| 4 People | $40,190 | $80,380 | $120,570 | $160,760 |

Alaska uses higher FPL thresholds than the contiguous 48 states. Values shown are 2025 HHS poverty guidelines, which determine 2026 marketplace subsidy eligibility. Residents earning below 138% FPL ($26,979 individual) may qualify for Alaska Medicaid instead of marketplace subsidies. Source: HHS ASPE poverty guidelines.

Real Example: Finding Affordable Health Insurance in Fairbanks

Abstract numbers only go so far. This real-world example shows how one Alaska resident found affordable health insurance in Alaska by applying subsidies she did not know she qualified for — cutting her monthly premium from $680 to $195, a savings of nearly $6,000 a year.

Jennifer, Self-Employed Graphic Designer, Age 35, $42,000 Income

The Situation: Jennifer, a freelance designer in Fairbanks, was paying $680/month for private coverage purchased directly from Premera — that’s $8,160 annually for a plan she rarely used beyond annual checkups.

The Discovery: After checking HealthCare.gov during Open Enrollment, Jennifer learned she qualified for $485/month in premium subsidies. At 279% of the federal poverty level, she also qualified for modest cost-sharing reductions on Silver plans.

The Result: Jennifer enrolled in a Silver plan with a $2,500 deductible for $195/month — saving $485/month compared to her previous coverage. Her new plan also includes better prescription coverage for her thyroid medication. Annual savings: $5,820 with improved benefits.

Check Your Subsidy Eligibility

Subsidy amounts vary by income and household size. Enter your details to compare plan options and see actual pricing for your area.

Strategies to Lower Health Insurance Costs in Alaska

Alaska residents can lower affordable health insurance costs through strategic plan selection, timing purchases during Open Enrollment, and maximizing available subsidies. Beyond choosing the right metal tier, several practical strategies help reduce both premium and out-of-pocket expenses throughout the coverage year.

Choose Silver at Lower Incomes

Under 250% FPLResidents earning under 250% FPL save more with Silver plans than Bronze despite higher premiums. Cost-sharing reductions dramatically lower deductibles — often providing $6,000+ in additional value that more than offsets the premium difference.

Use HSA-Compatible Plans

Tax SavingsHigh-deductible plans paired with Health Savings Accounts allow tax-free contributions for medical expenses. For 2026, individuals can contribute $4,400 and families $8,750. These contributions reduce taxable income while building funds for healthcare costs.

Leverage Telemedicine

$0–$50 vs. $150+Telemedicine visits cost $0–$50 versus $150+ for in-person urgent care. Alaska marketplace plans include telemedicine coverage, often before meeting deductibles — essential for residents in remote areas with limited provider access.

Review Coverage Annually

Open EnrollmentPlan options, prices, and subsidy amounts change yearly. Auto-renewing without comparing options often means missing better deals. Spending 30 minutes during Open Enrollment comparing plans can save $50–$200/month.

When to Enroll in Affordable Health Insurance in Alaska

Alaska residents enroll in affordable health insurance through the annual Open Enrollment period from November 1 through January 15. Plans selected by December 15 begin January 1; plans selected between December 16 and January 15 begin February 1. Outside this window, enrollment requires a qualifying life event such as job loss, marriage, birth of a child, or moving to Alaska from another state.

Medicaid Has No Enrollment Window

Alaska Medicaid enrollment remains open year-round for qualifying residents earning up to 138% FPL ($26,979 individual). Applications can be submitted anytime through the Alaska Department of Health or through HealthCare.gov. Processing typically takes 30–45 days, with coverage backdating to the application date if approved.

Frequently Asked Questions About Affordable Health Insurance in Alaska

Alaska residents searching for low-cost coverage frequently ask about subsidy eligibility, the cheapest plan types, cost-sharing reductions, and how to lower premiums through marketplace enrollment strategies for 2026.

What is the cheapest health insurance available in Alaska?

Bronze-tier marketplace plans through HealthCare.gov offer the lowest monthly premiums. With subsidies, many residents pay under $100/month. Catastrophic plans are available for those under 30 or with hardship exemptions, providing emergency coverage with minimal monthly costs but no subsidy eligibility.

How much are health insurance subsidies in Alaska?

During the 2025 plan year, Alaska had the highest average subsidies in the nation at $1,008/month, reducing the average enrollee’s net premium to $115/month. For 2026, subsidy amounts are smaller following the expiration of enhanced federal credits, but residents earning under 400% FPL still qualify for significant premium tax credits.

Can Alaska residents get free health insurance?

Yes. Alaska Medicaid covers residents earning up to 138% of the federal poverty level ($26,979 for an individual in 2026). Alaska Native and American Indian residents may also qualify for zero-premium, zero-cost-sharing marketplace plans regardless of income when receiving care through tribal health facilities.

Why is health insurance so expensive in Alaska before subsidies?

Alaska has the highest unsubsidized premiums nationally due to limited carrier competition (Premera Blue Cross and Moda Health are the only two marketplace carriers), small population spread across vast geography, high healthcare delivery costs, and expensive medical transport requirements. Federal subsidies offset most of these costs for eligible residents.

Who qualifies for health insurance subsidies in Alaska?

Alaska residents earning between 100% and 400% of the federal poverty level qualify for premium tax credits. For 2026, that means individuals earning $19,550 to $78,200 and families of four earning $40,190 to $160,760. Alaska uses higher FPL thresholds than the lower 48 states.

When can I sign up for affordable health insurance in Alaska?

Open Enrollment for 2026 coverage runs November 1 through January 15. Plans selected by December 15 begin January 1. Outside this window, enrollment requires a qualifying life event such as job loss, marriage, birth of a child, or moving to Alaska from another state. Medicaid enrollment is open year-round.

Alaska Health Insurance Resources

Complete 2026 overview — Premera plans, Health First Alaska Medicaid, and subsidy paths

Alaska Marketplace EnrollmentHealthCare.gov enrollment, Premera plan comparison, and 2026 open enrollment dates

Best Alaska Health Plans 2026Premera plan-by-plan comparison with annual out-of-pocket benchmarks by metal tier

Cheap Health Insurance in AlaskaLowest-cost 2026 Alaska plans — Bronze premiums, catastrophic options, and ways to cut monthly costs

Affordable Alaska Health Insurance Plans

Premiums and subsidy amounts differ by income level and household size. Enter your details to see actual plan pricing for your area.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Alaska residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.