Small Business Health Insurance in Louisiana: 2026 Group Plans & Options

Small business health insurance in Louisiana offers several paths for employers in 2026 — making Louisiana small business health insurance one of the most flexible markets in the Gulf South — from traditional group plans through Blue Cross Blue Shield of Louisiana to the SHOP marketplace and newer alternatives like ICHRAs that let employees choose their own individual plans. This guide covers what’s available to Louisiana employers, how to qualify for tax credits, and the key decisions facing businesses with 2–50 employees.

What does your business need?

Small Business Health Insurance Options in Louisiana

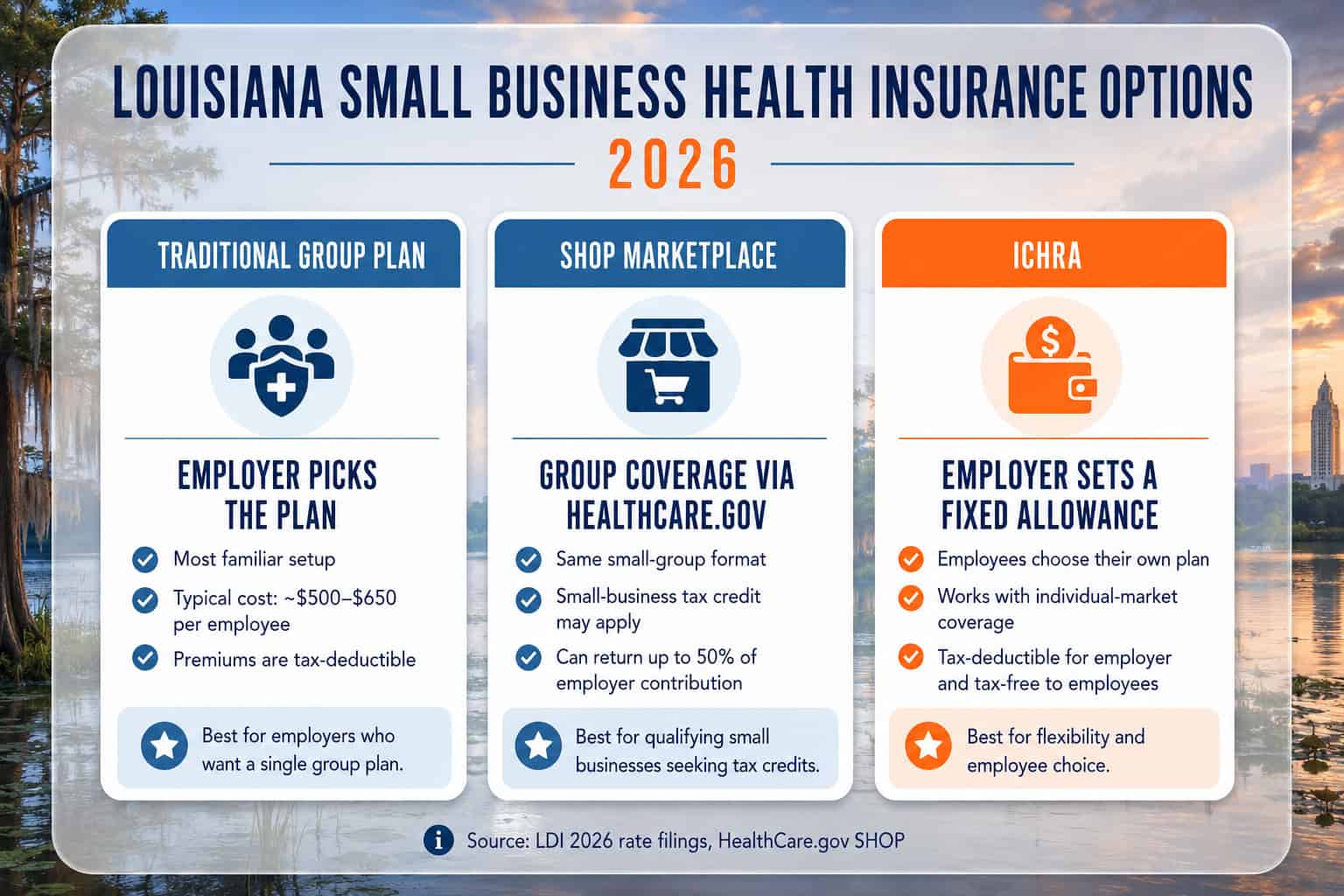

Louisiana small businesses with 2–50 employees can offer coverage through three primary channels: traditional small group plans from Blue Cross Blue Shield of Louisiana (the dominant small group carrier), the SHOP marketplace on HealthCare.gov, or an Individual Coverage Health Reimbursement Arrangement (ICHRA) that reimburses employees for individual plan premiums. Louisiana’s small group market saw rate increases averaging approximately 11.4% for 2026.

| Option | Eligible Businesses | Carriers in Louisiana | Tax Credit Eligible | Employee Choice |

|---|---|---|---|---|

| Traditional small group | 2–50 FTE | BCBS-LA (primary), HMO Louisiana | No (unless through SHOP) | Employer selects plan; employees enroll |

| SHOP on HealthCare.gov | 1–50 FTE | Same carriers, via HealthCare.gov | Yes — under 25 FTE + avg wages under $67,000 | Employees may choose from available metal tiers |

| ICHRA | Any size | Any — employees choose their own | No (but contributions are tax-free) | Full employee choice — HealthCare.gov or off-exchange |

| QSEHRA | Under 50 FTE, no group plan | Any — employees choose their own | No (but contributions are tax-free) | Full employee choice; max $6,350/individual in 2026 |

For many Louisiana small businesses — particularly those in parishes where carrier choice in the small group market is limited to BCBS-LA — the ICHRA model is gaining traction. Instead of the employer selecting a single group plan, the business sets a monthly dollar amount (e.g., $400/employee) and employees use that allowance to purchase their own individual plan through HealthCare.gov. This gives employees in Orleans Parish access to four carriers while an employee in Sabine Parish uses the same allowance for a BCBS plan — the employer’s cost is fixed regardless of parish or carrier selection.

Small Business Health Care Tax Credit in Louisiana

Small business health insurance Louisiana owners purchase through the SHOP marketplace qualifies for the Small Business Health Care Tax Credit — worth up to 50% of the employer’s premium contributions (35% for tax-exempt organizations). To qualify, the business must have fewer than 25 full-time equivalent employees, pay average annual wages under $67,000, and cover at least 50% of employee-only premium costs.

The credit is claimed on the employer’s annual federal tax return using IRS Form 8941. The maximum credit applies to businesses with 10 or fewer FTEs and average wages under $30,000. The credit phases out as employee count approaches 25 and average wages approach $67,000. Tax-exempt Louisiana organizations — including nonprofits and religious organizations — can claim up to 35% as a refundable credit.

Example: New Orleans Restaurant with 8 Employees

A New Orleans restaurant with 8 full-time employees averaging $31,000/year in wages purchases SHOP coverage through HealthCare.gov, contributing $480/month per employee toward a BCBS-LA Blue Connect Silver plan. Annual employer contribution: $46,080. The Small Business Health Care Tax Credit at approximately 42% (phased based on wages) returns roughly $19,350 — reducing the effective employer cost to $26,730, or about $278/month per employee.

Does Louisiana Require Employers to Offer Health Insurance?

Louisiana has no state employer mandate — unlike states such as Hawaii, which requires coverage for employees working 20+ hours/week. The federal ACA mandate applies only to businesses with 50 or more FTEs; with approximately 100,000 small businesses in Louisiana and 96% of them employing fewer than 20 workers, the vast majority face no coverage requirement at the state or federal level.

For Louisiana businesses at or near the 50-FTE threshold, the federal penalty is $2,970 per full-time employee (minus the first 30) in 2026. A 55-FTE Louisiana business not offering coverage faces a potential penalty of approximately $74,250/year. Unlike neighboring Texas — where large employer non-coverage rates run higher — Louisiana has no additional state-level enforcement mechanism. The ICHRA option is growing as a small business health insurance Louisiana alternative specifically because it lets multi-parish businesses offer coverage without committing to a single BCBS-LA network tier across all locations.

Louisiana Small Group Carriers for 2026

The small business health insurance Louisiana market is dominated by Blue Cross Blue Shield of Louisiana and its subsidiary HMO Louisiana, which together offer the broadest small group coverage across the state’s 64 parishes. BCBS-LA offers the same network tiers for small groups as for individual plans — Blue Connect (Ochsner), Signature Blue (LCMC), Community Blue (Baton Rouge General), and Precision Blue (FMOLHS). The Louisiana small group market saw rate increases averaging approximately 11.4% for 2026.

Small group plans in Louisiana are community-rated — premiums are based on employee ages, tobacco use, and parish location, not on the group’s health history. A 10-person group in East Baton Rouge Parish with an average employee age of 38 can expect small group Silver premiums of approximately $500–$650/month per employee before employer contributions. Louisiana requires a minimum of 2 eligible employees (working 25+ hours/week) for group coverage, and carriers require at least 75% of eligible employees to participate — if more than 25% of the group declines without other coverage, the group may be ineligible.

For businesses exploring the ICHRA alternative, employees purchase their own individual plans through HealthCare.gov or off-exchange, and the employer reimburses a set dollar amount tax-free. This shifts the carrier selection to the employee — a New Orleans employee might choose Ambetter for lower premiums while a Shreveport employee enrolls in BCBS Blue Connect for Ochsner access. The Best Health Insurance in Louisiana guide covers individual carrier options employees would choose from under an ICHRA arrangement.

Louisiana small businesses with 2–50 employees have three coverage paths in 2026 — traditional BCBS-LA group plans, the SHOP marketplace (with tax credits up to 50% of contributions for qualifying businesses), or ICHRA arrangements that let employees buy their own plans across all five marketplace carriers.

Compare Louisiana Small Business Health Plans

Louisiana small group Silver premiums average $500–$650/month per employee — but SHOP tax credits of up to 50% of contributions can cut that cost significantly for businesses with under 25 FTE and average wages under $67,000. Enter your employee count and parish to compare BCBS-LA group plans and ICHRA options.

ICHRA — An Alternative to Traditional Group Plans in Louisiana

An ICHRA lets Louisiana businesses set a fixed monthly dollar amount — say $400 or $500 per employee — for workers to buy their own individual plan through HealthCare.gov or off-exchange. Employer contributions are tax-deductible and tax-free to employees. Employees qualify for premium tax credits when the employer contribution meets the ACA affordability threshold.

ICHRAs are particularly well-suited to small business health insurance in Louisiana because of the state’s parish-based carrier variation. A traditional group plan locks all employees into BCBS-LA and one network tier — potentially problematic when a New Orleans employee needs Ochsner access (Blue Connect) but a Baton Rouge employee needs FMOLHS access (Precision Blue). With an ICHRA, each employee selects the individual plan that works best in their parish, and the employer’s per-employee cost stays fixed regardless of location or carrier selection.

ICHRA works well when

Employees are spread across multiple Louisiana parishes with different carrier availability. The business wants predictable, fixed monthly costs. Employees have diverse healthcare needs and prefer choosing their own plan type and metal tier from up to five individual market carriers.

Traditional group works well when

All employees are in the same parish with the same carrier options. The business qualifies for the SHOP tax credit (under 25 FTE, wages under $67,000). Employees prefer having the employer handle plan selection and administration through BCBS-LA or HMO Louisiana.

How to Set Up Small Business Health Insurance in Louisiana

Setting up small business health insurance Louisiana employers typically navigate four decisions: coverage type (group plan, SHOP, or ICHRA), carrier and network tier (BCBS-LA Blue Connect, Community Blue, etc.), contribution level (minimum 50% of employee-only premiums for SHOP tax credit eligibility), and enrollment timing. A licensed broker familiar with Louisiana’s parish-level carrier landscape can help evaluate which approach fits the business size, location, and employee demographics.

Determine your employee count and budget

Count full-time equivalent employees (25+ hours/week). Louisiana businesses under 25 FTE with average wages under $67,000 should evaluate SHOP for the tax credit. Businesses with 2–5 employees may find ICHRA or QSEHRA more cost-effective than traditional group rates. Louisiana requires a minimum of 2 eligible employees for group coverage.

Choose a coverage approach

Traditional group plan (employer selects BCBS-LA carrier and network tier), SHOP through HealthCare.gov (tax credit available), or ICHRA (employer sets dollar amount, employees buy their own plans from up to five marketplace carriers). Each has different administrative and cost implications for Louisiana businesses.

Get quotes from Louisiana small group carriers

For group plans, provide employee census data (ages, parish zip codes, tobacco status) to BCBS-LA or HMO Louisiana for accurate quotes. The Louisiana Department of Insurance publishes small group rate information. For ICHRA, determine the monthly allowance amount and let employees quote their own individual plans.

Enroll and communicate to employees

Group plans can start the first of any month — no open enrollment restriction for new groups. SHOP enrollment goes through HealthCare.gov’s small business portal. Provide employees with plan details, contribution amounts, and network information. Louisiana’s 12-month COBRA continuation applies to businesses with 2–19 employees after employee termination.

Louisiana Health Insurance Resources

Complete 2026 overview — carriers, costs, Medicaid, and enrollment

Marketplace & Enrollment GuideHealthCare.gov enrollment, deadlines, and plan comparison

Best Louisiana Health InsuranceCompare BCBS, Ambetter, UHC, and AmeriHealth by parish

Affordable Coverage & SubsidiesTax credits, CSR savings, and low-cost plan options

Short-Term Health InsuranceTemporary and bridge coverage options in Louisiana

Get Louisiana QuotesCompare 2026 plans and prices for your household

Individual Health InsurancePrivate and off-exchange plans for Louisiana individuals

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals

Frequently Asked Questions About Louisiana Small Business Coverage

Common questions Louisiana employers ask about small business health insurance — including why 100,000 Louisiana small businesses face no coverage mandate, how the SHOP tax credit phases out between 10–25 FTE and $30,000–$67,000 in average wages, and why ICHRA is gaining traction among multi-parish businesses where BCBS-LA network tier selection varies by location.

Is health insurance required for small businesses in Louisiana?

No. Louisiana has no state employer mandate. The federal ACA employer mandate applies only to businesses with 50 or more full-time equivalent employees. Louisiana businesses with fewer than 50 FTEs can offer small business health insurance voluntarily without penalty for not providing it. The vast majority of Louisiana’s approximately 100,000 small businesses fall below the 50-FTE threshold.

What is the Small Business Health Care Tax Credit?

The tax credit is worth up to 50% of the employer’s premium contributions (35% for tax-exempt organizations) for small businesses that purchase coverage through the SHOP marketplace on HealthCare.gov. To qualify, the business must have fewer than 25 full-time equivalent employees, pay average annual wages under $67,000, and cover at least 50% of employee-only premiums. Claimed on the federal tax return using IRS Form 8941.

What carriers offer small group plans in Louisiana?

Blue Cross Blue Shield of Louisiana and its subsidiary HMO Louisiana are the dominant small group carriers in Louisiana for 2026. BCBS-LA offers four network tiers for small groups — Blue Connect (Ochsner), Signature Blue (LCMC), Community Blue (Baton Rouge General), and Precision Blue (FMOLHS). Small group rate increases for 2026 averaged approximately 11.4% — making small business health insurance Louisiana carriers offer more expensive than prior years. Plans are community-rated based on employee ages, tobacco use, and parish.

What is an ICHRA and how does it work in Louisiana?

An Individual Coverage Health Reimbursement Arrangement lets employers set a fixed monthly dollar amount per employee for health insurance. Employees use that allowance to buy their own individual plan through HealthCare.gov or off-exchange from any of the five marketplace carriers. Employer contributions are tax-deductible and tax-free to employees. ICHRAs are well-suited to Louisiana businesses with employees across multiple parishes where carrier availability varies.

How much does small business health insurance cost in Louisiana?

Small business health insurance Louisiana Silver premiums run approximately $500–$650/month per employee for a group with an average age of 38 in East Baton Rouge Parish. Costs vary by employee ages, parish, carrier, and metal tier. Businesses qualifying for the SHOP tax credit can reduce effective costs by up to 50% of their premium contributions. ICHRA costs are fixed at whatever monthly amount the employer sets — there is no minimum required contribution.

What are Louisiana’s small group participation requirements?

Louisiana requires a minimum of 2 eligible employees (working 25+ hours per week) for group coverage. Carriers require at least 75% of eligible employees to participate in the group plan. If more than 25% of eligible employees decline coverage without proof of other health insurance, the group may not qualify. Employees who decline must typically sign a waiver confirming they have coverage elsewhere.

Find Small Business Health Insurance for Your Louisiana Team

Louisiana small group rates rose 11.4% for 2026. A 10-person group in East Baton Rouge with an average age of 38 pays $500–$650/month per employee through BCBS-LA — but the SHOP tax credit can return up to 50% of contributions for qualifying businesses. Enter your employee count and parish zip code to compare all three options.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Louisiana businesses. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.