Florida Small Business Health Insurance 2026: Group Plans Guide

Florida small business health insurance for 2026 covers three structural paths — traditional fully-insured group plans, level-funded plans with refund potential, and ICHRA reimbursement of individual marketplace coverage. Florida has approximately 1.4 million small businesses with most offering coverage voluntarily, since the ACA employer mandate applies only to businesses with 50+ FTEs.

What brings you here today?

Florida Small Business Health Insurance Options in 2026

Florida small businesses with 1-50 employees have three primary 2026 health insurance options: traditional fully-insured group plans through Florida Blue, Cigna, UnitedHealthcare, Humana, or Aetna; level-funded plans that combine group structure with self-funded refund potential; or ICHRA reimbursement of employee individual marketplace plans. Florida has approximately 1.4 million small businesses — the highest concentration of any state in the country, per the U.S. Small Business Administration — and most offer coverage voluntarily rather than under federal mandate.

Florida’s small business landscape is the largest in the country by a meaningful margin. According to the U.S. Small Business Administration 2025 Florida profile, Florida is home to approximately 1.4 million small businesses, representing 99.8% of all Florida businesses and employing roughly 41% of Florida private-sector workers. The breadth ranges from single-owner LLCs and 1099 contractors to 49-employee professional services firms operating across Miami-Dade, Broward, Hillsborough, Orange, and the I-4 corridor.

Florida group health insurance pricing operates differently from the individual marketplace. Group rates are based on the average demographics of the entire enrolled employee population, with carriers applying community rating principles to the small group market for 2-50 employee businesses. Florida small business premiums increased an average of 12-18% for 2026, substantially less than the 31.5% individual marketplace increase. The IRA’s enhanced premium tax credit expiration affected individual ACA shoppers significantly; group rating, which doesn’t rely on PTC subsidies, was much less disrupted.

💡 Aetna Group vs Aetna Marketplace — Separate Tracks

Aetna’s December 31, 2025 exit from the Florida individual marketplace did NOT affect Aetna group plans for Florida small businesses. Aetna group coverage remains fully available to Florida employers, competing with Florida Blue, Cigna, UnitedHealthcare, and Humana for new and renewal small business accounts.

Who Must Offer Health Insurance to Florida Employees?

Florida small businesses with fewer than 50 full-time equivalent employees are not required to offer health insurance under the Affordable Care Act employer mandate. Florida has no separate state-level mandate. Florida small businesses with 50+ FTEs are classified as Applicable Large Employers (ALEs) and must offer affordable, minimum-value coverage to full-time employees or face shared responsibility penalties. Most Florida small businesses offer voluntary coverage to attract and retain talent in competitive Florida labor markets.

The ACA employer mandate applies a specific threshold: 50 or more full-time equivalent (FTE) employees averaged over the prior calendar year. Full-time means 30+ hours per week; part-time hours are converted to FTE-equivalents. Florida small businesses below the 50-FTE threshold face no federal mandate to offer health insurance — the decision becomes purely strategic: a benefit to attract and retain employees in tight Florida labor markets, or a cost to control by not offering.

For Florida businesses approaching the 50-FTE threshold, the calculation method matters. The FTE count uses a 12-month look-back average, not a point-in-time headcount. Florida also has no state income tax, which affects employer total compensation calculations. Per CMS Florida employer group market data, voluntary offering rates among Florida small businesses with 10-49 employees run approximately 55-65%, similar to the national average.

Florida Small Business Group Plan Types: Traditional, ICHRA, Level-Funded

Florida small businesses choose between three structural plan types for 2026. Traditional fully-insured group plans transfer all risk to the carrier with predictable per-employee premiums. Level-funded plans combine group structure with self-funded refund potential when claims run below expectations. ICHRA lets Florida employers reimburse employees tax-free for individual marketplace plans instead of sponsoring group coverage.

Traditional Fully-Insured

Most CommonThe dominant Florida small business choice. The employer pays per-employee premiums monthly; the carrier handles all claims, administration, and risk. Premiums are predictable year-over-year and employer exposure is capped at premium contributions. Florida Blue, Cigna, UnitedHealthcare, Humana, and Aetna all offer competitive fully-insured small group plans. Tradeoff: full premium is paid even when claims are low, with no opportunity to recover unused funds.

Level-Funded

Fastest GrowingThe fastest-growing Florida small business option for 2026. Structurally self-funded with stop-loss insurance and aggregate refund provisions, level-funded plans look like traditional group from a monthly cash flow perspective. When total claims plus admin fees come in below the employer’s annual contribution, Florida employers receive a year-end refund. For healthier-than-average workforces — often professional services firms in Tampa, Orlando, and Jacksonville — level-funded can deliver 10-25% effective cost savings versus traditional group.

ICHRA

Max FlexibilityThe structural alternative for Florida employers who want to provide a benefit without managing a group plan. The Florida employer establishes a tax-free reimbursement budget per employee (or per employee class). Employees use those funds to purchase individual coverage on the Florida health insurance marketplace through HealthCare.gov. Administrative burden drops substantially — no carrier negotiation, no group plan renewal cycle, no enrollment census management. Best for geographically distributed teams or very small headcounts.

Top Florida Small Business Health Insurance Carriers for 2026

Florida Blue leads the small business market with all-67-county group plan availability and BlueCard nationwide network access. Cigna competes strongly in major metros with PPO, EPO, and HMO group options. UnitedHealthcare has a stronger employer-group presence than individual marketplace footprint in Florida. Humana maintains active South Florida group operations. Aetna remains fully available for Florida group coverage despite exiting the individual marketplace.

Florida Blue

All 67 CountiesThe structural anchor of the Florida small business group market. Flagship small group products include BlueOptions PPO for broader provider access and myBlue HMO for cost-focused groups. All-67-county coverage means businesses with rural employees (Panhandle, central agricultural counties) have meaningful coverage — most other carriers cannot field competitive group plans outside major metros. BlueCard nationwide reciprocity is valuable for multi-state businesses.

Cigna

Major MetrosCompetitive Florida small business group offerings concentrated in Miami-Dade, Broward, Hillsborough (Tampa), and Orange (Orlando) counties. Group plans include PPO, EPO, and HMO options with strong urban provider networks and international coverage benefits for businesses with traveling employees.

UnitedHealthcare

Employer-Group FocusUHC’s Florida presence skews heavily toward employer-group rather than individual. UHC group offerings often outcompete UHC individual offerings on network depth and plan flexibility, making UHC a serious contender for Florida small business accounts despite limited individual marketplace presence.

Humana

South FloridaActive South Florida group footprint with strong presence in Miami-Dade and Broward small business accounts. Competitive wellness programs and dental/vision bundling options make Humana a strong contender for benefit-conscious South Florida employers.

Aetna Group

Still AvailableAetna exited the Florida individual marketplace effective December 31, 2025, but Aetna small group and large group products remain fully available to Florida employers. Florida small businesses currently on Aetna group plans continue without disruption; new employers can consider Aetna group offerings on equal footing with other carriers.

Regional Carriers

County-SpecificAvMed and Health First serve specific Florida county group markets with competitive local pricing. AvMed has a strong presence in Central and South Florida; Health First operates primarily in Brevard and surrounding counties on Florida’s Space Coast.

Get a Florida Small Business Group Quote

A licensed Florida broker compares 2026 small business health insurance options across Florida Blue, Cigna, UnitedHealthcare, Humana, and Aetna — with per-employee pricing, ICHRA versus traditional group structure comparison, and level-funded refund modeling for your specific Florida business. Free, no obligation.

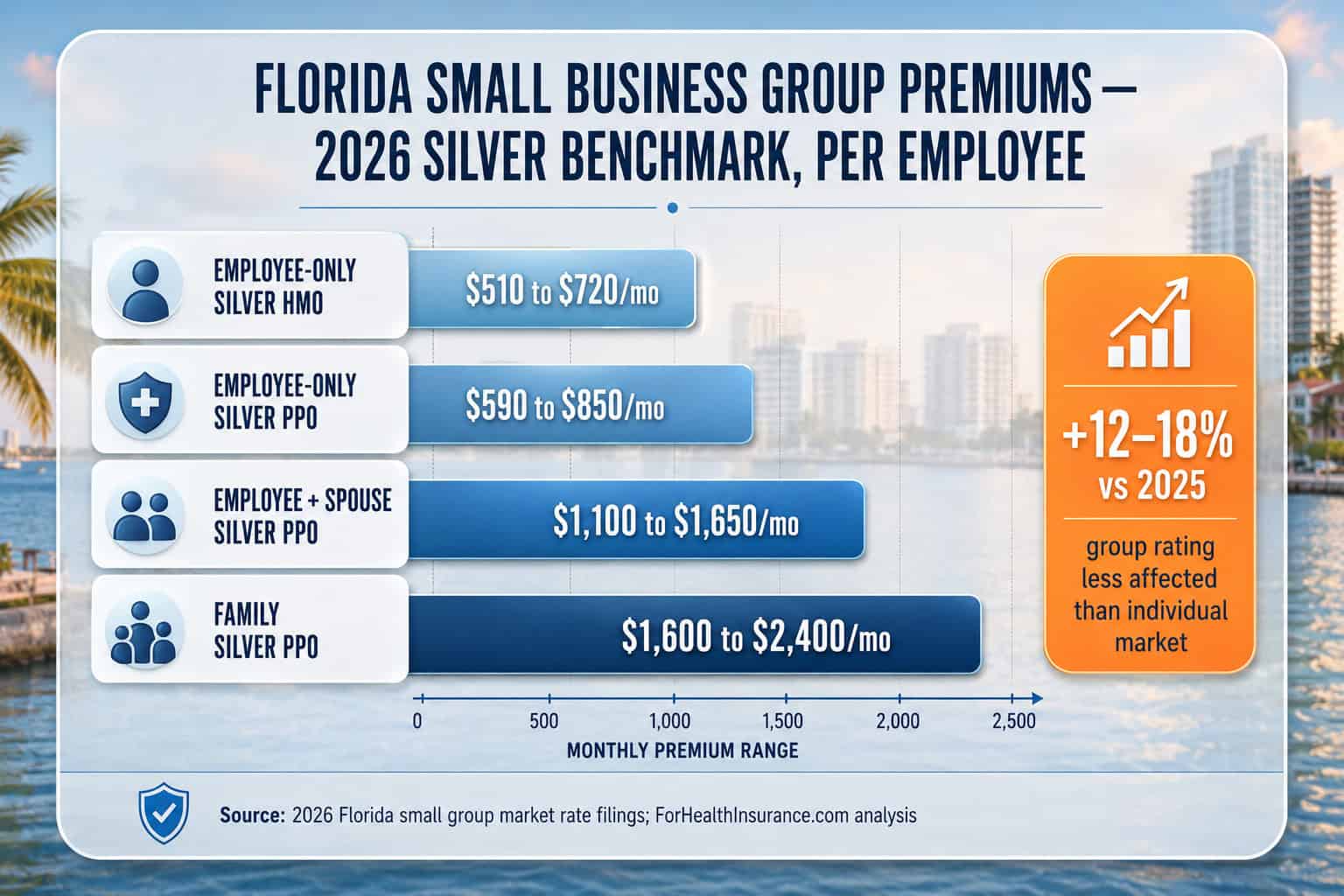

Florida Small Business Health Insurance Costs for 2026

Florida small business health insurance premiums for 2026 range from $550-$850 monthly per employee for employee-only Silver coverage, $1,100-$1,650 for employee-plus-spouse, and $1,600-$2,400 for family coverage. Florida group premiums increased an average of 12-18% for 2026 — well below the 31.5% individual marketplace increase. Employers typically contribute 50-75% of employee-only premium and 25-50% of dependent premium. Level-funded plans can run 10-25% below traditional group for healthier workforces.

Florida small business health insurance pricing depends on five primary factors: employee demographics (average age and gender distribution), county rating area, plan type and metal tier, carrier selection, and group size. Smaller groups (2-10 employees) typically pay higher per-employee premiums than larger small groups (25-50 employees) due to claims credibility.

| Florida Group Coverage Type | Monthly Premium Range (2026) | Typical Employer Contribution | Typical Employee Contribution |

|---|---|---|---|

| Employee-only Silver HMO | $510–$720/mo per employee | $300–$540 (50-75%) | $170–$360 |

| Employee-only Silver PPO | $590–$850/mo per employee | $350–$640 (50-75%) | $210–$430 |

| Employee + Spouse Silver PPO | $1,100–$1,650/mo | $550–$830 (50% of EE-only base) | $550–$820 |

| Family Silver PPO | $1,600–$2,400/mo | $750–$1,200 (varies by employer) | $850–$1,650 |

| Level-funded (healthier groups) | 10-25% below traditional | Same contribution percentages | Lower take-home cost |

Florida small business employers should factor in two additional cost considerations. First, the IRS Small Business Health Care Tax Credit (Form 8941) can refund up to 50% of an employer’s premium contribution for Florida small businesses with fewer than 25 FTEs, average wages under $66,000, and contributing at least 50% of employee premiums. Second, Florida has no state income tax, which simplifies employer total compensation modeling.

How to Set Up Group Health Insurance for Florida Business

Setting up Florida small business health insurance takes five steps: determine eligibility and ALE status, decide on plan structure (traditional, level-funded, or ICHRA), set employer contribution percentages, gather employee census data, then work with a licensed Florida broker to compare carrier quotes. Florida small business group enrollment can happen year-round; most employers target January 1 or July 1 effective dates for budgeting and renewal alignment.

Confirm eligibility and FTE count

Florida small business group plans require at least 2 employees (in most cases including a non-owner W-2 employee). Calculate your 12-month average FTE count to determine if you’re under 50 FTEs (small group) or 50+ FTEs (ALE with mandate obligations). Sole proprietors generally don’t qualify for group plans.

Choose plan structure

Decide between traditional fully-insured group (predictable cost, capped risk), level-funded (refund potential for healthier groups), or ICHRA (employee reimbursement for individual plans). Each structure has different administrative loads, risk profiles, and employee experience implications.

Set contribution percentages

Decide how much of each employee’s premium your Florida business will contribute. The federal Small Business Health Care Tax Credit requires minimum 50% employer contribution. Florida market norms run 50-75% of employee-only premium and 25-50% of dependent premium.

Gather employee census

Carriers need employee demographics for quoting: ages, ZIP codes, gender, dependent status, and tobacco-use information. Document W-2 employment relationships — 1099 contractors generally don’t qualify for group inclusion. Census timing affects quote accuracy.

The fifth step is broker engagement and carrier comparison. A licensed Florida broker takes the census, contribution structure, and plan-type preferences from Steps 1-4 and shops the major Florida carriers for competitive quotes. Broker compensation is built into carrier premiums — working with a broker costs no more than enrolling directly. Per Florida Department of Financial Services agent verification, only Florida-licensed agents can quote and bind Florida group coverage.

Florida Small Business Health Insurance FAQs

Florida small business owners commonly ask about their best 2026 options, employer mandate requirements, cost ranges, the Florida SHOP marketplace, ICHRA structure, and how Aetna’s individual marketplace exit affects group coverage.

What are the best Florida small business health insurance options for 2026?

The best Florida small business health insurance options for 2026 depend on company size, budget, and how much administrative work the employer wants to manage. Traditional fully-insured group plans through Florida Blue, Cigna, UnitedHealthcare, Humana, or Aetna remain the dominant choice for 2-50 employee Florida businesses. Level-funded plans deliver group-like coverage with potential refunds for healthier-than-expected utilization. ICHRA lets Florida employers reimburse employees for individual marketplace plans instead of sponsoring a group plan.

Are Florida small businesses required to offer health insurance to employees?

Florida small businesses with fewer than 50 full-time equivalent (FTE) employees are not required to offer health insurance under the Affordable Care Act employer mandate. The ACA’s employer shared responsibility provision applies only to applicable large employers (ALEs) — businesses averaging 50+ full-time employees including FTE-equivalents from part-time staff. Florida has no separate state-level employer health insurance mandate beyond federal ACA rules. Voluntary offering remains common in competitive Florida labor markets including Miami-Dade, Broward, Hillsborough, and Orange counties.

How much does Florida small business health insurance cost in 2026?

Florida small business health insurance premiums for 2026 vary by carrier, plan type, employee demographics, and county. Traditional fully-insured group plans typically run $550-$850 monthly per employee for employee-only Silver coverage, $1,100-$1,650 for employee-plus-spouse, and $1,600-$2,400 for family coverage. Florida small business premiums increased an average of 12-18% for 2026 — substantially less than the 31.5% individual marketplace increase. Level-funded plans can run 10-25% below traditional group premiums for healthier-than-average groups.

What is the Florida SHOP marketplace?

The Florida SHOP (Small Business Health Options Program) is the federal marketplace path for Florida small businesses with 1-50 employees to purchase group health insurance. Florida SHOP operates through HealthCare.gov as part of the federally-facilitated marketplace. Florida small businesses can enroll in SHOP coverage year-round, with no fixed open enrollment window. SHOP enrollment may qualify Florida employers with fewer than 25 FTEs, average wages under $66,000, and contributing at least 50% of employee premiums for the federal Small Business Health Care Tax Credit, worth up to 50% of the employer’s premium contribution.

What is an ICHRA for Florida small business?

An Individual Coverage Health Reimbursement Arrangement (ICHRA) lets Florida employers reimburse employees tax-free for individual health insurance premiums and qualifying medical expenses instead of sponsoring a traditional group plan. Florida small businesses can offer ICHRA to all employees or specific employee classes (full-time, part-time, salaried, hourly, geographic), with reimbursement amounts varying by class. Employees use ICHRA dollars to buy plans on the Florida marketplace through HealthCare.gov.

Did Aetna’s Florida marketplace exit affect small business group plans?

No. Aetna’s December 31, 2025 exit from the Florida individual marketplace did not affect Aetna’s group small business and employer-sponsored coverage in Florida. Aetna group plans remain fully available to Florida employers through the small business and large group markets. The marketplace exit only affected individual ACA enrollees who purchased Aetna plans directly through HealthCare.gov — not employees on Aetna group plans through their Florida employer.

Get Florida Small Business Group Coverage Tailored to Your Team

A licensed Florida broker matches your business to the right group health insurance structure — traditional fully-insured, level-funded with refund potential, or ICHRA — with side-by-side comparison across Florida Blue, Cigna, UnitedHealthcare, Humana, and Aetna. Free, no obligation, no extra cost.

Florida Health Insurance Resources

Statewide pillar — HMO, PPO, EPO, metal tiers, all carriers, and 2026 marketplace changes

Best Health Insurance in FloridaTop-rated carriers ranked by cost, network, and overall value for 2026

Affordable Florida Health InsuranceSubsidies, CSR savings, and low-cost plan options for individuals and families

Short-Term Health Insurance FloridaTemporary and bridge coverage options for Floridians between plans

Private Medical Insurance FloridaOff-exchange Florida coverage for self-employed and above-400%-FPL households

Florida PPO Health InsurancePPO coverage options and provider flexibility — BlueCard nationwide network

Florida Health Insurance MarketplaceHealthCare.gov enrollment for ICHRA employees and individual coverage shoppers

Blue Cross Blue Shield of FloridaFlorida Blue group products including BlueOptions PPO and myBlue HMO across all 67 counties

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Florida businesses and employers. We are not affiliated with any carrier or government agency. We help you compare group plans and enroll in coverage that meets your team’s needs at no extra cost to you.