Affordable Health Insurance in California: Costs and Savings for 2026

Affordable health insurance in California depends on income level, age, ZIP code, and whether coverage is purchased through Covered California or directly from a carrier off-exchange. The 2026 plan year brought a 10.3% average rate increase, the largest since 2018, along with the expiration of enhanced federal premium tax credits that affected affordable health insurance California enrollees that had kept costs lower for nearly 1.7 million enrollees since 2021. California responded with $190 million in state-funded subsidies targeting the lowest-income residents, but most enrollees above 150% of the federal poverty level are paying more in 2026 than in the previous year. Understanding how premiums, subsidies, and plan structure interact is essential to finding affordable health insurance California residents can rely on.

How Much Does Health Insurance Cost in California in 2026?

The cost of affordable health insurance California carriers offer varies widely based on the metal tier selected, the enrollee’s age, and the pricing region. The average monthly premium for a 40-year-old individual on a Bronze plan is approximately $420 before subsidies, while Silver plans average $510 and Gold plans average $580 across the state’s major carriers.

| Metal Tier | Avg. Monthly Premium (Age 40) | Deductible Range | Out-of-Pocket Max |

|---|---|---|---|

| Bronze | $370–$440 | $5,500–$7,000 | $9,200 |

| Silver | $460–$560 | $2,500–$4,500 | $9,200 |

| Gold | $520–$620 | $0–$1,500 | $8,550 |

| Platinum | $620–$740 | $0 | $4,500 |

| Catastrophic (under 30) | $280–$340 | $9,200 | $9,200 |

Rates represent approximate ranges across major California carriers for a 40-year-old individual in 2026. Actual premiums vary by ZIP code, carrier, and specific plan design. Premium tax credits through Covered California reduce costs for eligible households.

Health Insurance Costs by Age in California

Age is one of the largest cost variables for affordable health insurance California residents compare, because the Affordable Care Act allows carriers to charge older enrollees up to three times more than younger enrollees for the same plan. The following table shows approximate monthly Silver plan premiums by age bracket before subsidies are applied.

| Age | Silver HMO (Approx.) | Silver PPO (Approx.) | Age Factor |

|---|---|---|---|

| 21 | $320–$370 | $360–$410 | 0.635× |

| 30 | $370–$420 | $410–$470 | 1.000× |

| 40 | $460–$530 | $510–$600 | 1.278× |

| 50 | $640–$740 | $710–$830 | 1.786× |

| 60 | $840–$970 | $930–$1,080 | 2.714× |

| 64 | $890–$1,030 | $990–$1,150 | 3.000× (maximum) |

Rates are approximate pre-subsidy monthly premiums. The age factor column shows the ACA age-rating ratio relative to a 30-year-old baseline. Subsidy amounts increase with age, partially offsetting higher premiums for older enrollees.

For residents comparing carriers and plan structures across age brackets, the best health insurance in California guide profiles all 11 Covered California carriers with quality ratings and network details.

Premium Tax Credits and Subsidies in California

Premium tax credits are the primary tool for making health insurance affordable in California for residents with household incomes between 138% and 400% of the federal poverty level (FPL). Credits are available only through Covered California, not for off-exchange plans, and reduce the monthly premium based on income relative to the cost of the benchmark Silver plan in each rating region.

Federal Premium Tax Credits

Income: 138%–400% FPL

Credits reduce monthly premiums on Covered California plans. The amount depends on income, household size, and the benchmark Silver plan cost in the enrollee’s region. Credits are applied monthly to reduce out-of-pocket premium costs or reconciled when filing federal taxes.

Cost-Sharing Reductions (CSR)

Income: Up to 250% FPL, Silver plans only

Available only on Silver-tier Covered California plans, CSRs lower deductibles, copays, and the out-of-pocket maximum. At 150% FPL, a Silver plan’s deductible may drop from $4,500 to under $500, making Silver the most cost-effective tier for lower-income enrollees.

California State Subsidies ($190M)

Income: Up to 150% FPL

California allocated $190 million in state funding for 2026 to keep premiums near 2025 levels for the lowest-income enrollees. This state program, unique to California, partially fills the gap left by the expiration of enhanced federal subsidies at the end of 2025.

Enhanced Subsidy Expiration Impact

Effective: January 1, 2026

The American Rescue Plan’s enhanced subsidies expired December 31, 2025, affecting approximately 1.7 million California enrollees. Without the enhanced credits, the average net premium increase for affected enrollees is 66% — though actual impact varies by income and region.

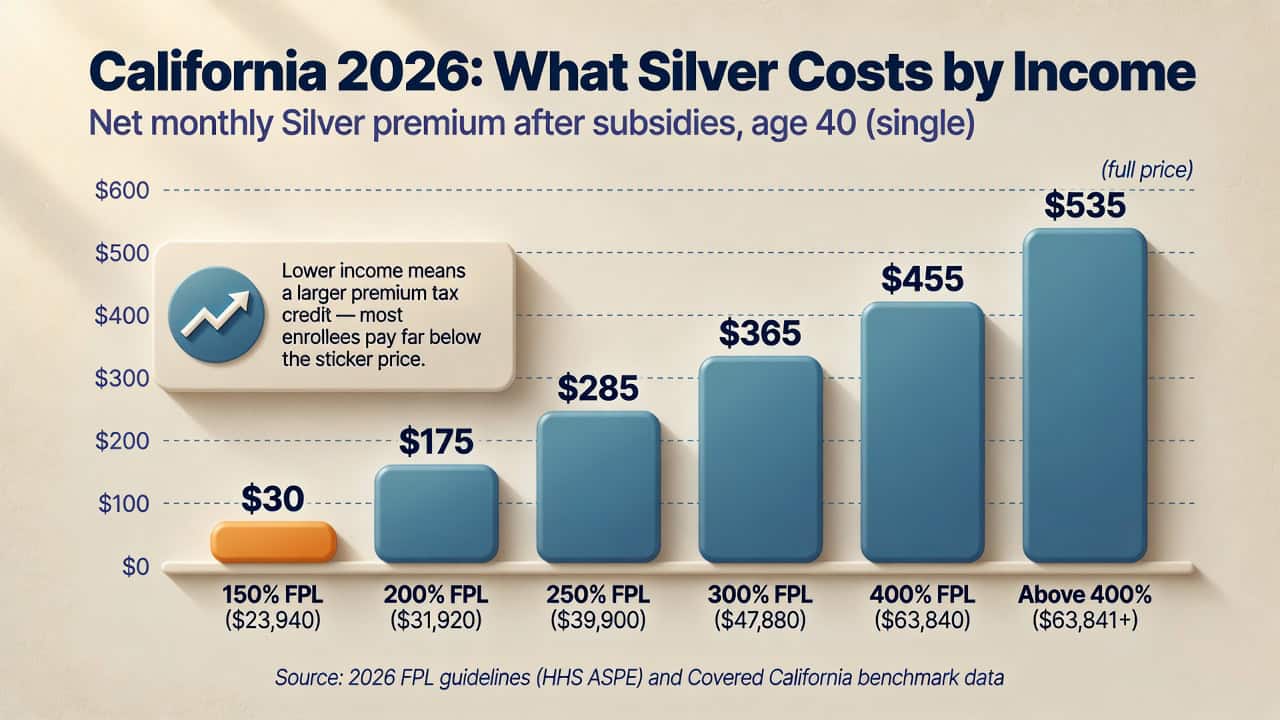

Affordability Snapshot: What Californians Actually Pay

At 150% FPL ($23,940 for a single filer), a Silver plan runs $10–$50 per month after federal credits and California’s $190 million state subsidy — against a $460–$560 sticker price. At 300% FPL ($47,880), the net Silver premium is $340–$390. Above 400% FPL ($63,841), subsidies stop entirely and the full $510–$560 applies.

⚠️ Important: The Subsidy Cliff Is Back for 2026

The enhanced subsidies have expired. Federal premium tax credits now end abruptly at 400% FPL ($63,840 for a single individual in 2026). An individual earning $63,000 may receive meaningful subsidies; an individual earning $64,000 receives nothing. A $1,000 income difference can cost thousands in additional annual premiums. Residents near this threshold should carefully estimate income and consult a licensed California agent before enrolling.

Subsidy Amounts by Income Level

The amount of affordable health insurance California residents receive through premium tax credits depends on household income measured against the federal poverty level. The following table shows approximate monthly subsidy amounts and net Silver plan costs for a 40-year-old individual at different income levels in 2026.

| Income (% FPL) | Annual Income (Single) | Approx. Monthly Subsidy | Net Silver Premium |

|---|---|---|---|

| 150% FPL | $23,940 | $440–$490 | $10–$50 (state subsidy helps) |

| 200% FPL | $31,920 | $310–$360 | $150–$200 |

| 250% FPL | $39,900 | $200–$250 | $260–$310 |

| 300% FPL | $47,880 | $120–$170 | $340–$390 |

| 400% FPL | $63,840 | $30–$80 | $430–$480 |

| Above 400% FPL | $63,841+ | $0 | $510–$560 (full price) |

Amounts are approximate for a 40-year-old individual. Actual subsidies depend on the benchmark Silver plan cost in the enrollee’s rating region. Family subsidies scale with household size. Data based on 2026 FPL guidelines from HHS ASPE.

Strategies to Lower Health Insurance Costs in California

Finding affordable health insurance California has available involves more than selecting the lowest-premium plan. The right strategy for affordable health insurance California residents pursue depends on income level, health care usage, and whether on-exchange or off-exchange enrollment makes more sense. Several strategies can reduce total costs by combining premium savings with lower out-of-pocket expenses, depending on income level, health care usage, and willingness to consider off-exchange options.

Silver Plan Switching

Consumers earning 150%–250% FPL should choose Silver plans to access cost-sharing reductions that dramatically lower deductibles and copays. At 150% FPL, a Silver plan’s effective deductible can drop below $500 — a benefit not available on any other metal tier.

Off-Exchange Shopping

Consumers above 400% FPL who receive no subsidies should compare off-exchange Silver PPO plans from Blue Shield and Anthem. Off-exchange Silver premiums avoid CSR cost loading, often $30–$50 per month cheaper than equivalent on-exchange Silver plans.

Income Management

Residents near the 400% FPL cliff can lower modified adjusted gross income through retirement contributions, HSA contributions (if on a qualifying HDHP), or business expense timing for self-employed individuals, potentially preserving subsidy eligibility worth thousands per year.

Agent-Assisted Comparison

A licensed California agent can compare plans across all 11 carriers, on-exchange and off-exchange, at no cost. Enrollment assistance identifies savings opportunities that online tools may miss, particularly the on-exchange vs. off-exchange PPO price gap.

Real-World Example: Unsubsidized Consultant in Sacramento

James, a 45-year-old consultant in Sacramento earning $68,000 per year, does not qualify for Covered California subsidies (income exceeds 400% FPL). On the exchange, a Silver HMO plan costs approximately $540 per month. A licensed agent identifies an off-exchange Blue Shield Silver 2600 PPO at $495 per month, $45 less without CSR loading, plus PPO flexibility for specialist visits without referrals. Annual savings: $540 with broader provider access. The California PPO health insurance guide details these off-exchange plan options.

Compare Affordable Plans for Your ZIP Code

Health insurance costs vary by ZIP code, age, and income across California’s 19 rating regions. Enter your details to see actual 2026 pricing with subsidy estimates, including off-exchange PPO options not shown on Covered California.

HMO vs. PPO: Cost Comparison in California

Plan structure affects affordability beyond just the monthly premium. HMO plans from carriers like Kaiser Permanente generally cost less per month than PPO plans from Blue Shield and Anthem, but PPO plans offer specialist access without referrals and out-of-network coverage that may reduce total costs for consumers who need frequent specialist care or travel regularly.

| Cost Factor | Silver HMO (Typical) | Silver PPO (Typical) |

|---|---|---|

| Monthly premium (age 40) | $460–$530 | $510–$600 |

| Deductible | $2,500–$4,000 | $2,600–$4,500 |

| Specialist copay | $55–$75 (with referral) | $50–$70 (no referral needed) |

| Out-of-network coverage | None (except emergencies) | Yes (at higher cost share) |

| Annual premium difference | Baseline | +$600–$840 per year |

| Off-exchange Silver advantage | N/A | $30–$50/mo savings (no CSR loading) |

For consumers who do not receive subsidies, the off-exchange Silver PPO savings can narrow or eliminate the HMO vs. PPO premium gap, making PPO plans cost-competitive while providing greater flexibility. The individual health insurance California guide covers plan selection by income pathway in more detail.

Additional Resources for Affordable Coverage

Beyond Covered California plans, several state programs supplement affordable health insurance California residents access for specific populations. These resources supplement marketplace coverage for residents who need additional assistance reducing costs.

Medi-Cal (Medicaid)

Free or very low-cost coverage for residents earning up to 138% FPL (~$22,025 for a single individual). Covers comprehensive benefits including doctor visits, prescriptions, hospital stays, and mental health. Apply through Covered California or county social services offices.

CA SHIP (State Health Insurance Assistance)

Free counseling and assistance for Medicare-eligible Californians through the Health Insurance Counseling and Advocacy Program (HICAP). Helps with Medicare enrollment, plan comparisons, and appeals. Call 1-800-434-0222 for assistance.

Covered California Tax Credits

The state exchange is the only pathway to federal premium tax credits and cost-sharing reductions. Residents who have not checked eligibility should use the Covered California calculator or contact a licensed agent to determine whether subsidies would lower their costs.

Mandate Exemptions

Residents for whom the lowest-cost Bronze plan exceeds 8.05% of household income may qualify for a mandate exemption, avoiding the penalty for going uninsured. The California Franchise Tax Board determines exemption eligibility at tax filing.

Frequently Asked Questions About Affordable Health Insurance in California

The following questions address the most common concerns about affordable health insurance California residents face, including costs, subsidies, off-exchange savings, and strategies for lowering premiums during the 2026 plan year.

What is the average cost of health insurance in California in 2026?

The average monthly premium for an individual Bronze plan is approximately $420 before subsidies, Silver approximately $510, and Gold approximately $580 for a 40-year-old. Actual costs vary significantly by carrier, rating region, and age. Subsidy-eligible consumers pay substantially less, some as little as $10–$50 per month for Silver coverage at the lowest income levels.

What happened to the enhanced health insurance subsidies in California?

The enhanced premium tax credits introduced by the American Rescue Plan in 2021 and extended through the Inflation Reduction Act expired on December 31, 2025. Without these enhanced credits, approximately 1.7 million California enrollees face higher premiums in 2026, an average net increase of 66% for those who previously received enhanced assistance. California’s $190 million state subsidy program partially offsets this for enrollees earning up to 150% FPL.

Are off-exchange plans cheaper than Covered California plans?

For consumers who do not qualify for subsidies, off-exchange Silver PPO plans from Blue Shield and Anthem are often cheaper than equivalent on-exchange Silver plans. On-exchange Silver premiums include cost-sharing reduction (CSR) loading, an added cost that subsidizes lower-income enrollees. Off-exchange plans do not carry this loading, producing Silver-tier savings of approximately $30–$50 per month. This advantage applies only at the Silver tier and only for unsubsidized consumers.

How do I qualify for Medi-Cal in California?

California residents with household incomes up to 138% of the federal poverty level — approximately $22,025 per year for a single individual in 2026 and generally qualify for Medi-Cal. Applications can be submitted through Covered California, directly through county social services offices, or by calling 1-800-300-1506. Medi-Cal provides comprehensive coverage at little or no cost to enrollees.

Is it cheaper to get health insurance through Covered California or directly?

The answer depends on income. Consumers who qualify for premium tax credits (income between 138% and 400% FPL) should enroll through Covered California because subsidies are only available on-exchange. Consumers above 400% FPL who receive no subsidies should compare off-exchange options, particularly Silver PPO plans, where premiums may be lower. A licensed agent can run both comparisons at no cost.

What is the California individual mandate penalty for 2026?

For the 2025 tax year (filed in 2026), the penalty is the greater of $950 per uninsured adult plus $475 per uninsured child, or 2.5% of gross household income above the filing threshold. In many cases, the cost of a subsidized Bronze plan is less than the penalty, making enrollment the more affordable option even for healthy consumers who rarely use care.

Related California Health Insurance Resources

Explore the rest of the California coverage library for carrier comparisons, enrollment pathways, and free help choosing a 2026 plan.

Complete 2026 guide to coverage options, enrollment, and subsidies.

Best Health Insurance in CaliforniaCarrier comparisons, quality ratings, and network details.

Individual Health InsuranceSelf-employed coverage, mandate details, and plan selection.

Find a California AgentFree enrollment help from licensed professionals.

Find Affordable Health Insurance in California

See actual 2026 plan pricing and subsidy estimates for your ZIP code, including off-exchange PPO options that Covered California does not display. Enter your details below or call for free, personalized enrollment help at no cost to you.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving California residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.