Individual Health Insurance Plans in California for 2026

Individual health insurance plans California residents can choose from are available through the Covered California exchange, directly from carriers off-exchange, or through public programs like Medi-Cal for those who meet income requirements. California’s individual market stands apart from most states: a state-level mandate requires all residents to carry qualifying coverage, the exchange offers 11 carriers with both HMO and PPO plan types, and an off-exchange market where Blue Shield and Anthem PPO plans may be less expensive than equivalent on-exchange options for consumers who do not receive subsidies. For self-employed Californians and others purchasing coverage on their own, understanding how income level affects both plan choices and costs is the most important first step.

How Individual Health Insurance Works in California

Individual health insurance plans California residents purchase cover people without employer coverage, a spouse’s employer plan, Medicare, or Medi-Cal. This includes self-employed professionals, freelancers, gig workers, early retirees, and anyone between jobs who needs individual health insurance California provides outside of employer coverage. Covered California, the state’s exchange, offers subsidized plans from 11 carriers, while off-exchange plans provide additional options for residents who earn above subsidy thresholds.

Unlike states that use the federal HealthCare.gov platform, California operates its own marketplace with independent enrollment deadlines and carrier negotiations. Open enrollment for the 2026 plan year ran from November 1, 2025 through January 31, 2026. Outside of open enrollment, residents can only enroll or change plans through a qualifying life event that triggers a special enrollment period.

California also enforces a state-level individual mandate, meaning residents face a tax penalty for going without qualifying health coverage. This mandate, separate from the federal individual mandate that was effectively eliminated in 2019, adds financial urgency to enrollment decisions and makes California one of only a handful of states where maintaining coverage is legally required.

California’s Individual Mandate and Penalty

California requires all residents to maintain qualifying health insurance coverage or pay a penalty when filing state income taxes. The California Franchise Tax Board (FTB) assesses the penalty, which for the 2025 tax year (filed in 2026) is the greater of two calculations.

| Penalty Method | Calculation | Example (Single Adult) |

|---|---|---|

| Flat dollar amount | $950 per uninsured adult + $475 per uninsured child | $950 |

| Percentage of income | 2.5% of gross household income above filing threshold | $1,125 (at $65,000 income) |

| Applied penalty | Whichever method produces the higher amount | $1,125 (percentage is higher) |

Exemptions exist for residents who cannot afford coverage (where the lowest-cost Bronze plan exceeds 8.05% of household income), those with religious exemptions, members of health care sharing ministries, and certain other categories. The FTB determines exemption eligibility when the tax return is filed.

Mandate Impact for Individuals

The penalty creates a financial floor: for many Californians, the cost of a subsidized Bronze plan through Covered California is less than the penalty itself. Residents considering going without coverage should compare the penalty amount against actual plan costs before making that decision. A licensed California agent can calculate both figures at no cost.

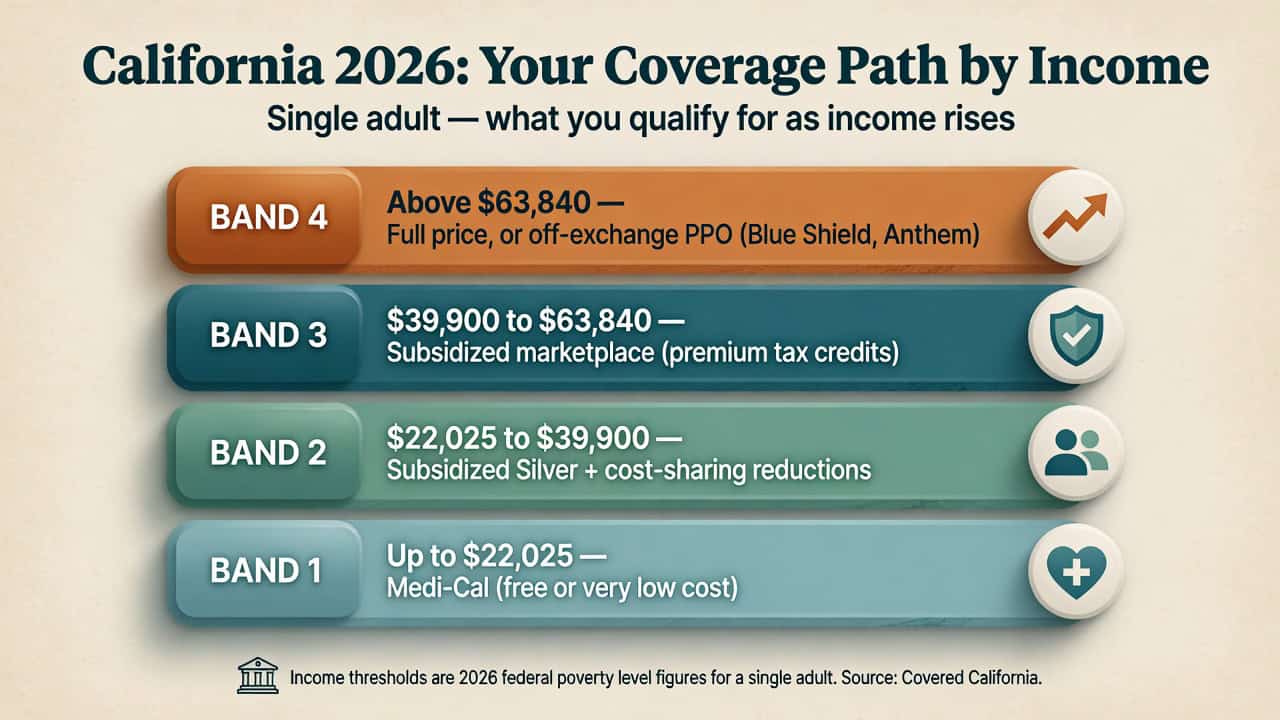

Income Pathways: Finding the Right Individual Plan

The most important factor when evaluating individual health insurance plans California residents choose is household income relative to the federal poverty level (FPL). Income determines whether a resident qualifies for Medi-Cal, subsidized exchange coverage, or should consider off-exchange options. The difference between these pathways can mean hundreds of dollars per month in premium costs.

Medi-Cal (Up to 138% FPL)

Income: Up to ~$22,025/year (single)

Free or very low-cost comprehensive coverage through California’s Medicaid program. Covers doctor visits, prescriptions, hospital stays, mental health, and more. Apply through Covered California or county social services. No monthly premium for most enrollees.

Subsidized Exchange (138%–400% FPL)

Income: ~$22,025–$63,840/year (single)

Premium tax credits reduce monthly costs on Covered California plans. Silver plans also offer cost-sharing reductions for incomes up to 250% FPL ($39,900), lowering deductibles and copays. State subsidies add extra help for incomes up to 150% FPL.

Full-Price Exchange (Above 400% FPL)

Income: Above ~$63,840/year (single)

No premium tax credits. Covered California plans available at full price. At this income level, comparing on-exchange and off-exchange options is essential. Off-exchange Silver PPOs from Blue Shield and Anthem often cost less due to the absence of CSR loading.

Off-Exchange PPO

Income: Above subsidy threshold

Blue Shield Silver 2600 and Silver 1750 PPO plans, exclusive to off-exchange enrollment, may carry lower premiums than on-exchange Silver for consumers who do not receive subsidies. These plans provide specialist access without referrals and partial out-of-network coverage. The California PPO health insurance guide compares specific plan details.

For a detailed breakdown of costs by metal tier and income level, including subsidy calculations and cost-saving strategies, the affordable health insurance California guide provides comprehensive pricing comparisons.

Individual Health Insurance for Self-Employed Californians

Self-employed residents, freelancers, independent contractors, and gig workers make up a significant share of the market for individual health insurance plans California provides. These residents purchase coverage on their own rather than through an employer, making them eligible for Covered California subsidies and the full range of plan options including off-exchange PPOs.

Self-employed Californians have a specific tax advantage: health insurance premiums paid for individual coverage are deductible on federal income tax returns as an above-the-line deduction (not an itemized deduction). This applies to premiums paid for the self-employed individual, their spouse, and dependents, reducing adjusted gross income and potentially affecting premium tax credit eligibility. The IRS Form 7206 instructions specify that the deduction cannot exceed the business’s net profit for the year.

Income estimation is particularly important for self-employed individuals because Covered California subsidies are based on projected annual income, which can fluctuate for freelancers and contractors. Overestimating income may result in smaller monthly subsidies than deserved, while underestimating may require repayment when filing taxes. Quarterly income reviews and mid-year Covered California updates can help keep subsidy amounts accurate.

Real-World Example: Freelance Developer in San Francisco

Sarah, a 34-year-old freelance web developer in San Francisco, estimates her 2026 income at $58,000, qualifying her for premium tax credits at approximately 363% of the federal poverty level. She qualifies for approximately $180 per month in premium tax credits through Covered California, reducing her Silver HMO plan from $530 to $350 per month. She also deducts her full $4,200 annual premium cost on her federal tax return, reducing her taxable income. If her income rises above $63,840, she would lose subsidy eligibility and should compare an off-exchange Blue Shield Silver PPO at approximately $510 per month against the now-unsubsidized on-exchange Silver HMO at $530.

Qualifying Life Events for Individual Enrollment

Outside of open enrollment, California residents can enroll in individual health insurance plans through a special enrollment period triggered by a qualifying life event (QLE). These events create a 60-day enrollment window during which residents can select a new plan through Covered California or enroll off-exchange.

Loss of Coverage

- Losing employer-sponsored health insurance

- Aging off a parent’s plan at 26

- COBRA coverage expiring

- Losing Medi-Cal eligibility

- Divorce ending spousal coverage

Life Changes

- Getting married or entering a domestic partnership

- Having or adopting a baby

- Moving to a new county or ZIP code

- Becoming a U.S. citizen or gaining lawful presence

- Release from incarceration

Income Changes

- Income dropping below 150% FPL (may newly qualify for Medi-Cal)

- Losing eligibility for employer coverage that becomes unaffordable

- Gaining or losing eligibility for premium tax credits

Other Events

- Becoming a member of a federally recognized tribe

- A court order requiring health coverage

- Gaining access to new individual market plans due to a permanent move

Residents who miss open enrollment and do not have a qualifying life event cannot enroll in an individual plan until the next open enrollment period. For those in coverage gaps, California’s ban on short-term insurance means ACA-compliant plans are the only available option. The short-term health insurance options in California covers alternative strategies for residents between coverage periods.

Individual Plan Options: COBRA vs. ACA Coverage

Californians who lose employer-sponsored coverage face a choice between COBRA continuation and enrolling in individual health insurance plans California has available through Covered California or off-exchange. COBRA allows continuation of the employer plan for up to 18 months, but at full cost plus a 2% administrative fee, making it significantly more expensive in most cases.

| Factor | COBRA | Individual ACA Plan |

|---|---|---|

| Monthly cost (typical) | $600–$750+ (full employer premium + 2%) | $350–$530 (before subsidies) |

| Subsidy eligible? | No | Yes (if income qualifies) |

| Duration | Up to 18 months | Renewable annually |

| Network | Same as employer plan | Carrier-specific; varies by plan |

| PPO available? | Depends on employer plan | Yes — Blue Shield, Anthem (on + off-exchange) |

| Best for | Mid-treatment patients who need provider continuity | Most people — especially subsidy-eligible |

Losing employer coverage is itself a qualifying life event, so residents can enroll in a Covered California plan within 60 days of the loss. In most cases, an individual ACA plan, especially with premium tax credits, costs substantially less than COBRA while providing comparable or better coverage. The exception is when a resident is mid-treatment with a provider in the employer plan’s network but not in any available individual plan network.

Compare Individual Plans for Your ZIP Code

Individual plan costs and subsidy amounts vary by ZIP code, income, and household size across California’s 19 rating regions. Enter your details to see actual 2026 pricing, including off-exchange PPO options not shown on Covered California.

How to Choose an Individual Health Insurance Plan

Selecting from the individual health insurance plans California has available requires evaluating several factors beyond the monthly premium. The following steps provide a structured approach based on personal health needs, financial situation, and provider preferences.

Estimate Your Income

Determine projected household income for the coverage year to identify whether you qualify for Medi-Cal, premium tax credits, or should focus on off-exchange options. Self-employed residents should use expected net business income after deductions.

Choose a Metal Tier

Bronze plans have the lowest premiums but highest out-of-pocket costs. Silver plans offer the best value for subsidy-eligible consumers. Gold and Platinum plans suit residents who use care frequently and prefer predictable costs throughout the year.

Decide HMO vs. PPO

HMO plans cost less but require referrals and limit provider choice. PPO plans from Blue Shield and Anthem allow specialist visits without referrals and provide out-of-network coverage, ideal for residents who travel or need provider flexibility.

Get Professional Help

A licensed California health insurance agent can compare plans across all 11 carriers, both on Covered California and off-exchange, at no cost. Enrollment assistance calculates exact subsidy amounts and identifies on vs. off-exchange savings opportunities.

For detailed carrier comparisons, quality ratings, and network information, the best health insurance in California guide profiles all 11 Covered California carriers.

Frequently Asked Questions About Individual Health Insurance in California

The following questions address common concerns about individual health insurance plans California residents face when purchasing coverage, including mandate penalties, self-employment deductions, qualifying life events, and plan options for the 2026 coverage year.

What is the penalty for not having health insurance in California?

The California individual mandate penalty for the 2025 tax year (filed in 2026) is the greater of $950 per uninsured adult and $475 per child, or 2.5% of gross household income above the filing threshold. The penalty is assessed by the California Franchise Tax Board and is collected through the state income tax return. Exemptions are available for residents who cannot find affordable coverage or meet other qualifying criteria.

Can self-employed Californians deduct health insurance premiums?

Yes. Self-employed individuals can deduct health insurance premiums as an above-the-line deduction on their federal income tax return. This applies to premiums paid for the self-employed person, their spouse, and dependents. The deduction cannot exceed the business’s net profit for the year and is not available for months when the individual was eligible for employer-sponsored coverage through a spouse or other source.

Is COBRA or an individual plan better after losing a job in California?

For most Californians, individual health insurance plans California offers through Covered California cost less than COBRA, especially for those who qualify for premium tax credits. COBRA requires paying the full employer premium plus a 2% administrative fee with no subsidy eligibility. The main reason to choose COBRA is to maintain continuity with a specific provider who does not participate in any available individual plan network, particularly important for residents mid-treatment.

Can individual health insurance plans California offers include PPO options?

Yes. Blue Shield of California and Anthem Blue Cross offer PPO plans both on the Covered California exchange and off-exchange. Off-exchange Silver PPO plans, including Blue Shield’s exclusive Silver 2600 and Silver 1750 products, may carry lower premiums than on-exchange Silver for consumers who do not receive subsidies, because off-exchange Silver plans do not include cost-sharing reduction loading.

What qualifies as a life event for special enrollment in California?

Qualifying life events include losing employer coverage, getting married, having or adopting a baby, moving to a new county, aging off a parent’s plan at 26, divorce, gaining citizenship, and certain income changes. Each event opens a 60-day special enrollment window during which residents can enroll in a Covered California plan or an off-exchange individual plan.

How do I estimate income for Covered California subsidies if I am self-employed?

Self-employed individuals should estimate net business income (gross revenue minus business expenses) for the coverage year. Covered California uses modified adjusted gross income (MAGI) for subsidy calculations. Because freelance income can fluctuate, mid-year income updates through Covered California help keep subsidy amounts accurate and reduce the risk of owing money back at tax time.

Related California Health Insurance Resources

Explore the rest of the California coverage library for carrier comparisons, cost breakdowns, and free help enrolling in a 2026 plan.

Complete 2026 guide to coverage options, enrollment, and subsidies.

Best Health Insurance in CaliforniaCarrier comparisons, quality ratings, and network details.

Affordable California CoverageCost breakdowns, subsidy strategies, and savings tips.

Find a California AgentFree enrollment help from licensed professionals.

Compare Individual Health Insurance Plans in California

See actual 2026 plan pricing for your ZIP code and income level, including off-exchange PPO options that Covered California does not display alongside your subsidy estimate. Enter your details below or call for free, no-obligation enrollment help.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving California residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.