Best Health Insurance in California: Top Companies for 2026

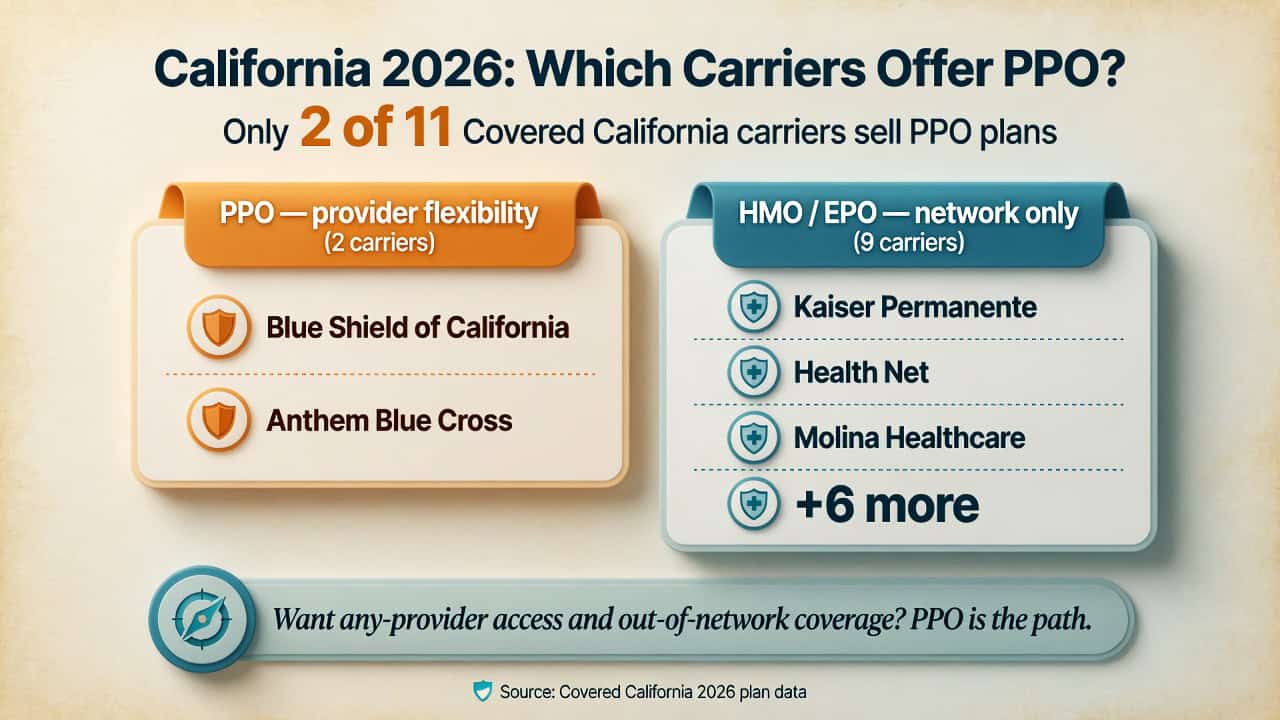

Eleven insurance companies offer individual and family health insurance plans through Covered California for the 2026 plan year, with additional carriers available off-exchange. The best health insurance in California for a given resident depends on location, budget, preferred doctors, and whether HMO or PPO plan structure is more important. Blue Shield of California and Anthem Blue Cross are the only carriers offering PPO plans, available both on the Covered California exchange and off-exchange, while Kaiser Permanente consistently earns the highest quality ratings among HMO carriers. California’s 19 pricing regions mean that carrier availability and costs vary significantly across the state, making carrier comparison essential before enrolling.

Top Health Insurance Companies in California for 2026

Determining the best health insurance in California starts with understanding the 11 carriers on the Covered California exchange, ranging from large national insurers to regional health plans. Each carrier receives quality ratings from the National Committee for Quality Assurance (NCQA), and the California Department of Insurance tracks consumer complaint ratios. The following three carriers illustrate the core choice California residents face: PPO flexibility versus HMO cost savings.

Blue Shield of California — PPO & HMO

Plan types: PPO, Trio HMO

Network: Large statewide PPO network

Key distinction: Only carrier offering exclusive off-exchange Silver PPO plans (Silver 2600 and Silver 1750) not available through Covered California. Off-exchange Silver PPO premiums are often lower than on-exchange Silver plans because they do not include cost-sharing reduction (CSR) loading.

Best for: Consumers who want PPO flexibility with specialist access and partial out-of-network coverage, or those who earn too much for subsidies and want lower Silver-tier pricing off-exchange.

Status: Nonprofit insurer

Anthem Blue Cross — PPO & HMO

Plan types: PPO, HMO

Network: Extensive statewide network

Key distinction: Received NCQA Health Equity Accreditation in August 2025. Offers PPO plans both on Covered California and off-exchange, providing a second PPO option alongside Blue Shield.

Best for: Consumers who want PPO access with a large provider network and strong brand backing, or those in regions where Blue Shield PPO availability is limited.

Status: For-profit insurer (Elevance Health subsidiary)

Kaiser Permanente — HMO Only

Plan types: HMO (integrated model)

Network: Kaiser-owned facilities only

Key distinction: Integrated care model where insurance and medical facilities operate as one system, often producing well-coordinated care with lower premiums but requiring all services within the Kaiser network except emergencies.

Best for: Consumers who prefer lower premiums, coordinated care, and do not need out-of-network flexibility or specialist access without referrals.

Status: Nonprofit insurer

All 11 Covered California Carriers Compared

The full Covered California carrier roster for 2026 includes both statewide and regional health plans, and choosing the best health insurance in California often means considering regional carriers alongside the major names. Not every carrier is available in every county; California’s 19 pricing regions determine which carriers residents can access. The California Department of Insurance maintains a complete list of licensed health insurers and consumer complaint data for each carrier.

| Carrier | Plan Types | Coverage Area | PPO Available? |

|---|---|---|---|

| Blue Shield of California | PPO, Trio HMO | Statewide | Yes (on + off-exchange) |

| Anthem Blue Cross | PPO, HMO | Statewide | Yes (on + off-exchange) |

| Kaiser Permanente | HMO | Statewide (major metros) | No |

| Health Net | HMO, EPO | Statewide | No |

| Molina Healthcare | HMO | Most regions | No |

| Balance by CCHP | HMO | SF Bay Area (Region 4) | No |

| Inland Empire Health Plan | HMO | Riverside, San Bernardino | No |

| L.A. Care Health Plan | HMO | Los Angeles County | No |

| Sharp Health Plan | HMO | San Diego County | No |

| Valley Health Plan | HMO | Santa Clara County | No |

| Western Health Advantage | HMO | Sacramento, Northern CA | No |

2026 Carrier Change — Aetna Exit

Aetna exited Covered California for the 2026 plan year, displacing approximately 21,000 enrollees in Regions 3, 5, 6, and 11. Former Aetna members were given the choice to select a new carrier or be automatically transitioned to the lowest-cost plan in the same metal tier. A licensed California agent can help identify comparable plan alternatives from the remaining carriers.

HMO vs. PPO vs. EPO: Plan Types in California

The most important structural decision when choosing the best health insurance in California is selecting between HMO, PPO, and EPO plan types. Each structure has different rules around provider access, referral requirements, and out-of-network coverage that directly affect both monthly premiums and how care is accessed. Blue Shield of California and Anthem Blue Cross are the only two Covered California carriers offering PPO plans, while the remaining nine carriers offer only HMO or EPO options.

| Feature | HMO | PPO | EPO |

|---|---|---|---|

| Primary care physician required? | Yes | No | Varies |

| Referrals for specialists? | Usually required | Not required | Usually not required |

| Out-of-network coverage? | No (except emergencies) | Yes (at higher cost) | No (except emergencies) |

| Monthly premiums (typical) | Lower | Higher | Moderate |

| Provider network size | Smaller, defined | Larger, flexible | Moderate |

| CA carriers offering this type | All 11 | Blue Shield, Anthem | Health Net |

| Available off-exchange? | Yes | Yes (includes exclusive Silver PPOs) | Limited |

The HealthCare.gov glossary provides official definitions for each plan type. For a detailed look at California PPO plan options, including off-exchange Silver PPO products not available through Covered California, the California PPO health insurance guide compares Blue Shield and Anthem PPO plans by metal tier, premium, and network size.

PPO plan structure works the same way across state lines, so residents comparing California options against what is sold elsewhere can review the national PPO health insurance resource for how referral-free specialist access and out-of-network benefits are structured nationwide.

Which California Health Insurance Is Best for Your Situation?

The best health insurance in California depends on individual circumstances rather than a single universal ranking. A carrier that works well for a healthy 28-year-old freelancer in San Francisco may be a poor fit for a 55-year-old with chronic conditions in Fresno. The following recommendations match common California resident situations with the carrier and plan structure most likely to meet their needs.

Families with Children

Top pick: Kaiser Permanente (HMO) or Blue Shield PPO

Kaiser’s integrated pediatric care and low copays make it a strong choice for families who live near Kaiser facilities. Families needing specialist access for a child without referrals may prefer a Blue Shield PPO, particularly those with children seeing out-of-network pediatric specialists.

Self-Employed / Freelancers

Top pick: Blue Shield Silver PPO (off-exchange)

Self-employed Californians earning above subsidy thresholds often save money on off-exchange Silver PPO plans, where premiums avoid CSR cost loading. The PPO structure also accommodates irregular schedules and travel without network restrictions.

Seniors (Under 65)

Top pick: Blue Shield or Anthem PPO

Californians approaching Medicare age typically have established specialist relationships. PPO plans allow continued access to those specialists without referrals and provide partial out-of-network coverage when traveling or relocating, both common concerns for this age group.

Budget-Conscious / Young Adults

Top pick: Molina Healthcare or Kaiser Bronze

Molina often has the lowest premiums on Covered California, making it a strong fit for healthy young adults who primarily need catastrophic protection. Kaiser Bronze plans also offer low premiums with access to preventive care at no cost.

Frequent Travelers

Top pick: Anthem Blue Cross PPO

Anthem’s nationwide PPO network through the Blue Cross Blue Shield Association provides coverage across all 50 states, making it the strongest choice for Californians who travel frequently for work or split time between states.

Chronic Conditions / Specialists

Top pick: Blue Shield PPO or Kaiser Gold/Platinum

Consumers managing chronic conditions benefit from either a PPO’s unrestricted specialist access or Kaiser’s coordinated care model, depending on whether current specialists are in the Kaiser network. Gold or Platinum tiers reduce ongoing out-of-pocket costs.

California Health Insurance Costs by Carrier and Metal Tier

Monthly premiums in California vary by carrier, metal tier (Bronze, Silver, Gold, Platinum), age, and pricing region. Finding the best health insurance in California at the right price requires comparing across all of these variables. The 2026 plan year brought a 10.3% average rate increase, the largest since 2018, though individual carriers and regions varied. The following table shows approximate monthly premiums for a 40-year-old across major carriers.

| Carrier | Bronze | Silver | Gold | Platinum |

|---|---|---|---|---|

| Kaiser Permanente | $370–$420 | $460–$530 | $520–$590 | $600–$680 |

| Blue Shield (HMO) | $380–$440 | $470–$550 | $530–$610 | $620–$700 |

| Blue Shield (PPO) | $420–$490 | $510–$600 | $580–$660 | $670–$750 |

| Anthem Blue Cross (PPO) | $410–$480 | $500–$580 | $570–$650 | $660–$740 |

| Health Net | $360–$410 | $450–$520 | $510–$580 | $590–$670 |

| Molina Healthcare | $340–$390 | $430–$490 | $490–$560 | N/A |

Rates are approximate monthly premiums for a 40-year-old individual in 2026. Actual rates vary by ZIP code and rating region. Premium tax credits through Covered California reduce costs for eligible households.

For detailed cost comparisons, subsidy calculations, and strategies to find the best health insurance in California at the lowest price, the affordable health insurance California guide breaks down pricing by age bracket, metal tier, and income level.

Real-World Example: Self-Employed Graphic Designer in San Jose

Maria, a 42-year-old graphic designer in San Jose earning $65,000 per year, does not qualify for Covered California subsidies. By enrolling in a Blue Shield Silver 2600 PPO off-exchange instead of an on-exchange Silver HMO, she saves approximately $45 per month because the off-exchange Silver PPO does not include CSR cost loading, and gains PPO flexibility to see specialists without referrals. Over 12 months, that adds up to $540 in savings with broader provider access.

See California Plan Pricing for Your ZIP Code

Plan costs and carrier availability depend on your ZIP code, age, and income. Enter your details to see actual 2026 pricing, including off-exchange PPO options from Blue Shield and Anthem not shown on Covered California.

How to Choose the Best Health Insurance Company in California

Choosing the best health insurance in California among 11 carriers across 19 pricing regions requires a structured approach rather than simply picking the lowest premium. The following steps help California residents narrow down the best carrier for their specific situation, starting with the most important factor of whether preferred doctors are in-network, then working through cost, plan type, and quality considerations.

1. Verify Provider Networks

Search each carrier’s provider directory to confirm that current doctors, specialists, and preferred hospitals participate. Network availability varies by region; a carrier with strong coverage in the Bay Area may have thin networks in the Central Valley.

2. Decide HMO vs. PPO

Determine whether referral-free specialist access and out-of-network coverage are worth the higher PPO premium. Consumers who see specialists regularly or travel frequently often benefit from PPO plans through Blue Shield or Anthem.

3. Compare Total Annual Costs

Look beyond monthly premiums to include deductibles, copays, coinsurance, and the out-of-pocket maximum. A Bronze plan with a $7,000 deductible may cost more overall than a Silver plan with a $3,500 deductible for consumers who use care regularly.

4. Check Prescription Coverage

Review each carrier’s drug formulary to verify that current medications are covered and note which cost tier they fall under. Drug costs and formulary placement vary significantly between California carriers.

5. Evaluate On vs. Off-Exchange

Consumers earning above subsidy thresholds should compare off-exchange plans, especially Silver PPOs, where premiums may be lower. Those who qualify for premium tax credits must enroll through Covered California to receive them.

6. Get Free Expert Help

A licensed California health insurance agent can compare plans across all 11 carriers at no cost and help navigate the on-exchange versus off-exchange decision, including off-exchange PPO options not shown on Covered California.

California Health Insurance Quality Ratings and Complaints

Quality metrics from independent rating organizations provide an objective layer of comparison when evaluating the best health insurance companies in California beyond plan costs and network size. CMS quality ratings and NCQA health plan accreditation evaluate carriers on clinical outcomes, member satisfaction, and administrative efficiency. The California Department of Insurance also publishes complaint ratios, measured as the number of complaints per 100,000 covered lives, which can reveal patterns in billing disputes, claims denials, and customer service issues.

| Carrier | NCQA Accreditation | Relative Complaint Level | Notable Quality Factor |

|---|---|---|---|

| Kaiser Permanente | Accredited | Below average | Consistently high quality scores; integrated care model |

| Blue Shield of California | Accredited | Average | Nonprofit; large PPO network |

| Anthem Blue Cross | Accredited | Average | NCQA Health Equity Accreditation (August 2025) |

| Health Net | Accredited | Above average | Large statewide HMO/EPO presence |

| Molina Healthcare | Accredited | Above average | Lowest premiums; Medi-Cal managed care background |

| L.A. Care | Accredited | Average | Largest public health plan in U.S.; LA County focused |

Complaint levels represent relative positioning among California carriers based on California Department of Insurance data. “Below average” indicates fewer complaints per enrollee than the carrier average.

Important Context: Reading Quality Ratings

Complaint ratios reflect customer service and claims handling patterns but do not measure clinical quality directly. A carrier with a higher complaint ratio may still deliver excellent medical care. Similarly, low premiums do not indicate lower quality. Molina Healthcare and Kaiser Permanente both have competitive pricing but very different care models. The best health insurance in California balances quality ratings, network fit, and total annual costs rather than relying on any single metric.

Frequently Asked Questions About the Best California Health Insurance

The following questions address the most common concerns California residents have when comparing health insurance carriers, evaluating plan types, and selecting the best health insurance company in California for the 2026 plan year.

Which California health insurance company has the best ratings?

Kaiser Permanente consistently receives the highest quality scores from NCQA among California health insurance carriers, reflecting its integrated care model where insurance and medical services operate under one system. However, Kaiser is an HMO, and residents searching for the best health insurance in California with PPO flexibility should compare Blue Shield of California and Anthem Blue Cross, both of which hold NCQA accreditation and offer PPO plans on and off the Covered California exchange.

Is PPO or HMO better in California?

Neither plan type is universally better. The right choice depends on how care is accessed. PPO plans from Blue Shield and Anthem allow specialist visits without referrals and partial out-of-network coverage, making them better for consumers who see specialists regularly, travel frequently, or want maximum provider flexibility. HMO plans offer lower premiums and coordinated care, making them better for consumers who are comfortable with network restrictions and referral requirements.

Why are off-exchange PPO plans sometimes cheaper than Covered California plans?

On-exchange Silver plans include cost-sharing reduction (CSR) loading, an extra cost built into Silver premiums to offset the expense of providing CSR benefits to lower-income enrollees. Off-exchange Silver PPO plans from Blue Shield and Anthem do not include this CSR loading, which can make their Silver premiums noticeably lower for consumers who do not receive subsidies. This pricing difference only applies to the Silver tier.

What happened to Aetna in California for 2026?

Aetna exited the Covered California marketplace for the 2026 plan year, affecting approximately 21,000 enrollees across Regions 3, 5, 6, and 11. Displaced members were given the option to actively choose a new carrier or be automatically moved to the lowest-cost plan in the same metal tier. The remaining 11 carriers continue to provide coverage in those regions.

Can a broker help compare all California health insurance companies?

Yes. Licensed health insurance agents in California can compare plans across all 11 Covered California carriers as well as off-exchange options from Blue Shield and Anthem, making them a valuable resource for finding the best health insurance in California. They are compensated by the carrier, not the consumer, so their comparison services and enrollment assistance cost nothing extra.

Does California have a health insurance mandate?

Yes. California’s state-level individual mandate requires all residents to maintain qualifying health coverage. The penalty for the 2025 tax year (filed in 2026) is the greater of $950 per uninsured adult and $475 per child, or 2.5% of gross household income above the filing threshold. More details on the mandate and how it affects individual health insurance in California are available in the dedicated guide.

Related California Health Insurance Resources

California’s health insurance market includes coverage options for individuals, families, and businesses. These guides cover key pathways available to California residents and employers in 2026.

Complete 2026 guide to coverage options, enrollment, and subsidies.

Affordable California CoverageCost breakdowns by tier, subsidy strategies, and savings tips.

Individual Health InsuranceSelf-employed coverage, mandate details, and plan selection.

Find a California AgentFree enrollment help from licensed professionals.

Compare California Health Insurance Companies

See actual 2026 plan pricing for your ZIP code across all 11 Covered California carriers, plus the off-exchange PPO options from Blue Shield and Anthem. Enter your details below or call for free, personalized help.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving California residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.