Affordable Health Insurance Illinois 2026: Subsidies, CSR & Lowest-Cost Plans

Affordable health insurance in Illinois changed substantially for 2026. The enhanced federal premium tax credits that lowered marketplace costs through 2025 expired at the end of last year, pushing average premiums up roughly 50 percent. Most Illinois households still qualify for substantial subsidies, but the math is different — and choosing the right metal tier, carrier, and program matters more than it did under the enhanced subsidies. This guide breaks down every affordability lever on Get Covered Illinois, from Medicaid through unsubsidized off-exchange options.

What brings you here today?

I may qualify for Medicaid or All Kids

Free or near-free coverage for Illinois households

Check eligibility ↓The 2026 Affordability Reality in Illinois

Affordable health insurance Illinois shoppers found in 2025 looks different in 2026. The enhanced federal premium tax credits introduced in 2021 expired at the end of last year, and the original Affordable Care Act subsidy structure returned. Get Covered Illinois reported that without the enhancements, the average Illinois family pays roughly $130 per month more in 2026 — a year-over-year jump near 50 percent driven by the subsidy expiration.

The good news: most Illinois households still qualify for substantial subsidies. The original ACA premium tax credits remain in place, the 400 percent FPL cliff partially returns (with a narrower 8.5 percent of income cap above 400 percent), and the Silver cost-sharing reduction program continues unchanged. Medicaid covers Illinois adults up to 138 percent of FPL, and All Kids covers children up to 318 percent of FPL regardless of immigration status. The strategies that produce affordable Illinois coverage in 2026 are different from 2025, but they still exist.

⚠️ What changed in 2026

The enhanced subsidies that capped marketplace premiums at 8.5 percent of income for everyone — including households above 400 percent FPL — expired December 31, 2025. The original ACA subsidy curve is back: subsidy amounts scale from roughly 2 to 9.83 percent of income across FPL bands, with a narrower 8.5 percent cap that only kicks in if the benchmark Silver plan would otherwise cost more than that.

Premium Tax Credits and Who Still Qualifies

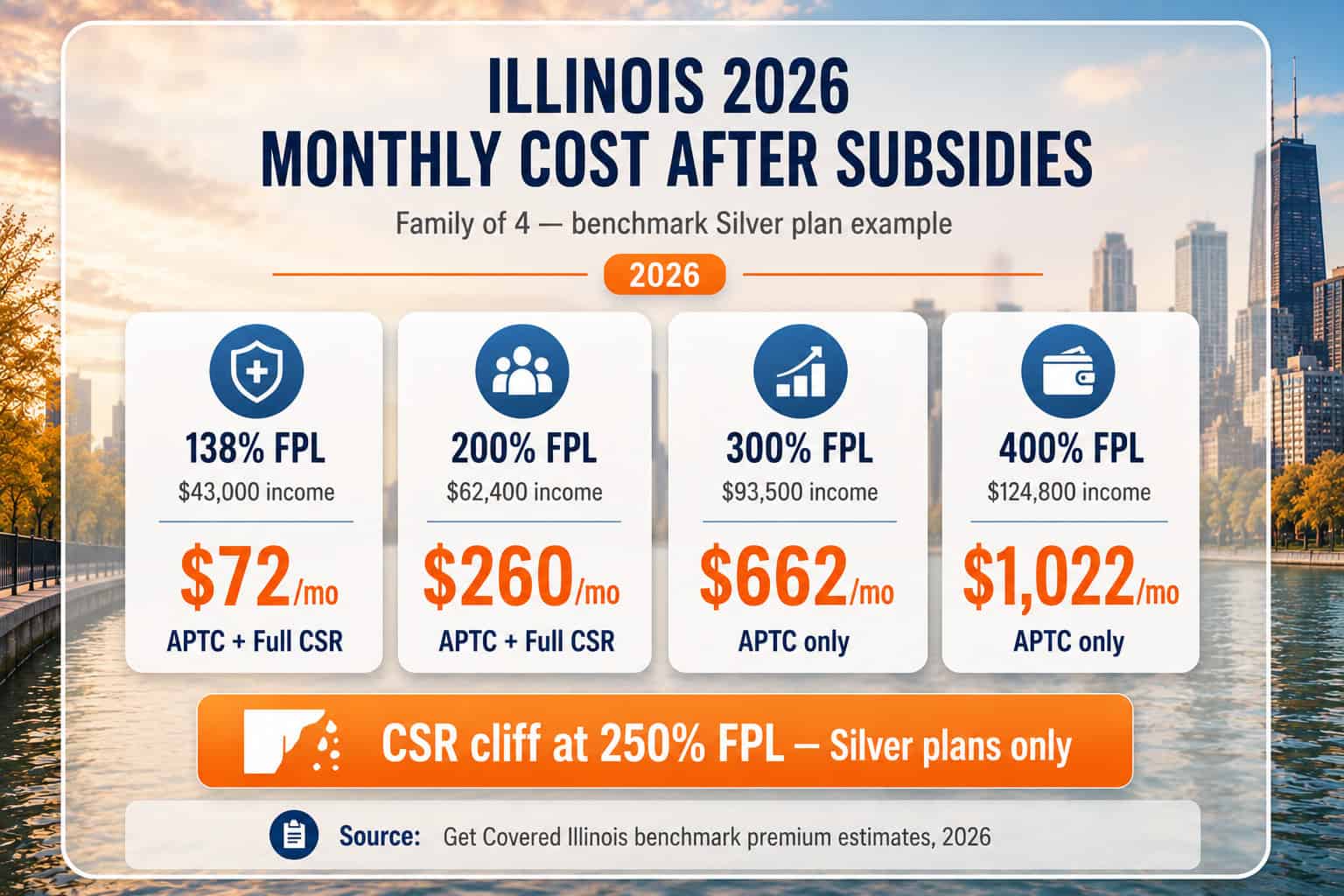

Premium tax credits remain the single biggest lever for affordable health insurance Illinois marketplace shoppers can use in 2026. The credit caps household contributions to the benchmark Silver plan at a percentage of income that scales with the federal poverty level — from roughly 2 percent at the bottom of the eligibility range up to 9.83 percent at 400 percent FPL. Above 400 percent FPL, a narrower 8.5 percent cap applies if the benchmark Silver would otherwise exceed it.

| Household Income (Family of 4) | % FPL | Premium Contribution Cap |

|---|---|---|

| $43,000–$56,000 | 138%–180% | ~2.0%–4.0% of income |

| $56,000–$78,000 | 180%–250% | ~4.0%–6.5% of income |

| $78,000–$93,500 | 250%–300% | ~6.5%–8.5% of income |

| $93,500–$124,800 | 300%–400% | ~8.5%–9.83% of income |

| Over $124,800 | Over 400% | 8.5% cap if benchmark Silver exceeds it |

The 2026 application of premium tax credits runs through Get Covered Illinois, the state-based marketplace that replaced HealthCare.gov on January 1, 2026. The eligibility checker estimates the credit amount before any plan is selected; the actual credit reconciles against final annual income at tax filing the following year. Households whose income changes substantially during the year should update Get Covered Illinois mid-year to avoid owing money back at tax time.

One change worth flagging for 2026: no on-exchange carrier filed Platinum-tier plans for the Illinois marketplace, per the Illinois Department of Insurance. Gold became the richest available tier through Get Covered Illinois. Households who want Platinum-level coverage must shop off-exchange, which forfeits premium tax credit eligibility entirely.

Cost-Sharing Reductions: Silver’s Hidden Discount

Cost-sharing reductions are the second affordability lever, and they go untapped by Illinois shoppers who default to Bronze for the cheapest premium. CSRs lower deductibles, copays, and out-of-pocket maximums on Silver-tier plans for households between 100 and 250 percent of the federal poverty level. The reduction is automatic once eligibility is confirmed — the Silver plan effectively becomes a richer Gold or Platinum equivalent at the original Silver premium.

| % FPL Band | CSR Variant | Effective Actuarial Value |

|---|---|---|

| 100%–150% | CSR 94 (full) | ~94% of expected costs covered |

| 150%–200% | CSR 87 (strong) | ~87% of expected costs covered |

| 200%–250% | CSR 73 (limited) | ~73% of expected costs covered |

| Over 250% | No CSR | Standard Silver 70% coverage |

The numbers matter. A standard Silver plan in Illinois for 2026 typically carries a deductible between $4,500 and $5,500 per individual. The same plan with CSR 94 carries an effective deductible under $500. A family of four at 140 percent of FPL — approximately $43,500 annual income — pays the same monthly premium as any other Silver shopper but faces dramatically lower out-of-pocket costs every time they use care. Bronze plans cannot receive CSRs; the discount only exists at Silver.

This is why Bronze is often the wrong choice for affordable health insurance Illinois shoppers in the 100–250 percent FPL range. A $90 Bronze plan with a $9,000 deductible costs more annually than a $50 Silver plan with full CSR if even modest medical use occurs. The right comparison is total annual cost: premium times twelve plus realistic out-of-pocket spending based on the household’s medical history.

See Your Illinois Subsidy Estimate

Premium tax credits and Silver cost-sharing reductions can drop a $1,650 monthly Illinois benchmark Silver to under $100 for qualifying households. A licensed Illinois broker can run the subsidy math, verify CSR eligibility, and compare all seven carriers at no cost.

Lowest-Premium Carriers in Illinois

Carrier choice matters less for households eligible for substantial subsidies — APTC caps the household contribution to the benchmark Silver, so the after-subsidy difference between the cheapest and second-cheapest plans often comes down to $10 or $20 per month. For households above the subsidy threshold, carrier choice drives the monthly bill directly. Three carriers consistently file the lowest premiums on Get Covered Illinois for 2026.

Molina Healthcare

Lowest PremiumFrequently the cheapest monthly premium on Get Covered Illinois, particularly in Cook County and surrounding suburbs. HMO-only with a narrower network and stricter referral requirements. Best for households who prioritize keeping monthly costs lowest and are comfortable with a smaller in-network provider list.

Ambetter from Celtic

Silver SpecialistMarketed under the Ambetter brand by Celtic Insurance. Strong Silver and Gold pricing across most Illinois counties. Bronze plans are no longer offered in Illinois for 2026, narrowing the budget options from this carrier. Best for households at 138 to 250 percent of FPL who qualify for Silver cost-sharing reductions.

Oscar Health Plan

Digital-FirstTech-focused HMO with competitive pricing in the Chicago metro and select downstate counties. Strong telehealth platform reduces the cost of routine care. Often a competitive choice for residents under 40 who prefer app-based plan management and are comfortable with a narrower in-network specialist list.

BCBSIL HMO

Network TradeoffBlue Cross Blue Shield of Illinois HMO plans typically file higher monthly premiums than Molina or Ambetter — but cover all 102 Illinois counties and include most major hospital systems. The premium difference is the price of network breadth. Best when preferred providers participate only in BCBSIL.

HMO network type drives much of the premium savings. HMOs require in-network care and primary care referrals for specialists, which insurers offset with lower monthly premiums — typically $80 to $200 below PPO equivalents for similar metal tiers. For households who already have a primary care preference and rarely travel out of state, HMO is the standard affordable choice.

Medicaid and All Kids: Free or Near-Free Coverage

For households below 138 percent of FPL, Medicaid is the most affordable health insurance Illinois option — coverage is typically free with no monthly premium and minimal out-of-pocket cost. Illinois fully expanded Medicaid under the Affordable Care Act in 2014, so the eligibility floor sits at 138 percent of FPL for adults regardless of family composition or disability status. Get Covered Illinois routes Medicaid-eligible applicants automatically to the Illinois Department of Healthcare and Family Services within the application flow.

| Program | Eligibility Threshold | Coverage |

|---|---|---|

| Medicaid (adults) | Up to 138% FPL | Free comprehensive coverage |

| All Kids (children) | Up to 318% FPL | Free or low monthly fee, all immigration statuses |

| Family Care | Up to 138% FPL | Free comprehensive coverage (parents and caretakers) |

| FamilyCare Premium | 138%–318% FPL (parents of All Kids) | Small monthly premium based on income |

All Kids is the Illinois CHIP program and is more generous than most state CHIP programs. The 318 percent FPL ceiling means a family of four with income up to roughly $99,000 still qualifies for All Kids coverage of their children, even while the parents shop the marketplace for adult coverage. All Kids covers children regardless of immigration status, which is unusual nationally and reflects Illinois state-only funding above the federal CHIP minimums. Children with All Kids and parents with marketplace coverage are a common Illinois household configuration that maximizes total affordability.

Tax Time Easy Enrollment for Uninsured Filers

Illinois added a state-only special enrollment pathway in 2026 called the Tax Time Easy Enrollment Program. Residents who indicate on their state income tax return that the household lacked health insurance can request enrollment help directly through the tax filing — Get Covered Illinois follows up with personalized outreach and grants a special enrollment opportunity without requiring a traditional qualifying life event. This pathway was not available under HealthCare.gov and became possible only with Illinois’ transition to a state-based marketplace.

How Tax Time Easy Enrollment works

File the standard Illinois income tax return and check the box indicating the household had no health insurance for some or all of the prior year. Get Covered Illinois receives the data automatically through state tax processing, contacts the household with subsidy-aware plan recommendations, and opens a special enrollment window. The household chooses a plan and enrolls — no separate marketplace application is required upfront.

The program is particularly valuable for households who missed the November 1 to January 31 open enrollment window because they did not realize they needed coverage, did not know the marketplace had moved to a state platform, or could not navigate the enrollment process during open enrollment. Tax filing happens annually whether or not the household has coverage, so it functions as a backup enrollment trigger that catches gaps the formal SEP categories miss.

Affordable Plan Strategies for Illinois Households

Beyond subsidies and program eligibility, four practical strategies consistently produce affordable Illinois coverage for households who do not qualify for Medicaid and want to minimize total annual cost rather than just monthly premium. Each strategy fits a specific household profile — the right one depends on income, expected medical use, and how much network flexibility matters.

Strategy 1: Silver with CSR if you qualify. Households at 100–250 percent of FPL almost always come out ahead with Silver because of cost-sharing reductions. The lower deductible and out-of-pocket maximum compensate for the higher Silver premium relative to Bronze. This is the single most underused strategy on Get Covered Illinois.

Strategy 2: HSA-eligible HDHP for healthy higher earners. Households above 250 percent FPL with minimal expected medical use can pair a Bronze HSA-eligible high-deductible health plan with maximum HSA contributions. The HSA reduces taxable income, builds long-term medical savings, and pairs naturally with a high-deductible plan when out-of-pocket spending is expected to stay low.

Strategy 3: HMO over PPO when network fits. HMO premiums run $80–200 lower than PPO equivalents for similar metal tiers. Households who already have a primary care preference and rarely travel out of state usually do not need PPO flexibility. The premium savings compound over twelve months.

Strategy 4: All Kids for children, marketplace for parents. Families between 138 and 318 percent of FPL should check All Kids eligibility before pricing family-coverage marketplace plans. Splitting children to All Kids and parents to marketplace coverage typically produces lower total monthly cost than family coverage on a single marketplace plan.

Common Cost Mistakes on the Illinois Marketplace

Four mistakes consistently push Illinois households into more expensive coverage than they needed to buy. Each one reflects a reasonable instinct — minimize the monthly bill — applied without modeling the total annual cost or checking eligibility for additional savings layers.

Defaulting to Bronze without checking Silver CSR

Bronze has the lowest premium but Silver with full CSR usually wins on total annual cost for households at 100–250 percent FPL. Run both numbers before choosing — the deductible difference often outweighs the monthly premium savings.

Ignoring All Kids for the children

Children up to 318 percent FPL qualify for All Kids regardless of immigration status. Many Illinois families buy family marketplace coverage when splitting the kids to All Kids would lower total monthly cost by $200–340 per month.

Underestimating annual income to maximize the subsidy

Premium tax credits reconcile against actual annual income at tax filing. Households that received APTC based on a lower estimate owe the difference back to the IRS — sometimes thousands of dollars. Over-estimating income is the safer error.

Auto-renewing without rerunning the subsidy estimate

Income and household composition change. The benchmark Silver premium changes every plan year. Households who auto-renew at the same APTC without re-verification often miss substantial additional savings or end up over-credited.

Frequently Asked Questions About Affordable Illinois Health Insurance

The most common questions Illinois residents ask about subsidies, Silver CSR, Medicaid eligibility, the 2026 premium increase, and whether Bronze or Silver is cheaper in the long run.

What is the cheapest health insurance plan in Illinois for 2026?

Molina Healthcare typically files the lowest monthly premium on Get Covered Illinois in Cook County and surrounding suburbs. Statewide, Ambetter from Celtic and Molina trade off as the lowest-premium options on Silver and Gold tiers — though Ambetter no longer offers Bronze in Illinois for 2026. The cheapest plan after subsidies depends on household income; many households at 138 to 250 percent of FPL pay under $50 per month for a Silver plan after premium tax credits and cost-sharing reductions.

How much can I save with a premium tax credit in Illinois?

Premium tax credits cap the household’s contribution to the benchmark Silver plan at a percentage of income that scales with FPL band — from roughly 2 percent for households near 138 percent FPL up to 9.83 percent for households at 400 percent FPL in 2026. Above 400 percent FPL there is no cap unless the benchmark Silver plan would exceed 8.5 percent of income, which preserves the previous enhanced-subsidy cliff fix on a narrower basis.

What is the Silver cost-sharing reduction in Illinois?

Cost-sharing reductions are an additional discount layered on top of premium tax credits for households between 100 and 250 percent of the federal poverty level who choose a Silver-tier marketplace plan. CSRs lower deductibles, copays, and out-of-pocket maximums substantially — a Silver plan with full CSR can have an effective deductible under $500 instead of the standard $5,000-plus. CSRs do not transfer to Bronze, Gold, or Catastrophic plans.

Do I qualify for Medicaid in Illinois?

Illinois Medicaid covers adults with household income up to 138 percent of the federal poverty level — approximately $20,800 for a single adult or $43,000 for a family of four in 2026. Eligibility runs through the Illinois Department of Healthcare and Family Services, and applicants are routed automatically within the Get Covered Illinois application flow. Children up to 318 percent of FPL qualify for All Kids regardless of immigration status, often before the adults in the household qualify for marketplace subsidies.

Why did my Illinois health insurance get more expensive in 2026?

The enhanced premium tax credits added by federal law in 2021 expired at the end of 2025. These had increased the subsidy amount across income bands and removed the 400 percent FPL cliff entirely. Without the enhancements, Illinois families pay roughly $130 per month more on average than they did in 2025 — a year-over-year increase near 50 percent. Carrier rate filings also rose modestly, but the subsidy expiration is the dominant driver.

Should I pick the cheapest Bronze plan to save money?

Not automatically. Bronze plans have the lowest monthly premium but deductibles of $7,000 to $9,200 per individual in 2026 — meaning the household pays for almost all care until the deductible is met. For households eligible for Silver cost-sharing reductions (income between 100 and 250 percent of FPL), Silver almost always beats Bronze on total annual cost. Bronze makes sense only for healthy adults well above subsidy thresholds who want catastrophic-only protection.

Illinois Health Insurance Resources

Statewide overview of carriers, costs, and coverage paths for 2026

Illinois Marketplace GuideGet Covered Illinois enrollment steps, deadlines, and the new state-based platform

Best Illinois Health InsuranceTop-ranked carriers and plan options for Illinois residents in 2026

Illinois PPO PlansBCBSIL PPO options and other flexible network choices statewide

Family Health InsuranceAll Kids, marketplace splits, and mixed-status coverage for Illinois households

Private Medical InsuranceOff-exchange and private health coverage for unsubsidized Illinois buyers

Small Business CoverageGroup health insurance options for Illinois employers under 50 employees

Short-Term CoverageGap coverage rules and marketplace alternatives for Illinois residents

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required

Find Your Most Affordable Illinois Plan

Subsidies, Silver CSR, Medicaid, and All Kids each lower the cost of Illinois coverage in different ways. A licensed Illinois broker maps the household to the right combination, verifies eligibility across all seven carriers, and completes enrollment at no cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Illinois residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.