Alaska Health Insurance: Your Guide to 2026 Coverage

Alaska has some of the highest health insurance premiums in the country — but most residents pay far less than the sticker price. Subsidies, a rare carrier rate decrease for 2026, and a marketplace with two competing plans mean there are real options for most budgets. Whether this is a first enrollment, a carrier switch, or just a check to see if a better deal exists, this guide covers what plans are available, what they actually cost after financial help, and how to get enrolled.

What brings you here today?

How to Get Alaska Health Insurance

Health coverage in Alaska is purchased through HealthCare.gov, the federal marketplace. Residents can enroll during Open Enrollment (November 1 through January 15) or within 60 days of a qualifying life event like job loss, marriage, or having a baby. Free enrollment assistance is available, and premiums are identical whether enrolling directly or with professional help.

HealthCare.gov Marketplace

Subsidies ApplyBest for: Anyone earning $19,550–$78,200 single who qualifies for subsidies. Two carriers compete: Premera (statewide) and Moda Health (metro areas). The only enrollment path where premium tax credits reduce the monthly bill.

Medicaid / Denali KidCare

Free or Low-CostBest for: Individuals earning below $19,550 per year and families with children. Alaska expanded Medicaid under the ACA. Denali KidCare covers uninsured children and pregnant women. Enrollment is open year-round with no deadline.

Direct From Carrier

No SubsidiesBest for: People above the subsidy threshold ($78,200+ single) who want a specific carrier. Same plans and premiums as the marketplace, but no subsidy option. Premera sells directly at premera.com.

Free Enrollment Assistance

No Added CostBest for: Anyone who wants help comparing options across both carriers. Free enrollment assistance is available through the marketplace and independent professionals. Premiums are the same price as enrolling directly.

Premera Blue Cross Blue Shield offers coverage statewide with the largest provider network in Alaska. Moda Health covers the most populated areas: Municipality of Anchorage, Matanuska-Susitna Borough, Kenai Peninsula Borough, Fairbanks North Star Borough, and Southeast Alaska. In rural areas outside Moda’s footprint, Premera is the only option.

Compare Plans From Both Alaska Carriers

Enter your info once to see real prices with subsidies applied for Premera and Moda plans.

What Alaska Health Insurance Costs

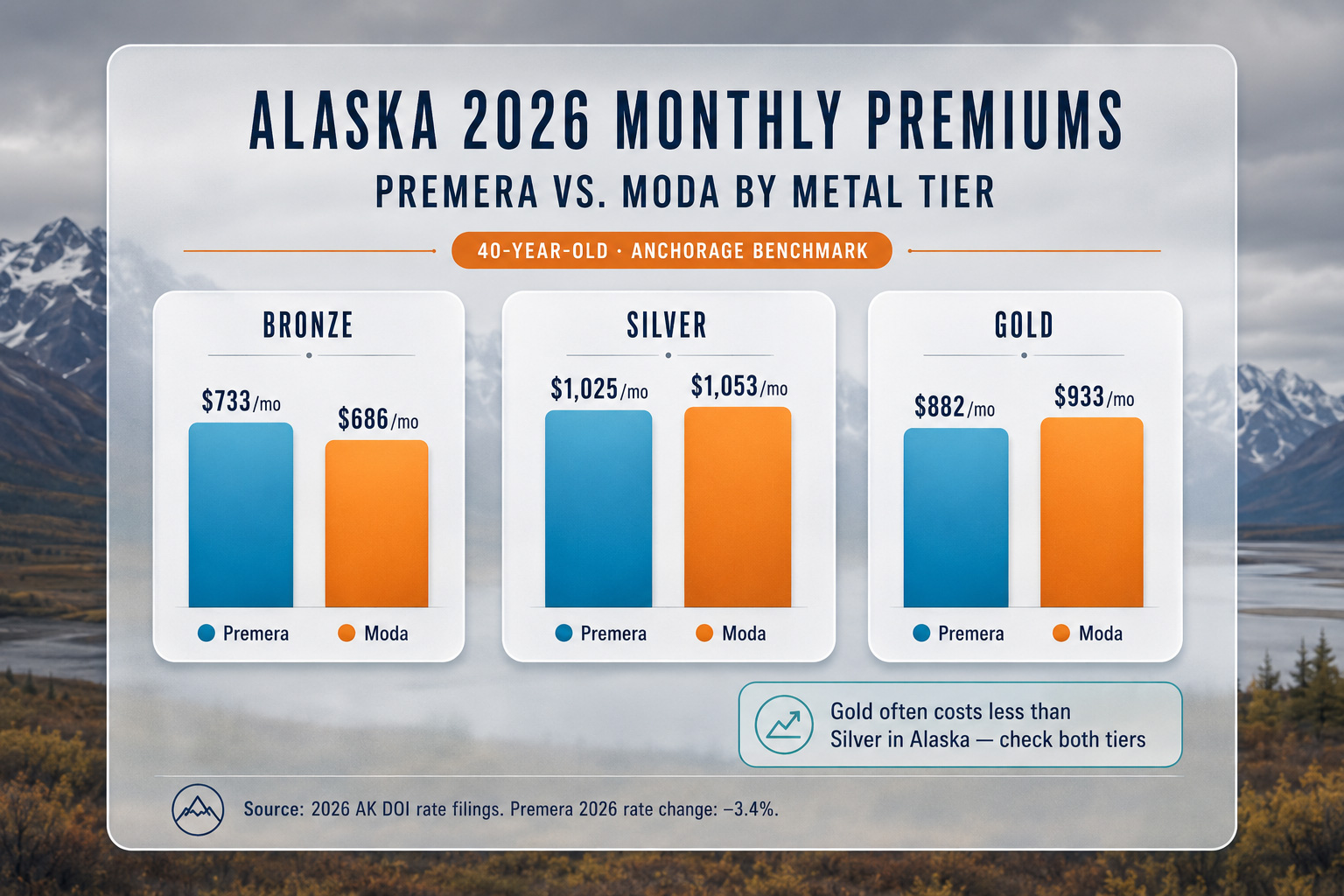

Premiums in Alaska are among the highest in the nation due to the state’s small population, remote geography, and high healthcare delivery costs. For 2026, Premera filed a 3.4% rate decrease while Moda’s rates vary by region. A 40-year-old pays $1,025 to $1,053 per month for a Silver plan before subsidies, depending on the carrier. After subsidies, most Alaskans pay significantly less.

Source: 2026 Alaska ACA rate filings via HealthCare.gov and state DOI-approved rates. Premera rate decrease per Premera Blue Cross Blue Shield of Alaska producer bulletin, Sept. 2025. Premiums are pre-subsidy for a 40-year-old, non-tobacco user.

Alaska’s Unusual Pricing: Gold Costs Less Than Silver

In most states, Gold plans cost more than Silver. In Alaska, the opposite is often true. Premera’s cheapest Gold plan costs $882/month compared to $1,025 for Silver. Gold plans also have lower deductibles ($1,111 vs. $2,525). For Alaskans with moderate to high healthcare needs, Gold often delivers better value than Silver even before considering subsidies.

These are pre-subsidy prices. According to CMS enrollment data, the majority of marketplace enrollees in Alaska received subsidies that covered a significant portion of their premiums. Subsidies are available for individuals earning between 100% and 400% of the Federal Poverty Level ($19,550 to $78,200 for a single person in 2026). For strategies to lower costs further, see cheap health insurance in Alaska and affordable coverage strategies.

Who Qualifies for Marketplace Subsidies in Alaska

Premium tax credits are available to Alaska residents earning between 100% and 400% of the Federal Poverty Level — $19,550 to $78,200 for a single person in 2026. Enhanced subsidies from the Inflation Reduction Act expired at the end of 2025 after Congress did not extend them, meaning the “subsidy cliff” returns: earn over 400% FPL and no credits apply.

Source: 2025 HHS Federal Poverty Guidelines for Alaska (ASPE.hhs.gov). Alaska has higher FPL thresholds than the 48 contiguous states. 2025 guidelines are used to determine 2026 marketplace subsidy eligibility.

Marcus runs a seasonal fishing charter business and needs year-round coverage. His income puts him at approximately 246% FPL under Alaska’s higher poverty guidelines, qualifying him for subsidies. A Premera Silver plan costs $1,025/month before credits, but after his estimated monthly subsidy, he pays significantly less. He chose a Gold plan instead at $882/month pre-subsidy, which after his credit costs well under $200/month — better coverage than Silver at a fraction of the price.

The subsidy cliff makes Alaska health insurance particularly challenging for those just above the income threshold. A single person earning $78,201 (just $1 over 400% FPL) could face over $12,000 per year in premiums with no financial help. Income planning strategies can help avoid this cliff. See affordable coverage strategies for details.

Alaska Health Insurance Carriers for 2026

Two carriers sell marketplace plans in Alaska for 2026: Premera Blue Cross Blue Shield of Alaska (available statewide) and Moda Health (available in Anchorage, Mat-Su, Kenai Peninsula, Fairbanks North Star, and Southeast Alaska). Premera offers the largest provider network statewide, while Moda provides competitive pricing in its service areas.

Premera Blue Cross Blue Shield of Alaska

StatewidePremera Blue Cross • Blue Cross Blue Shield of Alaska

- Coverage: All Alaska zip codes

- Network: Legacy network — largest in Alaska

- 2026 Rate Change: −3.4% (rate decrease)

- Plans: Bronze, Silver, Gold (no Platinum)

- Key Change: Adult dental benefits removed for 2026 to keep rates affordable

Best for rural Alaskans (only option in many areas) and anyone prioritizing network size and provider access.

Moda Health

Metro AreasModa Health • ODS Health

- Coverage: Anchorage, Mat-Su, Kenai Peninsula, Fairbanks, Southeast AK

- Network: Moda Select (renamed from Pioneer in 2026)

- 2026 Expansion: Aetna PPO network for out-of-area care

- Plans: Bronze, Silver, Gold

- Key Feature: Access to Aetna national PPO for services outside Alaska

Best for metro residents who want a second carrier option or need out-of-state network access.

Comparing networks is essential in areas where both carriers operate. Check whether doctors, specialists, and preferred hospitals participate in each carrier’s network before enrolling. For detailed carrier comparisons, see best health insurance in Alaska.

Types of Health Plans Available in Alaska

Marketplace plans in Alaska come in four metal tiers: Bronze (lowest premiums, highest out-of-pocket costs), Silver (moderate costs, eligible for cost-sharing reductions), Gold (higher premiums, lower deductibles), and Catastrophic (available to those under 30 or with hardship exemptions). Alaska does not offer Platinum plans. Most plans are PPO-style, offering flexibility to see specialists without referrals.

Source: 2026 Alaska marketplace plan data via HealthCare.gov, CMS Plan Finder. Premium ranges reflect lowest/highest available plan by tier for a 40-year-old. Deductible and OOP max ranges from Premera and Moda 2026 plan filings.

Alaska health insurance has a unique pricing dynamic where Gold plans often cost less than Silver. This makes Gold an attractive option for anyone with moderate to high healthcare needs. Silver plans remain valuable for those earning below 250% FPL ($37,650 single) who qualify for cost-sharing reductions (CSR) that lower deductibles and copays.

Enrollment Periods and Deadlines

Open Enrollment for 2026 coverage in Alaska runs November 1, 2025 through January 15, 2026. Enroll by December 15 for coverage starting January 1; enroll by January 15 for coverage starting February 1. Outside this window, enrollment is available within 60 days of a qualifying life event. Alaska Natives and American Indians can enroll year-round without a qualifying event.

Loss of Coverage

60 DaysLosing job-based insurance, aging off a parent’s plan at 26, COBRA expiring, or losing Medicaid eligibility. The 60-day window begins on the date coverage is lost.

Life Changes

60 DaysGetting married, having a baby, adopting a child, or getting divorced. These events trigger a 60-day special enrollment period to add or change coverage for affected household members.

Moving to Alaska

60 DaysRelocating to Alaska from another state opens a 60-day enrollment window. The move must be to a new coverage area. Moving within the same coverage area does not qualify.

Income Changes

SEPGaining or losing subsidy eligibility due to income changes, or losing Medicaid or CHIP coverage, triggers a special enrollment period. Report changes promptly at HealthCare.gov.

Important for 2027

Starting with 2027 Alaska health insurance plans, Open Enrollment will end December 15 instead of January 15 — a shorter window going forward. Plan ahead and avoid waiting until the last minute to compare or switch plans.

Frequently Asked Questions About Alaska Health Insurance

The most common questions about Alaska health insurance cover enrollment timing, subsidy eligibility, carrier options, and why premiums are so high. Below are answers specific to the 2026 plan year, including the current carrier lineup, income thresholds for subsidies, and open enrollment deadlines.

How do I get health insurance in Alaska?

Enroll through HealthCare.gov during Open Enrollment (November 1 through January 15) or within 60 days of a qualifying life event. Two carriers offer plans: Premera Blue Cross and Moda Health. Free enrollment assistance is available, and premiums are the same whether enrolling directly or with professional help.

How much does health insurance cost in Alaska?

Before subsidies, a Silver plan costs $1,025 to $1,053 per month for a 40-year-old depending on the carrier. Those are among the highest rates in the nation. After subsidies, most Alaskans pay significantly less. Gold plans often cost less than Silver in Alaska, making them a better value for many residents.

Who qualifies for subsidies in Alaska?

Households earning between 100% and 400% of the Federal Poverty Level qualify: $19,550 to $78,200 for a single person in 2026. Subsidies reduce monthly premiums based on income, with lower earners receiving larger credits. The enhanced subsidies from 2021–2025 expired at the end of 2025. The House passed an extension in January 2026, but Senate action is still pending.

What carriers sell health insurance in Alaska for 2026?

Two carriers participate in the marketplace: Premera Blue Cross Blue Shield of Alaska (available statewide with the largest network) and Moda Health (available in Anchorage, Mat-Su, Kenai Peninsula, Fairbanks North Star, and Southeast Alaska). In rural areas, Premera is typically the only option.

When can I enroll in coverage?

Open Enrollment runs November 1 through January 15 for coverage starting January 1 or February 1. Outside this window, enrollment is available within 60 days of a qualifying life event like job loss, marriage, or having a baby. Alaska Natives and American Indians can enroll year-round without a qualifying event.

Why is health coverage so expensive in Alaska?

Alaska’s small population (733,000), high healthcare delivery costs, remote geography requiring air transport for many services, and limited carrier competition drive premiums. Subsidies offset these costs for most enrollees. For 2026, Premera filed a 3.4% rate decrease, a rare improvement in a challenging market.

Alaska Health Insurance Resources

Premera Bronze, Silver, and Gold plan comparison with premium benchmarks by Alaska borough

Alaska Marketplace EnrollmentHealthCare.gov enrollment steps, Premera plan tiers, and 2026 open enrollment dates for Alaska

Affordable Coverage in AlaskaAlaska subsidy guide — 85% of enrollees receive an average $758/month in federal financial help

Cheap Health Insurance in AlaskaLowest-cost 2026 Alaska plans — Bronze premiums, catastrophic options, and ways to cut monthly costs

Find Your Alaska Health Plan

Most marketplace enrollees in Alaska receive subsidies that significantly reduce premiums. See what coverage would actually cost based on zip code, income, and household size.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Alaska residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.