Illinois Health Insurance 2026: Plans, Costs & Get Covered Illinois

Illinois health insurance changed substantially for 2026. The state launched its own marketplace, Get Covered Illinois, replacing HealthCare.gov on January 1, 2026. Four carriers exited the on-exchange market, leaving seven companies competing for Illinois enrollees. Average premiums climbed roughly 50 percent year over year as enhanced federal subsidies expired. This guide breaks down what residents need to know about coverage options, costs, carrier choices, enrollment through the new state platform, and the financial assistance available to households across the state in 2026.

What brings you here today?

Illinois Health Insurance in 2026: What’s Changed

Illinois marketplace enrollment moved to a state-run platform in 2026, with fewer carriers and higher premiums than the prior year. The Centers for Medicare and Medicaid Services approved Illinois’ transition to a state-based marketplace in 2025, and Get Covered Illinois began operating on January 1, 2026. Residents who previously enrolled through HealthCare.gov now use the new state platform for shopping, applying for subsidies, and managing coverage.

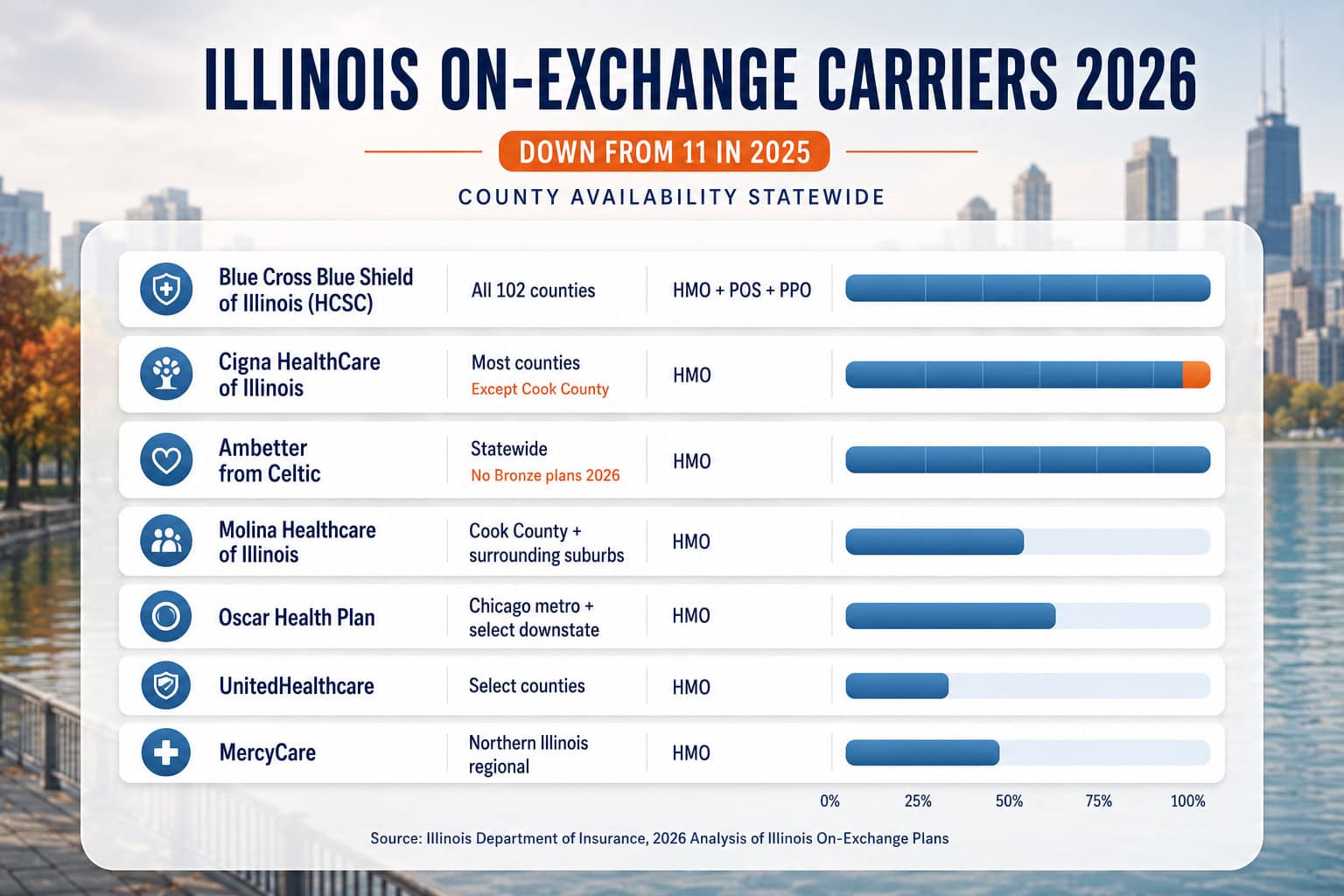

The carrier landscape contracted sharply. Eleven companies offered on-exchange plans in Illinois in 2025; only seven remain for 2026 after Aetna CVS, Aetna Life, Health Alliance, and Quartz exited the state. Anyone enrolled with one of those four carriers needed to actively select a new plan during open enrollment, and the Illinois Department of Insurance confirmed that 285 unique plan options remained available across the surviving carriers for plan year 2026.

⚠️ 2026 Subsidy Update

Enhanced federal premium tax credits that lowered marketplace costs since 2021 expired at the end of 2025. Get Covered Illinois reported that without the enhancements, Illinois families pay roughly $130 per month more on average than they did in 2025 — a year-over-year increase near 50 percent. Premium tax credits still exist at the original ACA levels; only the temporary boost was lost.

Get Covered Illinois used its new state authority to extend open enrollment by sixteen days, running through January 31, 2026 instead of the federal January 15 deadline. That kind of state-specific flexibility was not available to Illinois residents under HealthCare.gov. The platform also introduced a tax-time enrollment opportunity, allowing residents who confirm they are uninsured on their Illinois tax filing to trigger a special enrollment period without needing a qualifying life event.

Health Insurance Carriers Available in Illinois for 2026

Seven carriers offer on-exchange plans through Get Covered Illinois for 2026, with service areas varying significantly by county. Health Care Service Corporation, which operates as Blue Cross Blue Shield of Illinois, dominates the state market and is the only carrier offering HMO, POS, and PPO plans on the exchange — its network reaches all 102 Illinois counties. Cigna pulled out of Cook County for 2026, leaving Chicago-area residents who had Cigna coverage in 2025 to switch carriers.

Blue Cross Blue Shield of Illinois

StatewideOperated by Health Care Service Corporation. The dominant Illinois carrier — only on-exchange option offering HMO, POS, and PPO plans for 2026. Broadest network covering all 102 counties and most major hospital systems including Northwestern Medicine, Rush, and OSF HealthCare.

Cigna HealthCare of Illinois

No Cook CountyOffers plans in most Illinois counties for 2026 but exited Cook County effective January 1, 2026. Chicago residents who previously held Cigna coverage needed to select a new carrier. Emphasizes preventive care, telehealth integration, and prescription drug coverage in suburban and downstate markets.

Ambetter from Celtic

Cost-FocusedMarketed under the Ambetter brand by parent company Celtic Insurance. Popular cost-conscious choice for Illinois families seeking lower premiums on Silver and Gold metal tiers. Bronze plans are no longer offered in Illinois for 2026, narrowing the budget options from this carrier.

Molina Healthcare of Illinois

Budget TierFrequently the lowest-premium choice on Get Covered Illinois, particularly in Cook County and surrounding suburbs. Strong for households who prioritize keeping monthly costs low and are comfortable with a narrower HMO network and stricter referral requirements.

Oscar Health

Digital-FirstTech-focused carrier with a strong telehealth platform and concierge support model. Operates primarily in the Chicago metro and select downstate counties. Often a competitive choice for residents under 40 who prefer app-based plan management and virtual primary care.

UnitedHealthcare

Broad NetworkOne of the larger national carriers operating in Illinois. Offers ACA plans in select counties for 2026 and has the broadest reach among national for-profit insurers in Illinois Medicare Advantage. Strong digital tools and out-of-network coverage on certain plan tiers.

MercyCare rounds out the seven on-exchange carriers, operating regionally in northern Illinois with a faith-based provider network anchored to Mercyhealth System hospitals. Off-exchange, Aetna and Humana remain active in Illinois employer-sponsored and Medicare markets but no longer participate in the individual marketplace. Choosing a carrier should start with verifying that preferred doctors and hospitals participate in the plan’s network for 2026 — county-level availability shifts each year.

How Much Does Illinois Health Insurance Cost in 2026?

Unsubsidized Illinois marketplace premiums for 2026 typically run $385 to $920 per month for individuals, with family plans ranging from $1,250 to $2,950 monthly depending on age, household size, county, and metal tier. After premium tax credits — which most Illinois marketplace enrollees still qualify for — many households pay between $0 and $200 per month. The 2025-to-2026 jump was driven by expiration of the enhanced subsidies in place since 2021.

| Age | Bronze (unsubsidized) | Silver (unsubsidized) | Gold (unsubsidized) |

|---|---|---|---|

| 27 | $385–$465 | $480–$580 | $565–$680 |

| 40 | $510–$615 | $635–$770 | $745–$905 |

| 50 | $680–$815 | $845–$1,020 | $995–$1,200 |

| 60 | $910–$1,090 | $1,130–$1,365 | $1,330–$1,605 |

Cook County premiums tend to run slightly above the statewide median for Bronze and Silver plans but slightly below for Gold. Downstate rating areas — including Peoria, Springfield, Champaign-Urbana, and Carbondale — generally show lower premiums for the same plan structure because of lower provider costs and less network density. The largest cost differences across the state appear in the Bronze tier, where carrier-by-carrier pricing strategy varies widely; Gold-tier pricing is more standardized statewide.

Subsidy reality check

Even after the enhanced subsidies expired, most Illinois marketplace shoppers still qualify for the original ACA premium tax credits. A family of four in Springfield earning $75,000 typically pays around $290 per month for a benchmark Silver plan in 2026, compared to about $1,800 monthly without any subsidy. Running an eligibility check before shopping is the single biggest cost-saving move.

Out-of-pocket costs vary as much as premiums. Bronze plans have lower monthly costs but the highest deductibles, typically $7,000 to $9,200 per individual in 2026. Silver plans balance premiums and deductibles, and Silver plus cost-sharing reductions can offer the lowest total annual cost for households under 250 percent of the federal poverty level. Gold plans cost more monthly but reduce deductibles to roughly $1,500 to $3,000. Illinois removed Platinum plans from the on-exchange market for 2026, so anyone wanting that level of richness must look at off-exchange or employer-sponsored coverage.

Get Covered Illinois: Enrolling Through the State Marketplace

Get Covered Illinois became the only place Illinois residents can shop marketplace plans and apply for premium tax credits as of January 1, 2026. The state platform handles eligibility determination, plan comparison, and enrollment, and it integrates with the Illinois Department of Healthcare and Family Services to route Medicaid-eligible applicants automatically. Open enrollment for 2026 plans ran November 1, 2025 through January 31, 2026 — a sixteen-day extension past the federal deadline, made possible by Illinois’ new state-marketplace status.

| Step | What Happens | Time Estimate |

|---|---|---|

| 1. Window shopping | Browse 2026 plans by ZIP, see estimated subsidies before applying | 15–20 min |

| 2. Account & application | Create Get Covered Illinois login, complete household and income details | 20–30 min |

| 3. Eligibility determination | System routes to Medicaid, All Kids, or marketplace based on income | Same day |

| 4. Plan selection | Compare carriers, networks, and total annual cost across metal tiers | 30–60 min |

| 5. Payment & activation | First-month premium payment activates coverage | Immediate |

Illinois invested $6.5 million in a statewide navigator grant program through HFS and the Illinois Department of Insurance, embedding certified navigators in community organizations across the state to provide free enrollment help. Brokers licensed in Illinois — including ForHealthInsurance.com — can also help residents compare plans and complete applications at no cost. The Get Covered Illinois call center handles enrollment by phone at 1-866-311-1119 in English, Spanish, and through interpretation services for up to 200 other languages.

Outside open enrollment, a qualifying life event such as marriage, divorce, birth or adoption, loss of other coverage, or a permanent move into Illinois triggers a 60-day special enrollment period. Illinois added a unique tax-time enrollment opportunity for 2026: residents who indicate on their state tax return that the household is uninsured can trigger a special enrollment period without another life event. This pathway did not exist under the federal exchange and is one of the practical benefits of the SBM transition.

Get Help Enrolling Through Get Covered Illinois

Get Covered Illinois plans, subsidy estimates, and carrier networks change by ZIP code. Speaking with a licensed Illinois broker takes the guesswork out of comparing seven carriers and 285 plan options for 2026.

Plan Types Available in Illinois

Illinois on-exchange plans for 2026 include HMO, POS, and PPO network types, with all 285 on-exchange options sorted into Bronze, Silver, Gold, and Catastrophic metal tiers. Platinum-tier plans were removed from the Illinois on-exchange market for 2026 — the IDOI confirmed no carrier filed a Platinum offering. Blue Cross Blue Shield of Illinois is the only carrier offering all three network types; the other six offer HMOs with limited POS variants.

PPO

Most FlexiblePreferred Provider Organization plans let members see any in-network doctor without a referral, and provide partial coverage for out-of-network care. In Illinois, BCBSIL is the primary on-exchange PPO option for 2026, though off-exchange PPO plans are available from multiple carriers. Best fit for residents who travel frequently or want maximum doctor choice.

HMO

Lower CostHealth Maintenance Organization plans require staying in-network and getting a primary care referral for specialists. Most Illinois on-exchange carriers (Molina, Ambetter, Oscar, MercyCare) offer HMOs exclusively. Premiums run lower than PPO equivalents — often $80 to $200 less per month — making HMOs the most common choice for cost-conscious enrollees.

POS

Middle GroundPoint-of-Service plans blend HMO and PPO features: a primary care doctor coordinates in-network care, but out-of-network specialists are covered at a reduced rate. BCBSIL offers POS variants for 2026. Less common than HMO or PPO but useful for households who want network flexibility without full PPO pricing.

Catastrophic

Under 30 OnlyAvailable to Illinois residents under 30 or those with hardship exemptions. Very low premiums but a deductible equal to the annual out-of-pocket maximum ($9,200 for 2026). Premium tax credits cannot be applied to catastrophic plans. Useful as a worst-case-only safety net for young, healthy residents who do not qualify for cost-sharing reductions.

Among metal tiers, Bronze plans cover roughly 60 percent of total expected costs, Silver covers 70 percent, and Gold covers 80 percent. Without Platinum on the Illinois exchange in 2026, Gold becomes the richest available metal tier through Get Covered Illinois. Off-exchange, BCBSIL and a few other carriers offer Platinum-level products for residents willing to pay full premium without any chance of premium tax credits — that path makes sense mainly for households well above subsidy eligibility who anticipate high medical use.

Subsidies and Financial Assistance for Illinois Residents

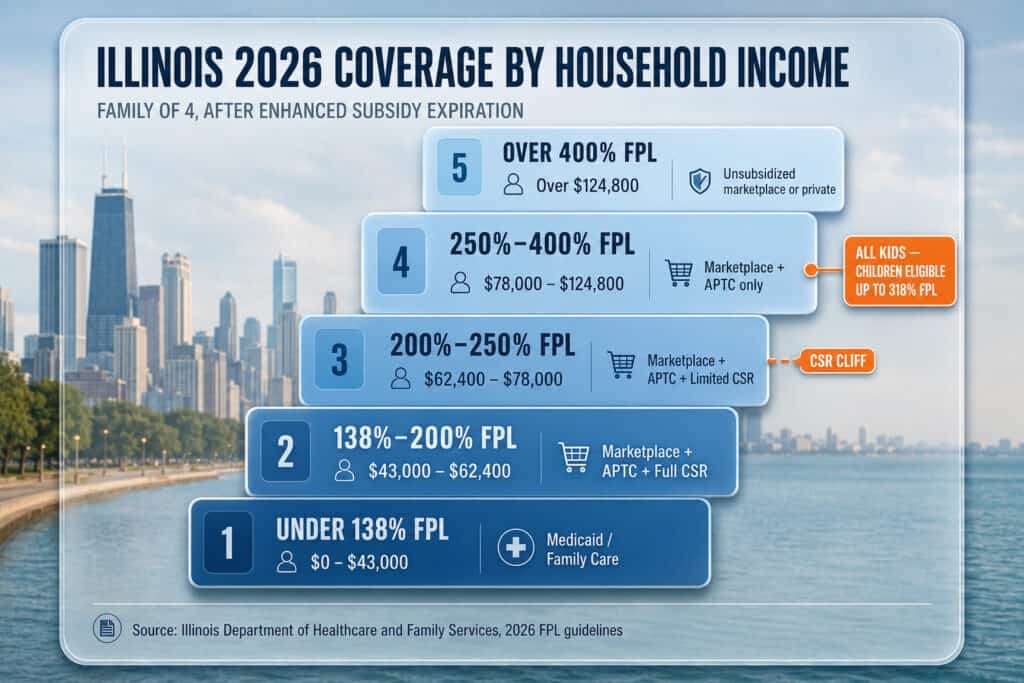

Illinois residents have access to three layers of financial assistance for 2026 health coverage: federal premium tax credits, federal cost-sharing reductions, and state-administered Medicaid and CHIP programs. The expiration of enhanced subsidies at the end of 2025 raised net premiums significantly, but the original ACA tax credits remain in place and still bring monthly costs into reach for most marketplace shoppers below 400 percent of the federal poverty level.

The Illinois Department of Healthcare and Family Services administers Medicaid and All Kids for residents below marketplace thresholds. Adults qualify for Medicaid at incomes up to 138 percent of the federal poverty level — about $20,800 for an individual and $43,000 for a family of four in 2026. Illinois fully expanded Medicaid under the Affordable Care Act in 2014, so there is no coverage gap; residents above Medicaid eligibility roll directly into marketplace tax credit eligibility without a no-coverage zone.

| Household Income | Family of 4 Income Range | Coverage Pathway |

|---|---|---|

| Under 138% FPL | Up to $43,000 | Medicaid / Family Care |

| 138%–200% FPL | $43,000–$62,400 | Marketplace + APTC + CSR |

| 200%–250% FPL | $62,400–$78,000 | Marketplace + APTC + limited CSR |

| 250%–400% FPL | $78,000–$124,800 | Marketplace + APTC only |

| Over 400% FPL | Over $124,800 | Unsubsidized marketplace or private |

All Kids covers children up to 318 percent of the federal poverty level — an income threshold higher than most other state CHIP programs. Illinois is also one of a small number of states that covers children under All Kids regardless of immigration status, expanding access for mixed-status families. Family Care, the state’s Medicaid program for parents of minor children, applies separate income rules and may be accessible to families whose income disqualifies them from adult expansion Medicaid.

Cost-sharing reductions (CSR) lower deductibles, copays, and out-of-pocket maximums for households between 100 and 250 percent of FPL who select a Silver-tier plan. The savings are substantial — a Silver plan with full CSR for a family of four near 150 percent of poverty can have an effective deductible under $500 rather than the standard $5,000-plus. Anyone qualifying for CSR should choose Silver to capture the benefit; it is not transferable to Bronze, Gold, or Catastrophic tiers.

DALL-E prompt:

Filename: il-pillar-subsidy-eligibility-ladder-statewide.jpg

Tool: ChatGPT / GPT Image

Scene type: Data visual — eligibility chart / cost ladder

State anchor: Illinois — 2026 federal poverty level thresholds, family of four

═══ CONTENT ═══

Title: “Illinois 2026 Coverage by Household Income”

Subtitle: “Family of 4, after enhanced subsidy expiration”

Layout: Stepped vertical ladder, five income bands stacked from lowest (bottom) to highest (top), each band a distinct card

Band 1 (bottom): “Under 138% FPL” | “$0 – $43,000” | “Medicaid / Family Care”

Band 2: “138%–200% FPL” | “$43,000 – $62,400” | “Marketplace + APTC + Full CSR”

Band 3: “200%–250% FPL” | “$62,400 – $78,000” | “Marketplace + APTC + Limited CSR”

Band 4: “250%–400% FPL” | “$78,000 – $124,800” | “Marketplace + APTC only”

Band 5 (top): “Over 400% FPL” | “Over $124,800” | “Unsubsidized marketplace or private”

Side callout marker at 318% FPL line: “All Kids — children eligible up to 318% FPL”

Footer note: “Source: Illinois Department of Healthcare and Family Services, 2026 FPL guidelines”

═══ DESIGN SYSTEM ═══

Premium Infographic System: soft shadows under each band card, subtle bevel/edge lighting, consistent top-left light source, layered surfaces. Strong title hierarchy (bold, spaced, top-aligned), clean numeric emphasis on income ranges and FPL percentages. Primary #407297 with gradient overlays (lightening from bottom band to top band). Accent #f87c25 only on the CSR cliff indicator between bands 3 and 4, and on the All Kids 318% callout. Card-based stepped layout, rounded corners, consistent grid alignment.

═══ HARD RULES ═══

• Exact dimensions: 1200×800px — no deviation

• All text fits inside containers — no overflow or clipping

• All five bands equal width

• Band heights proportional to FPL range width — visually accurate scaling

• No spelling errors — verify “All Kids,” “Family Care,” “APTC,” and “CSR” exact spelling

• No human subjects

• No flat grey tables, harsh outlines, or misaligned spacing

Choosing the Right Plan for Your Illinois Household

The right Illinois health insurance plan depends on three variables in roughly this order: which doctors and hospitals you want access to, your expected medical use for the year, and your income for subsidy eligibility. Starting with provider preferences before comparing premiums tends to produce better long-term satisfaction — switching plans mid-year is rarely possible, but anyone can compare prices among plans that all include their preferred providers.

Scenario 1: Young single adult in Chicago, age 27, $42,000 income. Income is around 280 percent of FPL — qualifies for premium tax credits but not cost-sharing reductions. A Bronze HMO from Molina or Ambetter typically lands at $90 to $140 per month after APTC. A Silver plan would cost $190 to $260 monthly but include more predictable copays. If healthy with no regular prescriptions, Bronze is usually the lowest total annual cost. If managing any chronic condition, Silver beats Bronze in the math.

Scenario 2: Family of four in Naperville, ages 38 and 40 with two children, $95,000 income. Income near 305 percent of FPL — qualifies for APTC, no CSR. A Silver BCBSIL HMO typically nets around $480 to $620 per month after subsidy. A Gold plan would push to $620 to $780 but reduce the deductible significantly. With two school-age children, Gold often makes sense to limit out-of-pocket exposure for sports injuries, illnesses, and routine care.

Scenario 3: Self-employed couple in Peoria, ages 52 and 55, $145,000 combined income. Income exceeds 400 percent of FPL — no premium tax credit. Unsubsidized BCBSIL PPO premiums for a couple this age typically run $2,400 to $2,900 per month for Silver and $2,800 to $3,400 for Gold. Comparing on-exchange to off-exchange PPO and private medical insurance options becomes worthwhile at this income level; for unsubsidized buyers, off-exchange Platinum plans or private coverage may offer better network access at similar cost.

Anyone with a specific Illinois doctor or hospital in mind should verify network participation for 2026 before selecting a plan. Northwestern Medicine, Rush, UChicago Medicine, Advocate, OSF, Memorial Health (Springfield), and Carle Health (Champaign-Urbana) all participate in BCBSIL’s broadest networks but may have narrower participation with other carriers. The Get Covered Illinois plan finder includes provider lookup; verifying directly with the doctor’s office is the most reliable check.

Frequently Asked Questions About Illinois Health Insurance

The most common questions Illinois residents ask about Get Covered Illinois, 2026 costs, carrier availability, Medicaid expansion, and how to verify doctor networks before selecting a plan.

What is Get Covered Illinois and how is it different from HealthCare.gov?

Get Covered Illinois became the state’s official health insurance marketplace on January 1, 2026, replacing HealthCare.gov for Illinois residents. The Centers for Medicare and Medicaid Services approved the transition in 2025. As a state-based marketplace, Get Covered Illinois has authority to extend enrollment periods and create state-specific special enrollment opportunities that the federal exchange could not offer Illinois residents.

How much does health insurance cost in Illinois in 2026?

Unsubsidized Illinois marketplace premiums for 2026 typically range from $385 to $920 per month for individuals depending on age, county, and metal tier, with family plans running $1,250 to $2,950 monthly. After premium tax credits, many Illinois residents pay $0 to $200 per month. Premiums rose roughly 50 percent over 2025 levels because enhanced federal subsidies expired at the end of 2025.

Which carriers offer health insurance in Illinois for 2026?

Seven carriers offer on-exchange plans in Illinois for 2026: Health Care Service Corporation (Blue Cross Blue Shield of Illinois), Cigna HealthCare of Illinois, Molina Healthcare of Illinois, Oscar Health Plan, Celtic Insurance Company (Ambetter), MercyCare, and UnitedHealthcare. This is down from eleven carriers in 2025 after Aetna CVS, Aetna Life, Health Alliance, and Quartz exited the Illinois market at the end of 2025.

When is open enrollment in Illinois for 2026 health insurance?

Open enrollment through Get Covered Illinois ran from November 1, 2025 through January 31, 2026, an extension of sixteen days past the federal January 15 deadline. The extension was possible because Illinois now operates its own state-based marketplace. Outside open enrollment, residents need a qualifying life event such as marriage, job loss, or having a baby to enroll, with one exception — the Tax Time Easy Enrollment Program.

Does Illinois have Medicaid expansion?

Yes. Illinois expanded Medicaid under the Affordable Care Act in 2014, and adults with household income up to 138 percent of the federal poverty level qualify for Medicaid coverage. Illinois operates its Medicaid program through the Department of Healthcare and Family Services. Children in households earning up to 318 percent of the federal poverty level qualify for All Kids, which is the state’s Children’s Health Insurance Program.

Can I see any doctor in Illinois with marketplace coverage?

Doctor access depends on the plan’s network type and the carrier. PPO plans from Blue Cross Blue Shield of Illinois offer the broadest statewide network, including most major hospital systems in Chicago, Springfield, Peoria, and Rockford. HMO plans require staying in-network and getting referrals for specialists. Cigna left Cook County for 2026, so Chicago-area residents who had Cigna in 2025 needed to switch carriers. Always verify a specific doctor’s participation before selecting a plan.

Illinois Health Insurance Resources

Get Covered Illinois enrollment steps, deadlines, and the new state-based platform

Best Illinois Health InsuranceTop-ranked carriers and plan options for Illinois residents in 2026

Illinois PPO PlansBCBSIL PPO options and other flexible network choices statewide

Family Health InsuranceAll Kids, marketplace splits, and mixed-status coverage for Illinois households

Affordable Illinois PlansSubsidy strategies and lowest-cost coverage paths after the 2026 rate jump

Private Medical InsuranceOff-exchange and private health coverage for unsubsidized Illinois buyers

Small Business CoverageGroup health insurance options for Illinois employers under 50 employees

Short-Term CoverageGap coverage rules and marketplace alternatives for Illinois residents

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required

Compare Illinois Health Insurance Plans

Comparing seven carriers and 285 plan options across Get Covered Illinois is faster with a licensed Illinois broker. ForHealthInsurance.com helps Illinois residents and businesses compare quotes, verify networks, and complete enrollment at no extra cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Illinois residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.