Affordable Health Insurance Indiana 2026: Costs, Plans & Savings

Affordable health insurance Indiana options range from no-cost HIP 2.0 Medicaid for lower-income Hoosiers to $700/month-plus Platinum plans for those who want maximum coverage. This guide covers what plans actually cost in Indiana in 2026, how subsidies reduce those costs, and strategies for finding the most affordable health insurance Indiana residents can access.

What brings you here today?

How Much Does Health Insurance Cost in Indiana?

In 2026, Indiana marketplace premiums for a 40-year-old in Indianapolis average ~$340/month for Bronze, ~$490/month for Silver, and ~$580/month for Gold before subsidies. After premium tax credits, available to most Hoosiers earning under $62,600/year single (400% of the 2025 ASPE Federal Poverty Guidelines), the average Indiana enrollee pays under $150/month. Costs vary by county, age, tobacco use, and plan type; rural Indiana counties served by fewer carriers often have higher benchmark premiums.

Bronze

Age 40, Indianapolis. Lowest premium, highest deductible ($6,000–$8,500). Best for healthy individuals who rarely use care.

Silver

Age 40, Indianapolis. Benchmark tier. Qualifies for cost-sharing reductions at 100–250% FPL, which can cut effective deductible to $800.

Gold

Age 40, Indianapolis. Higher premium, deductible as low as $500. Worth it if you use care regularly, and typically saves money vs Bronze for moderate care users.

HIP 2.0 (Medicaid)

For incomes under $22,026/year (single). POWER account contributions of $1–$27/month unlock HIP Plus with dental and vision. No deductible or out-of-pocket maximum.

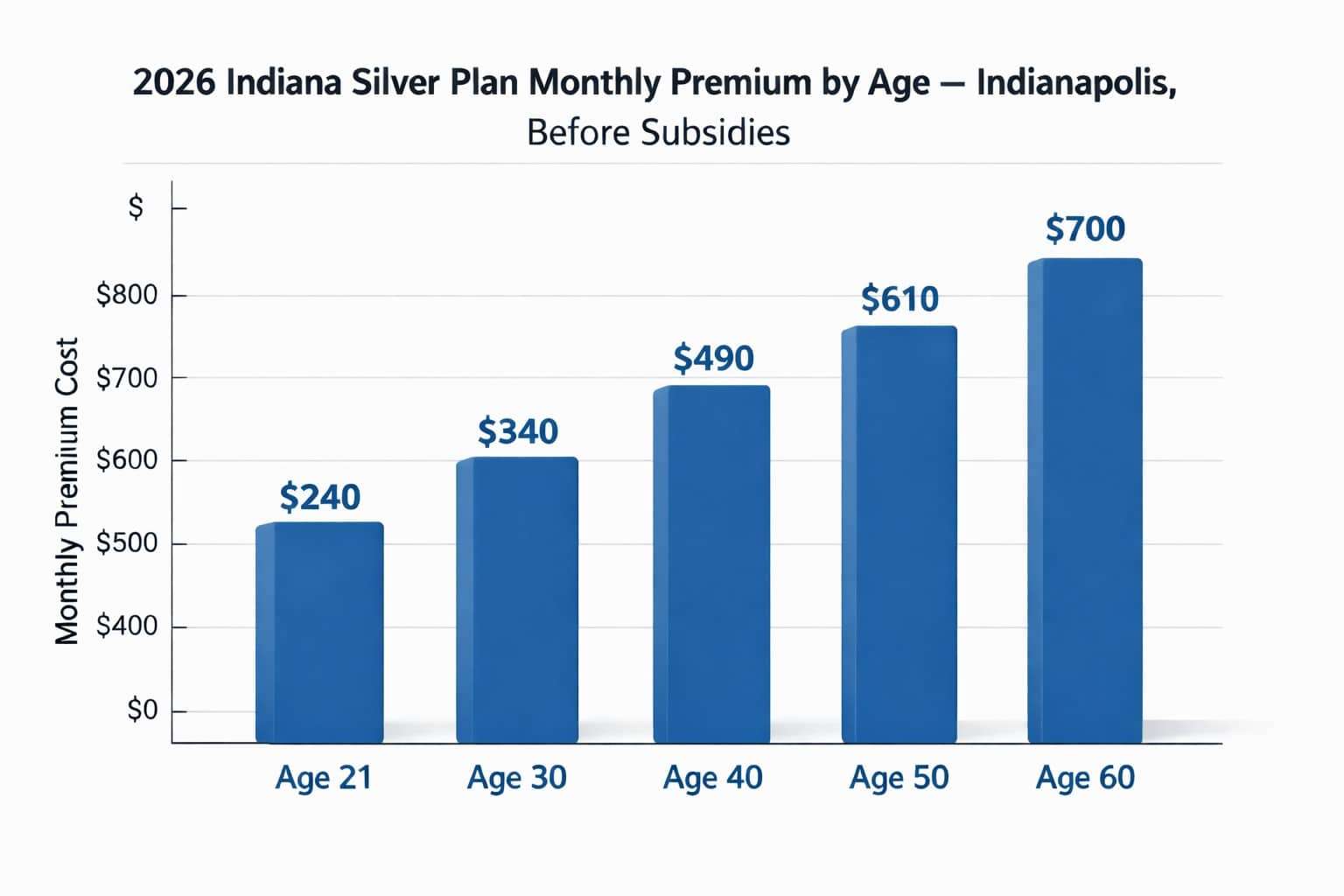

Affordable Health Insurance Indiana: Costs by Age

Indiana health insurance premiums increase with age under ACA rules. A 60-year-old can pay up to 3× what a 21-year-old pays for the same plan. For a Silver plan in Indianapolis, premiums range from approximately $240/month at age 21 to $700/month at age 60, before subsidies. Subsidies are based on income, not age, and older lower-income Hoosiers often receive larger credits that offset the age rating increase significantly.

Subsidies That Make Indiana Health Insurance Affordable

Premium tax credits reduce monthly costs for most Indiana marketplace enrollees. For 2026 coverage, roughly 80% of Indiana exchange enrollees receive subsidies, with the average credit estimated at around $481/month and net premiums near $137/month. Credits are calculated on household income and the county benchmark Silver plan. Enhanced credits above 400% FPL expired end of 2025, so Hoosiers above $62,600 (single) receive no credit in 2026.

| Annual Income (Single Adult) | % FPL (2026) | Estimated Monthly Credit | Est. Net Silver Premium |

|---|---|---|---|

| Under $22,026 | Under 138% | HIP 2.0, no marketplace needed | $0–$27/mo (POWER acct) |

| $23,000 | ~147% | ~$340–$380/mo | ~$110–$150/mo |

| $30,000 | ~192% | ~$280–$320/mo | ~$170–$210/mo |

| $40,000 | ~256% | ~$200–$240/mo | ~$250–$290/mo |

| $50,000 | ~320% | ~$130–$170/mo | ~$320–$360/mo |

| $62,600 | ~400% | Minimal or $0 | ~$490/mo (full premium) |

Silver plans + cost-sharing reductions: Indiana’s best-value tier for many Hoosiers

At incomes between $22,026 and $39,125 (138%–250% FPL), enrolling in a Silver plan unlocks cost-sharing reductions that slash the deductible from ~$4,000 to as low as $800. This combination of premium tax credits and CSRs makes Silver the most affordable health insurance Indiana residents at this income level can access, even though Bronze has a lower sticker premium.

Compare Indiana Health Insurance Plans for 2026

Ambetter and CareSource Bronze from ~$340/month, Anthem Silver from ~$490/month, HIP 2.0 at $0–$27 for incomes up to $22,026 — get a personalized Indiana quote and find the lowest-cost plan in your county.

Get a Quote Call 888-215-4045Cheapest & Most Affordable Health Insurance Indiana

The cheapest health insurance Indiana residents can buy depends on income. For those qualifying for HIP 2.0 ($0–$27/month), that is clearly the lowest-cost option. For marketplace enrollees, Bronze plans have the lowest premiums, around $175–$340/month for a 40-year-old before credits. Among carriers, Ambetter from MHS and CareSource typically offer the lowest-priced Bronze and Silver HMO plans in the counties where they operate, generally running $30–$60/month less than comparable Anthem plans.

Cheapest option: HIP 2.0

For Indiana residents earning under $22,026/year (single), HIP 2.0 Medicaid costs $1–$27/month with POWER account contributions. Dental and vision included under HIP Plus. Apply through Indiana FSSA’s HIP 2.0 program; enrollment is open year-round.

Cheapest ACA plan: Bronze HMO

Among marketplace plans, Ambetter and CareSource Bronze HMOs typically offer the lowest premiums in Indiana. Before subsidies, ~$175–$250/month for age 21–30. After subsidies, many Hoosiers at 200% FPL pay $10–$30/month for Bronze coverage.

Best value (not just cheapest): Silver + CSRs

At 138%–250% FPL, Silver with cost-sharing reductions is often cheaper in total annual cost than Bronze, even though the premium is higher. A Silver CSR plan can cut deductibles from $6,500 (Bronze) to $800, saving thousands if any care is used.

Cheapest off-exchange: Anthem PPO Silver

For Hoosiers above 400% FPL ($62,600 single) who don’t qualify for subsidies, Anthem off-exchange Silver PPO plans at $430–$460/month are typically $30–$60/month cheaper than the equivalent on-exchange Silver plan, because off-exchange plans don’t carry the CSR premium loading built into exchange Silver rates.

Strategies for Affordable Health Insurance Indiana Residents Use

Several strategies can reduce health insurance costs for Indiana residents beyond simply picking the lowest-premium plan. Hoosiers under $22,026/year (single) should apply to HIP 2.0 first. Those earning $22,026–$39,125 (138%–250% FPL) should choose Silver to unlock cost-sharing reductions that drop deductibles from ~$6,500 to as low as $800. Ambetter and CareSource typically run $30–$60/month less than Anthem for comparable Bronze and Silver plans. Hoosiers above $62,600 (400% FPL) should compare off-exchange Anthem PPO Silver at $430–$460/month against on-exchange Silver.

- Report accurate projected income: subsidies are based on projected income for the calendar year. Underreporting creates repayment obligations; overreporting leaves credits on the table. Income changes mid-year can be updated on HealthCare.gov.

- Consider Silver over Bronze if income is 138–250% FPL: cost-sharing reductions only apply to Silver plans. At these income levels, Silver’s lower deductible usually produces lower total out-of-pocket spending even with a slightly higher premium.

- Check for Hoosier Healthwise (CHIP) for children: Indiana’s CHIP program (Hoosier Healthwise Package C) covers children in working families with incomes up to approximately $84,000/year for a family of four (roughly 260% FPL in 2026) at low or no cost. This can significantly reduce family coverage costs versus covering children on a marketplace plan.

- Compare off-exchange options if above 400% FPL: Anthem off-exchange PPO Silver plans avoid the CSR premium loading built into on-exchange Silver. For Hoosiers not eligible for subsidies, this comparison often yields $30–$60/month in savings.

- Self-employed? Deduct your premium: Indiana sole proprietors and 1099 workers can deduct 100% of health insurance premiums (IRS Form 7206), reducing the effective after-tax cost by 22–37% depending on marginal tax rate.

- Verify county-specific carrier options: Indiana carrier availability varies significantly by county. Ambetter and CareSource are not available statewide; enrollees in Indianapolis or Fort Wayne may have access to lower-cost carriers unavailable in rural counties.

Example: Terre Haute family of three, household income $48,000

A Terre Haute household of three (two adults in their late 30s, one child) earning $48,000/year sits at approximately 180% FPL for a family of three in 2026. On the marketplace, a Silver plan with cost-sharing reductions would have a deductible as low as $2,500 (vs. $6,500 for Bronze). After premium tax credits of approximately $450/month, the family’s net Silver premium is roughly $200–$280/month for the adults. The child also qualifies for Hoosier Healthwise (CHIP) at minimal cost, potentially reducing total family health insurance spending to under $250/month.

County Variation in Affordable Health Insurance Indiana

Indiana health insurance costs vary by county because carriers file rates by pricing region and not all carriers operate statewide. Indianapolis metro residents (Marion, Hamilton, Hendricks, Johnson counties) typically have access to all five marketplace carriers, creating more competition and often lower benchmark premiums. Rural southern Indiana counties often have only one or two carriers available, which reduces competition and produces premiums 10–20% above the Indianapolis benchmark.

Carriers available vary by county: CareSource Indiana, Cigna, and UnitedHealthcare each operate in a limited set of Indiana counties rather than statewide. Anthem and Ambetter (Coordinated Care) have the broadest Indiana county footprints. County-level carrier availability and 2026 rate filings are published by the Indiana Department of Insurance, and federal marketplace enrollment data by state is released annually by the Centers for Medicare & Medicaid Services.

Frequently Asked Questions About Affordable Health Insurance in Indiana

Common Indiana health insurance affordability questions for 2026: average and cheapest plan costs, HIP 2.0 eligibility, subsidy strategies, and how Indiana compares to other states. Most Hoosiers at lower incomes have options under $50/month once subsidies and HIP 2.0 are considered.

What is the average cost of health insurance in Indiana per month?

The average cost of health insurance in Indiana in 2026 is approximately $340/month for a Bronze plan and $490/month for a Silver plan for a 40-year-old in Indianapolis, before subsidies. After premium tax credits, most Indiana marketplace enrollees pay under $150/month. Per 2026 marketplace data, roughly 80% of Indiana exchange enrollees receive subsidies, with the average credit around $481/month and net premiums averaging near $137/month.

What is the cheapest health insurance in Indiana?

For Hoosiers earning under $22,026/year (single), HIP 2.0 Medicaid is the lowest-cost option at $0–$27/month. Among ACA marketplace plans, Bronze HMO plans from Ambetter from MHS or CareSource Indiana are typically the cheapest available in counties where they operate, often $175–$250/month for a 30-year-old before subsidies. With subsidies applied, many Hoosiers at lower incomes pay under $50/month for marketplace coverage.

Does Indiana have affordable health insurance for low-income residents?

Yes. Indiana has two main low-income options: HIP 2.0 Medicaid for adults earning under $22,026/year (single) with $1–$27/month POWER account contributions, and subsidized Silver plans with cost-sharing reductions for incomes between 138% and 250% FPL ($22,026–$39,125 single). At these income levels, subsidized Silver plans can have deductibles as low as $800, making them among the most comprehensive affordable health insurance Indiana offers.

How do I get the most affordable health insurance in Indiana?

The most affordable health insurance in Indiana depends on your income. Apply through Indiana FSSA if income is below $22,026/year (HIP 2.0). Use HealthCare.gov if income is above that threshold. At 138%–250% FPL, choose Silver to access cost-sharing reductions, not just the lowest premium. Above 400% FPL ($62,600 single) without subsidy eligibility, compare off-exchange Anthem PPO Silver plans alongside on-exchange options, as they often cost less due to the absence of CSR premium loading.

Is health insurance cheaper in Indiana than other states?

Indiana’s marketplace premiums are near the national average. A 40-year-old Silver plan in Indianapolis at ~$490/month compares to national benchmark averages of $480–$520/month in 2026. Indiana does not have a state individual mandate (unlike California or New Jersey), which slightly reduces enrollment costs by not penalizing the uninsured but also affects the risk pool. Indiana’s HIP 2.0 Medicaid program provides strong low-cost coverage for lower-income residents, which is a meaningful affordability advantage compared to non-expansion states.

More Indiana Health Insurance Resources

Complete overview of coverage options for Hoosiers, including carriers, costs, HIP 2.0, and enrollment.

Indiana Marketplace & EnrollmentHealthCare.gov enrollment, subsidy eligibility, and open enrollment dates for Indiana residents.

Best Health Insurance in IndianaCompare top carriers in Indiana by cost and network: Anthem, Ambetter, CareSource, Cigna, and UnitedHealthcare.

Indiana Health Insurance BrokersHow licensed Indiana brokers help with plan comparison and enrollment at no cost to Hoosiers.

Indiana Individual Health InsuranceIndividual plan options for self-employed Hoosiers, freelancers, and those without employer coverage.

Indiana Short-Term Health InsuranceShort-term coverage options in Indiana for gaps between jobs or SEP windows, plus what they cover and limits.

Indiana Small Business Health InsuranceGroup coverage for Indiana businesses with 1–50 employees: SHOP marketplace, carriers, and tax credits.

PPO vs HMO vs EPO vs POSNational comparison of plan types with network rules, referrals, and costs explained for Indiana shoppers.

PPO Health Insurance PlansNational PPO plan hub covering how PPO networks, referrals, and out-of-network benefits work.

Get Indiana Health Insurance Quotes for 2026

Anthem Silver from ~$490/month, Ambetter and CareSource Bronze from ~$340/month, HIP 2.0 at $0–$27 for incomes up to $22,026 — compare all Indiana options and find your coverage.

Get a Quote Call 888-215-4045Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Indiana residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.