Indiana Health Insurance Marketplace 2026: Plans & Enrollment Guide

Indiana uses the federal marketplace at HealthCare.gov rather than a state-run exchange for individual and family health insurance enrollment. The Indiana health insurance marketplace in 2026 offers plans from five carriers, with subsidies available to most Hoosiers. This guide covers how the marketplace works, what plans cost, how to qualify for financial help, and the enrollment windows Hoosiers need to know.

What brings you here today?

How the Indiana Health Insurance Marketplace Works

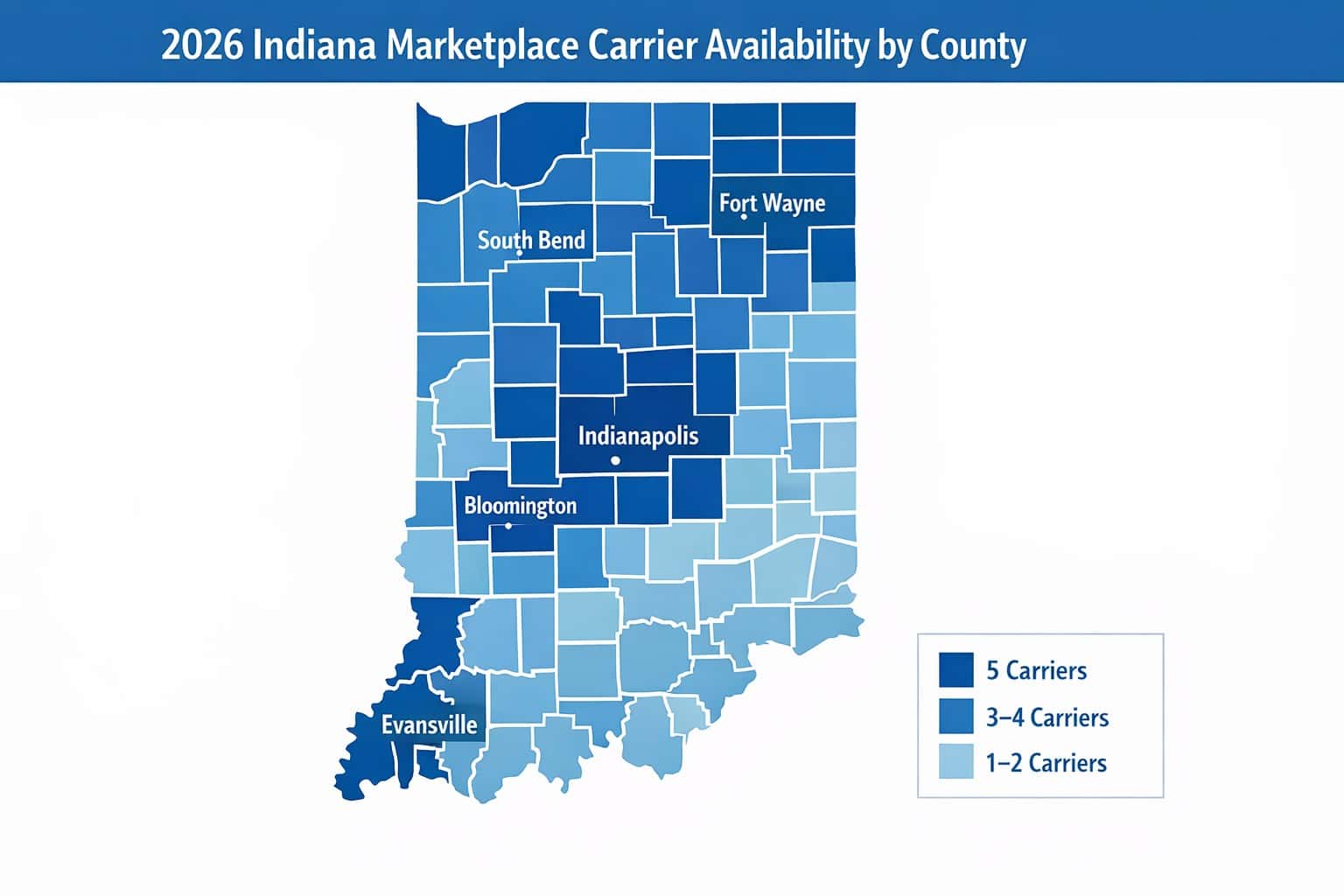

Indiana does not run a state-based exchange. Hoosiers shop for marketplace plans at HealthCare.gov, the federal platform, where five carriers offer individual and family plans in 2026: Anthem Blue Cross Blue Shield, Ambetter from Coordinated Care (Centene/MHS), CareSource Indiana, Cigna, and UnitedHealthcare. In 2025, approximately 350,000 Indiana residents enrolled in marketplace plans, with 85% receiving premium tax credits averaging $468/month.

Because Indiana uses HealthCare.gov rather than its own exchange, residents have fewer state-level tools than shoppers in states like California (Covered California) or Colorado (Connect for Health Colorado). What Indiana does have is HealthCare.gov’s full federal plan comparison interface, plus the GetCoveredIndiana.gov navigator network. This federally funded program provides free in-person enrollment assistance across the state.

Indiana’s marketplace is also distinct because the state’s Medicaid expansion, the Healthy Indiana Plan (HIP 2.0), funnels lower-income residents away from the exchange and into a separate program. Hoosiers earning under roughly $22,026/year (single adult, 138% FPL) are routed to HIP 2.0 rather than marketplace plans, which affects who shows up in Indiana’s marketplace enrollment numbers.

Indiana uses HealthCare.gov instead of a state exchange

There is no separate “Indiana marketplace website.” All plan comparison, subsidy calculations, and enrollment happen at HealthCare.gov. When searching for help, look for GetCoveredIndiana.gov navigator programs for free local assistance.

What Plans Are Available on Indiana’s Marketplace?

The Indiana health insurance marketplace for 2026 offers Bronze, Silver, Gold, and Platinum plans across five carriers, though not all carriers operate in every county. Anthem Blue Cross Blue Shield has the broadest statewide reach and is the only carrier offering PPO plans. Ambetter from Coordinated Care (Centene), CareSource, Cigna, and UnitedHealthcare primarily offer HMO or EPO plans with narrower networks. Bronze plans average ~$340/month and Silver plans ~$490/month for a 40-year-old in Indianapolis before subsidies.

Metal Tier Plans Explained

All Indiana marketplace plans are organized into four metal tiers. The tiers don’t indicate the quality of care; they determine the split between what you pay in premiums versus what you pay when you use care:

| Metal Tier | Avg. Monthly Premium (Age 40, Indianapolis) | Deductible Range | Best For |

|---|---|---|---|

| Bronze | ~$340/month | $6,000–$8,500 | Healthy adults who rarely use care; HSA-compatible |

| Silver | ~$490/month | $2,500–$5,000 | Subsidy recipients; qualifies for cost-sharing reductions |

| Gold | ~$580/month | $500–$1,500 | Regular care users; lower out-of-pocket costs |

| Platinum | ~$700/month | $0–$500 | High care users; limited carrier availability in Indiana |

Silver is the only tier that qualifies for cost-sharing reductions (CSRs)

If your income is between 100% and 250% FPL (roughly $15,060–$37,650 for a single adult), enrolling in a Silver plan unlocks lower deductibles and out-of-pocket maximums that are not available on Bronze, Gold, or Platinum. For many Hoosiers in this income range, Silver is the best financial value even if the premium looks higher.

Subsidies and Financial Help for Indiana Residents

Most Indiana health insurance marketplace enrollees qualify for premium tax credits. For 2026, credits are available to households earning between 100% and 400% FPL, roughly $15,060 to $60,240 for a single adult. The average Indiana enrollee with subsidies pays under $150/month after credits. Hoosiers above 400% FPL may also qualify under current Inflation Reduction Act provisions; verify at HealthCare.gov.

Example: Indianapolis Single Adult, Age 35, $32,000/year

At 213% FPL, this Hoosier qualifies for strong premium tax credits. Without subsidies, a Silver plan might run $450/month. After credits, the estimated net premium is approximately $85–$110/month. If income is under $37,650 (250% FPL), cost-sharing reductions on that Silver plan would also reduce the deductible from ~$4,000 to roughly $800–$1,500, a substantial benefit not visible in the headline premium.

Income Pathways for Indiana Residents

Under $22,026 (single) — HIP 2.0

Most qualify for Indiana’s Medicaid expansion (HIP 2.0). Apply through Indiana FSSA, not HealthCare.gov. Enrollment is open year-round, with no open enrollment window required.

$22,026–$37,650 — Subsidized Silver

Strong premium tax credits plus cost-sharing reductions on Silver plans. This is the highest-value zone on Indiana’s marketplace, where Silver plans effectively cost less than Bronze when CSRs are included.

$37,651–$60,240 — Subsidized Marketplace

Premium tax credits reduce costs on any metal tier. Silver remains a common choice. Credits phase out as income rises toward 400% FPL (~$60,240 for a single adult).

Above $60,240 — Full Price or Off-Exchange

Limited or no subsidies. Compare on-exchange Silver plans against off-exchange Anthem PPO plans. The off-exchange option often costs $30–$60/month less for residents above this threshold.

Find Your Indiana Marketplace Plan

Compare 2026 Indiana plans across all carriers and subsidy levels. Free enrollment assistance, no obligation.

Indiana Health Insurance Marketplace Enrollment Dates 2026

Indiana health insurance marketplace plans for 2026 were available through the annual Open Enrollment Period (OEP) that ran November 1 through January 15. Enrolling by December 15 started coverage on January 1. For anyone who missed that window, coverage is only available through a Special Enrollment Period triggered by a qualifying life event, or through HIP 2.0 Medicaid, which accepts applications year-round.

| Event | Date | Result |

|---|---|---|

| Open Enrollment begins | November 1, 2025 | Plans available to browse and enroll |

| December 15 deadline | December 15, 2025 | Enroll by this date for January 1, 2026 coverage start |

| Open Enrollment ends | January 15, 2026 | Last day to enroll for 2026 coverage (coverage starts February 1) |

| Special Enrollment | Year-round (QLE required) | 60-day window after qualifying life event |

| HIP 2.0 enrollment | Year-round | No OEP, apply anytime through Indiana FSSA |

Special Enrollment: What If You Missed Open Enrollment?

Missing open enrollment doesn’t mean going without coverage. A qualifying life event (QLE) opens a 60-day Special Enrollment Period on HealthCare.gov. Common Indiana QLEs include losing job-based coverage, getting married, having a child, moving to Indiana, or losing HIP 2.0 eligibility when income rises above 138% FPL. Short-term plans are also available in Indiana as a stopgap. Unlike California and Colorado, Indiana permits short-term coverage under federal rules.

Lost job-based coverage

Losing employer coverage, including when COBRA expires, triggers a 60-day SEP. This is the most common qualifying event for Indiana marketplace enrollees. The SEP window starts the day coverage ends, not the day of job loss.

Lost HIP 2.0 eligibility

When income rises above 138% FPL (~$22,026/year single), Hoosiers lose HIP 2.0 eligibility and gain a special enrollment window to transition to a marketplace plan. This is one of the most Indiana-specific QLEs and affects thousands of Hoosiers each year.

Moved to Indiana

Moving to Indiana from another state, or moving between Indiana counties if the move changes available plans, is a QLE. Bring documentation of your new Indiana address. Coverage can start the first of the month after enrollment.

Marriage, birth, adoption

Getting married, having a baby, or adopting a child each open a 60-day window. Newborns can be added to a marketplace plan retroactively from the date of birth. Enrollment within 60 days of the birth date is required.

Indiana Health Insurance Marketplace vs. Off-Exchange Plans

On-exchange plans are sold through HealthCare.gov and are eligible for premium tax credits and cost-sharing reductions. Off-exchange plans are sold directly by carriers outside HealthCare.gov and are not eligible for subsidies. However, for Hoosiers who don’t qualify for credits (generally those earning above $60,240 as a single adult), off-exchange Anthem PPO Silver plans typically run $30–$60/month less than equivalent on-exchange Silver plans, because they don’t carry the cost-sharing reduction loading built into exchange Silver pricing.

An enrollment assistant can compare both on- and off-exchange Indiana health insurance marketplace options simultaneously. HealthCare.gov only shows on-exchange plans, so residents comparing all options need to request off-exchange quotes separately. This is especially relevant for self-employed Hoosiers and those with higher incomes who want the flexibility of an Anthem PPO without paying the on-exchange Silver premium premium.

Frequently Asked Questions About the Indiana Marketplace

Does Indiana have its own health insurance exchange?

No. Indiana uses the federal marketplace at HealthCare.gov and does not operate a state-based exchange. All Indiana health insurance marketplace plan shopping, subsidy applications, and enrollment happen through HealthCare.gov. For free local enrollment help, Indiana residents can use the GetCoveredIndiana.gov navigator network.

When is open enrollment for Indiana marketplace plans in 2026?

Open enrollment for 2026 Indiana health insurance marketplace plans ran November 1, 2025 through January 15, 2026. Enrolling by December 15 started coverage January 1. If that window has passed, a Special Enrollment Period is available if you’ve had a qualifying life event, such as losing other coverage, getting married, or losing HIP 2.0 eligibility.

What carriers are available on Indiana’s marketplace in 2026?

Five carriers offer plans on Indiana’s 2026 health insurance marketplace: Anthem Blue Cross Blue Shield (statewide, PPO and HMO), Ambetter from Coordinated Care Corporation (Centene/MHS; HMO/EPO, strong Indianapolis and Fort Wayne presence), CareSource Indiana (HMO, select counties), Cigna (HMO/EPO, select counties), and UnitedHealthcare (HMO/EPO, select counties). Not all carriers are available in every Indiana county; rural southern Indiana counties may have only 1–2 options.

How do I apply for health insurance on Indiana’s marketplace?

Go to HealthCare.gov and create an account or log in. You’ll enter household income, household size, and zip code to see available Indiana health insurance marketplace plans and subsidy estimates. Indiana residents can also get free help applying through GetCoveredIndiana.gov navigator programs or by calling 888-215-4045 to speak with a licensed enrollment assistant who can compare both marketplace and off-exchange plans.

What is the difference between the marketplace and HIP 2.0?

The marketplace (HealthCare.gov) serves Hoosiers earning above roughly $22,026/year as a single adult, those who don’t qualify for Medicaid. HIP 2.0 (Healthy Indiana Plan) is Indiana’s Medicaid expansion program for adults earning up to 138% FPL (~$22,026 single). HIP 2.0 is administered through Indiana FSSA, not HealthCare.gov, and is open year-round. If income is near the HIP 2.0 threshold, an enrollment assistant can determine which program applies. Learn more about HIP 2.0 at the Indiana FSSA Healthy Indiana Plan page.

More Indiana Health Insurance Resources

Complete overview of coverage options for Hoosiers, including carriers, costs, HIP 2.0, and enrollment.

Best Health Insurance in IndianaCompare top carriers in Indiana by cost and network: Anthem, Ambetter, CareSource, Cigna, and UnitedHealthcare.

Indiana Health Insurance BrokersHow licensed Indiana brokers help with plan comparison and enrollment at no cost to Hoosiers.

Indiana Individual Health InsuranceIndividual plan options for self-employed Hoosiers, freelancers, and those without employer coverage.

Affordable Health Insurance in IndianaHow to lower your Indiana health insurance costs with subsidies, HIP 2.0, and off-exchange comparisons.

Indiana Short-Term Health InsuranceShort-term coverage options in Indiana for gaps between jobs or SEP windows, plus what they cover and limits.

Indiana Small Business Health InsuranceGroup coverage for Indiana businesses with 1–50 employees: SHOP marketplace, carriers, and tax credits.

PPO vs HMO vs EPO vs POSNational comparison of plan types with network rules, referrals, and costs explained for Indiana shoppers.

PPO Health Insurance PlansNational PPO plan hub covering how PPO networks, referrals, and out-of-network benefits work.

Ready to Enroll in an Indiana Marketplace Plan?

Compare 2026 Indiana marketplace plans, both on-exchange and off-exchange, with a licensed enrollment assistant at no cost to you.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Indiana residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.