Indiana Health Insurance: 2026 Plans, Costs & Enrollment Guide

Indiana residents have several paths to health coverage in 2026 — from federal marketplace plans and the state’s Medicaid expansion program to off-exchange PPO plans for those who don’t qualify for subsidies. This guide walks through the main options, what plans cost in Indiana this year, and how to find coverage that fits your situation.

What brings you here today?

How Indiana Health Insurance Works in 2026

Indiana uses the federal HealthCare.gov marketplace — not a state-run exchange — and has no state individual mandate penalty. In 2026, approximately 350,000 Hoosiers enrolled in marketplace plans; 85% received premium tax credits averaging $468/month. The benchmark Silver plan premium for a 40-year-old in Indianapolis runs approximately $490/month before subsidies.

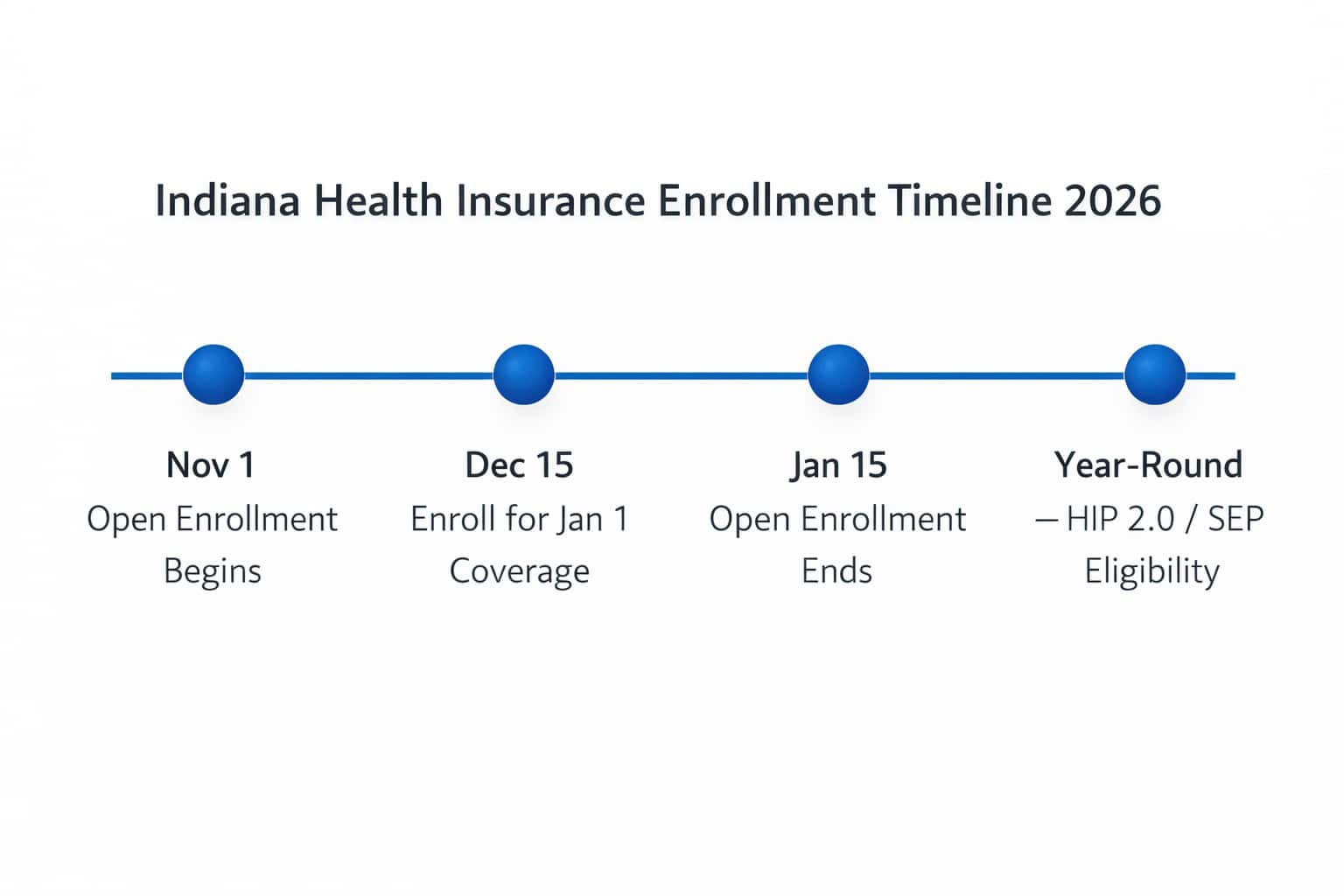

Because Indiana uses HealthCare.gov rather than a state-run exchange, Hoosiers shop the same federal platform but see only Indiana-specific carriers — Anthem, Ambetter from MHS, CareSource, Cigna, and UnitedHealthcare. Open Enrollment runs November 1 – January 15. Indiana’s lack of a state mandate distinguishes it from penalty states like California ($900+/adult) and New Jersey.

Indiana’s Medicaid expansion program — the Healthy Indiana Plan, or HIP 2.0 — operates under a federal waiver that is unique among expansion states. HIP 2.0 requires monthly contributions to a POWER account (a health savings-style account) as a condition of full benefits. This structure distinguishes Indiana’s Medicaid expansion from every other state.

No state mandate in Indiana

Unlike California ($900+/adult penalty) or New Jersey, Indiana does not charge a state tax penalty for being uninsured. Federal penalties were also eliminated after 2018. However, going without coverage still carries financial risk — one hospitalization can exceed $30,000 without insurance.

How Much Does Health Insurance Cost in Indiana?

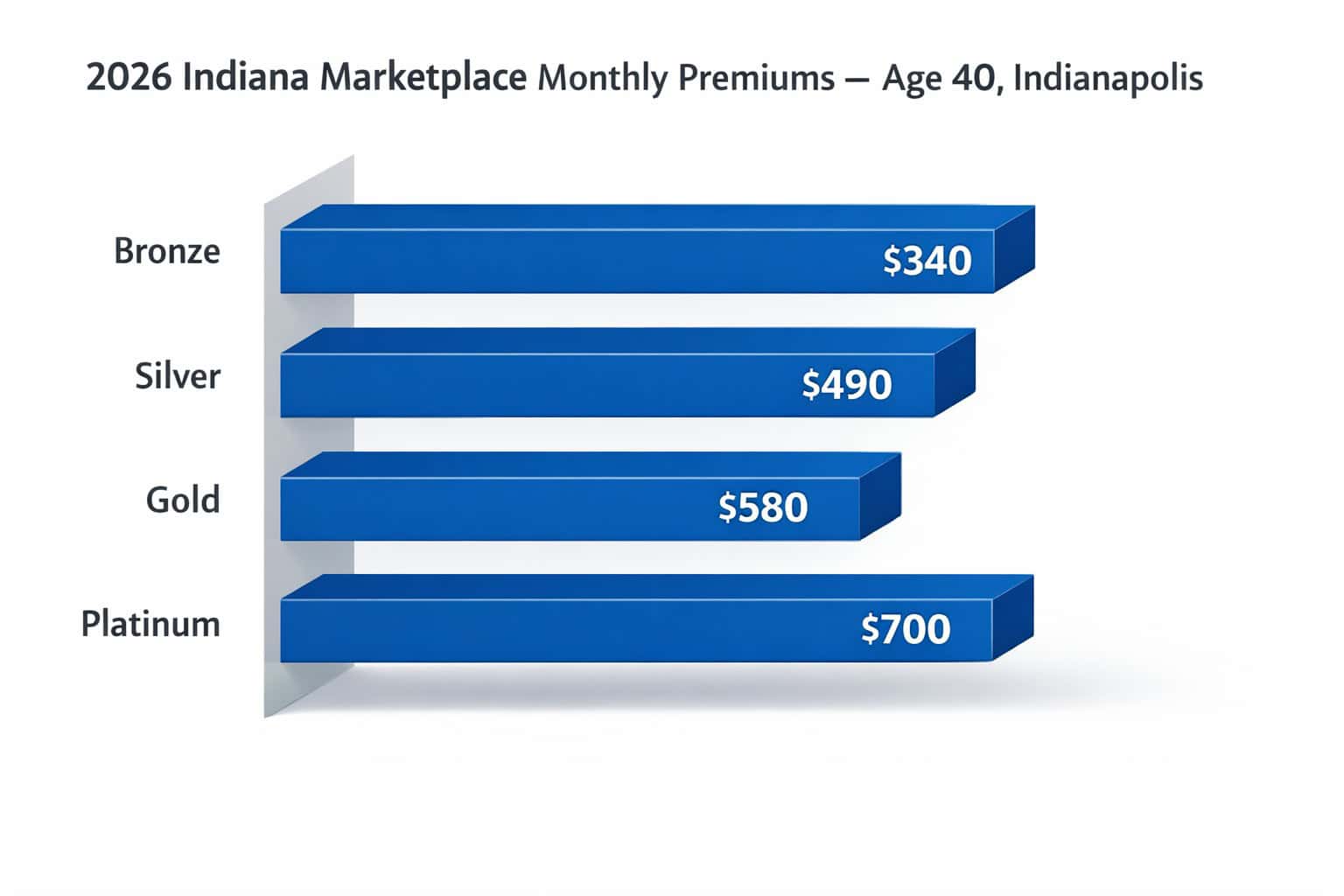

Indiana marketplace premiums for a 40-year-old average roughly $490/month for a Silver plan and $340/month for a Bronze plan in 2026, before subsidies. After premium tax credits, most Indiana marketplace enrollees pay significantly less — the average subsidized enrollee pays under $150/month. Costs vary by county, age, tobacco use, and plan type.

Bronze Plan — ~$340/mo

Age 40, Indianapolis. Lowest premiums, highest out-of-pocket costs. Best for healthy adults who rarely use care.

Silver Plan — ~$490/mo

Age 40, Indianapolis. Benchmark tier for subsidy calculations. Cost-sharing reductions available for incomes up to 250% FPL.

Gold Plan — ~$580/mo

Age 40, Indianapolis. Higher premiums, lower deductibles. Worth considering if you use care regularly.

Platinum Plan — ~$700/mo

Age 40, Indianapolis. Highest premiums, lowest cost-sharing. Rare in Indiana — limited carrier availability.

Premium Tax Credits and Subsidies

Premium tax credits are available to Indiana residents earning between 100% and 400% of the Federal Poverty Level (FPL) — roughly $15,060 to $60,240 for a single adult in 2026. The Inflation Reduction Act expanded credits for incomes above 400% FPL, though those enhanced subsidies were set to expire at the end of 2025. Indiana residents above 400% FPL shopping for marketplace plans in 2026 should verify current subsidy availability at HealthCare.gov.

Indiana residents under 100% FPL who don’t qualify for Medicaid (due to HIP 2.0 eligibility rules or immigration status) may face a coverage gap. In this situation, a licensed enrollment assistant can help identify whether HIP 2.0, CHIP, or other programs apply.

| Household Income (Single Adult) | % of FPL | Coverage Pathway |

|---|---|---|

| Under $15,060 | Under 100% | HIP 2.0 (Medicaid expansion) if eligible |

| $15,060 – $21,000 | 100–139% | HIP 2.0 or subsidized marketplace |

| $21,001 – $45,180 | 140–300% | Subsidized marketplace (strong credits) |

| $45,181 – $60,240 | 301–400% | Subsidized marketplace (moderate credits) |

| Over $60,240 | Above 400% | Full-price marketplace or off-exchange PPO |

Indiana residents above the subsidy threshold — generally those earning over $60,240 as a single adult — often find that Anthem’s off-exchange PPO Silver plans run $30–$60/month less than comparable on-exchange Silver plans, because off-exchange plans aren’t priced with cost-sharing reduction loading. See the best Indiana health insurance guide for current Anthem off-exchange rates.

Indiana’s Healthy Indiana Plan (HIP 2.0) — Medicaid Expansion

HIP 2.0 is Indiana’s Medicaid expansion program, available to adults ages 19–64 earning up to 138% of FPL (about $22,026 for a single adult in 2026). Unlike other states’ Medicaid expansions, HIP 2.0 requires monthly POWER account contributions — typically $1–$27/month based on income. Members who contribute get HIP Plus benefits; those who don’t are enrolled in the more limited HIP Basic tier.

HIP 2.0 operates under Indiana’s Section 1115 Medicaid waiver — administered by the Indiana Family and Social Services Administration (FSSA) since 2015, making it one of the longest-running consumer-directed Medicaid expansion programs in the country. The POWER account functions like a health savings account: Indiana enrollees contribute monthly, and the state and federal government add matching funds that cover the first layer of out-of-pocket costs.

HIP Plus vs. HIP Basic

HIP Plus enrollees who make required POWER account contributions get dental and vision coverage, no copays for most services, and access to non-emergency medical transportation. HIP Basic, for those who miss contributions, includes copays for many services and excludes dental and vision. Income at 0–22% FPL is contribution-exempt.

To apply for HIP 2.0, Indiana residents can apply through the Indiana FSSA Office of Medicaid Policy and Planning or through a licensed enrollment assistant. Unlike marketplace plans, HIP 2.0 enrollment is open year-round — there is no restricted open enrollment window.

Indiana Health Insurance Carriers in 2026

Indiana’s 2026 federal marketplace has 5 carriers: Anthem Blue Cross Blue Shield, Ambetter from MHS, CareSource Indiana, Cigna, and UnitedHealthcare. Anthem is the only carrier offering statewide PPO plans. Indiana’s average 2026 rate increase is approximately 7–9%. Rural southern Indiana counties may have only 1–2 carrier options while Indianapolis metro counties have 4–5 — one of the widest urban-rural gaps in the Midwest.

Anthem Blue Cross Blue Shield

- Largest carrier in Indiana by individual market share

- Offers PPO and HMO plan types on- and off-exchange

- Off-exchange PPO plans available statewide

- Strong provider network — most Indiana hospitals in-network

- NCQA accredited

Ambetter from MHS

- Managed Health Services — Indiana-based carrier

- HMO and EPO plan types on exchange

- Competitive Silver and Bronze premiums

- Strong presence in Indianapolis, Fort Wayne, and Evansville

- Also administers HIP 2.0 Medicaid in Indiana

CareSource Indiana

- Expanded to Indiana marketplace after 2020

- HMO plan type; lower-cost Silver options

- Focused on Medicaid-adjacent income levels

- Available in select Indiana counties

Cigna Health and Life Insurance Company

- National carrier returning to/expanding in Indiana’s 2026 marketplace

- HMO and EPO plan options

- Available in select Indiana counties — confirm by ZIP before enrolling

- Uses Cigna’s national provider network for in-network care

UnitedHealthcare Insurance Company

- National carrier offering 2026 Indiana marketplace plans

- HMO/EPO options with access to UnitedHealthcare’s national network

- Available in select Indiana counties — confirm coverage by ZIP

- Large provider network useful for Hoosiers with out-of-state providers

Indiana Farm Bureau Health Plans

- ACA-exempt health benefit plans — not minimum essential coverage

- Available only to Farm Bureau members

- Not eligible for premium tax credits

- Significant Indiana market presence — important to understand limitations

Indiana Farm Bureau Health Plans are NOT ACA-compliant

These plans do not meet minimum essential coverage requirements, may exclude pre-existing conditions, and do not cover all essential health benefits. They cannot be used to demonstrate coverage for tax purposes. Carefully review benefits before enrolling.

Plan Types: HMO, PPO, and EPO in Indiana

Most Indiana marketplace carriers offer HMO or EPO plans — Ambetter from MHS and CareSource primarily sell HMOs starting around $430/month Silver, while Anthem offers the only PPO plans in Indiana’s individual market at approximately $490–$560/month Silver. An Anthem PPO runs $60–$90/month more than a comparable HMO, but provides direct specialist access at IU Health, Franciscan Health, and Ascension St. Vincent without referrals.

HMO

Referrals required. Must use in-network providers. Lower premiums. Best for predictable, routine care. MHS/Ambetter, CareSource, Cigna, and UnitedHealthcare offer HMO plans in Indiana.

EPO

No referrals, but network-only. Out-of-network care not covered except emergencies. Moderate premiums. Ambetter from MHS offers EPO options.

PPO

No referrals. Out-of-network allowed. See any licensed Indiana or out-of-state provider. Highest premiums. Anthem is the primary PPO carrier in Indiana. PPO vs HMO vs EPO comparison →

How to Enroll in Indiana Health Insurance

Indiana residents enroll through HealthCare.gov during Open Enrollment, which runs November 1 through January 15 — enrolling by December 15 starts coverage January 1. Approximately 350,000 Hoosiers selected marketplace plans during the 2025 open enrollment window, with 85% qualifying for premium tax credits. A qualifying life event opens a 60-day Special Enrollment Period; HIP 2.0 enrollment is open year-round.

Check your income and eligibility

Determine whether you qualify for HIP 2.0 (under ~$22,026/year single), premium tax credits (up to ~$60,240), or full-price coverage. This determines which products and savings you can access.

Compare plans at HealthCare.gov or with an enrollment assistant

Indiana’s marketplace is at HealthCare.gov — there is no separate state exchange. Enrollment assistants can also show you off-exchange plans (like Anthem PPO) not visible on the federal site.

Select a plan and confirm your coverage starts

After enrolling, you’ll receive a member ID card within 2–3 weeks. Confirm your first premium payment is received — coverage does not activate until the first payment clears.

Qualifying Life Events in Indiana

Outside of open enrollment, a qualifying life event (QLE) opens a 60-day window for Indiana residents to enroll through HealthCare.gov or switch plans. Hoosiers who lose HIP 2.0 eligibility — a common occurrence when income rises above 138% FPL — also trigger a special enrollment window. Common Indiana QLEs include:

- Losing job-based coverage (including COBRA expiration)

- Moving to Indiana from another state or county

- Getting married or divorced

- Having or adopting a child

- Losing eligibility for HIP 2.0 or other Medicaid programs

- Turning 26 and aging off a parent’s plan

Compare Indiana Health Insurance Plans

Get quotes for marketplace, PPO, and off-exchange plans side by side. No cost, no obligation.

Family and Children’s Coverage in Indiana

Indiana families can enroll in marketplace plans covering all household members, or use CHIP (Children’s Health Insurance Program, called Hoosier Healthwise in Indiana) for children in households earning up to 250% FPL — roughly $75,150 for a family of four in 2026. Hoosier Healthwise covers children at low or no cost and includes dental and vision benefits not always included in adult marketplace plans.

For families above the CHIP threshold, a family Silver plan in Indianapolis averages approximately $1,100–$1,400/month before subsidies, depending on ages of covered family members. Families with employer offers of coverage that meet affordability standards may not qualify for marketplace subsidies, even if their income would otherwise qualify. A licensed enrollment assistant can evaluate whether the employer offer creates an affordability barrier.

Example: Indiana Family of Four

A Fort Wayne family of four — two adults in their mid-30s, two children — with a household income of $72,000 (about 240% FPL) would qualify for a Silver plan with premium tax credits. Their estimated net monthly premium after credits: approximately $320–$400/month depending on the carrier and county. The children would also qualify for Hoosier Healthwise, potentially reducing the family’s coverage costs further.

PPO Plans and Off-Exchange Coverage in Indiana

Anthem Blue Cross Blue Shield is Indiana’s only statewide PPO carrier, offering off-exchange PPO plans covering any licensed provider without a referral. For residents earning above $60,240 (single adult, 400% FPL), Anthem off-exchange PPO Silver plans typically run $430–$460/month — roughly $30–$60/month less than equivalent on-exchange Silver plans, which carry cost-sharing reduction loading. The PPO health insurance plans guide covers how Indiana’s options compare nationally.

Indiana’s major health systems — IU Health (the state’s largest), Franciscan Health, Ascension St. Vincent, Parkview Health in Fort Wayne, and Deaconess in Evansville — are broadly in-network with Anthem PPO plans. This statewide network access is the key reason self-employed Hoosiers, frequent travelers, and those with established specialist relationships often prefer PPO coverage over HMO alternatives.

For a detailed comparison of Indiana’s 2026 Anthem PPO tiers, network access at IU Health and Franciscan Health, and off-exchange pricing, the best health insurance in Indiana guide covers carriers, costs, and enrollment options. For a broader look at national PPO plan structures, the PPO Health Insurance Plans overview covers national plan structures.

Small Business Health Insurance in Indiana

Indiana small businesses with 1–50 full-time employees can offer group coverage through the SHOP marketplace or directly through Anthem or MHS. Businesses with fewer than 25 FTE employees averaging under $58,000/year in wages may qualify for the Small Business Health Care Tax Credit — worth up to 50% of premiums paid, potentially saving $3,000–$8,000/year for a small team. Indiana has no state employer mandate; the federal 50-FTE threshold triggers shared responsibility provisions.

Indiana has no state employer mandate. Businesses with 50 or more full-time equivalents trigger federal shared responsibility provisions; those under 50 FTE can offer coverage voluntarily through carriers like Anthem and MHS without penalty exposure. Indiana’s lack of a state mandate makes it more flexible than states with additional employer-level requirements. For help structuring group coverage, the Indiana small business health insurance guide covers SHOP options, carriers, and tax credits.

Short-Term Health Insurance in Indiana

Indiana allows short-term health insurance plans — unlike California and Colorado, which ban them entirely. Indiana follows federal rules: terms up to 364 days, renewable for up to 36 months. Short-term premiums typically run 40–60% less than ACA premiums — a Bronze equivalent may cost $120–$180/month compared to $340/month ACA Bronze — but these plans can deny pre-existing conditions and exclude essential health benefits.

Indiana’s short-term rules — including Anthem Blue Cross Blue Shield’s short-term product lineup, the 364-day maximum term, and ACA-compliant gap alternatives via Indiana special enrollment — are covered in detail in the Indiana short-term health insurance guide.

Which Indiana Plan Is Right for You?

The right Indiana plan depends on income, health usage, and provider preferences. Residents earning under $22,026 (single adult) likely qualify for HIP 2.0; those between $22,026 and $60,240 should start on the marketplace for subsidy eligibility. Frequent care users often save money with a Gold plan despite higher premiums — Indiana Gold plans typically reduce annual out-of-pocket costs by $1,500–$3,000 compared to Bronze for the same care volume.

Low income (under 138% FPL)

Apply for HIP 2.0. Make POWER account contributions to access HIP Plus benefits including dental and vision. Enrollment is open year-round through Indiana FSSA.

Moderate income (139–300% FPL)

Strong premium tax credits available on the marketplace. Silver plans with cost-sharing reductions are often the best value at this income level — lower deductibles and out-of-pocket maximums.

Higher income (above 400% FPL)

Limited or no subsidies. Compare on-exchange Silver plans against off-exchange Anthem PPO plans — the off-exchange PPO often wins on cost and network flexibility for this group.

Self-employed / freelance

Off-exchange PPO plans allow specialist access without referrals — valuable when managing your own care without an employer HR team. Premiums are 100% deductible as a business expense.

Family with children

Check Hoosier Healthwise eligibility for children first — it covers kids up to 250% FPL at low or no cost. Adults can enroll separately in a marketplace plan if income is above Medicaid thresholds.

Between jobs

Job loss triggers a Special Enrollment Period. If the gap is expected to be short, compare COBRA costs against a Silver marketplace plan — marketplace premiums with subsidies often beat COBRA significantly.

Frequently Asked Questions About Indiana Health Insurance

Does Indiana have a penalty for not having health insurance?

No. Indiana does not have a state individual mandate or tax penalty for being uninsured. The federal penalty was also eliminated after the 2018 tax year. However, going without coverage carries financial risk — a single hospitalization or emergency can result in bills exceeding $30,000 without insurance.

What is HIP 2.0 and who qualifies in Indiana?

HIP 2.0 (Healthy Indiana Plan) is Indiana’s Medicaid expansion program for adults ages 19–64 earning up to 138% of the Federal Poverty Level — approximately $22,026 per year for a single adult in 2026. It is unique among Medicaid expansion programs because it requires monthly POWER account contributions (typically $1–$27/month) to access full HIP Plus benefits. Enrollment is open year-round through the Indiana FSSA.

Can I use Indiana Farm Bureau health plans as my main coverage?

Indiana Farm Bureau health plans are ACA-exempt benefit plans, not minimum essential coverage. They may have pre-existing condition exclusions, benefit caps, and coverage gaps that standard marketplace plans do not have. They are available only to Farm Bureau members and are not eligible for premium tax credits. They should not be treated as equivalent to marketplace or employer-sponsored plans.

When is open enrollment for Indiana health insurance?

Open enrollment for 2026 Indiana marketplace plans runs November 1 through January 15. Enrolling by December 15 gets coverage starting January 1. HIP 2.0 (Medicaid) enrollment is open year-round. Outside open enrollment, qualifying life events — like losing job-based coverage, getting married, or moving to Indiana — trigger a 60-day Special Enrollment Period.

What is the difference between a marketplace plan and an off-exchange plan in Indiana?

Marketplace plans are sold through HealthCare.gov and are eligible for premium tax credits and cost-sharing reductions. Off-exchange plans are sold directly by carriers like Anthem and are not eligible for subsidies, but may have lower base premiums for people who don’t qualify for credits. Off-exchange PPO plans are a common choice for higher-income Hoosiers who want broad provider access without the cost-sharing reduction loading built into on-exchange Silver plan pricing.

How do I find a health insurance enrollment assistant in Indiana?

Licensed enrollment assistants can help you compare marketplace, off-exchange, and Medicaid options at no cost to you — carrier commissions cover the service. ForHealthInsurance.com serves Indiana residents at 888-215-4045. You can also use Indiana’s GetCoveredIndiana.gov navigator network for free in-person enrollment assistance through federally funded programs.

Indiana Health Insurance Resources

HealthCare.gov enrollment, subsidy eligibility, county carrier availability, and 2026 open enrollment dates

Best Health Insurance in IndianaCompare Anthem PPO, Ambetter from MHS, CareSource, Cigna, and UnitedHealthcare with network access at IU Health and Franciscan

Indiana Health Insurance BrokerWork with a licensed Indiana broker at no cost — compare marketplace, off-exchange, and HIP 2.0 options

Individual Health Insurance IndianaCoverage for self-employed Hoosiers, freelancers, and residents purchasing outside an employer plan

Affordable Health Insurance IndianaHIP 2.0, Hoosier Healthwise, subsidy tables, and how 2026 premium credits affect Indiana families

Short-Term Health Insurance Indiana364-day short-term plans, Anthem’s lineup, and ACA-compliant alternatives for coverage gaps

Small Business Health Insurance IndianaGroup plans, SHOP marketplace, and ICHRA options for Indiana’s small business employers

PPO vs HMO vs EPO vs POSCompare plan type structures — network access, referrals, and out-of-pocket cost differences

PPO Health Insurance PlansNational PPO plan overview — flexible provider access, no referrals required, in and out of network

Ready to Find Your Indiana Health Insurance Plan?

Compare 2026 Indiana health insurance plans — marketplace, HIP 2.0, and off-exchange PPO options — for individuals, families, and Indiana small businesses. Speak with a licensed enrollment assistant at no cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Indiana residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.