Individual Health Insurance in Kentucky: 2026 Private & Marketplace Plans

Kentuckians who don’t have employer-sponsored coverage, Medicare, or Medicaid need individual health insurance — purchased through the kynect marketplace or directly from a carrier like Anthem. This guide covers how to buy individual health insurance in Kentucky in 2026, what plans cost for different situations, and how to decide between kynect and off-exchange options.

What’s your situation?

Who Needs Individual Health Insurance in Kentucky?

Individual health insurance in Kentucky covers anyone who does not have access to employer-sponsored group coverage, Medicare, or Medicaid. In 2026, approximately 86,000 Kentuckians purchased individual marketplace plans through kynect — down from 97,000 in 2025 after subsidies shrank. Additional Kentuckians buy individual coverage directly from Anthem off-exchange. The most common individual buyers are self-employed workers, freelancers, early retirees under 65, and people between jobs.

Kentucky does not require residents to carry health insurance — there is no state individual mandate and no federal penalty since 2019. But going without coverage carries substantial financial risk. The average inpatient hospital stay in Kentucky costs over $12,000, and a single emergency room visit can exceed $3,000 without insurance. Individual health insurance in Kentucky protects against these costs while providing access to preventive care, prescription coverage, and mental health services required under the ACA’s essential health benefits.

Where to Buy Individual Health Insurance in Kentucky

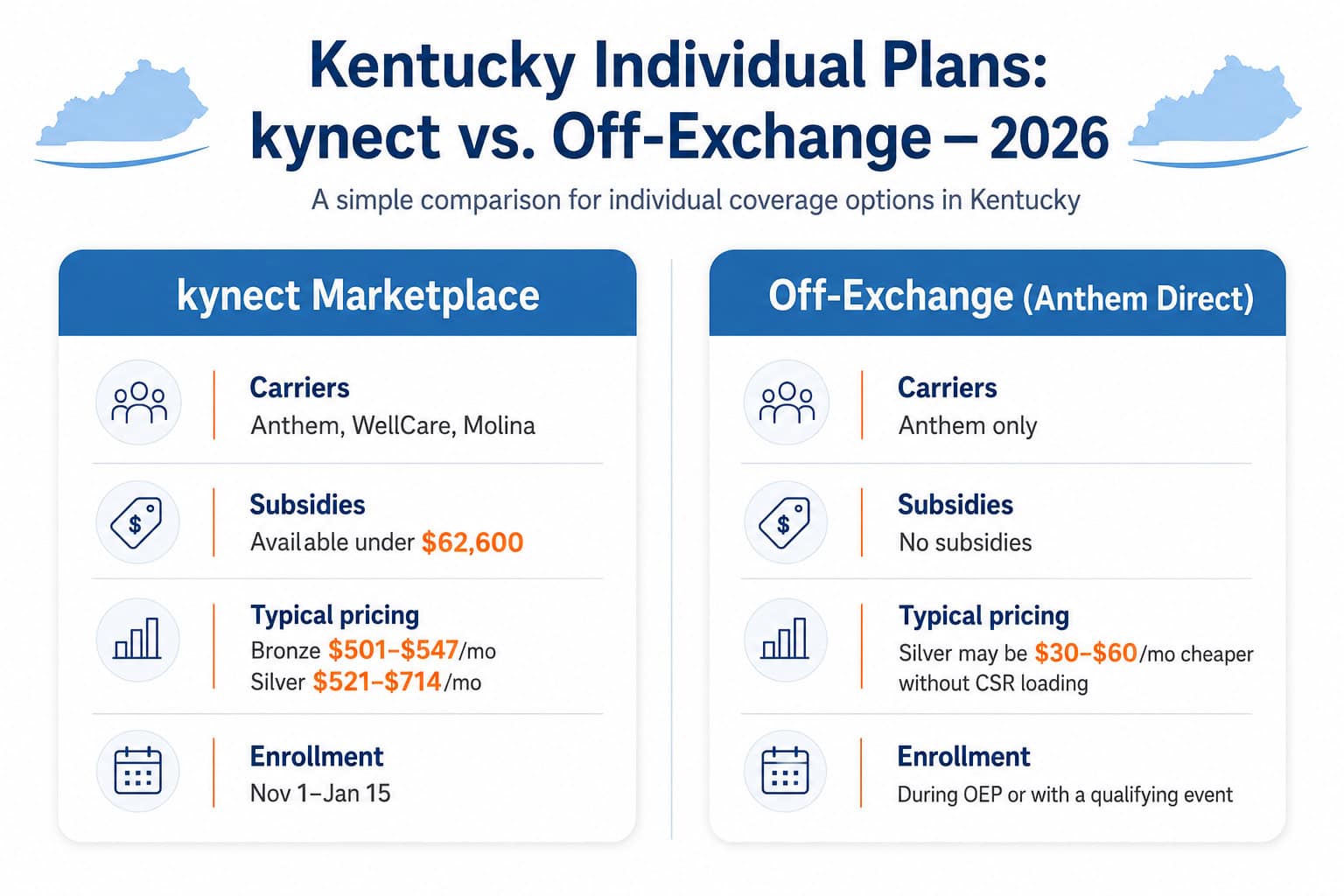

Individual health insurance in Kentucky is available through two channels: the kynect state marketplace (kynect.ky.gov) and directly from carriers off-exchange. Kynect offers plans from three carriers — Anthem, Ambetter from WellCare, and Molina — with subsidy eligibility for incomes up to $62,600 (single adult). Off-exchange plans from Anthem are available year-round and may carry lower premiums for those who don’t qualify for subsidies.

| Feature | kynect Marketplace | Off-Exchange (Anthem Direct) |

|---|---|---|

| Carriers available | Anthem, WellCare, Molina (county-dependent) | Anthem only |

| Subsidy eligible | Yes — incomes $15,960–$62,600 (single) | No |

| Cost-sharing reductions | Yes — Silver plans, incomes under $39,900 | No |

| Silver premium (age 40) | $521–$714/mo depending on carrier | May be $30–$60/mo less (no CSR loading) |

| Enrollment window | Nov 1 – Jan 15 (or SEP with qualifying event) | Nov 1 – Jan 15 (or SEP) |

| Best for | Incomes under $62,600 (subsidy eligible) | Incomes above $62,600 (no subsidies available) |

The decision between kynect and off-exchange is straightforward for most Kentuckians: if income is under $62,600 (single adult), enroll through kynect to access premium tax credits that reduce monthly costs significantly. If income is above $62,600, compare kynect full-price plans against off-exchange Anthem plans — the off-exchange Silver option may run $30–$60/month less because it doesn’t carry cost-sharing reduction loading. A licensed enrollment assistant can run both quotes at no cost. The kynect marketplace enrollment guide covers the full enrollment process.

Individual Plan Types Available in Kentucky

Kentucky’s individual health insurance market offers HMO plans from all three kynect carriers, plus Anthem’s Pathway and Transition network tiers that provide broader access. WellCare HMO Silver starts at ~$617/month (age 40) with $6,378 deductibles. Anthem Pathway Silver runs ~$714/month with $3,640 deductibles. Anthem Transition plans — available in 48 counties — provide the broadest network access to Baptist Health, Norton Healthcare, and UK HealthCare without referrals.

WellCare / Molina HMO

Lowest premiums. Referrals typically required for specialists. WellCare Silver ~$617/mo, Molina Silver ~$521/mo (Lexington area only). Best for budget-focused individuals who use a primary care physician as their main contact point.

Anthem Pathway

Mid-range premiums, narrower Anthem network. Silver ~$714/mo with $3,640 deductible. Available in all 120 counties. Lower cost than Transition but verify your doctors are in-network before enrolling.

Anthem Transition

Broadest network access. Includes Baptist Health, Norton Healthcare, UK HealthCare. Available in 48 counties. Higher premiums than Pathway. Best for individuals who need specialist access without referrals. See carrier network details →

Individual Coverage for Self-Employed Kentuckians

Self-employed Kentuckians — including freelancers, independent contractors, gig workers, and small business owners without group plans — make up a significant share of Kentucky’s individual health insurance market. Self-employed individuals can deduct 100% of their health insurance premiums as a business expense on their federal tax return, reducing the effective after-tax cost. A 40-year-old self-employed Kentuckian in a 22% federal tax bracket paying $617/month for WellCare Silver effectively pays ~$481/month after the deduction.

Self-employed Kentuckians who earn under $62,600/year should start on kynect — the premium tax credit applies first, and the self-employment deduction applies to whatever portion remains. Those above the subsidy threshold should compare kynect full-price plans against off-exchange Anthem Transition plans, then apply the self-employment deduction to the chosen plan’s premium. Anthem’s broader Transition network is particularly valuable for self-employed individuals who manage their own care without an employer HR team to coordinate referrals.

Example: Self-Employed Graphic Designer in Louisville

A 35-year-old freelance graphic designer in Louisville earning $48,000/year (about 301% FPL) qualifies for a modest premium tax credit on kynect. After the credit, a WellCare Silver plan might cost approximately $350/month. The self-employment health insurance deduction reduces that further to an effective ~$273/month after tax savings. Without both the credit and the deduction, the same plan would cost $617/month — the combined savings is $344/month or $4,128/year.

Self-employment health insurance deduction: The IRS allows self-employed individuals to deduct 100% of health insurance premiums paid for themselves and their family — directly reducing adjusted gross income. Unlike itemized deductions, this write-off applies even if you take the standard deduction. For a Kentuckian paying $617/month in a 22% bracket, the annual deduction is worth approximately $1,629 in federal tax savings.

Individual Coverage Between Jobs in Kentucky

Job loss triggers a 60-day Special Enrollment Period on kynect, allowing Kentuckians to purchase individual health insurance outside of the normal November–January open enrollment window. COBRA continuation coverage through a former employer averages approximately $702/month for an individual in Kentucky — compared to a subsidized kynect Silver plan that often costs $150–$300/month depending on income. For most between-jobs Kentuckians, a kynect marketplace plan is significantly cheaper than COBRA.

The timing matters: COBRA coverage can be elected retroactively up to 60 days after job loss, but kynect enrollment should happen as soon as possible to start coverage on the first of the following month. Kentuckians who expect a short gap (under 3 months) sometimes use COBRA’s retroactive feature as a safety net — electing COBRA only if a medical expense occurs during the gap — while also enrolling in a kynect plan for ongoing coverage. This strategy requires careful timing and is best discussed with a licensed enrollment assistant.

Don’t miss the 60-day SEP window: After losing job-based coverage, you have exactly 60 days to enroll on kynect. Miss this window and you must wait until the next open enrollment period (November 1 – January 15) — which could leave you uninsured for months. COBRA’s 60-day election window runs concurrently, so act on kynect first.

COBRA vs. kynect quick math: A 40-year-old in Jefferson County (Louisville) losing a $702/month COBRA-eligible employer plan and earning $45,000/year would pay approximately $180/month for a subsidized kynect Silver plan — saving $522/month. Over a 6-month job search, that’s $3,132 in savings by choosing individual health insurance in Kentucky through kynect over COBRA.

Compare Individual Kentucky Health Insurance Plans

See kynect marketplace and off-exchange Anthem plans for your county — check subsidies, compare networks, and enroll with licensed help at no cost.

What Does Individual Health Insurance Cost in Kentucky?

Individual health insurance in Kentucky costs between $501 and $895/month for a 40-year-old before subsidies, depending on carrier and metal tier. After premium tax credits, most subsidized enrollees pay under $200/month. Kentucky’s 2026 rate increases of 16.3%–37% across carriers made individual coverage significantly more expensive than 2025 — particularly for households above the $62,600 subsidy cutoff who now pay full price. WellCare Bronze (~$501/mo) is the cheapest unsubsidized option statewide.

| Metal Tier | WellCare (Age 40) | Anthem Pathway (Age 40) | Deductible Range |

|---|---|---|---|

| Catastrophic | — | ~$520/mo | $10,600 |

| Bronze | ~$501/mo | ~$547/mo | $7,850–$10,600 |

| Silver | ~$617/mo | ~$714/mo | $3,640–$6,378 |

| Gold | ~$687/mo | ~$895/mo | $1,125–$2,300 |

2026 rate increase context: Kentucky’s individual market premiums rose 16.3%–37% for 2026 after the enhanced ARP subsidies expired and carriers revised filings upward. A 40-year-old Kentuckian who paid ~50/month for a Silver plan in 2025 now pays 17–14/month unsubsidized. Most subsidized enrollees saw smaller net increases — subsidies averaged 34/month for 2026 kynect enrollees, per CMS enrollment data.

Age is the largest variable in individual plan pricing. A 26-year-old in Kentucky pays roughly 60% of a 40-year-old’s premium for the same plan, while a 60-year-old pays approximately 200%–250% more. Kentucky does not allow tobacco rating surcharges above the ACA’s 50% maximum, and gender-based pricing is prohibited. For Kentuckians under 30, Catastrophic plans at approximately $520/month offer the lowest premiums with $10,600 deductibles and three free primary care visits per year.

Individual Coverage for Early Retirees (Under 65)

Kentuckians who retire before Medicare eligibility at age 65 face the highest individual health insurance premiums in the market — a 60-year-old in Kentucky pays approximately $1,200–$1,500/month for a Silver plan before subsidies. After the 2026 subsidy expiration, a 60-year-old in Christian County earning $62,700/year saw premiums jump from $444 to $933/month. Early retirees with income under $62,600 can still access premium tax credits through kynect, making subsidized coverage far cheaper than COBRA or retiree health benefits.

For early retirees with assets but lower taxable income — common when drawing from savings rather than earned income — structuring income to stay below 400% FPL ($62,600 single, $128,600 couple) can preserve subsidy eligibility on kynect. This strategy requires careful tax planning with a financial advisor, as Roth conversions, capital gains, and Social Security income all count toward modified adjusted gross income (MAGI) used for subsidy calculations. According to the Kentucky Department of Insurance, about 80% of kynect enrollees qualified for subsidies averaging $634/month — making income management a high-value strategy for early retirees near the threshold. The affordable health insurance Kentucky guide covers additional cost-reduction strategies.

How to Choose the Right Individual Plan in Kentucky

Choosing individual health insurance in Kentucky comes down to three decisions: metal tier (how much you want to pay monthly vs. at the doctor), carrier (which network includes your doctors and hospitals), and channel (kynect for subsidies vs. off-exchange for potentially lower unsubsidized premiums). A Kentuckian in Fayette County has the most options — three carriers on kynect plus off-exchange Anthem. A Kentuckian in Harlan County has only Anthem.

Healthy, rarely uses care

Bronze plan with HSA. WellCare Bronze ~$501/mo or Anthem Bronze ~$547/mo. High deductibles ($7,850–$10,600) but lowest monthly cost. HSA contributions reduce after-tax costs further. Best for individuals under 40 with no chronic conditions.

Moderate care user

Silver plan — especially with CSR if income qualifies (under ~$39,900 single). A CSR Silver plan at 150% FPL can have deductibles under $1,000, making it the best value in Kentucky’s individual market for regular doctor visits and prescriptions.

Frequent care or chronic conditions

Gold plan. WellCare Gold ~$687/mo with $1,125 deductible is the strongest value for high utilizers. Anthem Gold runs $895/mo with $2,300 deductible — significantly more expensive for a higher deductible.

Needs specific hospitals/specialists

Anthem Transition plan. The only individual option in Kentucky with guaranteed in-network access to Baptist Health, Norton Healthcare, and UK HealthCare. Available in 48 counties. Verify your county has Transition access before enrolling.

Frequently Asked Questions About Individual Kentucky Coverage

Do I need health insurance in Kentucky?

Kentucky does not have a state individual mandate — there is no tax penalty for being uninsured. The federal penalty was eliminated after 2018. However, going without individual health insurance in Kentucky carries financial risk: the average inpatient hospital stay costs over $12,000, and a single emergency visit can exceed $3,000 without coverage.

Can I buy individual health insurance outside of open enrollment?

Only with a qualifying life event — job loss, marriage, divorce, having a child, moving to a new county, or losing Medicaid eligibility. These events trigger a 60-day Special Enrollment Period on kynect. Medicaid and KCHIP enrollment is available year-round. Off-exchange plans from Anthem also require a qualifying event or OEP enrollment.

Is COBRA or a kynect plan cheaper in Kentucky?

For most Kentuckians, a subsidized kynect plan is significantly cheaper than COBRA. COBRA averages approximately $702/month for individual coverage in Kentucky, while a subsidized kynect Silver plan often costs $150–$300/month depending on income. COBRA makes sense only if your employer plan has specific coverage (like an in-progress treatment) that a marketplace plan wouldn’t cover.

Can self-employed Kentuckians deduct health insurance premiums?

Yes — self-employed individuals can deduct 100% of their health insurance premiums as a business expense on their federal tax return. This applies to premiums paid through kynect or off-exchange. A 40-year-old self-employed Kentuckian in a 22% federal tax bracket paying $617/month for individual health insurance in Kentucky effectively pays ~$481/month after the deduction.

What is the cheapest individual plan in Kentucky for 2026?

WellCare Expanded Bronze at approximately $501/month (age 40) is the cheapest individual marketplace plan available statewide. Molina offers the cheapest Silver at ~$521/month but only in 5 Lexington-area counties. After subsidies, many Kentuckians pay under $150/month. Kentuckians earning under $22,025/year (single adult) qualify for Medicaid at $0/month — the cheapest coverage option by far.

Should I buy individual insurance through kynect or directly from Anthem?

If your income is under $62,600 (single adult), enroll through kynect — premium tax credits and cost-sharing reductions are only available on-exchange. If your income is above the subsidy threshold, compare kynect full-price plans against off-exchange Anthem plans — the off-exchange Silver option may be $30–$60/month cheaper because it doesn’t carry cost-sharing reduction loading. A licensed enrollment assistant can run both quotes at no cost.

Kentucky Health Insurance Resources

2026 pillar guide — kynect, Kentucky Medicaid, KCHIP, HB 2 reforms, and the ~89,000 Kentucky enrollees

Kentucky Health Insurance Marketplacekynect enrollment, subsidy eligibility, county carrier availability, and 2026 open enrollment dates

Best Health Insurance in KentuckyCompare all 3 carriers — Anthem, Ambetter by WellCare, Passport by Molina — with Kentucky county coverage

Affordable Health Insurance KentuckyKentucky Medicaid, KCHIP, premium tables, and how HB 2 affects 478,900 expansion adults

Short-Term Health Insurance Kentucky4-month gap coverage limits under federal rules — bridge between jobs or before Kentucky kynect OEP

PPO Health Insurance PlansCompare PPO options nationwide — flexible provider access, no referrals required, in and out of network

Find Individual Health Insurance in Kentucky

Compare 2026 kynect and off-exchange Anthem plans for your Kentucky county. Check subsidy eligibility and enroll with licensed enrollment assistance at no cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Kentucky residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.