Short-Term Health Insurance in Kentucky: 2026 Temporary Plans

Short-term health insurance in Kentucky provides temporary medical coverage for Kentuckians in gap situations — between jobs, waiting for employer coverage to start, or bridging the months until the next open enrollment. This guide covers Kentucky’s current short-term rules, what these plans cost compared to ACA-compliant options on kynect, and when temporary coverage makes sense versus alternatives.

What’s your gap situation?

Kentucky Short-Term Health Insurance Rules in 2026

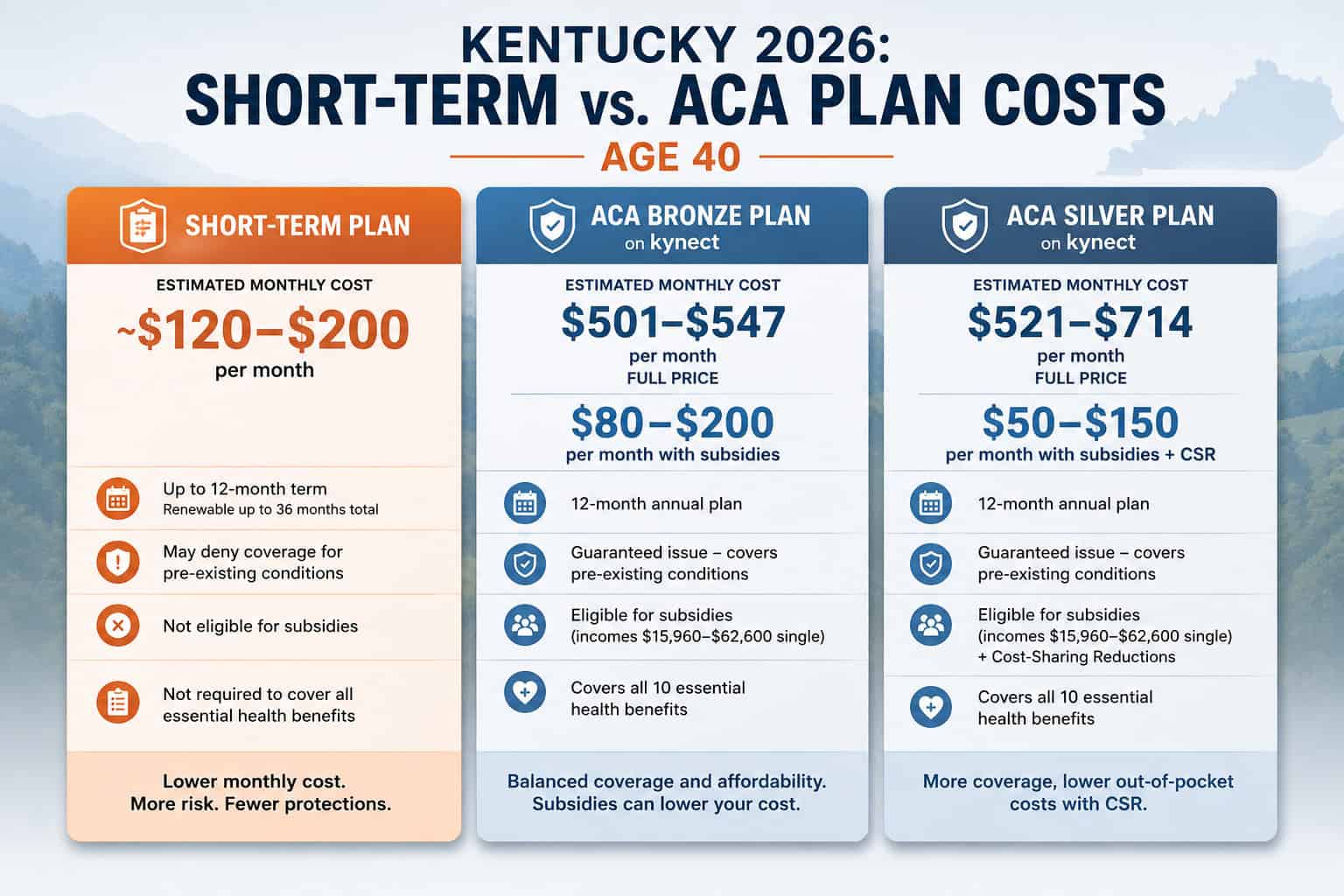

Kentucky has no state-specific limit on short-term health insurance duration and defaults to federal rules. As of August 2025, the Trump administration stopped enforcing the Biden-era 3-month cap, restoring the pre-2024 federal standard: initial terms up to 12 months, renewable for up to 36 months total. At least 6 carriers sell short-term plans in Kentucky in 2026, with premiums running $120–$200/month for a 40-year-old.

The federal rules governing short-term plans in Kentucky shifted twice in recent years. The Biden administration limited initial terms to 3 months and total duration to 4 months (effective September 1, 2024). The Trump administration reversed course on August 7, 2025, announcing it would not enforce the 4-month cap. As of 2026, plans with initial terms up to 12 months and renewals up to 36 months are once again available in Kentucky. Kentuckians can now use short-term coverage as extended gap coverage, not just a bridge of a few weeks.

The Kentucky Department of Insurance has recommended that carriers clearly disclose renewability terms to consumers, noting that even under the old rules, many short-term plans were not guaranteed renewable. Short-term health insurance in Kentucky requires a health questionnaire — unlike ACA plans on kynect, which cannot deny coverage or charge more based on health status.

Short-Term vs. ACA Plans — What Kentucky Coverage Actually Costs

Short-term health insurance in Kentucky typically costs 40–60% less than unsubsidized ACA marketplace premiums — a short-term plan for a healthy 40-year-old may run $120–$200/month compared to $501–$714/month for a kynect Bronze or Silver plan. However, after subsidies, ACA plans on kynect can cost as little as $50–$150/month for qualifying Kentuckians. The cost advantage of short-term plans disappears for anyone who qualifies for premium tax credits.

| Feature | Short-Term Plan | ACA Plan (kynect) |

|---|---|---|

| Monthly premium (age 40) | ~$120–$200 | $501–$714 (full price); $50–$200 (with subsidies) |

| Maximum duration | Up to 12 months; renewable up to 36 months total | 12-month annual plan |

| Pre-existing conditions | May be excluded or denied | Covered — guaranteed issue |

| Essential health benefits | Not required — may exclude maternity, mental health, Rx | All 10 EHBs covered |

| Subsidy eligible | No | Yes — incomes $15,960–$62,600 (single) |

| Health questionnaire | Required — can be denied | None — guaranteed issue |

| Enrollment window | Year-round | Nov 1 – Jan 15 (or qualifying life event) |

| Counts as minimum essential coverage | No | Yes |

Short-term plans are NOT ACA-compliant: Short-term health insurance in Kentucky does not qualify as minimum essential coverage, is not available through kynect, cannot receive premium tax credits, and may exclude pre-existing conditions including diabetes, heart disease, and cancer. These plans are designed for temporary gaps only — not as a substitute for comprehensive coverage.

What Short-Term Plans Don’t Cover in Kentucky

Short-term health insurance in Kentucky is not required to cover the ACA’s 10 essential health benefits. Most short-term plans in Kentucky exclude maternity and newborn care, mental health and substance use treatment, prescription drugs (or offer very limited formularies), preventive care and wellness visits, and pre-existing conditions. Coverage is focused on unexpected illness and injury — emergency room visits, urgent care, hospitalization, and surgery.

Pre-existing condition exclusions are the most significant limitation. Short-term insurers in Kentucky use post-claims underwriting — meaning they review medical records after a claim is filed to determine whether the condition existed before enrollment. A Kentuckian with controlled diabetes who enrolls in a short-term plan and then needs diabetes-related care could have the entire claim denied retroactively. The ACA essential health benefits standard requires marketplace plans on kynect to cover all pre-existing conditions without exclusions.

Application denials are also common. Short-term insurers typically disqualify applicants with certain conditions — including HIV/AIDS, cancer history, heart disease, emphysema, and in some cases obesity above certain thresholds. Unlike kynect marketplace plans, which are guaranteed issue regardless of health status, short-term health insurance in Kentucky is medically underwritten and can reject applicants based on their health questionnaire responses.

When Short-Term Coverage Makes Sense in Kentucky

Short-term health insurance in Kentucky is most appropriate for healthy individuals facing a brief coverage gap — typically 1–3 months — who don’t qualify for kynect subsidies and have no pre-existing conditions. The most common scenarios are waiting for employer coverage to start (many Kentucky employers have 30–90 day waiting periods), bridging months between job loss and the next open enrollment, and recent college graduates aging off a parent’s plan before the November enrollment window.

Waiting for employer coverage

A new employee in Lexington with a 90-day waiting period for group health benefits needs 3 months of bridge coverage. A short-term plan at ~$150/month covers unexpected illness and injury during the gap — total cost ~$450 compared to ~$1,500+ for 3 months of unsubsidized kynect coverage.

Between jobs, short gap expected

A healthy 28-year-old in Louisville who left a job in March and expects to start a new position in May. Two months of short-term coverage at ~$100/month bridges the gap affordably. If income qualifies for subsidies, a kynect SEP plan may be cheaper — check both.

Aging off parent’s plan

A 26-year-old aging off a parent’s plan triggers a kynect Special Enrollment Period. But if the timing falls outside OEP and the individual doesn’t want to commit to a full marketplace plan, 3 months of short-term coverage bridges to the next open enrollment.

NOT recommended for

Anyone with pre-existing conditions (claims will be denied). Anyone who qualifies for kynect subsidies (ACA plans cost less after credits). Anyone needing coverage beyond 4 months. Anyone who needs maternity, mental health, or prescription drug coverage.

Compare Short-Term and ACA Plans in Kentucky

See short-term options alongside subsidized kynect plans for your county. A licensed enrollment assistant can help determine which option fits your gap situation.

Alternatives to Short-Term Coverage in Kentucky

Before purchasing short-term health insurance in Kentucky, Kentuckians should evaluate three ACA-compliant alternatives: a kynect Special Enrollment Period plan (triggered by job loss, marriage, move, or other qualifying events), Kentucky Medicaid (year-round enrollment for incomes under $22,025/year single adult), and COBRA continuation coverage from a former employer (~$702/month average in Kentucky). Each provides comprehensive coverage that short-term plans cannot match.

| Option | Approx. Monthly Cost (Age 40) | Duration | Pre-Existing Covered? | Best For |

|---|---|---|---|---|

| Short-term plan | ~$120–$200 | 3 months (4 max) | No | Healthy individuals, brief defined gaps |

| kynect SEP plan (subsidized) | ~$50–$200 after credits | 12-month annual | Yes | Anyone with a qualifying life event + income under $62,600 |

| kynect plan (full price) | ~$501–$714 | 12-month annual | Yes | Income above subsidy threshold, needs full ACA coverage |

| Kentucky Medicaid | $0 | Year-round | Yes | Income under $22,025/year (single adult) |

| COBRA | ~$702 | 18 months | Yes (same employer plan) | Ongoing treatment with specific in-network provider |

The most common mistake is purchasing short-term health insurance in Kentucky without first checking whether a qualifying life event triggers a kynect Special Enrollment Period. Job loss, moving, marriage, having a child, and losing Medicaid eligibility all open a 60-day SEP window. A subsidized kynect Silver plan at $150/month provides 12 months of comprehensive, guaranteed-issue coverage — far better value than 3 months of limited short-term coverage at $150/month that excludes pre-existing conditions and essential health benefits.

Kentucky Medicaid is available year-round to adults earning under $22,025/year (single) at no monthly cost. Approximately 1.5 million Kentuckians are currently enrolled. For individuals between jobs whose income has dropped below the Medicaid threshold, applying through kynect.ky.gov takes 20–30 minutes and provides immediate, comprehensive coverage. The affordable health insurance Kentucky guide covers Medicaid eligibility and other low-cost options in detail.

Frequently Asked Questions About Kentucky Short-Term Coverage

How long can a short-term plan last in Kentucky?

As of 2026, short-term health insurance in Kentucky can last up to 12 months initially, with renewals up to 36 months total. Kentucky has no separate state duration rule and defaults to federal guidelines. The Biden administration limited plans to 3 months/4 months (effective September 2024), but the Trump administration stopped enforcing that cap in August 2025, restoring the longer durations. At least 6 carriers sell short-term plans in Kentucky with varied term options.

Does short-term insurance cover pre-existing conditions in Kentucky?

No. Short-term health insurance in Kentucky may exclude pre-existing conditions and uses post-claims underwriting — meaning the insurer can review medical records after a claim is filed and deny coverage for conditions that existed before enrollment. This is the most significant difference from ACA-compliant plans on kynect, which cover all pre-existing conditions without exclusions.

Is short-term coverage cheaper than kynect plans?

Before subsidies, yes — short-term plans cost roughly $120–$200/month compared to $501–$714/month for kynect Bronze or Silver plans (age 40). After subsidies, ACA plans on kynect often cost $50–$200/month for qualifying Kentuckians, making them cheaper than short-term plans with far more comprehensive coverage. The cost advantage of short-term plans applies mainly to Kentuckians above the subsidy threshold ($62,600 single adult) who face full-price kynect premiums.

Can I buy short-term health insurance anytime in Kentucky?

Yes — short-term plans are available year-round with no open enrollment restriction. Coverage can begin as early as the next day after approval. However, approval requires a health questionnaire and applicants can be denied based on health history. ACA marketplace plans on kynect are guaranteed issue (no health questions) but require open enrollment or a qualifying life event for enrollment.

Should I get short-term insurance or a kynect SEP plan?

If a qualifying life event (job loss, move, marriage, etc.) triggers a kynect Special Enrollment Period, a subsidized marketplace plan is almost always the better choice — it provides 12 months of guaranteed-issue, ACA-compliant coverage at a subsidized price. Short-term health insurance in Kentucky makes sense only when no SEP is available, the gap is 3 months or shorter, and the individual is healthy with no pre-existing conditions.

Does Kentucky ban short-term health insurance?

No. Unlike California and Colorado, which ban short-term plans entirely, Kentucky allows short-term health insurance and has no separate state duration limit. The state defaults to federal guidelines, which currently allow plans up to 12 months with renewals up to 36 months total following the Trump administration’s August 2025 non-enforcement of the Biden-era 4-month cap.

Kentucky Health Insurance Resources

2026 pillar guide — kynect, Kentucky Medicaid, KCHIP, HB 2 reforms, and the ~89,000 Kentucky enrollees

Kentucky Health Insurance Marketplacekynect enrollment, subsidy eligibility, county carrier availability, and 2026 open enrollment dates

Best Health Insurance in KentuckyCompare all 3 carriers — Anthem, Ambetter by WellCare, Passport by Molina — with Kentucky county coverage

Affordable Health Insurance KentuckyKentucky Medicaid, KCHIP, premium tables, and how HB 2 affects 478,900 expansion adults

Individual Health Insurance KentuckyCoverage for self-employed Kentuckians, Bluegrass farm operators, and residents above the $62,600 subsidy cutoff

PPO Health Insurance PlansCompare PPO options nationwide — flexible provider access, no referrals required, in and out of network

Need Gap Coverage in Kentucky?

Compare short-term plans and ACA alternatives for your specific gap situation. A licensed enrollment assistant can help determine the most cost-effective option for your Kentucky county.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Kentucky residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.