Small Business Health Insurance in Kentucky: 2026 Group Plans & Options

Kentucky small businesses have several options for offering health benefits in 2026 — from traditional group plans through Anthem and WellCare to the SHOP marketplace on kynect and newer alternatives like ICHRAs that let employees choose their own individual plans. This guide covers what’s available to Kentucky employers, how to qualify for tax credits, and the key decisions facing businesses with 1–50 employees.

What does your business need?

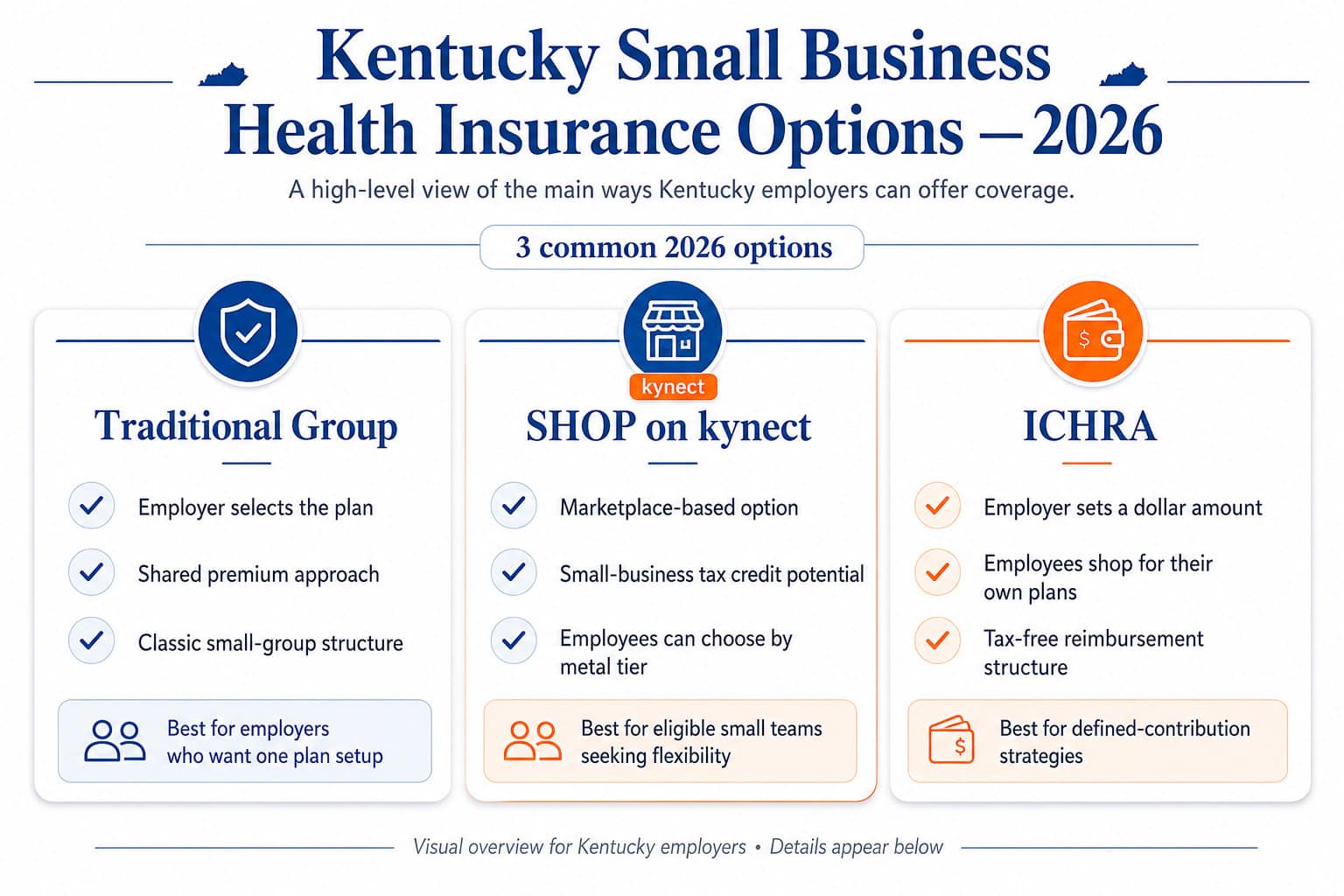

Small Business Health Insurance Options in Kentucky

Kentucky small businesses with 1–50 employees can offer coverage through three primary channels: traditional small group plans purchased directly from carriers like Anthem and WellCare, the SHOP (Small Business Health Options Program) marketplace on kynect, or an Individual Coverage Health Reimbursement Arrangement (ICHRA) that reimburses employees for individual plan premiums. Each approach has different cost structures, administrative requirements, and flexibility for the 2026 plan year.

| Option | Eligible Businesses | Carriers in KY | Tax Credit Eligible | Employee Choice |

|---|---|---|---|---|

| Traditional small group | 1–50 FTE | Anthem, WellCare (varies by county) | No (unless through SHOP) | Employer selects plan; employees enroll |

| SHOP on kynect | 1–50 FTE | Same carriers, via kynect | Yes — under 25 FTE + avg wages under ~$65,000 | Employees may choose from available metal tiers |

| ICHRA | Any size | Any — employees choose their own | No (but contributions are tax-free) | Full employee choice — kynect or off-exchange |

| QSEHRA | Under 50 FTE, no group plan | Any — employees choose their own | No (but contributions are tax-free) | Full employee choice; max $6,350/individual in 2026 |

For many Kentucky small businesses — particularly those in rural counties where carrier choice is limited to Anthem — the ICHRA model is gaining traction. Instead of the employer selecting a single group plan, the business sets a monthly dollar amount (e.g., $400/employee) and employees use that allowance to purchase their own individual plan through kynect or off-exchange. This gives employees in Fayette County access to three carriers while an employee in Harlan County uses the same allowance for an Anthem plan — the employer’s cost is fixed regardless of geography.

Small Business Health Care Tax Credit in Kentucky

Kentucky small businesses that purchase coverage through the SHOP marketplace on kynect may qualify for the Small Business Health Care Tax Credit — worth up to 50% of the employer’s premium contributions (35% for tax-exempt organizations). To qualify, the business must have fewer than 25 full-time equivalent employees, pay average annual wages under approximately $65,000 (inflation-adjusted annually), and cover at least 50% of employee-only premium costs. For a qualifying 10-employee Kentucky business, this credit can save $3,000–$8,000/year.

The credit is claimed on the employer’s annual federal tax return using IRS Form 8941. The maximum credit applies to businesses with 10 or fewer FTEs and average wages under $30,000. The credit phases out as employee count approaches 25 and average wages approach $65,000. Tax-exempt Kentucky organizations — including nonprofits and religious organizations — can claim up to 35% as a refundable credit.

Example: Bowling Green Auto Repair Shop

A Bowling Green auto repair shop with 8 full-time employees averaging $34,000/year in wages purchases SHOP coverage through kynect, contributing $450/month per employee toward Anthem Silver premiums. Annual employer contribution: $43,200. The Small Business Health Care Tax Credit at approximately 40% (phased based on wages) returns roughly $17,280 — reducing the effective employer cost to $25,920, or about $270/month per employee.

SHOP enrollment on kynect: Kentucky small businesses enroll in SHOP through kynect.ky.gov — not through HealthCare.gov, which handles federally-facilitated states only. A licensed enrollment assistant at ForHealthInsurance.com can handle the entire SHOP application and tax credit calculation at no cost. Call 888-215-4045. The tax credit is only available for plans purchased through SHOP — not for direct-purchase group plans from Anthem or WellCare.

Does Kentucky Require Employers to Offer Health Insurance?

Kentucky has no state employer mandate requiring small business health insurance in Kentucky or any other coverage. The federal shared responsibility provision (ACA employer mandate) applies only to Applicable Large Employers with 50 or more full-time equivalent employees — businesses with fewer than 50 FTEs face no federal penalty for not offering coverage. Approximately 89% of Kentucky businesses have fewer than 20 employees, making the vast majority exempt from any employer mandate.

For Kentucky businesses at or near the 50-FTE threshold, the federal penalty for not offering affordable, minimum-value coverage is $3,340 per full-time employee (minus the first 30) in 2026. A 55-FTE Kentucky business that does not offer coverage would face a potential penalty of approximately $83,500/year (25 employees × $3,340). Businesses approaching this threshold should evaluate whether offering small business health insurance in Kentucky through a group plan or ICHRA is more cost-effective than absorbing the penalty.

Kentucky Small Group Carriers for 2026

Small business health insurance in Kentucky is available from Anthem Blue Cross Blue Shield and WellCare for traditional small group plans. Anthem offers the broadest small group network in Kentucky — including Pathway and Transition tiers — with coverage available in all 120 counties. The Kentucky small group market saw rate increases averaging approximately 14% for 2026, lower than the individual market’s 15%–37% increases, reflecting the more stable risk pool in employer-sponsored coverage.

Small group plans in Kentucky are community-rated — meaning premiums are based on employee ages, tobacco use, and county, not on the group’s health history. A 10-person group in Jefferson County (Louisville) with an average employee age of 38 can expect small group Silver premiums of approximately $550–$650/month per employee before employer contributions. Anthem’s small group Transition network includes Baptist Health, Norton Healthcare, and UK HealthCare — the same broader-network access available in the individual market.

For businesses exploring the ICHRA alternative, employees purchase their own individual plans through kynect or off-exchange, and the employer reimburses a set dollar amount tax-free. This shifts the carrier selection to the employee — a Louisville employee might choose WellCare for lower premiums while a Pikeville employee enrolls in Anthem Pathway as the only available option. The Best Health Insurance in Kentucky guide covers individual carrier options employees would choose from under an ICHRA arrangement.

Compare Kentucky Small Business Health Plans

Compare 2026 group plans from Anthem BCBS and Ambetter by WellCare of Kentucky, check SHOP tax credit eligibility (up to $25,000/year for businesses under 25 FTE), and explore ICHRA alternatives — all for Kentucky employers with 1–50 employees.

ICHRA — An Alternative to Traditional Group Plans in Kentucky

An Individual Coverage Health Reimbursement Arrangement (ICHRA) allows Kentucky employers to set a fixed monthly dollar amount per employee — say $400 or $500 — which employees use to purchase their own individual health insurance through kynect or off-exchange from Anthem. Employer contributions are tax-deductible for the business and tax-free to the employee. Employees who purchase kynect plans with ICHRA funds may also qualify for premium tax credits if their income and the employer contribution meet affordability thresholds.

ICHRA is one of the fastest-growing small business health insurance options in Kentucky. ICHRAs are particularly well-suited to small businesses in Kentucky because of the state’s geographic carrier variation. A traditional group plan locks all employees into one carrier and network — problematic when a Louisville employee has three carrier options but a Harlan County employee has only Anthem. With an ICHRA, each employee selects the plan that works best in their county, and the employer’s per-employee cost stays fixed regardless of location or carrier selection.

ICHRA works well when

Employees are spread across multiple Kentucky counties with different carrier availability. The business wants predictable, fixed monthly costs. Employees have diverse healthcare needs and prefer choosing their own plan type and metal tier.

Traditional group works well when

All employees are in the same county with the same carrier options. The business qualifies for the SHOP tax credit (under 25 FTE, wages under ~$65,000). Employees prefer having the employer handle plan selection and administration.

How to Set Up Small Business Health Insurance in Kentucky

Setting up small business health insurance in Kentucky requires four decisions: coverage type (group plan, SHOP, or ICHRA), carrier selection (Anthem and/or WellCare for group plans), contribution level (minimum 50% of employee-only premiums for SHOP tax credit eligibility), and enrollment timing (group plans can start any month, not restricted to open enrollment). A licensed enrollment assistant can walk through all options and run quotes at no cost to the business.

Count full-time equivalent employees (30+ hours/week). Kentucky businesses under 25 FTE with average wages under ~$65,000 should evaluate SHOP for the tax credit. Businesses with 1–5 employees may find ICHRA or QSEHRA more cost-effective than traditional group rates.

Traditional group plan (employer selects carrier and plan), SHOP through kynect (employees may choose metal tier, tax credit available), or ICHRA (employer sets dollar amount, employees buy their own plans). Each has different administrative and cost implications.

For group plans: Anthem and WellCare serve the Kentucky small group market. Provide employee census data (ages, zip codes, tobacco status) for accurate quotes. For ICHRA: determine the monthly allowance amount and let employees quote their own individual plans through kynect or off-exchange.

Group plans can start the first of any month — no open enrollment restriction. SHOP enrollment goes through kynect.ky.gov — or call ForHealthInsurance.com at 888-215-4045 for guided enrollment. Provide employees with plan details, contribution amounts, and network information. Coverage activates once the first premium payment clears.

Frequently Asked Questions About Kentucky Small Business Coverage

Is health insurance required for small businesses in Kentucky?

No. Kentucky has no state employer mandate. The federal ACA employer mandate applies only to businesses with 50 or more full-time equivalent employees. Kentucky businesses with fewer than 50 FTEs can offer small business health insurance voluntarily without penalty for not providing it. Approximately 89% of Kentucky businesses fall below the 50-FTE threshold.

What is the Small Business Health Care Tax Credit?

The tax credit is worth up to 50% of the employer’s premium contributions (35% for tax-exempt organizations) for small businesses that purchase coverage through the SHOP marketplace. To qualify, the business must have fewer than 25 full-time equivalent employees, pay average annual wages under approximately $65,000 (inflation-adjusted annually), and cover at least 50% of employee-only premiums. Claimed on the federal tax return using IRS Form 8941.

What carriers offer small group plans in Kentucky?

Anthem Blue Cross Blue Shield and WellCare are the primary small group carriers in Kentucky for 2026. Anthem offers coverage in all 120 counties with Pathway and Transition network tiers. Small group rate increases for 2026 averaged approximately 14% — lower than the individual market’s 15%–37% increases. Group plans are community-rated based on employee ages, tobacco use, and county.

What is an ICHRA and how does it work in Kentucky?

An Individual Coverage Health Reimbursement Arrangement lets employers set a fixed monthly dollar amount per employee for health insurance. Employees use that allowance to buy their own individual plan through kynect or off-exchange. Employer contributions are tax-deductible and tax-free to employees. ICHRAs are well-suited to Kentucky businesses with employees across multiple counties where carrier availability varies significantly.

Can my employees keep their kynect subsidies with an ICHRA?

It depends on the ICHRA contribution amount and the employee’s income. If the employer’s ICHRA contribution is considered “affordable” under ACA standards (covering at least a threshold percentage of the lowest-cost Silver plan), the employee may not qualify for premium tax credits on kynect. If the contribution is below the affordability threshold, the employee can decline the ICHRA and receive kynect subsidies instead. A licensed enrollment assistant can run the affordability calculation.

How much does small business health insurance cost in Kentucky?

Small group Silver premiums in Kentucky for 2026 run approximately $550–$650/month per employee for a group with an average age of 38 in Jefferson County (Louisville). Costs vary by employee ages, county, carrier, and metal tier. Businesses qualifying for the SHOP tax credit can reduce effective costs by up to 50% of their premium contributions. ICHRA costs are fixed at whatever monthly amount the employer sets — there is no minimum requirement.

Kentucky Health Insurance Resources

2026 pillar guide — kynect, Kentucky Medicaid, KCHIP, HB 2 reforms, and the ~89,000 Kentucky enrollees

Kentucky Health Insurance Marketplacekynect enrollment, subsidy eligibility, county carrier availability, and 2026 open enrollment dates

Best Health Insurance in KentuckyCompare all 3 carriers — Anthem, Ambetter by WellCare, Passport by Molina — with Kentucky county coverage

Affordable Health Insurance KentuckyKentucky Medicaid, KCHIP, premium tables, and how HB 2 affects 478,900 expansion adults

Individual Health Insurance KentuckyCoverage for self-employed Kentuckians, Bluegrass farm operators, and residents above the $62,600 subsidy cutoff

PPO Health Insurance PlansCompare PPO options nationwide — flexible provider access, no referrals required, in and out of network

Find Small Business Health Insurance for Your Kentucky Team

Compare kynect SHOP group plans, ICHRA options, and off-exchange Anthem coverage for your Kentucky business. Licensed enrollment assistance at no cost — serving all 120 Kentucky counties.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Kentucky businesses. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.