Massachusetts Health Insurance: 2026 Plans, Costs & Enrollment Guide

Massachusetts offers some of the most generous paths to affordable coverage in the country for residents who qualify for state and federal help. ConnectorCare — a state-subsidized program available only through the Health Connector — provides $0 or low-premium plans with no deductibles, and the state added $250 million for 2026 to buffer the impact of expiring federal subsidies. This guide covers every pathway, from ConnectorCare and MassHealth to the state’s 2:1 age rating that keeps premiums lower for older enrollees.

What’s your income level?

ConnectorCare: Massachusetts’ Unique Affordable Coverage

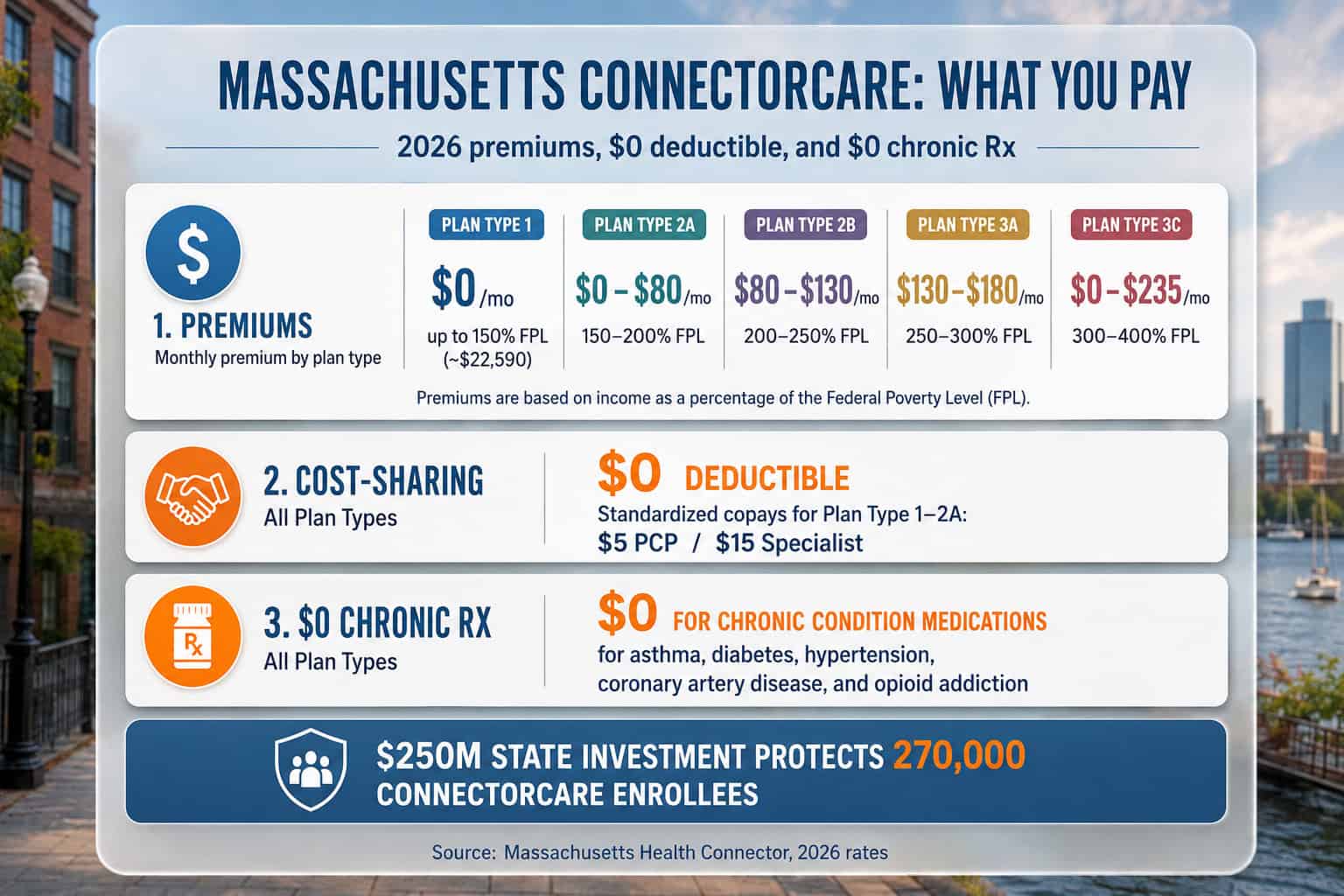

ConnectorCare is the most affordable health insurance in Massachusetts for residents earning between 100% and 400% FPL (up to ~$62,600 for an individual). These plans combine federal APTC with state subsidies to produce $0 or low premiums, $0 deductibles, standardized low copays, and $0 prescriptions for five chronic conditions. Approximately 270,000 Massachusetts residents are enrolled in ConnectorCare for 2026 — protected from federal subsidy cuts by a $250 million state investment.

What makes ConnectorCare different from subsidies in other states: in most states, federal APTC reduces the monthly premium but the enrollee still faces a deductible of $2,000–$9,100 on Silver plans. In Massachusetts, ConnectorCare eliminates the deductible entirely and standardizes copays across all participating carriers. A ConnectorCare Plan Type 2A enrollee pays $5 for primary care and $15 for specialists whether they choose BCBSMA, Harvard Pilgrim, WellSense, or any other carrier — the only difference is the provider network.

The $0 chronic-condition prescription benefit is particularly valuable. ConnectorCare covers medications for asthma, diabetes, hypertension, coronary artery disease, and opioid addiction at zero cost. A Massachusetts resident managing diabetes who takes insulin and metformin pays $0 for both through ConnectorCare — a benefit that can save $200–$500/month versus standard Silver plans with prescription copays. Per the Massachusetts Health Connector, ConnectorCare eligibility requires income between 100%–400% FPL, no access to affordable employer coverage, and agreement to file a federal tax return.

Plan Type 1

$0/moUp to 150% FPL (~$22,590). $0 premium, $0 deductible, lowest copays. The cheapest comprehensive coverage available in Massachusetts.

Plan Type 2A–2B

~$40–$130/mo150%–250% FPL. Low fixed premium with $0 deductible and $5–$10 primary-care copays. $0 chronic-condition prescriptions included.

Plan Type 3A

~$130–$180/mo250%–300% FPL. Still no deductible and standardized copays — substantially cheaper than an unsubsidized Silver plan in the same county.

Plan Type 3C

up to $235/mo300%–400% FPL (~$45,180–$62,600). The top ConnectorCare tier, continued for 2026 through the state’s $250M investment after Plan Type 3D ended.

MassHealth: Free Coverage Below 138% FPL

MassHealth (Massachusetts Medicaid) provides free or very low-cost coverage to residents earning up to 138% FPL (~$21,384 for an individual, ~$44,004 for a family of four). MassHealth enrollment is year-round — there is no open enrollment restriction. Residents who earn too much for MassHealth but qualify for ConnectorCare are transitioned seamlessly through the single Health Connector application, which determines eligibility for both programs.

MassHealth covers a comprehensive set of services including doctor visits, hospital care, prescription drugs, mental health, dental for adults and children, and vision. For residents hovering near the 138% FPL threshold, a small income change can shift eligibility between MassHealth (free) and ConnectorCare Plan Type 1 ($0 premium but with copays). Reporting income changes promptly ensures the correct coverage level without gaps. The MassHealth website handles applications for residents clearly below 138% FPL.

Health Safety Net (HSN): Massachusetts residents who do not qualify for MassHealth or Health Connector coverage — including some undocumented immigrants — may access the Health Safety Net. HSN pays for medically necessary services at participating hospitals and community health centers. It is funded by hospitals, insurers, and the state, and is currently running a significant shortfall, with an estimated $290 million deficit in the hospital fiscal year ending September 2025.

Check Your Affordable Coverage Options

See whether you qualify for ConnectorCare, MassHealth, or federal subsidies — and find out what affordable coverage in Massachusetts would cost for your household in 2026.

Affordable Options Above 400% FPL in Massachusetts

Massachusetts residents earning above 400% FPL (~$62,600 for an individual) no longer qualify for ConnectorCare or enhanced federal APTC in 2026 if enhanced credits have expired. However, two structural advantages still keep coverage more affordable than in most states: the 2:1 age-rating ratio (versus the 3:1 federal standard) and the 88% medical loss ratio requirement (versus the 80% federal minimum). Both directly reduce premiums for all Massachusetts enrollees regardless of income.

2:1 Age Rating

25–35% lowerMassachusetts caps age-based premium variation at 2:1, so the oldest enrollees pay at most double the youngest. A 64-year-old pays roughly $800–$900/month for Silver here, versus $1,100–$1,400 in a 3:1 state — saving residents 50+ an estimated 25%–35%.

88% Medical Loss Ratio

vs 80% federalCarriers must spend at least 88 cents of every premium dollar on member care — the strictest standard in the nation. Less revenue goes to administration and profit, and carriers below 88% must rebate members.

Bronze Plans

~$280–$350/moA WellSense Bronze plan — among the lowest-cost options on the Health Connector — runs about $280–$350/month for a 40-year-old, versus $450–$550 for Silver.

Catastrophic Plans

under 30Available to residents under 30 or with a hardship exemption. The lowest monthly premium of any tier, with coverage for three primary-care visits before the deductible applies.

For high earners who do not qualify for any subsidies, the lowest-cost route is a higher-deductible Bronze or catastrophic plan. The best health insurance in Massachusetts guide provides carrier-specific pricing by age and county, and residents who want broader provider access can compare PPO health insurance plans for nationwide coverage.

2026 Subsidy Changes Affecting Massachusetts

Massachusetts faces two major subsidy changes for 2026: the expiration of federal enhanced premium tax credits, which reduces subsidy amounts across income levels and removes APTC above 400% FPL, and federal eligibility changes that removed roughly 36,000 noncitizen members from ConnectorCare. Massachusetts responded with a $250 million state investment that protects approximately 270,000 ConnectorCare enrollees earning below 400% FPL — keeping affordable coverage intact despite the federal cuts.

| Population Affected | What Changed | Massachusetts Response |

|---|---|---|

| ~270,000 ConnectorCare enrollees (below 400% FPL) | Federal enhanced APTC expired — reduced subsidy amounts | $250M state investment; little to no premium increase for this group |

| ~19,000 Plan Type 3D members (400%–500% FPL) | Lost ConnectorCare eligibility; no longer qualify for APTC above 400% FPL | Must purchase unsubsidized plans; Plan Type 3C (up to 400% FPL) continues |

| ~36,000 noncitizen Plan Type 1 members | Lost APTC eligibility due to federal law changes | Health Safety Net for emergency care; state exploring additional options |

| Enrollees above 400% FPL | “Subsidy cliff” returns — no APTC above 400% FPL | 2:1 age ratio and 88% MLR still apply; catastrophic plans available |

Governor Healey described Massachusetts’ response as the strongest state plan in the country to protect against federal ACA cost increases. The $250 million funds additional state subsidies layered into ConnectorCare for 2026, ensuring roughly 270,000 enrollees below 400% FPL see little to no premium increase. Per healthinsurance.org, only about ten states offer any state-funded health insurance subsidies, and Massachusetts’ program is the most comprehensive. The Massachusetts marketplace guide covers how to enroll and check eligibility.

Affordable Health Insurance FAQ for Massachusetts

ConnectorCare can lower premiums to $0 for eligible residents, MassHealth covers those below 138% FPL for free, and a $250 million state investment protects roughly 270,000 enrollees from federal subsidy cuts. The questions below cover the cheapest options, the 2:1 age-ratio advantage, free coverage pathways, and what changed for 2026.

What is the cheapest health insurance in Massachusetts for 2026?

ConnectorCare Plan Type 1 is the cheapest option at $0/month premium with $0 deductible — available to Massachusetts residents earning up to 150% FPL (~$22,590/individual). For residents who do not qualify for ConnectorCare, WellSense Health Plan typically offers the lowest-premium plans on the Health Connector. Catastrophic plans are available to those under 30 or with a hardship exemption at approximately $200–$280/month.

How does the 2:1 age ratio help older Massachusetts residents?

Massachusetts limits age-based premium variation to 2:1 — the oldest enrollees pay at most double what the youngest pay for the same plan. Most other states use the federal 3:1 ratio. A 60-year-old in Massachusetts pays approximately 25%–35% less than the same person in a 3:1 state. This structural advantage applies to all Massachusetts health insurance plans regardless of subsidy eligibility or carrier selection.

What did Massachusetts do about expiring federal subsidies?

Massachusetts allocated an additional $250 million for 2026 to make ConnectorCare more robust, protecting approximately 270,000 enrollees with incomes below 400% FPL from significant premium increases caused by the expiration of federal enhanced premium tax credits. Governor Healey described this as the strongest state response in the country. ConnectorCare Plan Type 3C (300%–400% FPL) continues through 2026.

Can I get free health insurance in Massachusetts?

Yes, through two pathways. MassHealth (Medicaid) provides free coverage to residents earning up to 138% FPL (~$21,384/individual) with year-round enrollment. ConnectorCare Plan Type 1 provides $0/month premium plans to residents earning 100%–150% FPL through the Health Connector. Both programs cover comprehensive health services including doctor visits, prescriptions, mental health, and hospital care.

Is affordable health insurance in Massachusetts still available above 400% FPL?

ConnectorCare is not available above 400% FPL for 2026, and federal APTC may not be available above 400% FPL if enhanced credits have expired. However, Massachusetts’ 2:1 age ratio and 88% medical loss ratio keep unsubsidized premiums lower than in most states. Bronze and catastrophic plans offer the lowest monthly costs for residents who must pay full price. The Health Connector’s “Get an Estimate” tool shows unsubsidized pricing for your age and county.

More Massachusetts Health Insurance Guides

Massachusetts’ eight-carrier Health Connector, ConnectorCare subsidies, and 2:1 age rating make informed comparison shopping worthwhile. These guides cover the full marketplace, enrollment deadlines, carrier rankings, individual and small group plans, and PPO options for broader provider access.

Plans, carriers, costs, and enrollment in the Commonwealth.

Health Connector MarketplaceHow to enroll, deadlines, and qualifying life events.

Best Plans & CarriersBCBSMA, Harvard Pilgrim, Tufts, and more — ranked and compared.

Individual & Private PlansOff-exchange and self-employed coverage options.

Small Business CoverageGroup plans for employers with 1–50 employees.

PPO PlansOut-of-network flexibility and broader provider access nationwide.

Find Affordable Coverage in Massachusetts

With ConnectorCare plans starting at $0/month and a 2:1 age rating that keeps premiums lower for older enrollees, most Massachusetts residents pay far less than the sticker price. Check ConnectorCare and MassHealth eligibility and compare 2026 pricing in minutes.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Massachusetts residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.