Individual Health Insurance in Massachusetts: 2026 Private & Marketplace Plans

Massachusetts residents buying individual health insurance have two clear pathways: the Health Connector marketplace at MAhealthconnector.org, where subsidies and ConnectorCare are available, or directly from one of eight licensed carriers off-exchange, at full price with identical plan designs. Because Massachusetts operates a merged market, on-exchange and off-exchange individual plans carry the same rates — the only difference is subsidy access. This guide covers both pathways, self-employed coverage strategies, and how the state’s individual mandate affects plan selection.

What’s your situation?

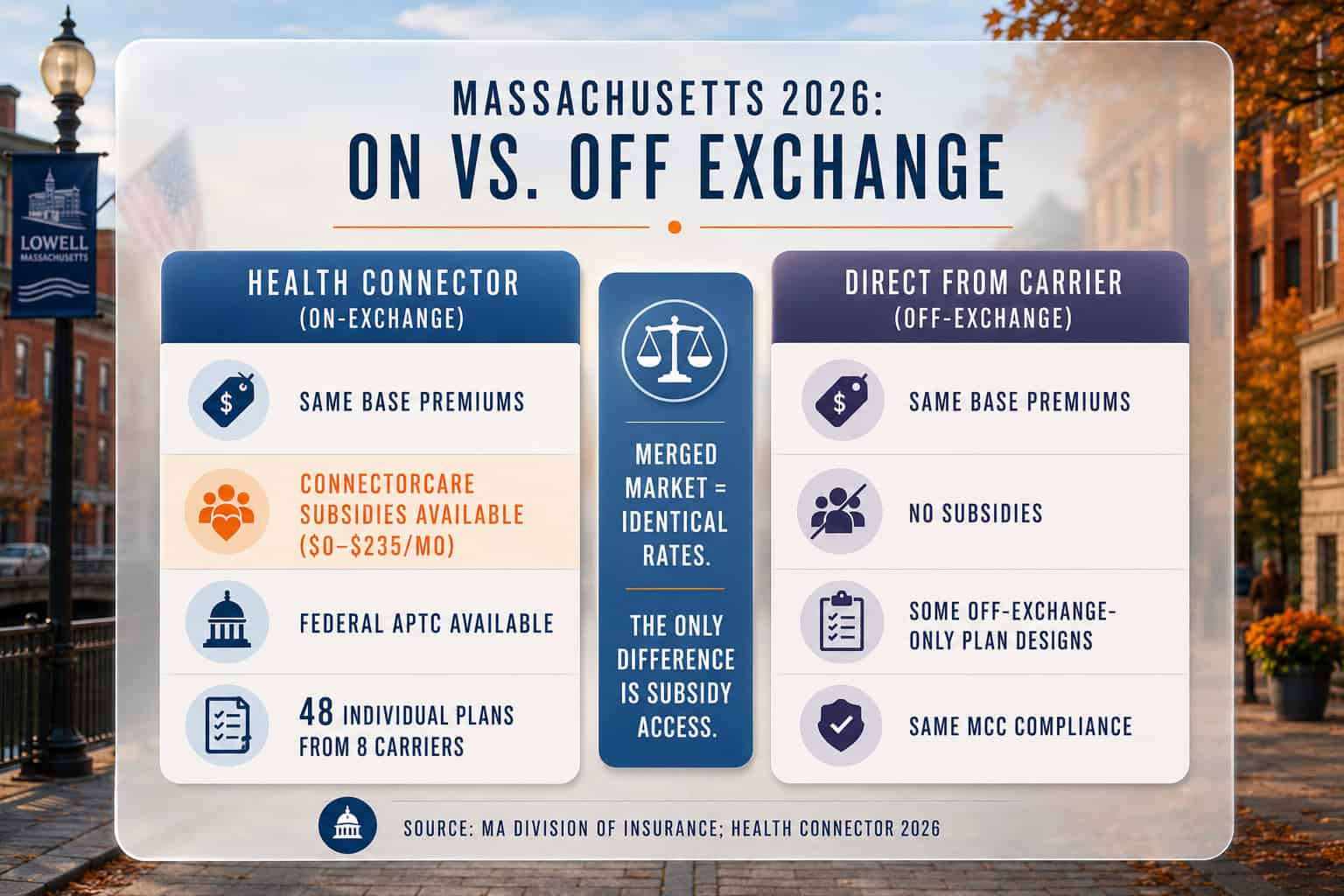

On-Exchange vs. Off-Exchange Individual Plans in Massachusetts

Individual health insurance in Massachusetts is available both on-exchange (through the Health Connector) and off-exchange (directly from carriers). Unlike most states, Massachusetts operates a merged individual and small-group market — meaning on-exchange and off-exchange plans carry identical rates from the same carriers. The only reason to choose on-exchange is subsidy access: ConnectorCare and federal APTC are available only through the Health Connector.

| Feature | On-Exchange (Health Connector) | Off-Exchange (Direct from Carrier) |

|---|---|---|

| Premiums | Same base rates as off-exchange | Same base rates as on-exchange |

| Subsidies available | Yes — ConnectorCare + federal APTC | No subsidies available |

| Carriers | 8 carriers (BCBSMA, Harvard Pilgrim, Tufts, etc.) | Same 8 + additional off-exchange-only options |

| Plan types | HMO, PPO, EPO (Bronze through Platinum + Catastrophic) | Same plan types at same rates |

| MCC compliance | All plans meet MCC standards | Most carrier plans meet MCC — verify before purchasing |

| Best for | Anyone who qualifies for ConnectorCare or APTC | High earners who prefer a direct carrier relationship |

The merged market is a unique feature that simplifies the individual health insurance decision considerably. In most other states, off-exchange plans can have different rates and designs than on-exchange plans. In Massachusetts, a BCBSMA Silver HMO purchased through the Health Connector costs exactly the same as the same plan purchased directly from BCBSMA — the plan design, network, and premium are identical. The only variable is whether you receive ConnectorCare or APTC subsidies, which require Health Connector enrollment. For any resident who qualifies for financial help, on-exchange is always the correct choice.

Off-exchange individual coverage makes sense only for residents earning above subsidy eligibility who prefer to work directly with a carrier or broker. Some carriers — including BCBSMA and Cigna — offer additional off-exchange-only plan configurations not available on the Health Connector. The Massachusetts Division of Insurance publishes a complete list of all individual and small-group plans available for 2026, both on and off-exchange.

Individual Health Insurance for Self-Employed Massachusetts Residents

Self-employed Massachusetts residents — freelancers, 1099 contractors, gig workers, and sole proprietors — are among the largest buyers of individual health insurance in the state. They purchase through the Health Connector and qualify for the same ConnectorCare and APTC subsidies as any other enrollee. They can also deduct 100% of health insurance premiums from Massachusetts adjusted gross income on Schedule Y of the state return, and HSA contributions of up to $4,400/individual are deductible for 2026.

The self-employed health insurance deduction applies on both the federal return (Form 1040, above the line) and the Massachusetts state return (Schedule Y). For a self-employed resident paying $3,600/year in net premiums after ConnectorCare subsidies, the combined deduction saves roughly $800–$1,200 in federal and state taxes. Massachusetts’ 2:1 age rating also benefits self-employed residents over 50 — a 58-year-old freelancer pays about 25%–35% less for the same plan than a 58-year-old in a federal 3:1 ratio state.

HSA eligibility for 2026: New for 2026, all Health Connector Bronze and Catastrophic plans qualify as high-deductible health plans (HDHPs) for HSA eligibility. Self-employed residents choosing a Bronze plan can open an HSA and contribute up to $4,400/individual or $8,750/family pre-tax. HSA contributions are deductible on both federal and Massachusetts state returns, per IRS Publication 502.

Compare Individual Health Insurance Plans in Massachusetts

See on-exchange and off-exchange options, check ConnectorCare eligibility, and compare carriers for your county.

The MCC Mandate and Individual Plan Selection

Massachusetts requires all individual health insurance plans to meet Minimum Creditable Coverage (MCC) standards — or the enrollee faces a state tax penalty via Schedule HC. MCC requires coverage for a comprehensive set of services including doctor visits, hospitalization, emergency care, mental health, substance abuse, and prescription drugs, plus preventive care without cost-sharing and an annual out-of-pocket maximum. Most plans sold by Massachusetts-licensed carriers meet MCC.

The MCC requirement is stricter than the federal ACA essential-health-benefit standard in some areas — particularly around deductible limits and prescription drug coverage. Per the Health Connector’s mandate guidance, MCC-compliant plans for 2026 must keep deductibles within state-set limits and cover preventive care without cost-sharing. All eight Health Connector carriers meet MCC on every marketplace plan. Off-exchange plans from Massachusetts-licensed carriers also typically meet MCC, but buyers should verify — the carrier must include an MCC-compliance notice on every plan sold in Massachusetts. Form MA 1099-HC, sent by January 31 each year, confirms whether your coverage met MCC.

Plans that do not meet MCC include short-term health insurance, health sharing ministries, fixed indemnity plans, and some out-of-state employer plans. Residents enrolled in non-MCC coverage face the state penalty of up to $135/month ($1,620/year) — even if they hold some form of coverage. The Massachusetts health insurance guide covers the penalty calculation, exemptions, and appeal process. Short-term plans aren’t even sold in Massachusetts — state law bars them — so they are not a usable option for avoiding the penalty.

Who Buys Individual Health Insurance in Massachusetts?

Approximately 391,744 Massachusetts residents enrolled in individual Health Connector plans for 2026 — a 0.7% increase from 389,191 in 2025, per CMS enrollment data. About 75% of 2026 enrollees receive subsidies (down from 87% in 2025 due to federal eligibility changes). Massachusetts has a nation-leading insured rate above 98% — the highest in the country — and individual coverage through the Health Connector is a central reason why.

Self-employed & freelancers

1099 / freelanceNo employer coverage available. Eligible for ConnectorCare and APTC based on net self-employment income, and able to deduct premiums on both federal and Massachusetts returns. The state’s technology, biotech, higher-education, and creative sectors drive significant freelance work in Middlesex, Suffolk, and Norfolk counties.

Between jobs or transitioning

Job transitionJob loss triggers a 60-day special enrollment period on the Health Connector. Individual coverage is typically cheaper than COBRA for residents who qualify for ConnectorCare. COBRA preserves the existing employer plan at full cost — often $600–$900/month for individual coverage in the high-cost merged market.

Early retirees (under 65)

Pre-MedicareBridge coverage between employer retirement and Medicare at 65. The 2:1 age ratio provides significant savings for pre-retirees — a 62-year-old pays at most double what a 21-year-old pays, versus 3x in most states. ConnectorCare eligibility extends to 400% FPL (~$62,600/individual), covering many early retirees.

Domestic partners

PartnershipsMassachusetts recognizes domestic partnerships for health insurance purposes, so partners can enroll together on individual family plans through the Health Connector. The Mass.gov health reform page covers dependent eligibility rules, including domestic-partnership coverage.

Individual premiums in Massachusetts reflect the state’s 2:1 age rating — Silver HMO plans for a 21-year-old start at about $394/month (WellSense) to $518/month (UnitedHealthcare EPO), while the same plans for a 40-year-old range from about $490 to $961/month before subsidies. The merged market’s average 2026 rate increase of 11.5% applies to both individual and small-group plans, per the Massachusetts Division of Insurance. The best health insurance in Massachusetts guide provides carrier-specific pricing by age and county.

Individual Health Insurance FAQ for Massachusetts

Massachusetts’ merged market means on- and off-exchange plans share the same rates, self-employed residents can deduct premiums on both returns, and the MCC mandate applies no matter where you buy. The questions below cover the on-vs-off decision, self-employed deductions, what MCC requires, COBRA comparisons, and how the mandate treats off-exchange plans.

Is off-exchange health insurance cheaper than the Health Connector in Massachusetts?

No. Massachusetts operates a merged market — on-exchange and off-exchange plans from the same carrier have identical rates. The only difference is that ConnectorCare subsidies and federal APTC are only available through the Health Connector. For anyone who qualifies for financial help, on-exchange is always cheaper. Off-exchange makes sense only for high earners who prefer a direct carrier relationship or want access to off-exchange-only plan designs.

Can self-employed people deduct health insurance premiums in Massachusetts?

Yes. Self-employed Massachusetts residents can deduct 100% of health insurance premiums (net of ConnectorCare subsidies and APTC) on both the federal return (Form 1040, above the line) and the Massachusetts state return (Schedule Y). HSA contributions are also deductible on both returns. For 2026, all Health Connector Bronze and Catastrophic plans qualify as HDHPs for HSA eligibility — contribution limits are $4,400/individual and $8,750/family.

What is Minimum Creditable Coverage (MCC)?

MCC is Massachusetts’ standard for qualifying health insurance — stricter than the federal ACA essential health benefit requirement. MCC requires coverage for doctor visits, hospitalization, emergency care, mental health, substance abuse, prescription drugs, and preventive care without cost-sharing, plus an annual out-of-pocket maximum within state-set limits. Plans that do not meet MCC — including short-term and health sharing ministries — trigger the state tax penalty even if they provide some coverage.

Is COBRA or Health Connector coverage cheaper in Massachusetts?

For most Massachusetts residents who qualify for ConnectorCare or APTC, Health Connector plans are significantly cheaper than COBRA. COBRA requires paying the full employer + employee premium share — often $600–$900/month for individual coverage in Massachusetts. A ConnectorCare plan for someone earning $30,000/year might cost $50–$80/month with $0 deductible. COBRA makes sense only when the employer plan has unique provider access or when income exceeds subsidy eligibility.

Does the individual mandate apply to off-exchange plans?

Yes. The Massachusetts individual mandate requires MCC-compliant coverage regardless of where you purchase it. Both on-exchange Health Connector plans and off-exchange plans from Massachusetts-licensed carriers typically meet MCC. The mandate applies to all adults 18 and older who are Massachusetts residents. Verify MCC compliance on any plan — carriers are required to include an MCC-compliance notice, and Form MA 1099-HC confirms MCC status at tax time.

More Massachusetts Health Insurance Guides

Individual coverage is one path through the Massachusetts system. These guides cover the full state overview, the Health Connector marketplace, carrier rankings, affordable and ConnectorCare options, small group plans, and PPO coverage for broader provider access.

Plans, carriers, costs, and the individual mandate.

Health Connector MarketplaceHow to enroll, deadlines, and qualifying life events.

Best Plans & CarriersBCBSMA, Harvard Pilgrim, Tufts, and more — ranked and compared.

Affordable CoverageConnectorCare, subsidies, and ways to lower premiums.

Small Business CoverageGroup plans for employers with 1–50 employees.

PPO PlansOut-of-network flexibility and broader provider access nationwide.

Find Individual Health Insurance in Massachusetts

Compare Health Connector and off-exchange plans from eight carriers, check ConnectorCare eligibility, and see 2026 pricing for your county.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Massachusetts residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.