Small Business Health Insurance in Massachusetts: 2026 Group Plans & Options

Massachusetts gives small employers something most states don’t: the individual and small-group markets are merged into one risk pool, so a business taps the same eight carriers and the same rate filings that individual residents see — with an 88% medical loss ratio and a 2:1 age band built in. The Health Connector serves businesses with 1–50 employees through a dedicated small-group portal offering 56 plans for 2026. This guide walks through group plan options, the SHOP tax credit, ICHRA alternatives, and what the merged market means for a Massachusetts business owner weighing coverage.

What does your business need?

Small Business Health Insurance Options in Massachusetts

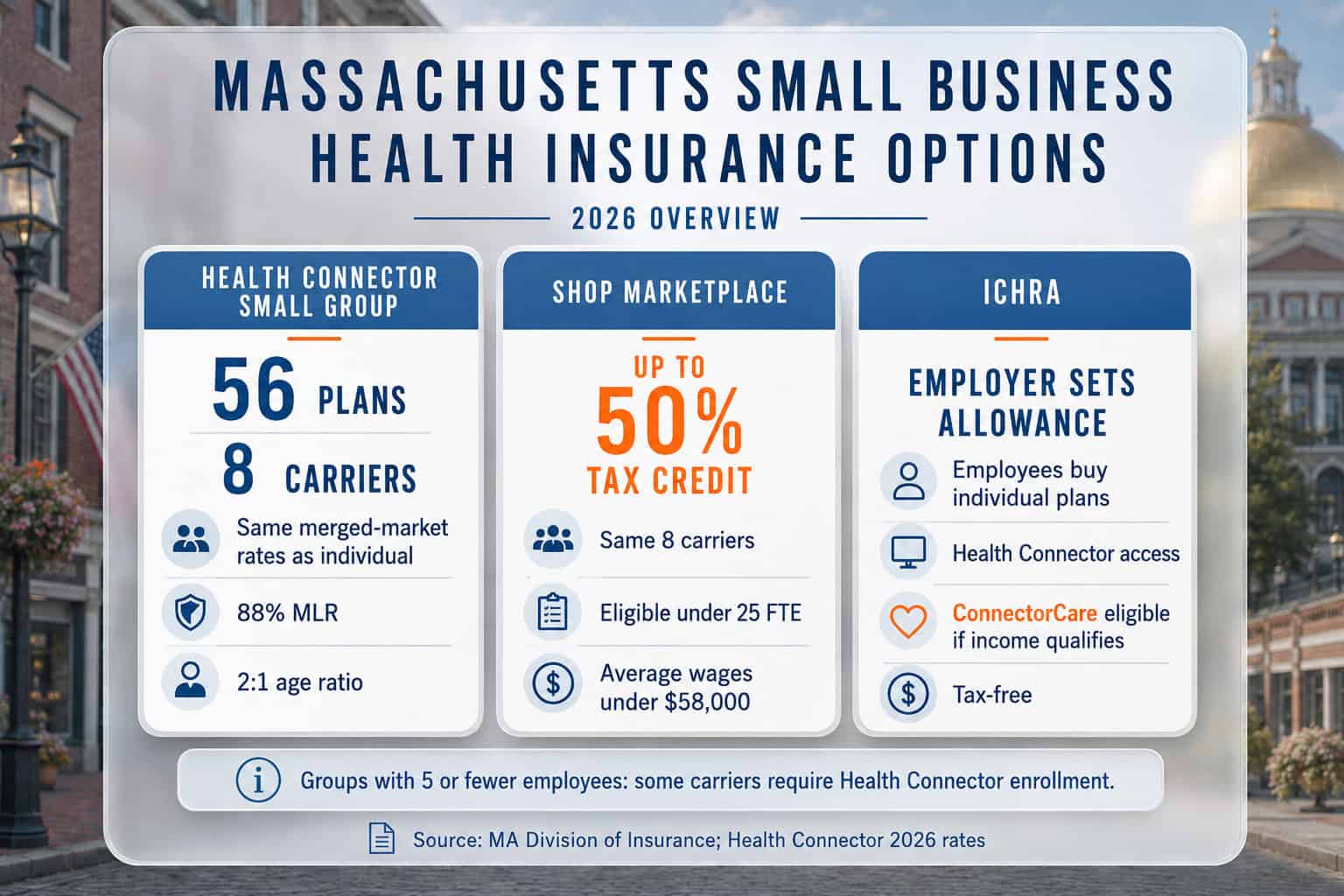

The Health Connector’s small-group portal anchors three coverage channels for Massachusetts employers in 2026: 56 small-group plans from eight carriers, the SHOP marketplace for the federal tax credit, and an ICHRA that routes employees to Health Connector individual plans. Because Massachusetts merges its individual and small-group risk pools, the small-group rate increase tracks the individual market’s 11.5% 2026 average, per the Massachusetts Division of Insurance.

| Option | Eligible Businesses | Carriers | Tax Credit Eligible | Key Feature |

|---|---|---|---|---|

| Health Connector small group | 1–50 employees | 8 carriers (same as individual market) | No (unless through SHOP) | Merged market — same rates as individual plans |

| SHOP marketplace | 1–50 employees | Same 8 carriers | Yes — under 25 FTE + avg wages under $58,000 | Only path to the Small Business Health Care Tax Credit |

| ICHRA | Any size | Any — employees choose their own | No (but contributions are tax-free) | Employees may qualify for ConnectorCare if income eligible |

| QSEHRA | Under 50, no group plan | Any — employees choose their own | No (but contributions are tax-free) | Max $6,350/individual in 2026; simpler than ICHRA |

The merged pool produces a quirk Massachusetts employers can exploit: a BCBSMA Silver HMO carries one price, whether a solo resident buys it on the Health Connector or a Northampton shop owner buys it for a four-person group. That single-price reality, layered on top of the state’s 88% medical loss ratio floor and 2:1 age band, is what makes shopping genuinely simpler for a Massachusetts employer — group coverage can be compared by simply reading the individual-market rate sheet, with no separate small-group quote to decode. Per the Division of Insurance plan listing, 56 small-group plans are approved for 2026 — the menu every Massachusetts small-business shopper chooses from.

Small groups with 5 or fewer employees: Several Massachusetts carriers — including WellSense, Tufts Health Public Plans, Fallon Health, and Health New England — require groups with five or fewer eligible employees to enroll through the Health Connector or designated intermediaries such as Health Services Administrators (HSA) at (781) 848-4950 or Small Business Service Bureau at (508) 756-3513. This is a Massachusetts-specific enrollment requirement, not a coverage limitation.

Small Business Health Care Tax Credit in Massachusetts

In Massachusetts the SHOP credit runs through one channel — the Health Connector’s small-group portal — and it is the only route to the federal Small Business Health Care Tax Credit, worth up to 50% of employer premium contributions (35% for tax-exempt employers). A Massachusetts firm qualifies with fewer than 25 full-time equivalents, average wages under $58,000, and at least half of employee-only premiums covered. The credit is claimed on IRS Form 8941.

The Merged Market Advantage for Massachusetts Employers

Massachusetts folds its individual and small-group buyers into one merged risk pool — a structure shared by only a handful of states — so a small employer and a solo individual see identical base rates from the same eight carriers. The payoffs for a Massachusetts group are concrete: an 88% medical loss ratio where federal small-group rules require only 80%, and a 2:1 age rating band where most states permit 3:1.

One rate decision covers both markets at once. When the Division of Insurance set the 11.5% average increase for 2026, that figure landed on individual and small-group plans together — there is no second small-group risk pool moving on its own schedule. For a Massachusetts employer, the upshot is plain comparison shopping: the group price is the same price an individual sees on the Health Connector for the identical plan. As of December 2024, roughly 711,563 people sat inside that combined merged pool, individual and small-group members counted together.

ConnectorCare changes the ICHRA math in Massachusetts in a way it can’t elsewhere. When a Springfield employer sets a $350/month ICHRA allowance, an employee earning inside 100–400% FPL can stack that allowance against a ConnectorCare plan and land on the program’s signature benefits — $0 deductibles and reduced copays that exist only inside the Massachusetts state-subsidy wrap, not in standard marketplace Silver plans. The employer funds a fixed, tax-free dollar amount; the state subsidy does the rest. No other state pairs an employer reimbursement arrangement with a benefit structure quite like ConnectorCare’s, which is why this combination shows up so often in Massachusetts small-business planning. The best health insurance in Massachusetts guide profiles each carrier’s network by region, and employees who want out-of-network flexibility can compare PPO health insurance plans.

Compare Massachusetts Small Business Health Plans

See group plan options from eight merged-market carriers, check SHOP tax credit eligibility, and explore ICHRA alternatives for your Massachusetts business.

How to Set Up Small Business Health Insurance in Massachusetts

Setting up small-business health insurance through the Massachusetts Health Connector involves choosing a coverage approach (group plan, SHOP, or ICHRA), selecting from eight merged-market carriers, determining contribution levels, and enrolling employees. The process runs fastest for groups that confirm carrier-specific enrollment rules first — those with five or fewer employees may be required to enroll through the Health Connector or designated intermediaries depending on the carrier selected.

Determine your employee count and budget

Count full-time equivalent employees. Massachusetts businesses under 25 FTE with average wages under $58,000 should evaluate SHOP for the tax credit. The Health Connector’s small-group portal serves businesses with 1–50 employees. For groups of 5 or fewer, check carrier-specific enrollment requirements — several carriers require Health Connector enrollment.

Choose a coverage approach

A traditional group plan (employer selects carrier and metal tier from 56 small-group plans), SHOP through the Health Connector (tax credit available), or an ICHRA (employer sets a dollar amount, employees buy their own plans — potentially qualifying for ConnectorCare). Each carries different administrative and cost implications.

Get quotes from Massachusetts merged-market carriers

Provide employee census data (ages, zip codes, tobacco status) for accurate quotes. Because of the merged market, small-group rates match individual rates from the same carrier — no separate small-group pricing surprises. Contact the Health Connector at 1-877-MA-ENROLL or a licensed broker for side-by-side carrier comparisons.

Enroll and communicate to employees

Group plans can start the first of any month. Provide employees with plan details, contribution amounts, and network information. Massachusetts requires employers to report coverage on Form MA 1099-HC for employees who are Massachusetts residents — confirming Minimum Creditable Coverage for the state individual mandate.

Massachusetts Small Business Health Insurance FAQ

Massachusetts’ merged market keeps small-group and individual rates identical, the SHOP credit runs through the Health Connector, and ICHRA can pair with ConnectorCare in a way no other state matches. The questions below cover merged-market pricing, plan counts, ICHRA-plus-ConnectorCare, the five-or-fewer enrollment rule, and how the individual mandate touches employers.

Are small group rates different from individual rates in Massachusetts?

No. Massachusetts operates a merged individual and small group market — the same carriers file the same base rates for both markets. A BCBSMA Silver plan costs the same for a small group as for an individual buyer. This merged market structure also means both markets share the same 88% medical loss ratio and 2:1 age rating ratio, providing consistent pricing protections across both segments.

How many small group plans are available in Massachusetts for 2026?

The Health Connector Board approved 56 small group plans from eight carriers for 2026, covering Bronze through Platinum tiers. The same eight carriers that serve the individual market — BCBSMA, Harvard Pilgrim, Tufts, WellSense, Mass General Brigham Health Plan, UnitedHealthcare, Fallon Health, and Health New England — also offer small group coverage. Coverage areas vary by carrier and county.

Can employees get ConnectorCare if the employer offers an ICHRA?

Potentially, yes. If a Massachusetts employer offers an ICHRA, employees use the allowance to purchase individual plans through the Health Connector. Employees whose household income falls between 100% and 400% FPL may qualify for ConnectorCare — receiving $0 or low-premium plans with no deductibles and $0 chronic condition prescriptions on top of the employer’s ICHRA contribution. Affordability calculations determine whether the employee can decline the ICHRA and receive full ConnectorCare benefits.

Why do some carriers require Health Connector enrollment for small groups?

Massachusetts law allows certain carriers to require groups with five or fewer eligible employees to enroll through the Health Connector or designated intermediaries. WellSense, Tufts Health Public Plans, Fallon Health, and Health New England all have this requirement for their smallest groups. This is an enrollment channel requirement, not a coverage limitation — the same plans and rates are available. Contact Health Services Administrators at (781) 848-4950 or Small Business Service Bureau at (508) 756-3513 for enrollment assistance.

Does the Massachusetts individual mandate affect employer coverage?

Employers are not mandated to provide MCC-compliant coverage under Massachusetts law — the mandate applies to individual residents. However, employers must report coverage on Form MA 1099-HC for employees who are Massachusetts residents, confirming whether the employer plan meets Minimum Creditable Coverage standards. Most employer-sponsored plans from Massachusetts-licensed carriers meet MCC. Self-insured employers should verify MCC compliance with their plan administrator.

More Massachusetts Health Insurance Guides

Group coverage is one part of the Massachusetts picture. These guides cover the full state overview, the Health Connector marketplace, carrier rankings, individual and affordable options, and PPO coverage for employees who want broader provider access.

Plans, carriers, costs, and the individual mandate.

Health Connector MarketplaceHow to enroll, deadlines, and qualifying life events.

Best Plans & CarriersBCBSMA, Harvard Pilgrim, Tufts, and more — ranked and compared.

Individual & Private PlansOff-exchange and self-employed coverage options.

Affordable CoverageConnectorCare, subsidies, and ways to lower premiums.

PPO PlansOut-of-network flexibility and broader provider access nationwide.

Find Small Business Health Insurance for Your Massachusetts Team

Compare merged-market plans from eight carriers, check SHOP tax credit eligibility, and explore ICHRA options — with licensed enrollment assistance at no cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Massachusetts businesses. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.