Affordable Health Insurance in Mississippi 2026: Low-Cost Plans & the Coverage Gap

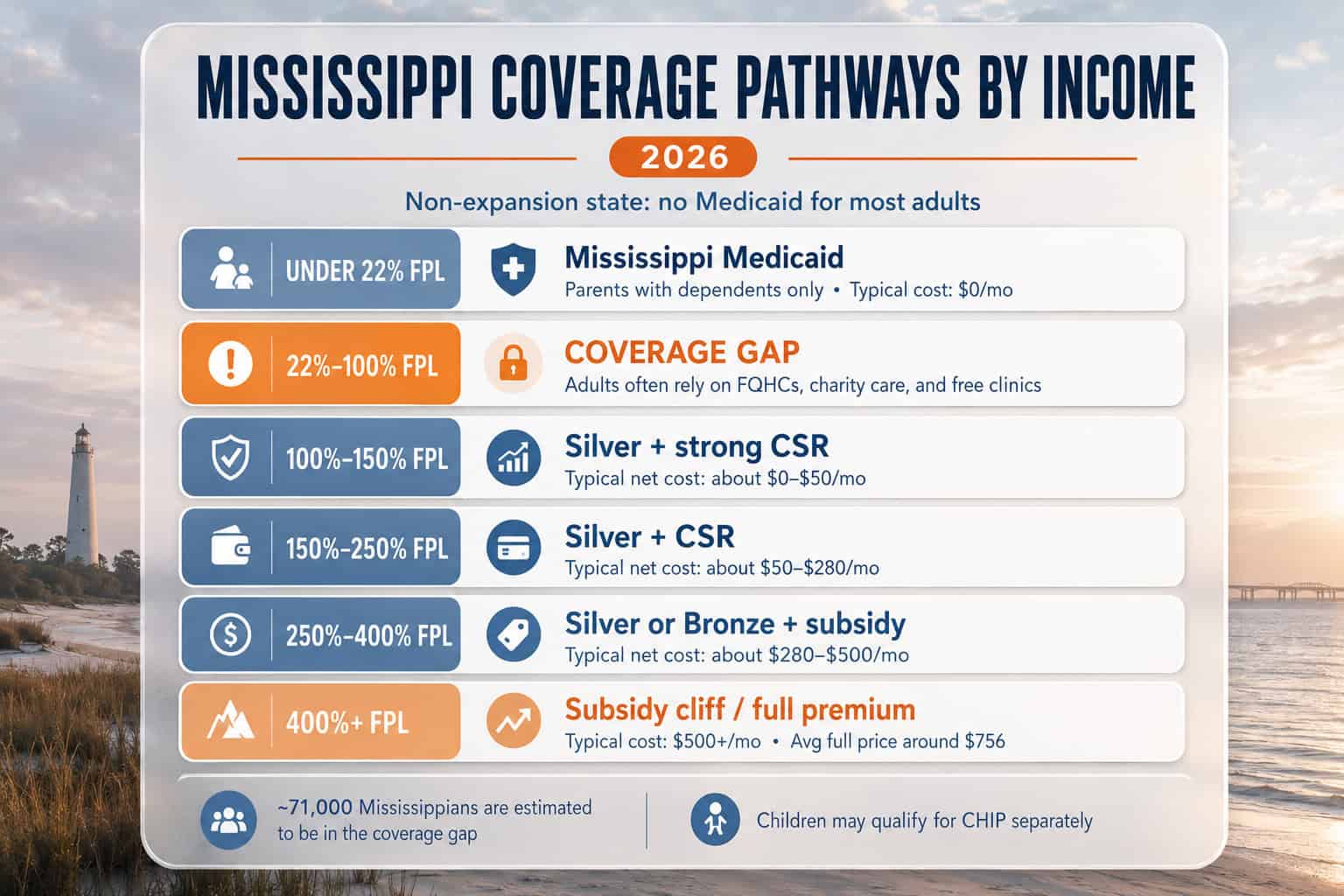

Affordable health insurance in Mississippi for 2026 is a harder problem than in most states — the weighted statewide rate increase is 43.4%, Mississippi has not expanded Medicaid, and roughly 71,000 adults sit in the coverage gap with no realistic coverage path. Yet for the roughly 90% of marketplace enrollees who qualify for premium tax credits, subsidized coverage on HealthCare.gov keeps individual plans within reach despite the rate shock — the average subsidized Mississippian pays about $85/month versus $756/month at full price. CHIP covers children up to 214% FPL, and pregnant women qualify for Mississippi Medicaid up to 194% FPL with 12-month postpartum coverage. This guide covers every affordability pathway — marketplace subsidies, Mississippi Medicaid, the coverage gap, CHIP, cost-sharing reductions, and where to find cheap health insurance in Mississippi when the rate shock bites.

Where does your household fall?

The Mississippi Coverage Gap: 71,000 Adults With No Path to Coverage

Roughly 71,000 Mississippi adults fall into the coverage gap — earning too little for marketplace premium tax credits (below 100% FPL, or $15,060/year single) but too much for Mississippi Medicaid’s restrictive eligibility (parents only at 22% FPL, about $488/month for a family of three; childless adults ineligible entirely). This gap exists because Mississippi is one of just 10 states that have not expanded Medicaid under the ACA.

For Mississippians in the gap, options are limited but real. More than 20 Federally Qualified Health Centers across the state provide primary care on a sliding-fee scale — from the Delta Health Center in Mound Bayou (one of the nation’s first FQHCs) to Jackson-Hinds Comprehensive Health Center. Hospitals maintain charity-care programs for emergency and ongoing needs, and nonprofit free clinics serve Jackson, Hattiesburg, the Gulf Coast, and other metros. If income can be projected at or above 100% FPL ($1,255/month single) during HealthCare.gov enrollment, marketplace plans with strong subsidies become available — for self-employed or gig workers this projection may be accurate and unlocks affordable health insurance in Mississippi through the Mississippi marketplace.

Mississippi Medicaid expansion status: Multiple expansion bills were introduced in 2024, including HB 1725, which passed the Mississippi House but died when the House and Senate versions couldn’t be reconciled. The Mississippi State Medical Association supports expansion, and Commissioner Mike Chaney has advocated for it — but without the governor’s support, expansion has not moved forward. Roughly 224,000 additional Mississippians would gain coverage if the state accepted expansion, per KFF estimates.

Marketplace Subsidies — How Premium Tax Credits Work in Mississippi

About 90% of Mississippi marketplace enrollees rely on the premium tax credit — the primary source of affordable health insurance in Mississippi. The credit caps a household’s benchmark Silver premium as a share of income: roughly 2% at 150% FPL, about 4% at 250% FPL, and 8.5% at 400% FPL under enhanced subsidies. Without enhanced subsidies, the cliff at 401% FPL eliminates all assistance and the average Silver stays near $756/month unsubsidized.

The most dependable affordable health insurance in Mississippi flows only through HealthCare.gov — private off-exchange plans from BCBS or Celtic don’t qualify. The IRS reconciles credits annually on Form 8962. For variable-income Mississippians — seasonal Gulf Coast tourism workers, Delta agricultural contractors, gig drivers — projecting income accurately matters: overestimating costs money each month, while underestimating triggers tax-time clawback. Cost-sharing reductions apply automatically to Silver plans for enrollees under 250% FPL, cutting deductibles from $5,000+ to as low as $700 — the single biggest lever on affordable health insurance in Mississippi for lower-income enrollees.

Most likely to find low-cost coverage

Lower-income households who can project income at or above 100% FPL, the self-employed with variable income, Gulf Coast seasonal workers, part-time workers without job-based coverage, and families with children eligible for CHIP. Roughly 90% of Mississippi marketplace enrollees qualify for premium tax credits — many pay close to $85 per month.

At risk of paying full price

Adults in the coverage gap below 100% FPL with no projectable income, childless adults ineligible for Mississippi Medicaid, and higher earners above the subsidy thresholds — especially if enhanced credits expire and the 401% FPL cliff returns, pushing the average Silver back toward $756 per month unsubsidized.

| Household Income (% FPL) | Best Coverage Path in Mississippi | Typical Net Cost |

|---|---|---|

| Under 22% FPL (parents w/ dependents) | Mississippi Medicaid | $0/month |

| 22%–100% FPL (adults) | Coverage gap — FQHCs, charity care, free clinics | Sliding scale or free |

| 100%–150% FPL | Silver + strong CSR, premium tax credit | ~$0–$50/month |

| 150%–200% FPL | Silver + CSR | ~$50–$150/month |

| 200%–250% FPL | Silver + limited CSR | ~$150–$280/month |

| 250%–400% FPL | Silver or Bronze + subsidy | ~$280–$500/month |

| 400%+ FPL | Enhanced subsidy (if extended) or full premium | $500+/month ($756 avg full) |

Mississippi Medicaid: Who Actually Qualifies in a Non-Expansion State

Mississippi Medicaid — administered by the Division of Medicaid — covers roughly 590,816 residents as of October 2025 through the MississippiCAN managed-care program. Eligibility is among the strictest in the nation. Parents with dependent children qualify at incomes up to about 22% FPL ($488/month for a family of three). Childless non-disabled adults under 65 do not qualify at any income. Children qualify up to 209% FPL, and pregnant women up to 194% FPL with 12-month postpartum coverage.

For the lowest-income families, Mississippi Medicaid is the most affordable health insurance in Mississippi available. Apply through the Mississippi Division of Medicaid at access.ms.gov, by phone at 1-800-421-2408, by mail, or in person at a regional Medicaid office. Mississippi Medicaid allows year-round enrollment — no Open Enrollment window applies. Income limits update March 1 each year based on the federal poverty guidelines, so applications submitted in January or February may use the prior year’s limits while later ones use the updated thresholds. For how Medicaid fits the full picture, see the Mississippi health insurance overview.

HR 1 / OBBBA changes arriving in late 2026: Federal legislation requires Mississippi Medicaid to implement six-month eligibility redeterminations (instead of annual) starting December 31, 2026, and an 80-hour monthly work or qualifying-activity requirement for adults ages 19–64 starting 2027. The Division of Medicaid must build new verification systems by year-end. Current enrollees should keep employment documentation current and update contact information at access.ms.gov to avoid coverage gaps during redetermination cycles.

Mississippi CHIP: Coverage for Children Up to 214% FPL

Mississippi’s Children’s Health Insurance Program covers children ages 0–18 in households earning up to 214% FPL — about $65,486 for a family of four in 2026. CHIP extends beyond the 209% FPL Medicaid threshold for children, catching households that earn slightly too much for Medicaid. It covers preventive care, immunizations, doctor visits, dental, vision, mental health, prescriptions, and hospitalization, and most eligible families pay no monthly premium and minimal cost-sharing.

CHIP enrollment is year-round through the same Mississippi Medicaid application process, and HealthCare.gov automatically screens marketplace applicants for Medicaid and CHIP eligibility, transferring qualifying children to the Division of Medicaid. Many Mississippi families whose parents buy marketplace plans — or whose parents fall in the coverage gap with no coverage at all — can still enroll children in CHIP at no cost. This matters especially in Mississippi, where a parent earning $14,000/year (in the gap) may have children who qualify for full CHIP coverage. Always check children’s eligibility independently of the parent’s situation, since CHIP is often the most affordable health insurance in Mississippi for children even when the adults are uninsured.

Find the Most Affordable Mississippi Coverage for 2026

Check premium tax credit eligibility, Mississippi Medicaid qualification, CHIP for your children, and marketplace options despite the 43.4% statewide rate increase. Licensed enrollment assistance walks through every Mississippi affordability pathway at no cost — coverage-gap resources included.

Finding the Cheapest Mississippi Plans Despite the Rate Shock

Despite the 43.4% weighted statewide rate increase, cheap health insurance in Mississippi is achievable for subsidy-eligible households. Oscar Health offers the cheapest 2026 Silver near $630/month in 11 counties, Cigna EPO Silver runs about $692/month, and Ambetter HMO Silver about $695/month with a 5-star rating. For enrollees under 250% FPL, Silver with cost-sharing reductions delivers the strongest value — a $5,000 deductible drops to roughly $700 with strong CSRs applied automatically.

Mississippi-specific strategies for affordable health insurance in Mississippi start with income projection. The Mississippi carrier comparison ranks the lowest-premium plans, and the individual plan guide covers self-employed and early-retiree affordability moves. If your income is near the 100% FPL threshold ($15,060 single), make sure projected income reaches at least $1,255/month during HealthCare.gov enrollment to unlock marketplace subsidies. For Gulf Coast seasonal workers with variable income, projecting conservatively above 100% FPL opens access to heavily subsidized Silver plans — often the cheapest route to real coverage. If income drops below 100% FPL during the year, update HealthCare.gov immediately, since a mid-year change may qualify you for a Special Enrollment Period or redirect you to Mississippi Medicaid. Help Health Mississippi navigators at 601-376-9000 can run affordability calculations for free, comparing every route to affordable health insurance in Mississippi side by side.

Affordability Questions From Mississippi Residents

What is the Mississippi coverage gap?

The coverage gap affects roughly 71,000 Mississippi adults who earn too little for marketplace premium tax credits (below 100% FPL) but too much for Mississippi Medicaid (parents at 22% FPL, childless adults ineligible). This gap exists because Mississippi has not expanded Medicaid. Neighboring expansion states like Louisiana and Arkansas have no gap. Options for gap residents include FQHCs, hospital charity care, and free clinics.

Who qualifies for Mississippi Medicaid in 2026?

Parents with dependent children qualify at incomes up to about 22% FPL ($488/month for a family of three). Children qualify up to 209% FPL through Medicaid and 214% FPL through CHIP. Pregnant women qualify up to 194% FPL with 12-month postpartum coverage. Aged, blind, and disabled adults qualify under separate criteria. Childless non-disabled adults under 65 do not qualify regardless of income.

How much does subsidized Mississippi coverage cost?

The average subsidized Mississippi marketplace enrollee pays about $85/month versus $756/month at full price. At 150% FPL, premium tax credits cap the benchmark Silver plan at roughly 2% of income — often $0–$50/month premiums. Cost-sharing reductions for Silver plans under 250% FPL further reduce deductibles and copays. About 90% of Mississippi marketplace enrollees qualify for some premium tax credit.

What happens if enhanced subsidies expire?

The Mississippi Insurance Department projects roughly 200,000 Mississippians could drop marketplace coverage if enhanced subsidies expire. A 60-year-old couple earning $82,000 could see premiums jump from about $685/month to over $2,200/month. CMS expanded catastrophic plan eligibility for 2026 under a hardship exemption for households newly losing subsidy access, and Mississippi’s rural hospitals project significant losses from increased uncompensated care.

Can children get CHIP even if parents have no coverage?

Yes. Mississippi CHIP eligibility is based on household income, not on the parent’s coverage status. A parent in the coverage gap with no insurance may have children who qualify for CHIP at no cost if household income falls under 214% FPL ($65,486 for a family of four). Always check children’s eligibility independently — apply through the Mississippi Division of Medicaid or HealthCare.gov.

What if I earn just below 100% FPL — am I stuck in the gap?

Not necessarily. If you’re self-employed or have variable income, projecting income at or above 100% FPL ($15,060/year single, $1,255/month) during HealthCare.gov enrollment can unlock marketplace subsidies. The IRS reconciles at tax time — if actual income ends up below 100% FPL you may owe back subsidies, but if it lands between 100% and 400% FPL the subsidy holds. A licensed enrollment assistant can help model realistic income projections.

Related Mississippi Health Insurance Resources

Explore related guides for Mississippi’s overall coverage landscape, marketplace enrollment, top-rated carriers, and PPO plan flexibility to help navigate affordable health insurance decisions in the Magnolia State.

Plans, costs, carriers, and how coverage works statewide.

Marketplace EnrollmentHealthCare.gov enrollment, deadlines, subsidies, and qualifying life events.

Best Plans & CarriersAmbetter, Blue Cross Blue Shield of Mississippi, Cigna, and Oscar compared.

PPO PlansReferral-free specialist access and out-of-network coverage nationwide.

Explore Every Mississippi Affordability Pathway

From the coverage gap to premium tax credits to CHIP, a licensed enrollment assistant can map the cheapest legitimate coverage for your household and county — and confirm whether you qualify for Mississippi Medicaid. Free, with no cost to you.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Mississippi residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.