Individual Health Insurance in Mississippi 2026: Private Plans, PPO & Subsidies

Individual health insurance in Mississippi serves residents who don’t get coverage through an employer — self-employed professionals, early retirees under 65, gig workers, part-time employees, and anyone between jobs. Five carriers sell individual plans on HealthCare.gov for 2026, with Oscar Health newly entering 11 counties, while Blue Cross Blue Shield of Mississippi sells private off-exchange plans as the state’s only PPO. Because Mississippi has not expanded Medicaid, the individual market carries a heavier load than in expansion states — about 313,392 Mississippians enrolled in marketplace plans for 2026, many of whom would be on Medicaid elsewhere. This page covers who buys individual and private health insurance in Mississippi, how on-exchange enrollment compares to off-exchange, self-employed tax strategies, early-retiree planning, and metal-tier selection.

What’s your individual coverage situation?

Who Needs Individual Coverage in a Non-Expansion State

Individual health insurance in Mississippi serves a broader population than in Medicaid-expansion states because Mississippi has not expanded Medicaid. Self-employed workers, freelancers, early retirees, gig workers, part-time employees, and people between jobs all buy individual plans. Mississippi’s marketplace also absorbs low-income adults above 100% FPL who would be on Medicaid in expansion states, while roughly 71,000 more residents sit in the coverage gap with no realistic coverage path at all.

Mississippi’s non-expansion creates a direct pipeline from poverty to the individual market. An adult earning $15,060/year (100% FPL for one) qualifies for marketplace subsidies in Mississippi — making individual coverage effectively free for many. But an adult earning $14,000/year (93% FPL) falls into the coverage gap: too high for Mississippi Medicaid’s 22% FPL parent threshold, too low for marketplace subsidies. This gap doesn’t exist in expansion states like neighboring Louisiana or Arkansas, which is why individual health insurance in Mississippi reaches deeper into low-income households than in most states. For Mississippians right at the 100% FPL line, projecting income carefully during HealthCare.gov enrollment can mean the difference between subsidized individual coverage and no coverage at all.

The individual market in Mississippi is dominated by HMO plans. Ambetter from Magnolia Health (142,324 enrollees), Cigna EPO (53,064 enrollees), Molina HMO, UnitedHealthcare HMO, and new entrant Oscar Health HMO serve the marketplace. BCBS of Mississippi offers the state’s only PPO but markets it primarily off-exchange as private health insurance, and Celtic also sells off-exchange only. All individual plans bought through HealthCare.gov or directly from carriers are ACA-compliant — pre-existing conditions are covered, all 10 essential health benefits are included, and no benefit caps apply.

HealthCare.gov vs Private Off-Exchange: When BCBS Mississippi PPO Wins

Individual health insurance in Mississippi comes from two channels: HealthCare.gov (on-exchange, subsidy-eligible) or private off-exchange plans bought directly from carriers (no subsidies). For roughly 90% of Mississippi enrollees who qualify for premium tax credits, HealthCare.gov wins on cost. Private off-exchange BCBS Mississippi PPO wins for unsubsidized households above 400% FPL who value PPO flexibility — the only true out-of-network benefit in the Mississippi individual market.

| Feature | HealthCare.gov (On-Exchange) | Private Off-Exchange (Direct) |

|---|---|---|

| Premium tax credits | Yes — ~90% of MS enrollees qualify | No |

| Cost-sharing reductions | Yes (Silver plans, under 250% FPL) | No |

| PPO availability | BCBS MS on-exchange (limited PPO) | BCBS MS off-exchange PPO — broadest network |

| Carrier options | 5 carriers (+ Oscar in 11 counties) | BCBS MS + Celtic |

| ACA protections | Yes | Yes (ACA-compliant plans) |

| Best for | Subsidy-eligible Mississippians (under 400% FPL) | Higher-income, PPO-seeking, travelers, snowbirds |

The PPO trade-off is uniquely sharp in Mississippi because no on-exchange carrier offers a robust PPO. For a Jackson-area attorney earning $95,000/year (well above the subsidy cliff), private off-exchange BCBS MS PPO may cost roughly $850/month but delivers statewide network access plus out-of-network benefits at major academic medical centers in Memphis, New Orleans, and Birmingham. The same individual choosing Ambetter HMO on HealthCare.gov without a subsidy pays about $695/month but is locked into in-network care within Mississippi. That $155/month difference buys significant flexibility for complex or specialist-heavy needs — the central reason some Mississippians choose private health insurance over a subsidized HMO. For a full carrier-by-carrier breakdown of networks, ratings, and 2026 pricing, see the Mississippi best plans and carriers comparison.

Self-Employed Mississippians and the Individual Market

Self-employed Mississippians are the single largest individual market segment. Without employer coverage, 1099 contractors, freelancers, small business owners, artists, and independent professionals buy plans through HealthCare.gov or private off-exchange. The self-employed health insurance deduction allows deducting 100% of premiums as an adjustment to gross income — reducing taxable income before the standard deduction, not as an itemized expense — one of the biggest reasons individual health insurance in Mississippi is more affordable for the self-employed than the sticker price suggests.

Premium tax credits and the self-employed deduction interact through an iterative IRS calculation described in IRS Publication 974. For many Mississippi self-employed filers, this means effective premium costs after all tax benefits run 25–40% lower than the sticker price. A Hattiesburg consultant earning $52,000 might pay $245/month after subsidy for an Ambetter Silver HMO and deduct the $2,940 annual premium at tax time — saving an additional $700+ in federal taxes. Effective cost: roughly $185/month for full ACA coverage.

Example — Jackson Freelance Developer, Age 34, $58,000 Income: A self-employed software developer in Jackson earning $58,000/year (about 380% FPL) selects Oscar Health Silver HMO at $630/month full premium — the cheapest Silver in Jackson’s 11-county Oscar service area. Estimated premium tax credit: about $340/month. Net monthly cost after subsidy: roughly $290/month ($3,480/year). The self-employed deduction saves an additional $835 at the 24% bracket. Effective annual cost: approximately $2,645, or $220/month for ACA-compliant individual coverage on Oscar’s telemedicine-forward platform.

Compare Mississippi Individual Coverage Options

See individual and private plans from all 2026 Mississippi carriers — Ambetter, BCBS MS (including off-exchange PPO), Cigna, Molina, UHC, and Oscar Health. Calculate subsidy impact and self-employed deduction value with a licensed enrollment assistant, at no cost to you.

Pre-Medicare Coverage for Mississippi Early Retirees

Mississippi early retirees — those between 55 and 64 who leave the workforce before Medicare — rely heavily on individual health insurance in Mississippi through HealthCare.gov. Without employer coverage, pre-Medicare retirees face the highest premiums by age (a 60-year-old pays roughly 3x a 21-year-old) but also benefit most from premium tax credits when they control retirement income through strategic account withdrawals.

For Mississippi early retirees, MAGI management is the most powerful tool. A 62-year-old couple in Hattiesburg with $850,000 in retirement assets can draw from a Roth IRA (not counted as MAGI), keep taxable IRA withdrawals under $62,000 combined, and qualify for substantial premium tax credits that cut a $2,200/month Ambetter Silver premium to about $440/month. The same couple drawing $85,000 from traditional IRAs crosses the subsidy cliff and pays full price — a $21,000/year swing in healthcare cost from a $23,000 difference in income strategy. The Mississippi affordable coverage guide covers MAGI strategies in more detail.

Mississippi’s 43.4% statewide rate increase for 2026 hits early retirees hardest because their base premiums are already the highest. A 60-year-old Ambetter enrollee in Jackson saw a full-price Silver premium climb from about $1,060/month in 2025 to roughly $1,475/month in 2026 per filings approved by the Mississippi Insurance Department. Subsidies absorb most of this for qualifying retirees, but unsubsidized early retirees face the most expensive individual health insurance in Mississippi of any age group before Medicare. Private off-exchange BCBS Mississippi PPO — with its +23.34% increase, the lowest in the state — is often the least-bad option for higher-income pre-Medicare residents who also want PPO access to Memphis or New Orleans specialists.

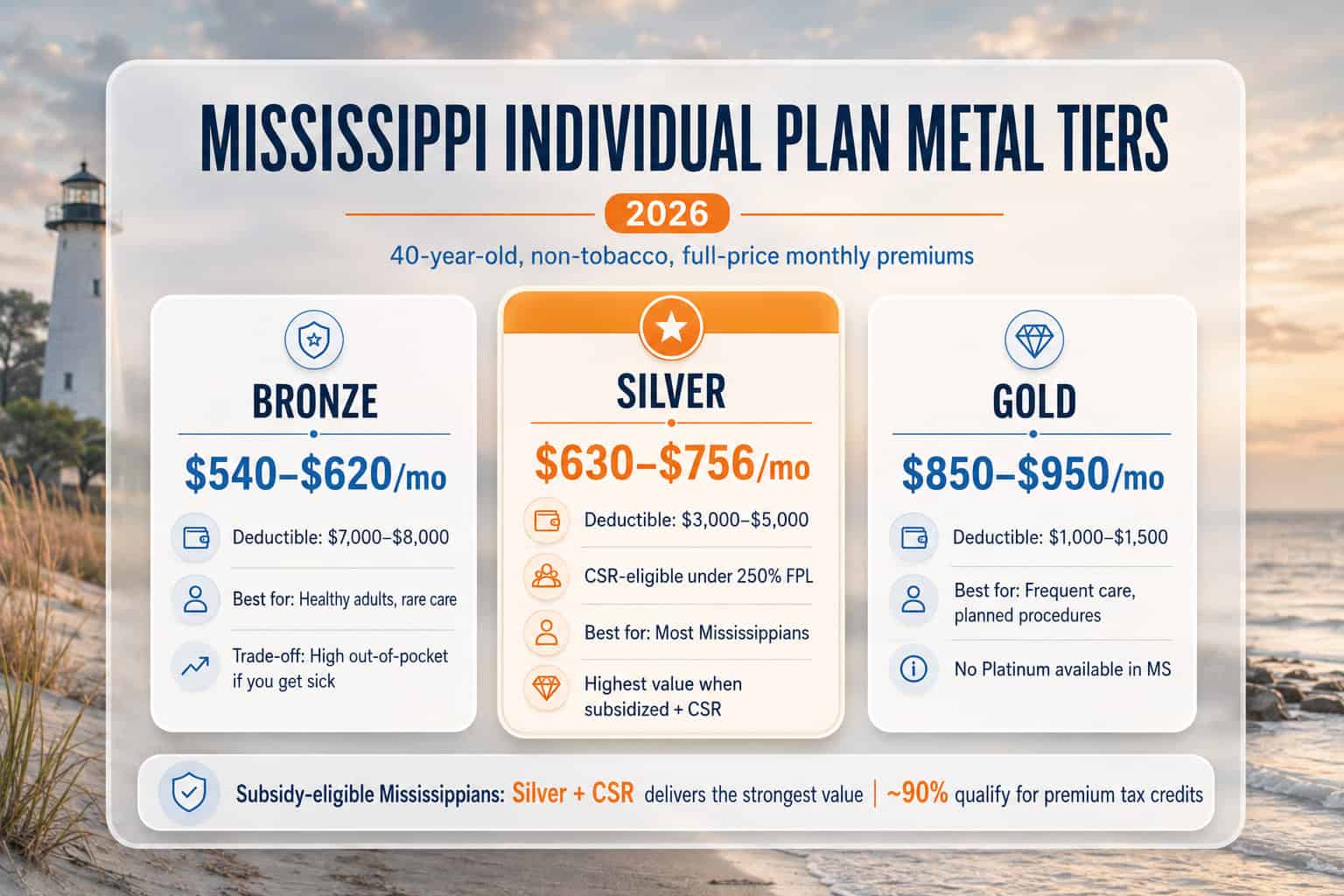

Choosing a Metal Tier for Your Mississippi Individual Plan

Mississippi marketplace plans come in three available metal tiers: Bronze (lowest premium, highest deductible), Silver (moderate premium, CSR-eligible under 250% FPL), and Gold (higher premium, lower deductible) — no Platinum plans are sold in Mississippi. Oscar Health offers the cheapest Silver near $630/month for a 40-year-old, while Cigna Bronze starts around $596/month. For low-use healthy adults, Bronze saves monthly but exposes you to $7,000+ deductibles before coverage starts.

For subsidy-eligible Mississippians earning under 250% FPL, Silver plans with cost-sharing reductions deliver the best overall value — the CSR lowers deductibles, copays, and out-of-pocket maximums automatically at no extra cost. A standard $5,000 Silver deductible might drop to $700 under strong CSRs, making Silver + CSR substantially better than Bronze for anyone who expects to use care during the year, even when the Bronze premium looks cheaper. For most households, matching metal tier to expected use is the final step in choosing the right individual health insurance in Mississippi. For healthy Mississippians above 250% FPL with minimal needs, Bronze minimizes monthly cost — but one ER visit can mean $5,000+ out of pocket.

Individual Coverage Questions From Mississippi Residents

Who typically buys individual health insurance in Mississippi?

Self-employed professionals, 1099 contractors, freelancers, early retirees under 65, part-time workers without benefits, adult children aging off a parent’s plan at 26, and people between jobs. Mississippi’s individual market also absorbs low-income adults above 100% FPL who would be covered by Medicaid in expansion states — about 313,392 Mississippians enrolled in 2026 marketplace plans.

Can self-employed Mississippians deduct individual plan premiums?

Yes. The self-employed health insurance deduction lets sole proprietors, LLC members, S-corp shareholders (2%+), and partners deduct 100% of premiums for themselves and dependents as an adjustment to gross income. It coordinates with marketplace subsidies through an iterative calculation in IRS Publication 974. Effective premium costs after all tax benefits typically run 25–40% below sticker price for Mississippi self-employed filers.

Is private off-exchange BCBS Mississippi PPO available on HealthCare.gov?

BCBS of Mississippi sells both on-exchange and off-exchange, but its flagship PPO is primarily marketed off-exchange as private health insurance that doesn’t qualify for premium tax credits. For unsubsidized Mississippians above 400% FPL, off-exchange BCBS MS PPO provides the broadest statewide network with out-of-network coverage — valuable for Memphis, New Orleans, and Birmingham specialist access. Subsidy-eligible enrollees usually do better on-exchange with HMO or Cigna EPO plans.

What’s the coverage gap and does it affect individual plan eligibility?

Mississippi’s coverage gap affects roughly 71,000 adults who earn below 100% FPL ($15,060/single) but above Mississippi Medicaid’s 22% FPL parent threshold. They’re ineligible for both Medicaid and marketplace subsidies. This gap exists only in non-expansion states like Mississippi. Adults at or above 100% FPL can enroll in individual marketplace plans with premium tax credits, so projecting income to at least 100% FPL during enrollment is critical.

When can I enroll in Mississippi individual coverage?

Open Enrollment for 2026 ran November 1, 2025 through January 15, 2026. For 2027 coverage, the window shortens to November 1 – December 15, 2026. Outside these periods, a Qualifying Life Event (job loss, marriage, birth, moving, loss of Medicaid) triggers a 60-day Special Enrollment Period. Mississippi Medicaid and CHIP allow year-round enrollment for eligible residents.

Are pre-existing conditions covered on Mississippi individual plans?

Yes. Every ACA-compliant individual plan sold in Mississippi — on-exchange and off-exchange — covers pre-existing conditions with no waiting periods, no exclusions, and no higher premiums based on health history. This applies to all five 2026 marketplace carriers plus off-exchange BCBS MS and Celtic. Only non-ACA products like short-term plans and health sharing ministries can exclude pre-existing conditions.

Related Mississippi Health Insurance Resources

Explore related guides for Mississippi’s overall coverage landscape, marketplace enrollment, the coverage gap and affordability options, and PPO plan flexibility to help navigate individual coverage decisions in the Magnolia State.

Plans, costs, carriers, and how coverage works statewide.

Marketplace EnrollmentHealthCare.gov enrollment, deadlines, subsidies, and qualifying life events.

Affordable Coverage & the GapPremium tax credits, the coverage gap, Medicaid, and CHIP alternatives.

PPO PlansReferral-free specialist access and out-of-network coverage nationwide.

Find 2026 Mississippi Individual Coverage

Compare individual and private plans from Ambetter, BCBS MS (on- and off-exchange PPO), Cigna EPO, Molina, UHC, and Oscar Health. Subsidy calculations, self-employed tax planning, and early-retiree MAGI strategy from a licensed enrollment assistant. Free, with no cost to you.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Mississippi residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.