Affordable Health Insurance in Missouri: 2026 Costs & Subsidies

Finding affordable health insurance in Missouri starts with one fact most shoppers underestimate: roughly 90% of the state’s 417,000 marketplace enrollees receive premium tax credits, and many pay a small fraction of the sticker price. For 2026, nine carriers compete on HealthCare.gov, with Blue Cross Blue Shield of Kansas City cutting Silver rates 4.1% in western counties even as Cox Health Plans rose 30.4% near Springfield. This guide breaks down what coverage really costs across Missouri, who qualifies for free MO HealthNet, the cheapest plans by metal tier, and the practical ways Missourians lower their premiums in 2026.

What’s your path to affordable coverage in Missouri?

How Much Does Health Insurance Cost in Missouri in 2026?

Unsubsidized 2026 premiums in Missouri average roughly $480 per month for a benchmark Silver plan, but the range is wide: Blue Cross Blue Shield of Kansas City cut Silver rates 4.1% in western counties while Cox Health Plans rose 30.4% near Springfield and Ambetter climbed 24.37%. After premium tax credits, most enrollees pay far less. What you actually pay for affordable health insurance in Missouri depends on your county, age, income, and the carrier you choose.

Sticker price and real cost diverge sharply in Missouri. A 40-year-old in Jackson County (Kansas City) might see a benchmark Silver plan near $520 per month before any subsidy, while the same shopper in St. Louis County sees modestly higher rates tied to the BJC HealthCare and SSM Health systems. Greene County residents around Springfield often find lower benchmark figures. Because affordable health insurance in Missouri is so heavily shaped by subsidies, the smartest comparison is always after-credit cost, not the headline premium.

Three factors move a Missourian’s premium the most: age (a 60-year-old pays roughly three times a 21-year-old’s rate under federal age-banding), county (carrier competition ranges from two plans in rural counties to seven in the St. Louis metro), and metal tier. The Missouri Department of Commerce and Insurance publishes the approved rate filings each year, and the spread between the cheapest and most expensive carrier in a single county can exceed $200 per month for comparable coverage.

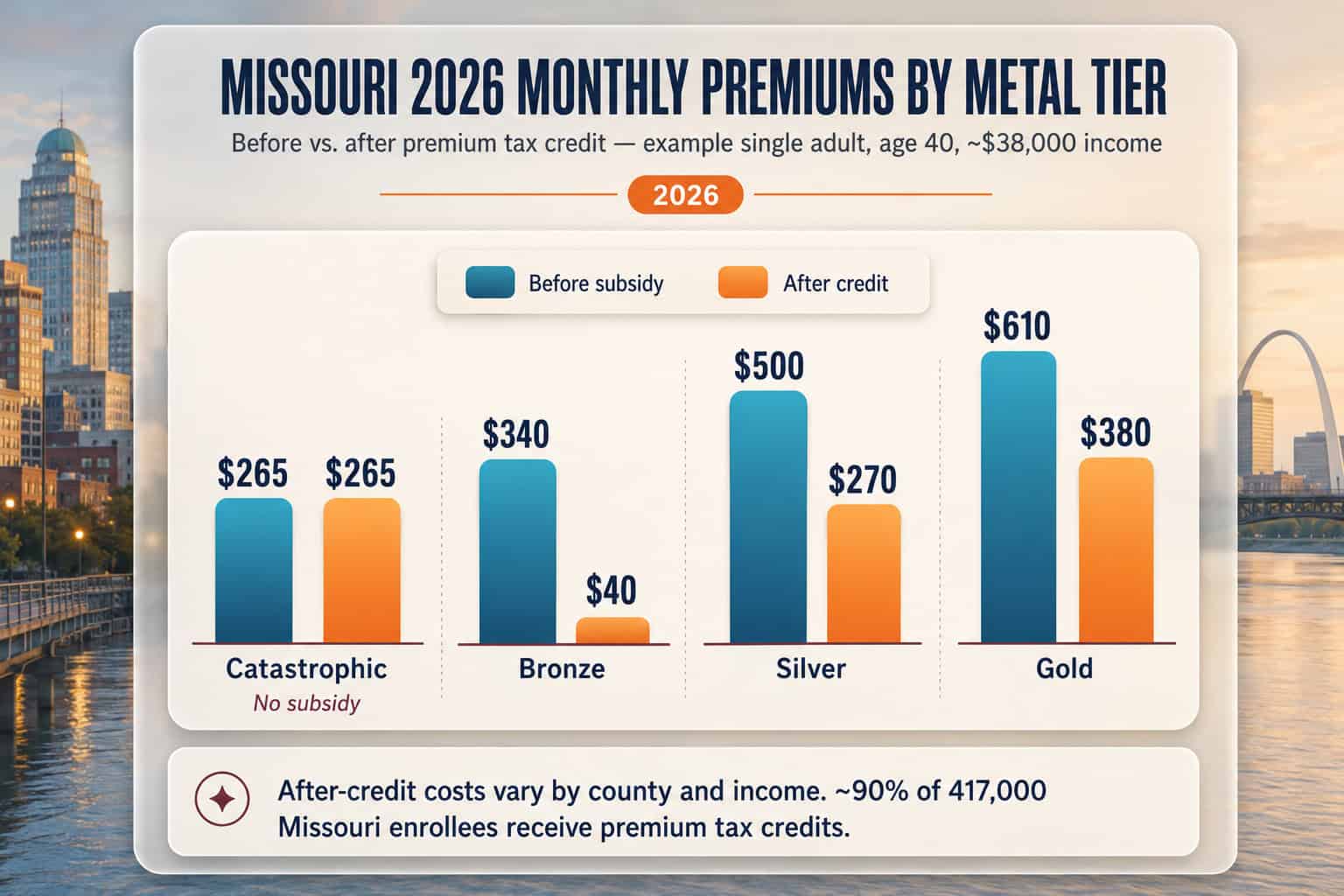

Premium Tax Credits Make Coverage Affordable in Missouri

About 90% of Missouri’s roughly 417,000 marketplace enrollees receive premium tax credits, and a St. Louis County single adult earning $38,000 commonly gets around $485 per month — turning a $755 Silver plan into roughly $270. Premium tax credits are the single biggest lever for affordable health insurance in Missouri: they scale by household income against the benchmark Silver plan in your county, applying the same federal formula used nationwide but to Missouri-specific premiums.

The federal subsidy math works the same in every state, but the dollars depend on local premiums. A household between 100% and 400% of the Federal Poverty Level qualifies for premium tax credits, and enhanced subsidies enacted under the American Rescue Plan and extended by the Inflation Reduction Act pushed eligibility above 400% FPL. For a Springfield family in Greene County, that can mean the difference between an unaffordable $1,890 monthly Silver plan and a manageable $330 after credits. Subsidies reconcile at tax time through IRS Form 8962, so accurate income estimates matter.

There is a real 2026 risk Missourians should weigh: roughly 60,000 to 80,000 Missouri families would lose subsidy eligibility if enhanced credits expire without a Congressional extension. If that happens, the 400% FPL “subsidy cliff” returns — a single Missourian earning just over $62,600 would face the full unsubsidized premium. For now, affordable health insurance in Missouri remains within reach for the large majority who qualify, but the window to lock in 2026 savings runs on the federal Open Enrollment calendar.

MO HealthNet: Free and Low-Cost Coverage in Missouri

Missourians earning under 138% of the Federal Poverty Level — about $21,597 for one adult or $44,367 for a family of four in 2026 — qualify for free or near-free coverage through MO HealthNet, the state’s voter-approved expanded Medicaid program. For the lowest-income residents, MO HealthNet is the most affordable health insurance in Missouri available, with no monthly premium. HealthCare.gov screens for it automatically during the application.

Missouri voters approved Medicaid expansion in 2020, and MO HealthNet now covers adults up to 138% FPL who previously fell into the coverage gap. Enrollment runs year-round through the Missouri Department of Social Services — there is no Open Enrollment restriction, and coverage can be retroactive up to three months for eligible applicants. Children in households above the MO HealthNet line may still qualify for Show Me Healthy Kids, Missouri’s CHIP program, which extends low-cost coverage to families who earn too much for Medicaid but struggle with marketplace premiums.

Don’t assume you earn too much: Missouri’s redeterminations move thousands of residents on and off MO HealthNet each year. If your income dropped — job loss, reduced hours, self-employment slowdown — re-check eligibility before paying for a marketplace plan. Losing MO HealthNet also triggers a Special Enrollment Period, so a coverage gap need not become permanent.

Cheapest Marketplace Plans by Metal Tier in Missouri

The cheapest marketplace tier in Missouri is Bronze, with 2026 premiums roughly $300–$380 per month before subsidies for a 40-year-old, often dropping near $0 after credits. Blue Cross Blue Shield of Kansas City carries the lowest Silver option in western Missouri after its 4.1% cut, while Ambetter from Home State Health is frequently cheapest elsewhere. Choosing the most affordable health insurance in Missouri means weighing premium against deductible, not premium alone.

Metal tiers trade monthly premium against out-of-pocket cost. Bronze plans have the lowest premiums but deductibles often exceeding $7,000 — best for healthy Missourians who rarely use care and want catastrophic protection. Silver plans cost more monthly but unlock Cost-Sharing Reductions for households under 250% FPL, frequently making them the true value pick. Gold plans suit those with regular prescriptions or chronic conditions. Adults under 30 can also buy a catastrophic plan, the lowest-premium option of all, though it does not qualify for premium tax credits.

| Metal Tier | Typical 2026 MO Premium (age 40, pre-subsidy) | Deductible Range | Best For |

|---|---|---|---|

| Catastrophic (under 30) | $230–$300/mo | ~$9,200 (ACA max) | Young, healthy, no subsidy |

| Bronze | $300–$380/mo | $6,000–$8,000+ | Low premium, rare care use |

| Silver | $440–$560/mo | $3,500–$5,500 (lower with CSR) | Under 250% FPL — best value |

| Gold | $540–$680/mo | $1,000–$2,500 | Regular prescriptions, chronic care |

Compare Affordable Missouri Plans in Minutes

A licensed agent sorts all nine Missouri carriers — BCBS Kansas City, Ambetter from Home State Health, Cox Health Plans, and the rest — by after-subsidy cost for your county, so you see the genuinely affordable health insurance in Missouri for your household, not just the lowest sticker price. If plan quality and network strength matter as much as price, compare how carriers stack up in the guide to the best health insurance in Missouri before you decide.

Ways to Lower Your Health Insurance Costs in Missouri

The fastest way to lower costs is confirming your premium tax credit, since roughly 90% of Missouri enrollees qualify and many leave money unclaimed. Beyond subsidies, Missourians cut costs by choosing a Silver plan when under 250% FPL to capture Cost-Sharing Reductions, pairing a Bronze plan with an HSA, or — for those whose employers offer one — using an ICHRA allowance. Each route to affordable health insurance in Missouri depends on income and how often you use care.

For households just above the MO HealthNet line, Cost-Sharing Reductions are the most overlooked savings: choosing Silver under 250% FPL lowers deductibles and copays automatically, often making Silver cheaper overall than Bronze despite a higher premium. Self-employed Missourians can deduct premiums and should report income carefully, since fluctuating freelance earnings in Jackson or Greene County often unlock larger credits than people expect. Healthy enrollees can pair a Bronze plan with a Health Savings Account to shelter pre-tax dollars against the higher deductible.

Employees whose Missouri small business offers an Individual Coverage Health Reimbursement Arrangement can use that fixed allowance toward an individual plan on HealthCare.gov — see the Missouri small business coverage guide for how ICHRA works. And every Missourian should re-shop at renewal: with BCBS of Kansas City cutting rates while Cox rose 30.4%, last year’s cheapest plan may not be this year’s, and auto-renewing without comparing can quietly raise costs hundreds of dollars a year.

Who Qualifies for Affordable Coverage in Missouri?

Nearly every Missourian qualifies for some form of cost relief: under 138% FPL (about $21,597 for one adult) routes to free MO HealthNet, while 100%–400% FPL and beyond unlocks premium tax credits on HealthCare.gov. With about 90% of the state’s 417,000 enrollees subsidized, affordable health insurance in Missouri is the rule, not the exception. Eligibility turns on household income relative to the federal poverty guidelines applied to Missouri premiums.

The income bands work in tiers. A single adult in Missouri earning under roughly $21,597 (138% FPL) qualifies for MO HealthNet at no premium. Between that line and 400% FPL — about $62,600 for one person — premium tax credits apply on a sliding scale, with larger credits at lower incomes. Enhanced subsidies currently extend help above 400% FPL, capping benchmark Silver premiums at a percentage of income, as detailed on the HealthCare.gov cost-savings page. A family of four in Greene County earning $64,000 sits near 198% FPL, qualifying for both substantial credits and Cost-Sharing Reductions.

Most likely to find low-cost coverage

Low-to-moderate income households, the self-employed with variable income, part-time workers without job-based coverage, early retirees before Medicare, and anyone who recently lost MO HealthNet. These Missourians typically qualify for meaningful premium tax credits or Medicaid.

May pay full price without planning

Higher earners above the subsidy thresholds, especially if enhanced credits expire. These Missourians benefit most from comparing Bronze plans across carriers, HSA-eligible options, and — where available — an employer ICHRA allowance to offset cost.

Frequently Asked Questions About Affordable Missouri Coverage

How much does the cheapest health insurance cost in Missouri?

For 2026, the lowest unsubsidized Bronze premiums in Missouri run roughly $300–$380 per month for a single adult around age 40, with Blue Cross Blue Shield of Kansas City offering the cheapest Silver option in western counties after its 4.1% rate cut. After premium tax credits, many Missourians pay far less — some qualify for $0 Bronze plans. Catastrophic plans for those under 30 run lower still but carry very high deductibles.

Who qualifies for free health insurance in Missouri?

Missourians earning under 138% of the Federal Poverty Level — about $21,597 for a single adult or $44,367 for a family of four in 2026 — qualify for free or near-free coverage through MO HealthNet, Missouri’s voter-approved expanded Medicaid program. Children may qualify for Show Me Healthy Kids (CHIP) at higher income levels. MO HealthNet enrolls year-round through the Missouri Department of Social Services, with no Open Enrollment restriction.

What is the most affordable health insurance in Missouri without a subsidy?

Without a subsidy, the most affordable health insurance in Missouri is typically a Bronze plan from the lowest-cost carrier in your county — often BCBS of Kansas City in the west or Ambetter from Home State Health elsewhere. Bronze plans carry low premiums but high deductibles. Adults under 30 can also buy a catastrophic plan. Comparing all nine Missouri carriers by total annual cost, not just premium, finds the real value.

Do most Missourians get subsidies on the marketplace?

Yes. Roughly 90% of Missouri’s marketplace enrollees — of about 417,000 statewide — receive premium tax credits that lower their monthly cost. Households between 100% and 400% of the Federal Poverty Level qualify, and enhanced subsidies have extended help above 400% FPL. A St. Louis County single adult earning $38,000 commonly receives around $485 per month, turning a $755 Silver plan into roughly $270.

Is short-term health insurance a cheap option in Missouri?

Missouri permits short-term plans for an initial term up to 364 days with renewals up to 36 months total, and premiums look cheap — often under $150 per month. But they are not ACA coverage: they can exclude pre-existing conditions, skip prescription and maternity benefits, and impose annual caps. For most Missourians, a subsidized Bronze or Silver plan is both more affordable after credits and far more protective than short-term coverage.

How can a self-employed Missourian find affordable coverage?

Self-employed Missourians buy individual coverage through HealthCare.gov and, because business income often fluctuates, frequently qualify for sizable premium tax credits — a Greene County freelancer estimating $40,000 may pay a fraction of sticker price. Reporting an accurate income projection is key, since subsidies reconcile at tax time. A licensed agent can model after-subsidy costs across all nine Missouri carriers before you commit to a plan.

Related Missouri Health Insurance Resources

Explore related guides for Missouri’s overall coverage landscape, marketplace enrollment, small business and group options, and PPO plan flexibility to help navigate affordable health insurance decisions in the Show-Me State.

Plans, costs, carriers, and how coverage works statewide.

Marketplace EnrollmentHealthCare.gov enrollment, deadlines, and qualifying life events.

Small Business & Group PlansSHOP coverage, group options, and tax credits for employers.

PPO PlansReferral-free specialist access and out-of-network coverage nationwide.

Find Your Most Affordable Missouri Plan for 2026

Get free, licensed help comparing after-subsidy costs across all nine Missouri carriers. A licensed agent checks your premium tax credit and MO HealthNet eligibility, then finds the genuinely affordable health insurance in Missouri that fits your household and budget.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Missouri residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.