Health Insurance Marketplace in Missouri: 2026 HealthCare.gov Enrollment Guide

The health insurance marketplace in Missouri is operated by the federal government through HealthCare.gov — Missouri does not run its own state-based exchange. Nine carriers offer plans for 2026, though only UnitedHealthcare serves every Missouri county, with Ambetter from Home State Health covering all but six rural counties. The Missouri Department of Commerce and Insurance (DCI) regulates carrier rates and plan filings, while HealthCare.gov handles enrollment. This guide covers how the federal exchange works for Missouri residents in 2026, who qualifies for subsidies, when Open Enrollment runs, and how Cover Missouri Coalition navigators help Missourians enroll at no cost.

Where are you in the Missouri enrollment process?

How the Missouri Health Insurance Marketplace Works

The health insurance marketplace in Missouri is run by the federal government through HealthCare.gov, not the state — Missouri opted not to build its own state-based health insurance marketplace when the ACA launched, so all enrollment, plan shopping, and subsidy applications happen on the federal marketplace. The Missouri Department of Commerce and Insurance regulates carrier rates and filings, while HealthCare.gov handles enrollment. The Cover Missouri Coalition, funded by the Missouri Foundation for Health, provides free enrollment help statewide.

For 2026, nine carriers offer plans on HealthCare.gov for Missouri residents: Blue Cross Blue Shield of Kansas City, Anthem Blue Cross Blue Shield of Missouri, Ambetter from Home State Health, UnitedHealthcare, Oscar Health, Cox Health Plans, Cigna, Aetna, and Medica. Only UnitedHealthcare covers every Missouri county statewide. Ambetter covers every county except six rural ones — Clark, Lewis, Marion, St. Francois, Schuyler, and Scotland. St. Louis metro residents typically see seven carriers competing for their business, while rural counties may have only two. The exchange displays each plan with standardized information (premium, deductible, out-of-pocket maximum, network type, covered drug list) to allow apples-to-apples comparison. The individual marketplace covers individuals and families; small employers have a separate track through the SHOP marketplace, covered in the Missouri small business health insurance guide.

HealthCare.gov also screens for MO HealthNet (Missouri Medicaid) eligibility during the application process. Households earning under 138% of the Federal Poverty Level — approximately $21,597 for a single adult or $44,367 for a family of four in 2026 — are routed to the Missouri Department of Social Services for MO HealthNet enrollment instead of being shown marketplace plans. This single-portal eligibility check prevents Missourians from accidentally enrolling in marketplace coverage when they qualify for free Medicaid through Missouri’s voter-approved Medicaid expansion.

How to Enroll in a Missouri Marketplace Plan for 2026

Missouri shoppers choose from up to nine marketplace carriers depending on county, and the Cover Missouri Coalition offers free navigator help statewide. Enrollment runs through HealthCare.gov in five steps: create or log into an account, complete the eligibility application with household and income details, compare the plans available in your county, select one, and pay the first month’s premium to activate coverage. For a first-time enrollee with documents ready, the process typically takes 30–60 minutes.

Gather required information

Have ready: Social Security numbers for everyone in the household, employer and income details, current health insurance information (if any), and projected 2026 household income. Self-employed Missourians should have their best income estimate based on prior-year returns and expected changes.

Create a HealthCare.gov account

Visit HealthCare.gov and create an account or log in to your existing one. The federal portal serves all Missourians applying for marketplace coverage. You’ll verify your identity through Experian’s verification system — most enrollees clear this step in under five minutes.

Complete the eligibility application

Enter household composition, projected income, and current coverage status. The application screens for MO HealthNet, Show Me Healthy Kids (CHIP), and marketplace eligibility automatically. If you’re routed to MO HealthNet, you can complete that application through the Missouri Department of Social Services. If you qualify for marketplace subsidies, the system calculates your estimated premium tax credit.

Compare and select a plan

Filter by metal tier (Bronze, Silver, Gold, Platinum), carrier, premium range, deductible, and total annual cost. Verify your doctors and prescription drugs are in-network for any plan you’re considering. Subsidized enrollees should focus on after-subsidy cost rather than sticker price. Kansas City metro residents should compare BCBS of Kansas City carefully — its 4.1% rate cut makes it the lowest Silver option in western Missouri for 2026.

Pay first premium and activate

Coverage activates only when the carrier receives your first premium payment, not when you select the plan on HealthCare.gov. Most Missouri carriers require payment within 30 days. After payment, ID cards arrive within 7–14 days and you can begin using your coverage on the effective date.

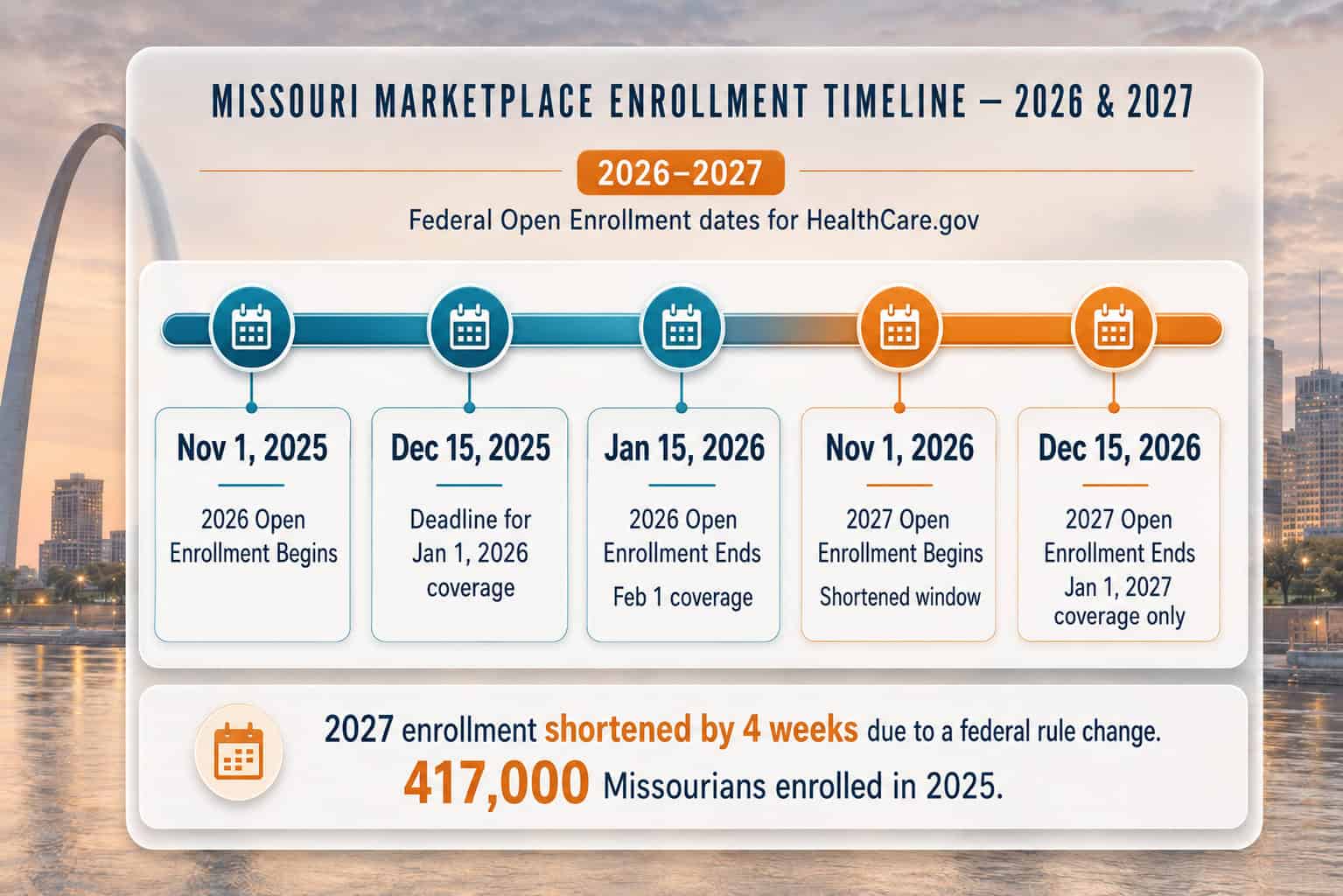

Missouri Marketplace Open Enrollment Dates

With roughly 417,000 Missourians enrolled in 2025 marketplace coverage, the state runs on the federal Open Enrollment calendar through HealthCare.gov. Open Enrollment for 2026 Missouri coverage ran November 1, 2025 through January 15, 2026. For 2027, the federal government shortened the window to November 1 through December 15, 2026 — six weeks instead of ten. Plans selected during that window take effect January 1, 2027, and there is no automatic renewal — every household must actively confirm or change coverage.

| Plan Year | Open Enrollment Window | Coverage Effective |

|---|---|---|

| 2026 (current) | Nov 1, 2025 – Jan 15, 2026 | Jan 1 or Feb 1, 2026 |

| 2027 (upcoming) | Nov 1 – Dec 15, 2026 | Jan 1, 2027 |

| Special Enrollment | 60 days from Qualifying Life Event | First of following month |

| MO HealthNet / Show Me Healthy Kids | Year-round (no OEP restriction) | Retroactive up to 3 months if eligible |

Shorter 2027 enrollment window: The federal rule change shortens Open Enrollment by approximately four weeks starting with the 2027 plan year. December 15, 2026 is the absolute deadline for 2027 marketplace coverage — no extensions and no January enrollment window. Missourians who miss December 15 without a Qualifying Life Event will be uninsured until the 2028 Open Enrollment window. Mark calendars early.

Special Enrollment Periods for Missouri Marketplace Plans

Loss of MO HealthNet eligibility is one of the most common Special Enrollment triggers in Missouri, as ongoing Medicaid redeterminations move residents off the rolls and onto marketplace coverage. Beyond that, the standard federal Qualifying Life Events apply — marriage, birth or adoption, loss of job-based coverage, COBRA expiring, aging off a parent’s plan at 26, or moving to Missouri. Each grants 60 days from the event to enroll through the HealthCare.gov Special Enrollment Period portal.

Qualifying Life Events that trigger SEP

Marriage, birth, adoption, divorce, death of a family member, loss of job-based coverage, loss of MO HealthNet, moving to Missouri from another state, becoming a U.S. citizen, leaving incarceration. Documentation of the event is typically required to enroll during the 60-day SEP window.

Events that do NOT trigger SEP

Voluntarily dropping coverage, missing payments and losing coverage, changing your mind about a Missouri plan you selected, getting fired and refusing COBRA. These do not qualify — Missourians in these situations typically wait until the next Open Enrollment or apply for MO HealthNet if income-qualified.

Get Help Enrolling in Missouri Marketplace Plans

Comparing nine Missouri carriers across counties where availability runs from two plans in rural areas to seven in the St. Louis metro takes time. A licensed agent sorts BCBS Kansas City, Ambetter from Home State Health, Cox Health Plans, and the rest by network and subsidy fit at no cost, while the Cover Missouri Coalition offers free navigator help statewide.

Renewing Missouri Marketplace Coverage for 2026 and Beyond

Because Missouri 2026 premium changes varied sharply by carrier — BCBS of Kansas City cut rates 4.1% while Cox rose 30.4% and Ambetter jumped 24.37% — active renewal matters more here than in steadier markets. Missouri marketplace plans do not automatically renew with subsidies preserved: every enrollee must log into HealthCare.gov each year, update income and household composition, and confirm or change their plan. Auto-renewing without reviewing the rate impact could produce a surprise bill hundreds of dollars higher.

With Cox Health Plans subscribers facing a 30.4% increase while BCBS Kansas City members see a 4.1% cut, the renewal review is where Missouri enrollees either lock in savings or absorb an avoidable jump. Returning enrollees verify income against 2026 subsidy tables, confirm household members, and check whether their plan still appears in their county — Ambetter’s pullback from Clark, Lewis, Marion, St. Francois, Schuyler, and Scotland counties means some rural Missourians must actively choose a new carrier rather than auto-renew. Reporting income shifts matters because they reset premium tax credit amounts: a St. Louis County household that underestimates earnings owes the difference back at tax time, while overestimating ties up money all year.

Subsidies and Premium Tax Credits on the Missouri Marketplace

A St. Louis County resident earning $38,000 typically qualifies for about $485/month in premium tax credits, bringing a Silver plan from $755/month down to around $270/month. Subsidies on the Missouri health insurance marketplace scale by household income and the cost of the benchmark Silver plan in your county. Roughly 60,000–80,000 Missouri families would lose subsidy eligibility if enhanced credits expire without Congressional extension — making the 2026 subsidy question especially consequential for the state’s marketplace enrollees.

Two types of financial assistance flow through the Missouri health insurance marketplace: Premium Tax Credits (which lower monthly premiums) and Cost-Sharing Reductions (which lower deductibles and copays for enrollees under 250% FPL who choose Silver plans). Enhanced subsidies enacted under the American Rescue Plan and extended by the Inflation Reduction Act expanded eligibility above 400% FPL — but are scheduled to revert to pre-2021 rules without Congressional extension. Subsidies on the health insurance marketplace in Missouri reconcile at tax time via IRS Form 8962. The Missouri affordable coverage guide details subsidy eligibility by household size and income.

Example: Springfield Family of 4, $64,000 Income. A Greene County family of four (two adults ages 38 and 40, two children) earning $64,000/year is at approximately 198% FPL. Their estimated 2026 marketplace options: UHC Silver family plan at approximately $1,890/month full price minus approximately $1,560/month in premium tax credits = about $330/month after subsidy. A Bronze plan would run closer to $175/month after the same subsidy but with a higher deductible. Because the household is under 250% FPL, the Silver plan also qualifies for cost-sharing reductions that lower deductibles and copays significantly — typically the better value for families with regular healthcare needs.

Frequently Asked Questions About the Missouri Marketplace

Where do I sign up for the Missouri health insurance marketplace?

Missouri residents enroll in the health insurance marketplace in Missouri through HealthCare.gov, the federal marketplace. Missouri does not operate its own state-based exchange. The HealthCare.gov platform handles all aspects of enrollment — eligibility screening, plan comparison, subsidy calculation, and plan selection. Free, licensed enrollment assistance is available through the Cover Missouri Coalition (Missouri Foundation for Health) at 1-800-466-3213 or through licensed agents.

When is Missouri marketplace Open Enrollment?

Open Enrollment for 2026 coverage on the health insurance marketplace in Missouri ran November 1, 2025 through January 15, 2026. For 2027 coverage, the window is shortened to November 1 through December 15, 2026 — about six weeks. Outside Open Enrollment, a Qualifying Life Event is needed to enroll. MO HealthNet and Show Me Healthy Kids allow year-round enrollment.

How do I qualify for Missouri marketplace subsidies?

Subsidy eligibility is determined by household income relative to the Federal Poverty Level. Households earning between 100% and 400% FPL typically qualify for premium tax credits. Enhanced subsidies extended eligibility above 400% FPL through 2025. Under the pre-2021 rules that return if enhanced subsidies aren’t extended, the 400% FPL cliff hits hard — an unsubsidized Missourian earning $62,600+ would pay the full $9,060/year for an average UHC or Ambetter plan.

What happens if I miss the December 15, 2026 deadline for 2027 coverage?

Missouri residents who miss the December 15, 2026 Open Enrollment deadline generally cannot enroll in marketplace coverage for 2027 without a Qualifying Life Event. The federal government shortened the 2027 window to six weeks. Options at that point: MO HealthNet if income-qualified (under 138% FPL), short-term coverage as a stopgap, or waiting until the November 2027 Open Enrollment.

Is there a separate Missouri marketplace, or just HealthCare.gov?

HealthCare.gov is the only official Missouri marketplace. Missouri opted not to build a state-based exchange when the ACA launched, so all individual marketplace enrollment runs through the federal portal. The Missouri Department of Commerce and Insurance regulates carrier rates and plan filings, but enrollment itself is federal. Any third-party site claiming to be the “Missouri marketplace” should be verified before enrollment.

What if my income changes during the year?

Report income changes to HealthCare.gov as soon as they occur. Income increases reduce your premium tax credit (so you’ll owe less or nothing back at tax time). Income decreases increase your subsidy and lower your monthly premium. Failing to report changes can result in either a tax bill in April or paying more than necessary throughout the year. The IRS reconciles subsidies annually using Form 8962.

Related Missouri Health Insurance Resources

Explore related guides for Missouri’s overall coverage landscape, finding affordable plans and subsidies, comparing top-rated carriers, and PPO plan flexibility to help navigate marketplace decisions in the Show-Me State.

Plans, costs, carriers, and how coverage works statewide.

Affordable Coverage & SubsidiesLow-cost plans, premium tax credits, and ways to cut costs.

Best Carriers & PPO PlansHow Missouri’s top carriers rank by network and quality.

PPO PlansReferral-free specialist access and out-of-network coverage nationwide.

Enroll in Your 2026 Missouri Marketplace Plan

Get free, licensed help with HealthCare.gov enrollment. A licensed agent compares all nine Missouri carriers — including BCBS KC’s rate cut in western counties — checks subsidy eligibility, and walks you through every step of the application.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Missouri residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.