Shop and Save on Affordable Massachusetts Health Insurance

Whether you’re enrolling for the first time, checking whether you qualify for ConnectorCare, or comparing carriers before the deadline, Massachusetts gives you eight carriers to choose from through its own state marketplace — the Massachusetts Health Connector — with plans across every metal tier. Most Health Connector enrollees receive financial help that brings monthly costs down sharply, and the state’s ConnectorCare program layers extra subsidies on top of federal credits to deliver $0-deductible coverage for those who qualify. This guide breaks down what plans are available, what they actually cost at different incomes, the state’s individual mandate, and how to get enrolled.

Where do you want to start with Massachusetts health insurance?

How Much Does Health Insurance Cost in Massachusetts?

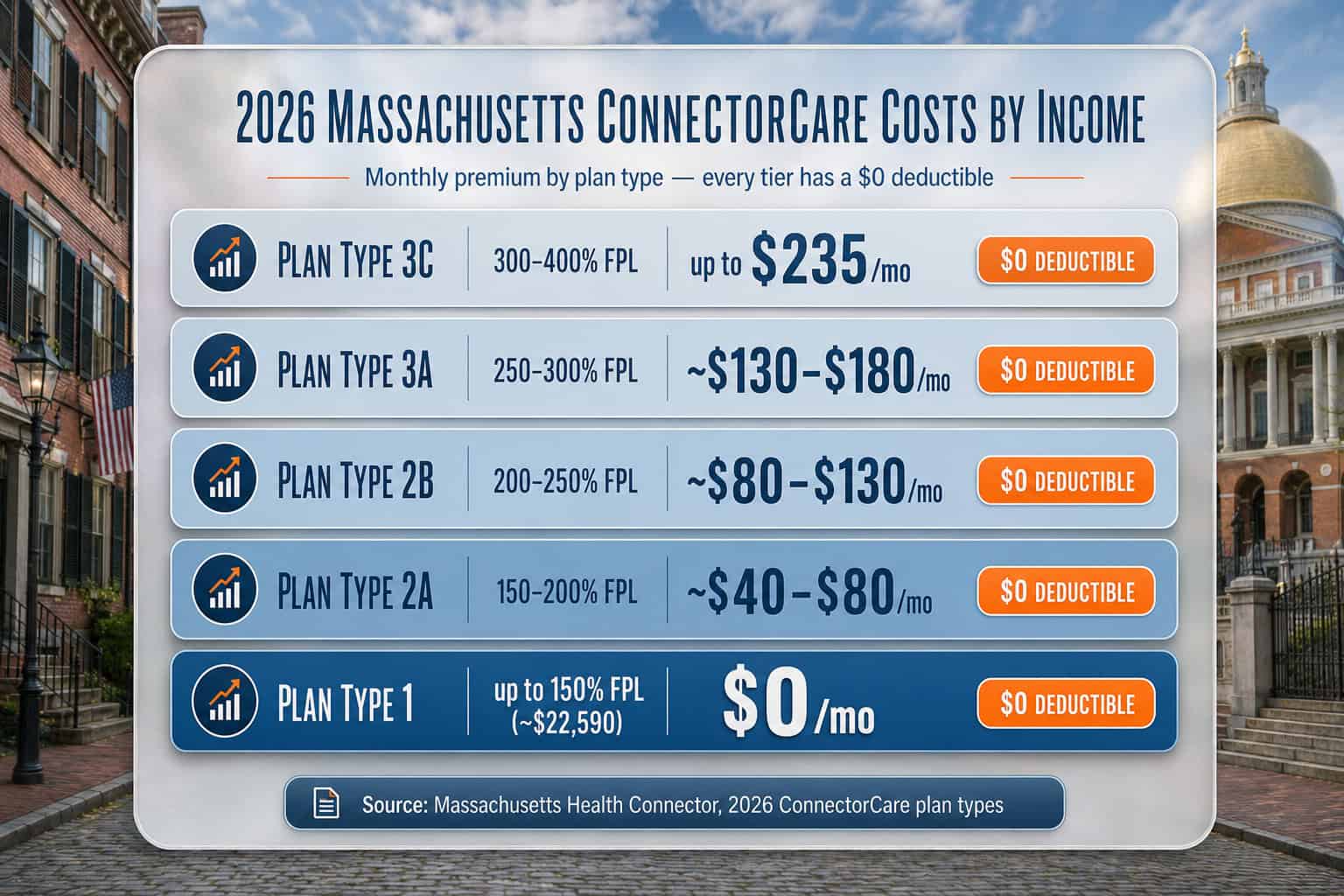

Massachusetts health insurance costs depend heavily on whether you qualify for ConnectorCare, the state’s subsidized coverage program. More than 83% of Health Connector enrollees receive financial help, with an average subsidy of $404 per month and an average after-subsidy premium of $126 per month. ConnectorCare plans range from $0/month for incomes up to 150% of the federal poverty level to roughly $235/month at 300%–400% FPL — all with no deductible and low fixed copays. For cost-reduction strategies, see the guide to affordable health insurance in Massachusetts.

For 2026, the Massachusetts Division of Insurance approved a merged-market weighted average rate increase of approximately 11.5% — well below the national average — driven by prescription drug costs and the projected impact of the expiration of enhanced federal premium tax credits at the end of 2025. Massachusetts also caps age-based pricing at a 2:1 ratio, so a 64-year-old pays at most twice what a 21-year-old pays for the same plan, compared with the 3:1 federal standard used in most other states.

| ConnectorCare Plan Type | Income Range (Individual) | Monthly Premium | Deductible |

|---|---|---|---|

| Plan Type 1 | Up to 150% FPL (~$22,590) | $0/month | $0 |

| Plan Type 2A | 150%–200% FPL (~$22,590–$30,120) | ~$40–$80/month | $0 |

| Plan Type 2B | 200%–250% FPL (~$30,120–$37,650) | ~$80–$130/month | $0 |

| Plan Type 3A | 250%–300% FPL (~$37,650–$45,180) | ~$130–$180/month | $0 |

| Plan Type 3C | 300%–400% FPL (~$45,180–$62,600) | Up to $235/month | $0 |

| Unsubsidized | Above ~$62,600 | Full price (varies by carrier/tier) | $0–$9,100 |

ConnectorCare combines federal advance premium tax credits with state-funded subsidies, producing no-deductible plans with standardized copays regardless of which carrier you choose. Every ConnectorCare plan also covers certain chronic-condition prescriptions at $0 — including medications for asthma, diabetes, hypertension, coronary artery disease, and opioid addiction. No other state layers its own subsidies this deeply on top of the federal credits.

Young Adults (Age 26)

~$0–$55/moA 26-year-old earning under 200% FPL typically lands in ConnectorCare Plan Type 1 or 2A — between $0 and roughly $55/month with a $0 deductible. Massachusetts’ 2:1 age-rating cap keeps young-adult premiums comparatively low even off-subsidy.

Adults (Age 40)

~$126/moThe average after-subsidy premium across Health Connector enrollees is about $126/month. A 40-year-old in a mid-income ConnectorCare band pays a fixed monthly amount with no deductible and low copays.

Older Adults (Age 60)

2:1 capBecause Massachusetts caps age rating at 2:1 rather than the federal 3:1, a 60-year-old pays at most twice a 21-year-old’s premium for the same plan — meaningfully less than older adults pay in most states before subsidies.

After Subsidies

~$126/moMore than 83% of Health Connector enrollees receive financial help, with subsidies averaging $404/month in 2025 and an average net premium near $126/month across all ages.

Massachusetts Health Insurance Companies and Carriers

Eight carriers offer individual and family plans through the Massachusetts Health Connector for 2026. Coverage areas vary by region — eastern Massachusetts counties such as Suffolk, Middlesex, and Norfolk typically have access to all eight, while residents in Hampden or Berkshire County in the west may find Fallon Health, Health New England, and Blue Cross Blue Shield of Massachusetts. For carrier rankings by network and region, see the guide to the best health insurance in Massachusetts.

| Carrier | Plan Types | Coverage Area | Notable Feature |

|---|---|---|---|

| Blue Cross Blue Shield of MA | HMO, PPO | Statewide | Largest carrier; multiple network tiers including Preferred Blue PPO |

| Harvard Pilgrim Health Care | HMO, PPO | Statewide (most counties) | Broad provider network; part of Point32Health with Tufts |

| Tufts Health Plan (3 entities) | HMO, POS | Varies by entity | Tufts Health Direct, Tufts Health Public Plans, Tufts Health Together |

| Mass General Brigham Health Plan | HMO | Eastern MA | Aligned with the Mass General Brigham hospital system |

| UnitedHealthcare | HMO, PPO | Multiple counties | National carrier; broad provider network |

| WellSense Health Plan | HMO | Eastern MA, select counties | Among the lowest-cost in the merged market; ConnectorCare focus |

| Fallon Health | HMO | Central and western MA | Community Care Network in Berkshire, Bristol, Hampden, Worcester |

| Health New England | HMO | Western MA | Baystate Health alignment; Springfield and the Berkshires |

Carrier selection matters most in western and central Massachusetts, where fewer carriers operate. Because Massachusetts runs a merged individual and small-group market, the same carrier rate increases apply to both segments — the 2026 merged-market average is about 11.5%. Massachusetts also requires an 88% medical loss ratio, meaning carriers must spend at least 88 cents of every premium dollar on member care, the strictest standard in the nation against the 80% federal minimum. All carriers discontinued GLP-1 weight-loss drug coverage on 2026 marketplace plans. Residents who want the widest provider access, including out-of-network coverage, often compare PPO health insurance plans from BCBSMA and Harvard Pilgrim.

Compare Massachusetts Health Insurance Plans

See which carriers serve your county, check ConnectorCare eligibility, and compare 2026 plan costs from all eight Health Connector carriers side by side.

Massachusetts Individual Mandate and Tax Penalty

Massachusetts requires most adults 18 and older to maintain coverage that meets Minimum Creditable Coverage (MCC) standards — or face a tax penalty on their state income tax return through Schedule HC. The penalty for 2026 can reach up to $135/month ($1,620/year) per uninsured adult. Massachusetts is one of only five states plus DC that enforces an individual mandate with financial penalties.

The penalty amount scales with income: residents earning below 150% FPL ($22,590 for an individual) face no penalty, since ConnectorCare is available at a $0 premium. Between 150% and 400% FPL, the penalty is half the lowest-priced ConnectorCare premium for that income; above 400% FPL, it is half the lowest-priced Bronze plan premium. A gap of 63 consecutive days or fewer does not trigger a penalty, and residents can appeal by showing coverage was unaffordable for their income.

How the Massachusetts Health Connector Works

The Massachusetts Health Connector at MAhealthconnector.org is a state-based marketplace — Massachusetts does not use HealthCare.gov. Open enrollment for 2026 ran November 1, 2025, through January 23, 2026, with a December 23 deadline for January 1 coverage. Approximately 391,744 residents enrolled for 2026, a slight increase from the 389,191 who enrolled for 2025, per CMS open enrollment data.

The Health Connector is the longest-running state-based marketplace in the country, established in 2006 under the Massachusetts health reform law that became the model for the federal ACA. It serves individuals, families, and small businesses with up to 50 employees, and determines eligibility for MassHealth (Medicaid), ConnectorCare, and unsubsidized plans through a single application. About 75% of 2026 enrollees receive some form of subsidy, down from 87% in 2025 because of federal policy changes affecting noncitizen eligibility and the expiration of enhanced premium tax credits. For a full walkthrough, see the Massachusetts marketplace and enrollment guide.

Subsidies and ConnectorCare in Massachusetts

Massachusetts offers a dual-subsidy system unlike any other state: federal advance premium tax credits, available in every state, layered with state-funded ConnectorCare subsidies that further reduce premiums, eliminate deductibles, standardize copays, and cover chronic-condition medications at $0. For 2026, ConnectorCare Plan Type 3C (300%–400% FPL) continues, while Plan Type 3D (400%–500% FPL) ended due to federal policy changes. Over 90% of ConnectorCare-eligible enrollees pay reduced premiums through this combined structure. Massachusetts allocated additional state funding for 2026 to partially buffer the loss of more than $425 million in federal aid if Congress does not extend the enhanced credits.

Federal Premium Tax Credits

For residents earning above the ConnectorCare threshold, standard federal premium tax credits still apply based on income and the benchmark Silver plan in their county, under IRS premium tax credit rules. Credits can be taken in advance to lower monthly premiums or claimed at tax time.

State ConnectorCare Subsidies

ConnectorCare adds state dollars on top of the federal credits for residents earning between 100% and 400% FPL. The result is no-deductible plans with standardized copays and $0 chronic-condition prescriptions, regardless of carrier. Massachusetts allocated additional state funding for 2026 to partially buffer the loss of more than $425 million in federal aid if Congress does not extend the enhanced credits.

MassHealth and the Health Safety Net

MassHealth (Medicaid) covers residents earning up to 138% FPL (about $21,597 for an individual), and the same Health Connector application screens for it automatically. The Health Safety Net pays for medically necessary care at participating hospitals and community health centers for residents who do not qualify for MassHealth or Connector coverage. Both are administered through MassHealth.

How to Enroll in Massachusetts Health Insurance

Enrolling in Massachusetts health insurance starts at MAhealthconnector.org, the state marketplace — not HealthCare.gov. Open enrollment for 2026 ran November 1, 2025, through January 23, 2026, with a December 23 deadline for January 1 coverage. Outside open enrollment, a qualifying life event opens a special enrollment period. Free help is available by phone at 1-877-MA-ENROLL (1-877-623-6765). For a complete walkthrough, see the Massachusetts marketplace enrollment guide.

Gather Information

Step 1Collect Social Security numbers, immigration documents if applicable, employer and income information, and current policy numbers for everyone who needs coverage.

Apply on the Health Connector

Step 2A single application at MAhealthconnector.org screens for MassHealth, ConnectorCare, and unsubsidized plans, then shows the programs and subsidies the household qualifies for.

Compare Plans and Carriers

Step 3Review options from the eight carriers serving your county across metal tiers and ConnectorCare plan types. Compare premiums, copays, provider networks, and prescription coverage.

Enroll and Pay First Premium

Step 4Select a plan that fits the household budget and needs, then make the first premium payment. Coverage is not active until that first payment is received.

Free in-person enrollment assistance is available statewide through Health Connector–certified navigators and community health centers, including assisters in Boston, Worcester, Springfield, and the Berkshires.

Choosing the Right Massachusetts Health Insurance Plan

For most subsidy-eligible residents earning under 400% of the federal poverty level, a ConnectorCare plan delivers the best overall value — $0 deductible, low fixed copays, and $0 chronic-condition prescriptions — which is why more than 83% of Health Connector enrollees take financial help. Residents above the ConnectorCare threshold weigh metal tiers and networks the way buyers do in other states, with carrier choice mattering most in western and central counties.

Qualify for ConnectorCare

Best valueHouseholds earning 100%–400% FPL get the strongest deal in the country: $0-deductible plans, standardized copays, and $0 chronic-condition drugs — often $0–$235/month depending on income band.

Healthy and Rarely Use Care

BronzeOff-subsidy residents who rarely see a doctor can take a Bronze plan for the lowest premium, accepting a higher deductible in exchange. Massachusetts’ 2:1 age cap keeps Bronze pricing gentler for older adults than in most states.

Frequent Care or Ongoing Conditions

GoldResidents managing a chronic condition off-subsidy often save with a Gold plan’s lower deductible and copays, especially given the 88% medical loss ratio that holds carrier pricing close together.

Need Provider Flexibility

PPOBCBSMA and Harvard Pilgrim offer PPO plans for residents who travel, see out-of-state specialists, or want out-of-network access. Compare PPO health insurance plans for nationwide coverage.

Other Health Coverage Options in Massachusetts

Beyond Health Connector plans and MassHealth, Massachusetts residents can access employer-sponsored group coverage, off-exchange individual plans purchased directly from one of the eight licensed carriers, and the Health Safety Net for residents who do not qualify for other coverage. Because Massachusetts runs a merged individual and small-group market, off-exchange plans are identical in coverage and price to on-exchange plans — but ConnectorCare and federal subsidies are available only through the Health Connector.

For small employers, the Health Connector’s small-group portal serves businesses with 1–50 employees using the same eight carriers; the small business health insurance in Massachusetts guide covers group options. Self-employed residents and those buying without a subsidy can review the individual health insurance in Massachusetts guide for off-exchange and private-plan details.

Frequently Asked Questions About Massachusetts Health Insurance

Eight carriers sell Massachusetts health insurance through the state’s own Health Connector, the individual mandate requires Minimum Creditable Coverage with a Schedule HC penalty for gaps, and ConnectorCare can lower premiums to $0 for eligible residents. The questions below cover the mandate, ConnectorCare, carriers, the state marketplace, short-term plans, and enrollment deadlines.

Does Massachusetts require health insurance?

Yes. Massachusetts has an individual mandate requiring most adults 18 and older to maintain coverage that meets Minimum Creditable Coverage (MCC) standards. Residents who do not comply face a tax penalty on their state return via Schedule HC, reaching up to $135/month ($1,620/year) per uninsured adult in 2026. Massachusetts is one of only five states plus DC with an active mandate penalty.

What is ConnectorCare and who qualifies?

ConnectorCare is the Massachusetts state-subsidized program offered through the Health Connector. It layers state subsidies on top of federal premium tax credits to provide $0 or low-premium plans with no deductibles, low copays, and $0 prescriptions for chronic conditions. For 2026, residents earning between 100% and 400% FPL (up to ~$62,600 for an individual) may qualify; Plan Type 1 is $0/month up to 150% FPL.

How many carriers are on the Massachusetts Health Connector?

Eight carriers offer plans through the Health Connector for 2026: Blue Cross Blue Shield of Massachusetts, Harvard Pilgrim Health Care, Tufts Health Plan, Mass General Brigham Health Plan, UnitedHealthcare, WellSense Health Plan, Fallon Health, and Health New England. Eastern Massachusetts has the most carrier choice, while western counties may have three to four options.

Is the Massachusetts Health Connector the same as HealthCare.gov?

No. Massachusetts operates its own state-based marketplace, the Massachusetts Health Connector at MAhealthconnector.org. Massachusetts residents do not use HealthCare.gov. The Health Connector has its own application, its own deadlines (January 23 versus HealthCare.gov’s January 15), and the ConnectorCare subsidy program that HealthCare.gov states do not offer.

Can I buy short-term health insurance in Massachusetts?

No. Massachusetts does not allow the sale of short-term health insurance because state law requires all plans to follow guaranteed-issue and rating rules these plans do not meet. Short-term plans also fail Minimum Creditable Coverage standards, so they would not satisfy the individual mandate and would leave you exposed to the state tax penalty of up to $135/month. MCC-compliant Health Connector plans are the practical path to compliant coverage.

When is open enrollment for Massachusetts health insurance?

Open enrollment for 2026 coverage through the Massachusetts Health Connector ran November 1, 2025, through January 23, 2026, with a December 23 deadline for January 1 coverage. Outside open enrollment, you can enroll through a qualifying life event such as losing other coverage, getting married, having a child, or moving to a new Massachusetts county. Call 1-877-MA-ENROLL (1-877-623-6765) for help.

Massachusetts Health Insurance Resources

Explore related guides for Health Connector enrollment steps, ConnectorCare and affordable coverage strategies, carrier comparisons and rankings, individual and small group plans, and PPO options for residents who want broader provider access across the Commonwealth.

How to enroll, deadlines, and qualifying life events.

Best Plans & CarriersBCBSMA, Harvard Pilgrim, Tufts, and more — ranked and compared.

Individual & Private PlansOff-exchange and self-employed coverage options.

Small Business CoverageGroup plans for employers with 1–50 employees.

Affordable CoverageConnectorCare, subsidies, and ways to lower premiums.

PPO PlansFlexibility for specialists and out-of-network care nationwide.

Find the Right Massachusetts Health Insurance Plan

With eight carriers on the Health Connector and ConnectorCare plans that can drop premiums to $0, the right coverage depends on income, county, and household size. See every option side by side in minutes.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Massachusetts residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.